In the third chapter of the "previous article", we focused on analyzing projects like Synthetix, Gains Network, and Ostium. This article will build on the previous text and further expand to include other representative cases.

Three, Representative Projects and Structural Game: Oracle Pricing + Pool-based vs. Order Book

3.3 Orderbook Representative: Hyperliquid HIP-3 Ecosystem

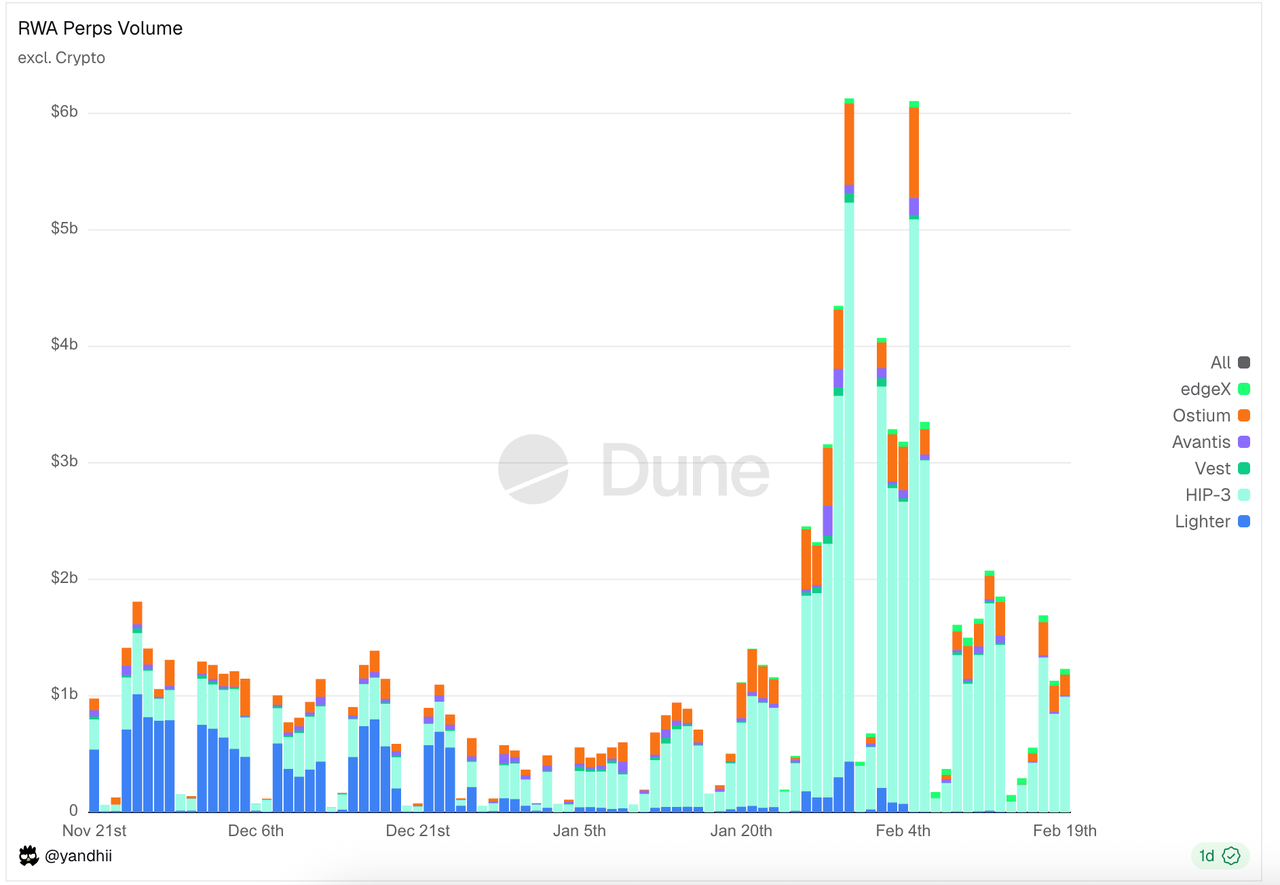

In the order book sector, the Hyperliquid HIP-3 ecosystem accounts for the vast majority of trading volume and positions. Outside of the Hyperliquid ecosystem, platforms such as Lighter and Vest Markets have also initiated competition.

