Written by: Yokiiiya

After the recent financial report released by Circle, the stock price has noticeably risen again, leading to a surge in market attention. However, rather than focusing on short-term fluctuations, I am more interested in reviewing a more intriguing topic: what has Circle been doing in the 9 months since going public? How has its stock price fluctuated? More importantly, what key actions has it advanced in terms of product capability, network structure, and financial infrastructure? When you look at these changes collectively, you may find that Circle's goals are likely no longer just about "issuing stablecoins" in a simple sense.

Next, we can first briefly review the changes in Circle's stock price and market value over the past few months, and then examine what key layouts it has advanced in product and network dimensions behind these market fluctuations.

1. Changes in Stock Price and Market Expectations After Going Public

If we only look at the market performance over the past few months, Circle's stock price trajectory is quite representative: it has almost completely gone through a process of “narrative expectation—emotional decline—fundamental verification—re-pricing”. In the early stages after going public, the market's perception of Circle was still very simplistic: a stablecoin issuing company.

Circle's core asset is USDC. In the eyes of many investors at that time, the most direct profit model for the company was: users exchange dollars for USDC, with Circle investing the reserve funds in short-term U.S. Treasury securities, and the interest spread becomes the primary source of income. In a high-interest-rate environment, this model is indeed very profitable. However, it also brings a significant issue: the company's profitability is highly dependent on the macro interest rate cycle.

Thus, in the initial stage after going public, the market's pricing logic for Circle was more akin to that of: a money fund management company or an interest-dependent stablecoin issuer, rather than a financial infrastructure company.

As time passed, the market began to gradually realize two changes.

First, the stablecoin market is rapidly expanding. As the world's second-largest dollar stablecoin, USDC's circulating scale and transaction volume continue to grow, providing Circle with a certain scale elasticity in its revenue base.

Second, Circle's strategic narrative is changing. The company is placing less emphasis on “stablecoin issuance” and more on: a global payment network, developer APIs, and stablecoin settlement infrastructure. In other words, Circle is attempting to transform USDC from a product into a network. It was only after this narrative began to be understood by the market that Circle's stock price started to exhibit new upward potential.

If in the early stages post-IPO, the market's valuation logic for Circle was “stablecoin issuer,” then in recent quarters, more and more investors have begun to try to understand this company from another perspective: whether it has the opportunity to become a provider of financial infrastructure in the era of stablecoins. To answer this question, we need to look at what Circle has truly done in the past 9 months.

2. 9 Months Post-Listing: Key Actions Taken by Circle

If we only look at the stock price, it is easy to consider Circle a stablecoin company. However, if we organize the product actions post-listing along a timeline, we discover another fact: Circle is continually enhancing the infrastructure layer of the stablecoin network.

