Written by: BLOCKHEAD

Translated by: Plain Language Blockchain

There is a piece of financial news that won't make the headlines, yet it has touched off a market movement over the years. It did not involve a price surge or celebrity influence, just a press release about middleware. Broadridge recently integrated Crypto.com into the NYFIX order routing network—allowing this institutional broker to route cryptocurrency orders through the same facilities they use to process equities and fixed income products. Such news seems trivial, but it hints at power within a specific context.

Because context is everything. This is not an isolated development, but a connection point around which a foundational infrastructure, regulation, and institutional capital network concerning digital assets is being built. The debate about whether cryptocurrencies belong in institutional portfolios will no longer be resolved through discussion, as the infrastructure has become a reality.

Market Infrastructure Pipeline

FIX (Financial Information Exchange Protocol) has dominated the flow of trade orders between financial institutions since 1992. It is a standardized information protocol that allows funds in London to send orders to electronic merchants in Tokyo without anyone needing to answer a phone. It is standardized, auditable, and deeply embedded in institutional operations to the extent that most large firms cannot trade without it.

Now, cryptocurrency orders can operate on the same system. The news may have limited headline significance, but as a symptom, it is highly significant—it indicates that traditional finance hasn't constructed a parallel (and undoubtedly clumsy) infrastructure for digital assets; rather, it is extending its existing infrastructure.

A Grand Edition with Important Items

The integration of Broadridge-NYFIX has an accelerating pattern:

In April 2025, Ripple acquired a major merchant through a secret route for $2.05 billion—becoming the first cryptocurrency company to own and operate a global multi-asset merchant, handling $30 trillion annually, serving over 300 institutional clients. This isn’t just a cryptocurrency company acquiring another cryptocurrency company; it's the crypto industry buying the “pipeline” that operates Wall Street.

Kraken launched an institutional-grade major business in mid-2025, offering liquidity across more than 20 global trading venues.

The derivatives trading platform regulated by the Commodity Futures Trading Commission (CFTC) and Bitnomial in Kuala Lumpur launched new U.S. crypto derivatives, accepting digital assets as collateral for the first time—meaning institutions can directly pledge Bitcoin or Ethereum and convert them into cash.

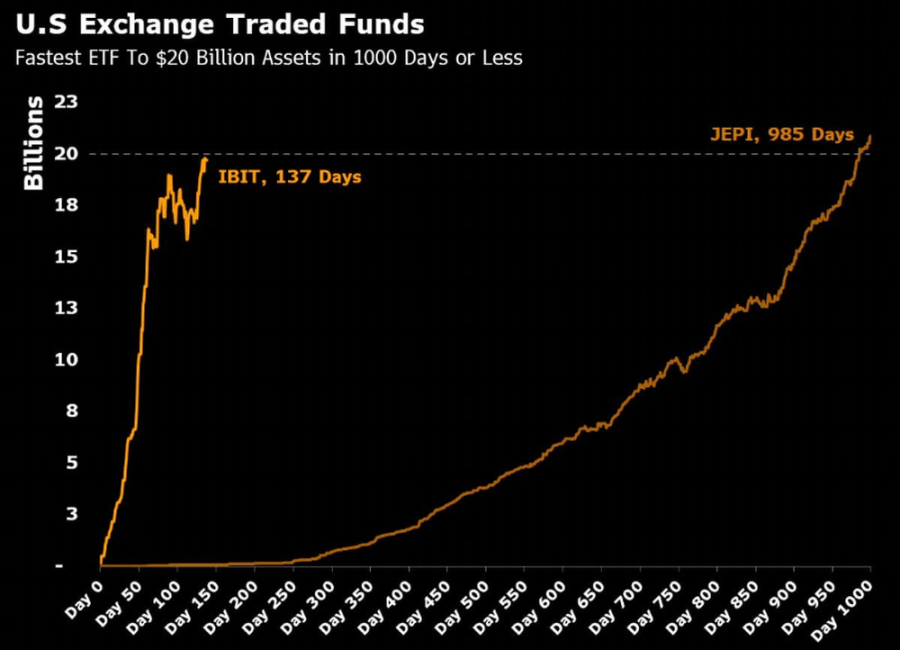

BlackRock's currency ETF (IBIT) has become the fastest-growing ETF in history. Public pension funds in Ontario, Canada, and Wisconsin have now included digital assets in their long-term holdings.