Data Source: https://dune.com/yandhii/rwa-perps

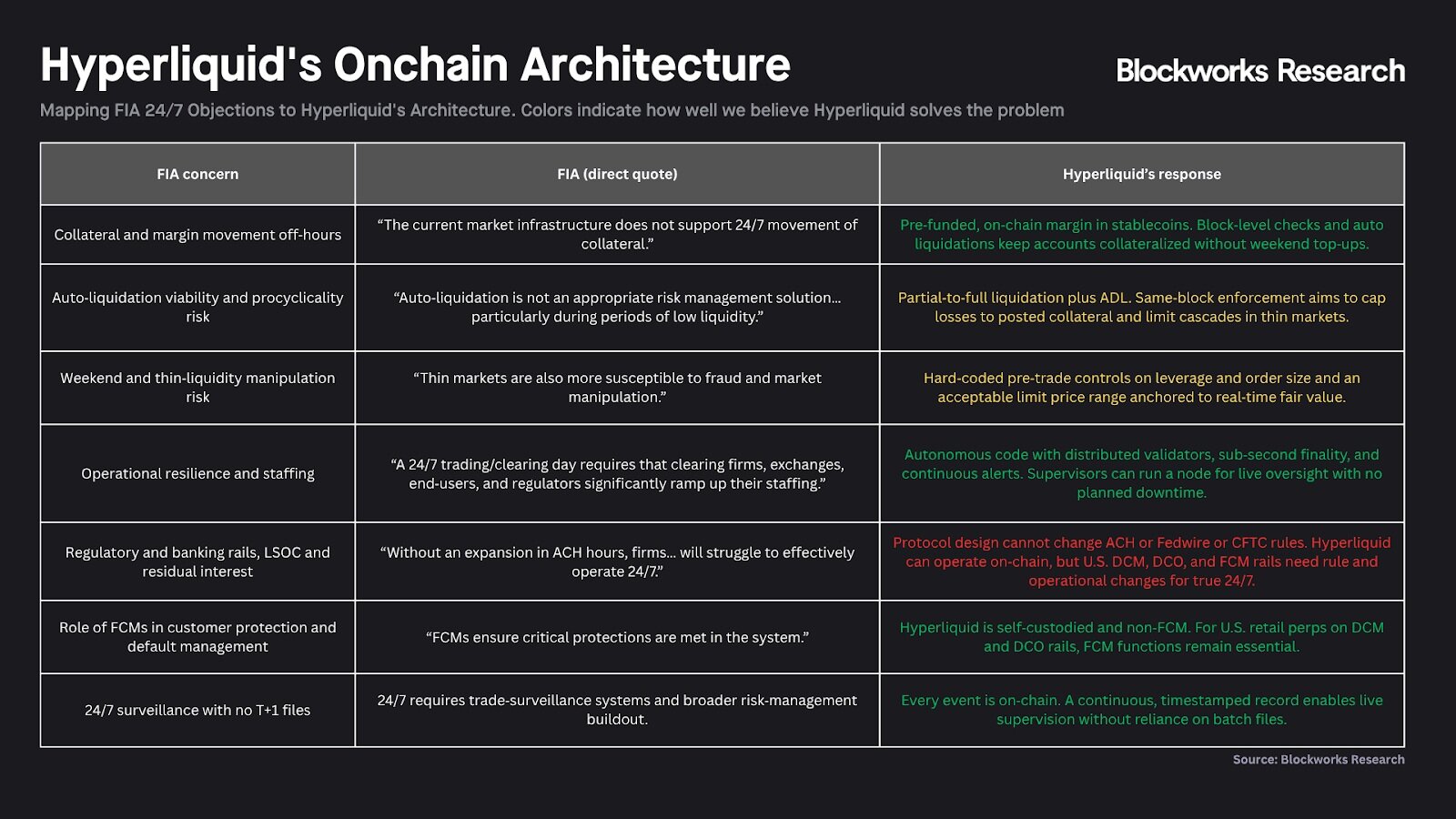

Hyperliquid & HIP-3: Decentralized Nasdaq Infrastructure

Hyperliquid has completed a strategic transformation from a single perpetual contract exchange to a "high-performance clearing and matching infrastructure layer" through HIP-3 upgrades. Its core vision is to split the functions of DCM (Designated Contract Market) and DCO (Derivatives Clearing Organization) from traditional finance on-chain. Under this structure, the Hyperliquid chain itself plays a unified DCO role, providing the underlying matching engine, risk control, and fund settlement; while third-party teams act as "deployers," assuming the DCM role by responsible for front-end customer acquisition, market operations, and asset listings. This layered design aims to create a "decentralized Nasdaq," facilitating perpetual trading of various assets through a unified settlement layer.

Figure: The above image summarizes how Hyperliquid hopes to become "a more open, transparent, and efficient financial system" in response to the CFTC's concerns about perpetual contracts and around-the-clock trading.Response to the CFTC's concerns about perpetual contracts and around-the-clock trading. For example: through a 24/7 automatic clearing protocol that replaces traditional DCO's reliance on the banking system, utilizing non-custodial technology to eliminate bloated FCM intermediaries, and reconstructing DCM's regulatory logic with real-time on-chain data, it highlights how blockchain technology can directly overcome the physical time differences and efficiency bottlenecks of traditional finance.