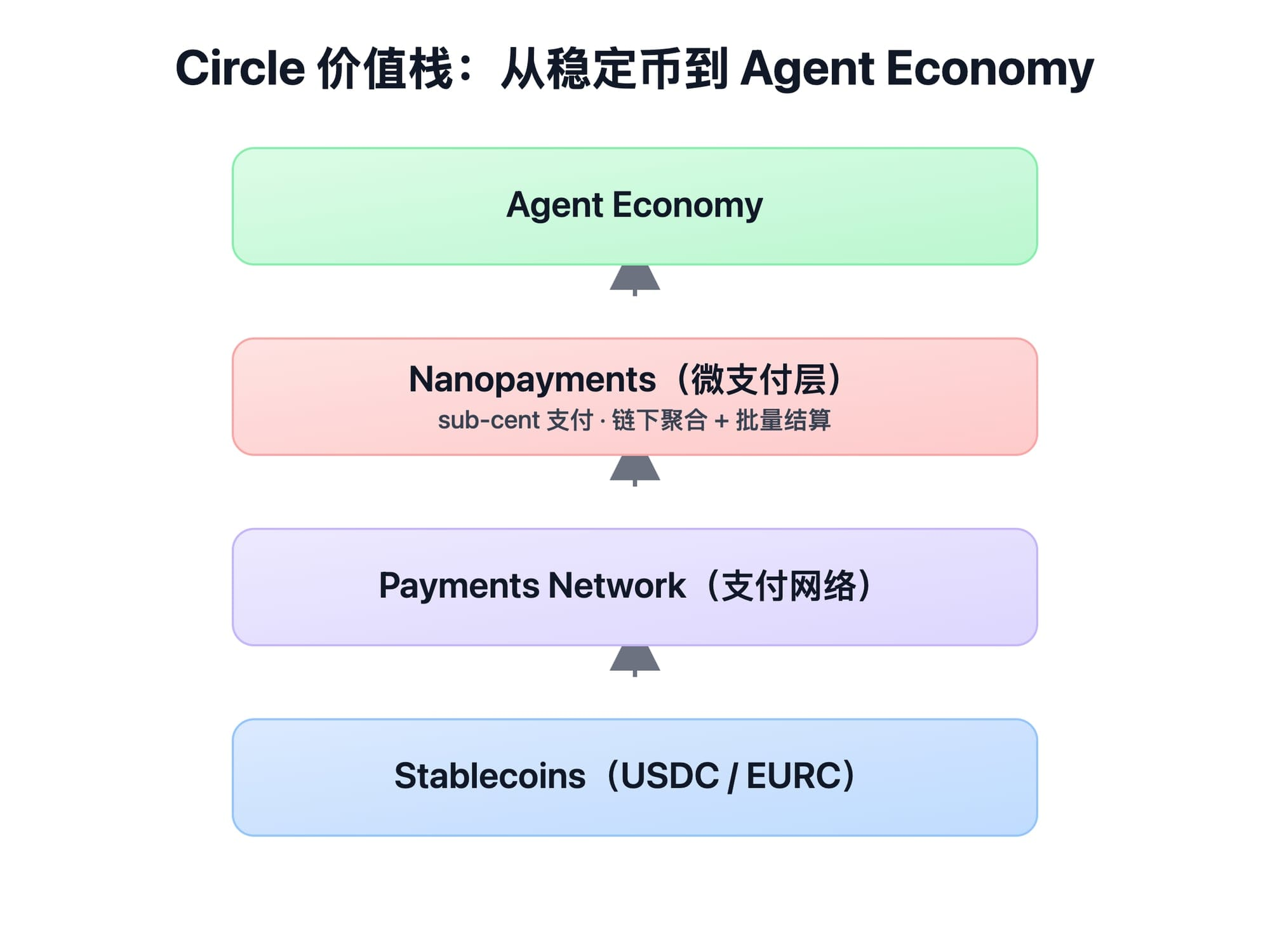

In the past 9 months, Circle has consistently advanced in aspects such as payment networks, developer platforms, cross-chain capabilities, and micropayments, with a very clear overall path: it is not merely creating a stablecoin product, but is building a complete financial technology stack (financial stack) around stablecoins.

At the foundational level is the stablecoin itself, such as USDC, which provides a blockchain-based dollar asset. Above this layer, Circle is building payment networks, such as the Circle Payments Network, to enable stablecoins to be used in cross-border settlements and capital flows. Moving up another level are the developer infrastructure components, including APIs, wallet capabilities, and cross-chain tools, allowing internet products to more easily integrate into the stablecoin system. The recently launched Nanopayments is beginning to address a new question: how will payments be completed between numerous AI agents in future economic activities?

Traditional payment systems are designed for humans, but transactions between machines often share three characteristics: high frequency, very small amounts, and automatic execution. The goal of Nanopayments is to enable stablecoins to support transactions at the level of one-millionth of a dollar, reducing costs through off-chain aggregation and batch on-chain settlement.

If stablecoins solve the problem of “on-chain dollars,” then Nanopayments attempts to solve the problem of “payments between machines.”

From this perspective, what Circle is doing is no longer merely issuing stablecoins, but rather attempting to construct a network of financial infrastructure operating around stablecoins.

3. What Circle Really Wants to Escape Is the Identity of "A Token Issuer Making Money by Interest Spread"

If we continue to view Circle as a stablecoin issuing company, its valuation anchor is actually very singular: interest rates, reserve income, and stablecoin scale. The logic of this model is quite simple. Users exchange dollars for USDC, and the issuer holds these dollar reserves, investing the funds in short-term U.S. Treasury securities and other assets to earn interest revenue. In an environment of high global interest rates, this model can indeed generate substantial cash flow.

But the issues are equally clear: this revenue structure is highly sensitive to the macro interest rate cycle. Once interest rates decline, the income from stablecoin reserves will also decrease accordingly. Therefore, if a company's business model primarily relies on stablecoin reserve interest, it can be easily perceived by the capital market as a interest-driven financial company. This is precisely the market perception that Circle has been trying to change.

In the past 9 months, Circle's most significant change has not been the launch of a specific product, but rather gradually establishing a new capability: network capability. When a company's role shifts from "issuing an asset" to "organizing the flow of funds in a network," its source of value will also change accordingly. This change is reflected in at least three aspects.

First, the revenue logic shifts from "spread-driven" to "network-driven."

In the traditional stablecoin model, revenue primarily comes from the interest income of reserve assets, essentially relying on the macro interest rate environment. However, as the payment network and developer ecosystem gradually take shape, the company's value will increasingly derive from the usage depth of the network itself, such as payment traffic, settlement scale, and developer access. The former is closer to cyclical variables, while the latter is closer to structural variables.

Second, the competition dimension shifts from "who issues the most" to "who connects the deepest."