Each point is data: they collectively depict a market structure constructed by those who believe that “the legitimacy of cryptocurrencies is no longer in question.”

Those with Knives Entered the Gunfight

The past perception that institutions' concerns about cryptocurrencies stemmed from—skeptical boards, risk committees wary of Bitcoin—has always been a misdiagnosis. The real impediment is on the operational side.

Compliance teams cannot map crypto transactions to existing monitoring frameworks; risk management departments cannot obtain standardized pricing data; operational teams find that settling crypto transactions entirely requires setting up independent daily work tools, login permissions, and reconciliation processes. In large financial institutions, these flows are no small matter; they determine what is feasible and what is not.

The common goal of the current wave of infrastructure development is to eliminate these obstacles one by one. FIX connectivity, institutional-grade custody, major services… cryptocurrency is gradually no longer a “special case” but becoming a “viable option.”

It’s the “Ratchet” Effect, Simply Switchable

Institutional acceptance of new asset classes has never been a one-time event. Reflecting back on how hedge funds developed derivatives in the 1980s and 1990s: no single event triggered it; it was the gradual accumulation of legal frameworks, accounting standards, risk models, and specialized talent. Each institution establishing derivative capabilities wants later entrants to feel this path is easier and more accessible. At some point, the question is no longer whether to establish a derivatives department, but rather “how large should we scale?”

Digital assets are traveling the same path, but at a faster pace. The repeal of SAB 121 and the establishment of the U.S. Strategic Bitcoin Reserve have given this asset class the highest level of endorsement. The comprehensive effectiveness of Europe’s MiCA law, the VARA in Dubai, and the MAS in Singapore have achieved full licensing.

The two most significant developing markets in Asia are also following suit:

In Japan, the Financial Services Agency (FSA) announced a reclassification of crypto assets, shifting them from the Payment Services Act to the Financial Instruments and Exchange Act. This is based on a recognition that digital assets are currently primarily viewed as investments rather than transactional tools. The practical significance is that banks, insurance companies, and trust banks can begin treating cryptocurrencies like equities and bonds.

The Digital Asset Basic Law, serving as the parent law, covers stablecoins, digital asset ETFs, and blockchain tools in public finance. Starting from 2030, blockchain deposit tokens are expected to be used for about 25% of treasury payments, with focus set to begin in 2026.

A sovereign government routing the fiscal operation of its tax facilities through digital infrastructure is a decisive step, not a gamble. The agreement confirms the unified replacement of “virtual assets” in Korean financial law with “digital assets”—this detail reflects a significant shift in the nation’s definition of these attributes.

Japan and South Korea are both large, custodial, and heavily regulated financial markets. Their actions carry more weight than fintech centers merely offering sandbox licenses. Coupled with the U.S., EU, Singapore, and Hong Kong, almost all institutional capital in the world operates on the same basic premise: digital assets need an appropriate regulatory framework.

Individually, each development is incremental; but together, they are irreversible.

What Is All This “Building” For?

The tokenization of real-world assets (RWA) has grown by 380% in three years, reaching $25 billion, and is projected to grow to $30 trillion by 2034.

According to Coinbase’s “2025 State of Cryptocurrency Report,” 76% of institutional investors plan to allocate to tokenized assets by 2026.

Major financing of digital assets, cross-margining between crypto spot and listed futures, tokenized government bonds settled on traditional rails—none of these are speculative; they are already in production or being developed by top financial institutions whose names appear on fund offering memoranda, not token statements.

The design of the FIX protocol was originally intended not just for equities but for any financial instruments that need to be traded in a standardized, interoperable manner. Cryptocurrencies now operate on it, fulfilling the protocol's intended function, merely in the form of digital tools.

The Questions Have Changed

For a decade, the debate within institutional investment committees has been categorical: Is this asset class worthy of a spot in the investment portfolio at the summit? The defense debate has ended, not because everyone has been convinced, but because there are now enough people among the world’s largest asset allocators who have crossed this stage such that the remaining holdouts need to explain themselves.

The current question is about scaling implementation, access, risk frameworks, and custody arrangements. This is a completely different conversation—once pension funds, sovereign wealth funds, and major brokers begin discussing an asset class using these terms, the direction of developments is often quite predictable.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。