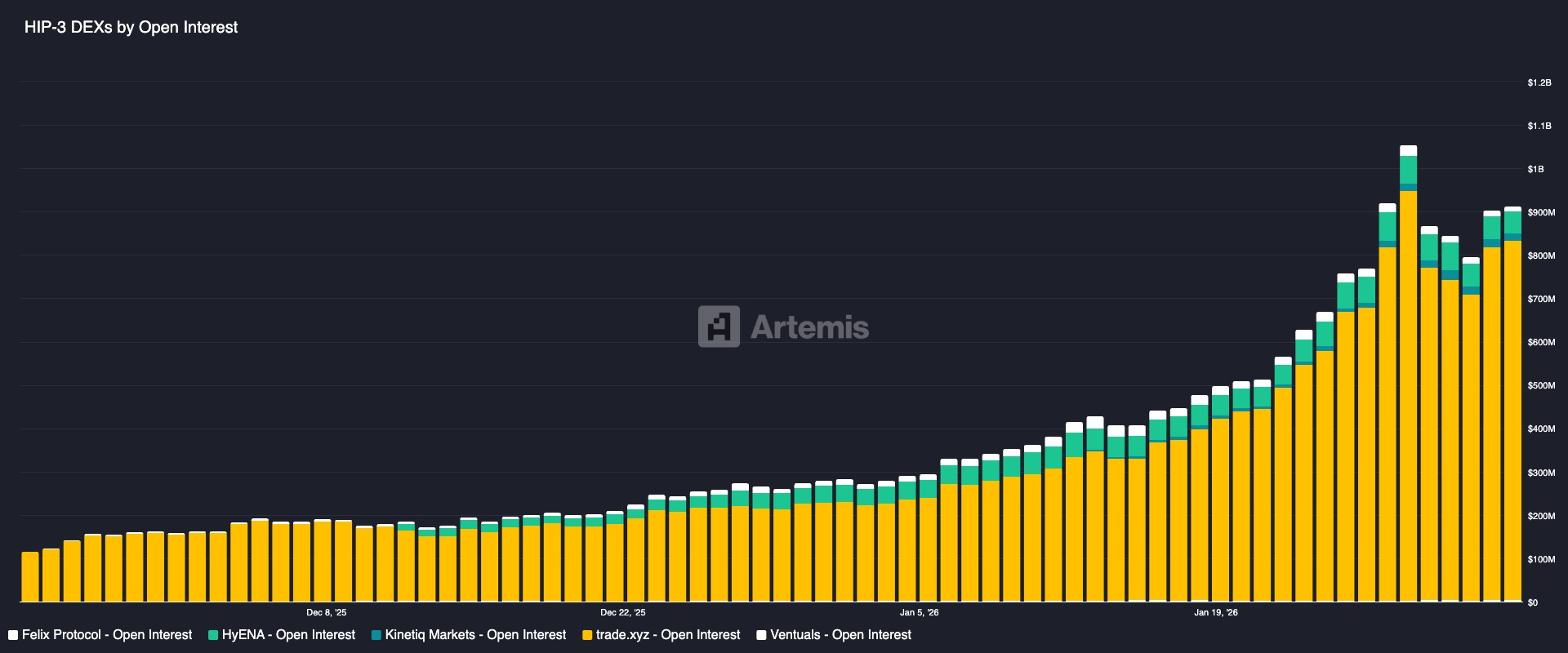

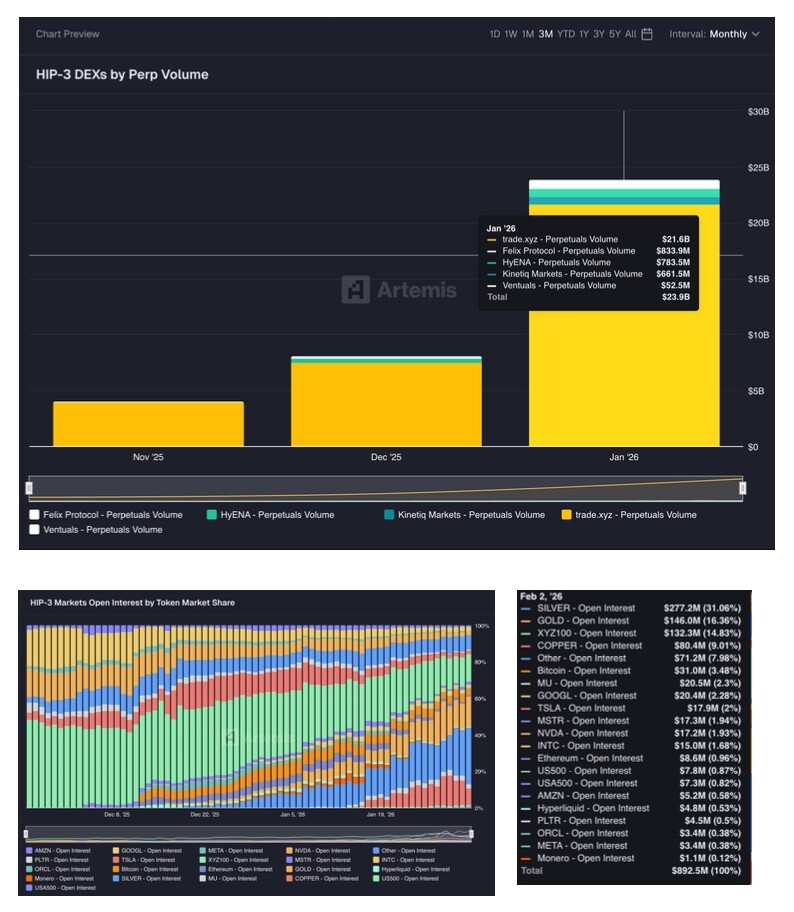

HIP-3 Ecosystem RWA Perps Project

Project Overview

- Trade.xyz is developed by HyperUnit, the asset layer team officially collaborating with Hyperliquid, and was the first to launch the XYZ100 perpetual contract tracking the Nasdaq 100 index along with several leading US tech stocks. With rich asset bridging (supporting liquidity injection for mainstream assets like BTC, ETH, and SOL through HyperUnit), Trade.xyz currently leads in trading volume among all HIP-3 perpetual exchanges, contributing about 90% of the market transaction volume.