Stablecoins themselves are not difficult to replicate, but the settlement networks formed around stablecoins, cross-chain liquidity routing, and developer ecosystems require long-term accumulation. Once a large amount of capital flow and application scenarios operate on a particular network, new competitors, even if they issue similar assets, will find it hard to replicate such network effects in a short time. Therefore, the long-term moat may not lie in the tokens themselves, but in network organizational capabilities.

Third, the valuation framework shifts from "financial product company" to "financial infrastructure company."

Valuation of financial product companies typically revolves around the income capabilities of a single product; however, the value of financial infrastructure companies derives more from network effects, standardization capabilities, and the interface positions within the entire system. This is also why more and more investors are beginning to discuss Circle's upper limits: its growth potential may no longer be solely dictated by interest rates.

From this perspective, Circle's recent series of moves are not isolated events, but rather a continuous amplification towards the same direction—transforming stablecoins from a product into a network; thereafter advancing this network into the financial infrastructure of the digital economy. What truly deserves tracking is not how the stock price will move after the next financial report, but whether Circle can secure the position of “default settlement layer.”

4. From Stablecoin Network to Agent Payments: Circle's Next Step

If we move the timeline forward a bit, we find that some of Circle's recent actions are not only about expanding the payment network, but are also attempting to answer a longer-term question: what should the payment system look like when more and more economic activities are completed automatically by software? In the era of traditional internet, most transactions are initiated by humans.

Whether it’s card networks, bank transfers, or e-wallets, these systems are essentially designed around the behaviors of “human users.” However, with the emergence of AI agents, the participants in economic activities are changing.

An increasing number of tasks are being executed by automated programs, such as data purchases, API calls, resource scheduling, and various digital service transactions. These behaviors often share several common characteristics:

Higher transaction frequency

Smaller single amounts

Payments triggered automatically by programs

In such scenarios, the cost structure and processing methods of traditional payment networks are hard to adapt. This is precisely the background for Circle’s recent launch of the Nanopayments testing network. The goal of this system is to support extremely low-value payment transactions, even reaching the level of one-millionth of a dollar. Through off-chain transaction aggregation + batch on-chain settlement, Circle attempts to enable stablecoins to support large-scale micropayment scenarios. If this model can stand, the role of stablecoins will also change. In the past, stablecoins were mainly used for capital flows in exchanges and cryptocurrency market settlements; in the future, they might become a settlement unit between machines. From this perspective, Circle's recent series of layouts are pointing in the same direction: stablecoins are not only a digital asset; they might also become a payment primitive in the future digital economy. If the stablecoin network can support high-frequency, low-cost, automated transactions, then its application range will no longer be limited to the cryptocurrency market, but potentially expand into a broader internet economy.

This also explains why Circle has been emphasizing a larger vision while building payment networks, developer platforms, and micropayment infrastructure: to create an Internet Financial System.

If this system gradually takes shape, the significance of the stablecoin network will also change. It will no longer just be an asset form in the cryptocurrency market but might become a financial underlying protocol in the digital economy.

At that time, the ultimate competition in stablecoins might no longer be about "who has issued more tokens," but rather who can occupy the default settlement layer in the digital economy.

5. In the Next 12 Months, Understanding Circle's Three Key Metrics

At this point, the real question is not about the narrative but about validation. In the next 12 months, if you want to determine whether Circle is truly transitioning to financial infrastructure, you can focus on three key metrics.

First, regulatory enforceability: whether the rules can truly be implemented.

The policy framework in the stablecoin industry is gradually becoming clearer, but "having a framework" does not mean "enforceable." What truly matters is: whether the regulatory rules in different regions can connect, whether institutions are willing to continue engaging under the new framework, and whether compliance costs are controllable. If regulation only remains at the principle level, the expansion speed of the stablecoin network will likely be limited; however, if it enters the enforceable phase, Circle's path into the institutional market may significantly accelerate.

Second, network usage depth: not the number of collaborations, but the actual settlement flow.

To judge Circle's development, one cannot only look at partnership announcements but must also observe whether these collaborations translate into sustained capital flows and settlement scales. For example: cross-border payments, business settlements, developer access. Whether these scenarios move from "pilot" to "normalized usage." For infrastructure companies, the most important indicator has never been how many partnerships signed, but rather how many times the network has been used.

Third, income structure migration: whether it can transition from interest-driven to network-driven.

If future income still predominantly relies on interest from stablecoin reserves, Circle's valuation will remain highly tied to interest rate cycles. However, if payment networks, developer capabilities, and settlement services begin to contribute a higher proportion of income, the market is more likely to value this company according to financial infrastructure logic. This will determine Circle's valuation ceiling, whether to stay within the range of a cyclical financial company or enter the domain of network-type financial infrastructure companies.

What has been most noteworthy about Circle in the past 9 months is not the stock price fluctuations after a financial report, but that it is completing an identity transformation: from "a company issuing stablecoins," to "the financial infrastructure layer of the stablecoin era."

If this path holds, it will rewrite not only its valuation logic but also the default settlement method within the digital economy.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。