- Markets.xyz is launched by the Kinetiq team of the Liquid Staking project on Hyperliquid, focusing on indices and launching various index/macroeconomic perpetual contracts (including S&P 500, US Tech Index, Euro, US Treasury Index, Energy Index, etc.). Another difference is that it uses USDH as the margin denomination currency, significantly reducing trading fees and increasing rebates, competing with Trade through cost advantages (USDH is the native stablecoin issued by the Native Markets team, which has implemented fee reduction and rebate activities to compete with cross-chain asset projects).

- Felix initially started as a lending and stablecoin protocol for Hyperliquid, issuing synthetic dollars feUSD through CDP and providing a "Felix Vanilla" matching lending market. Following the launch of HIP-3, Felix expanded its business map, becoming one of the deployers in the HIP-3 perpetual market. Felix's settlement currency also uses the USDH stablecoin.

- Dreamcash is a mobile trading terminal for RWA perpetual contracts developed by Beam.

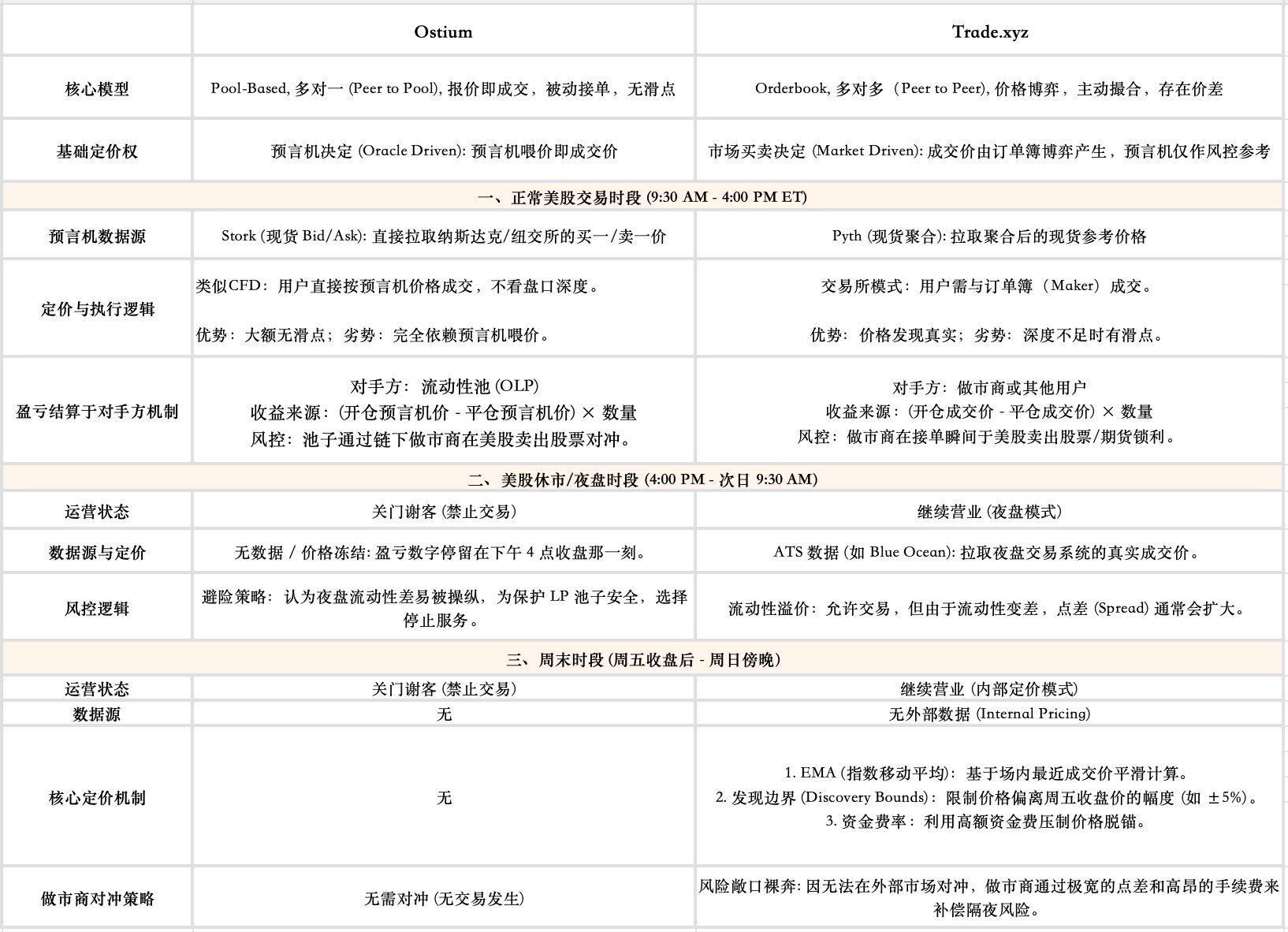

Core Pricing Mechanism: Market-driven Pricing + Oracle Risk Control

The core technical challenge of the 24/7 RWA Perps project built based on the Orderbook model is how to provide a fair and robust pricing even during the market closure of the underlying assets. Taking Trade, the leading project in the HIP-3 ecosystem in this field, as an example, its core design is based on a dual-track mechanism of market pricing and oracle risk control.

- Core of Price Discovery: Determined by the market rather than the oracle

Unlike the Pool-based model that directly uses oracle quotes as the transaction price, Trade's transaction price is entirely generated by the interaction between buyers and sellers on its order book. The oracle does not play the role of "price setter" but acts as an "umpire," with the prices it provides primarily used for risk control.

- Marked Price: Used to calculate users' position gains and losses and determine forced liquidation

The system's profit and loss calculations, funding rate, and forced liquidation do not use instantaneous transaction prices but rely on a more robust marked price. Trade's marked price is generated by taking the median of the following three components: oracle price, long-term deviation from the average, and immediate order book price. This design aims to smooth out market noise and prevent malicious manipulation, ensuring that users’ accounts are not wrongly liquidated due to price crashes on the order book.

- Oracle Data Source Switching During Full Trading Hours: To achieve around-the-clock operation, the oracle's data source seamlessly switches according to US stock trading hours: during normal trading hours it references external oracles like Pyth; during nighttime trading, it references the night trading prices provided by ATS (Alternative Trading Systems, like Blue Ocean); and during weekends, it activates an internal pricing model.

3.4 Ostium vs Trade Pricing Logic and Oracle Role Comparison

Ostium opted for greater safety and price accuracy, sacrificing some availability (not available on weekends). Trade opted for availability and gamification, sacrificing some price stability (potentially decoupling or having significant fluctuations in funding rates over the weekend). The role of the oracle also differs significantly between these two project models, in Ostium’s Pool-based model, the oracle acts as a price setter (determining trades), while in Trade the oracle is an umpire (only affects funding rates and is responsible for deciding forced liquidations, regardless of how trades occur)

Chapter Four RWA Perps Regulatory Limitation Analysis

4.1 Core Logic of US Derivatives Regulation: Classification of Underlying Assets Determines Compliance Path

In the US financial regulatory system, the first step in determining whether a derivative can be listed and how it can be listed is to ascertain the legal attributes of its underlying assets, which directly decides the jurisdiction of regulatory oversight and, subsequently, the type of licenses that the exchange must acquire.

For commodities such as gold, silver, foreign exchange (FX), and Bitcoin, US law defines them as "commodities." Therefore, perpetual contracts based on such assets fall under the category of commodity futures, with a relatively straightforward and clear regulatory path: they are entirely within the jurisdiction of the Commodity Futures Trading Commission (CFTC). Exchanges only need to register as Designated Contract Markets (DCM) and connect with Derivatives Clearing Organizations (DCO) to conduct business.

However, once the underlying asset of the perpetual contract changes to a single stock or a narrow-based index, the situation fundamentally changes: derivatives involving a single security or a small basket of securities must simultaneously comply with the joint regulation of the SEC and CFTC.

The requirement to simultaneously accept the joint regulation of the SEC and CFTC is the primary reason why compliant stock perpetual contracts are still absent in the current US market. The background of this regulatory clause traces back to a regulatory turf war between the SEC and CFTC in the 1980s: at that time, the SEC and CFTC contested the regulatory authority over newly emerging stock futures contracts, culminating in the "Shad-Johnson Agreement" signed in 1982, which directly prohibited the trading of single stock futures and narrow-based stock index futures on US exchanges in an almost "one-size-fits-all" manner, with the intention of avoiding further friction between institutions. Although the Commodity Futures Modernization Act of 2000 (CFMA) revised this ban, allowing such contracts to be traded in the market as "security futures products," the accompanying conditions were exceedingly stringent: the product must simultaneously accept dual regulation by the SEC and CFTC, which has become a fundamental legal barrier to innovation in equity derivatives.

Any platform wishing to offer stock perpetual contracts to US retail customers must not only hold a single license but must also complete the following two registrations:

- Register with the CFTC as a Designated Contract Market (DCM) or Swap Execution Facility (SEF)

- Register with the SEC as a National Securities Exchange

This means the platform must satisfy two sets of compliance standards set by different institutions, which may conflict in areas such as margin calculation, information disclosure, and trade reporting. Such high compliance thresholds and operational costs effectively constitute a "barrier to entry" for single stock perpetual contracts, leading to the current absence of compliant retail products of this kind in the US.

4.2 Structural Conflicts of Exchanges: Why Compliance Migration Costs are Extremely High

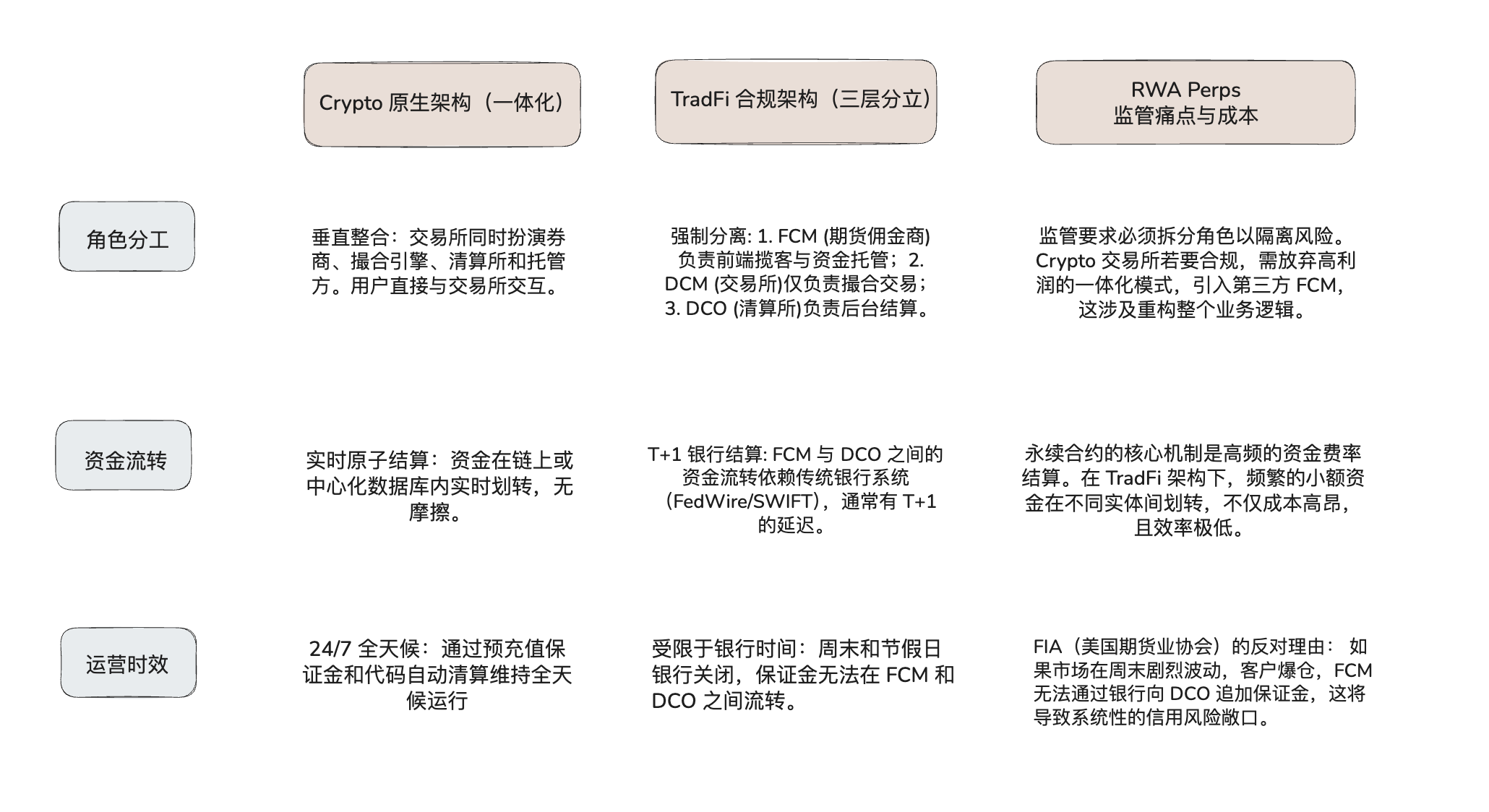

If exchanges in the US, such as Coinbase and Robinhood, genuinely wish to launch Equity Perps products, they must confront not only the difficulties of obtaining the legal licenses discussed above but also face structural conflicts in underlying infrastructures.

Cryptocurrency exchanges generally adopt a "vertically integrated" architecture, while US regulatory requirements mandate a risk isolation-based "three-tier separation" architecture. If crypto exchanges wish to achieve compliance, they must disassemble their existing efficient tech stacks to accommodate traditional financial clearing processes.

Comparative Analysis of Crypto and TradFi Market Structures:

Thus, for US exchanges to launch Equity Perps, they not only need to resolve the "dual license" legal issues but also address the physical contradictions between "24/7 trading demands" and "non-24/7 banking settlement systems." This mismatch in infrastructure is currently the largest bottleneck.

4.3 Opportunity Window for Offshore Markets: Regulation S

Due to the short-term difficulty of breaking through domestic regulatory restrictions in the US, the vast majority of stock perpetual contract liquidity has been squeezed into offshore markets. Offshore exchanges (serving non-US clients) typically rely on compliance exemptions based on Regulation S in US securities law. The core logic of this regulation is that as long as the issuance and sale of securities products occur entirely outside the US, and the issuer does not conduct Directed Selling Efforts towards US persons, registration with the SEC is not required. This necessitates that platforms strictly implement geographic barriers to block US IPs and explicitly prohibit US users in their legal terms.

In this context, RWA Perps Dex is encountering a unique market window. They have the opportunity to establish a reciprocal commercial distribution model by collaborating with traditional long-tail brokers in offshore regions:

CFD Broker + RWA Perps Dex Reciprocal Model: This collaboration may be attractive to traditional brokers, as their traditional CFD business faces increasingly tightening regulations (such as EU ESMA leverage restrictions), while on-chain perpetual contracts often exist in a regulatory blind spot, allowing for higher leverage. More importantly, brokers only need to maintain front-end customer relationships while outsourcing complex margin management, clearing, and hedging risks to on-chain protocols (back-end), significantly reducing their middle and back-office operational costs. Additionally, the DEX's self-custody attributes address user trust issues regarding fund misappropriation by small to mid-sized brokers.

For Equity Perps Dex, this model resolves the most challenging customer acquisition issue. Crypto-native users have relatively limited interest in trading US stocks, while traditional brokers hold a large volume of real retail traffic seeking exposure to US stocks. By embedding as a technical back-end within brokers, the DEX can maintain technological neutrality while compliant brokers handle KYC/AML processes at the front end, thus having the opportunity to scale up beyond the original DeFi world.

4.4 Potential Legal Risks

Despite the business logic of offshore and DeFi models being sound, it is also essential to be wary of the "long-arm jurisdiction" risk posed by US regulatory agencies. If offshore protocols cannot completely sever ties with US users at both the technical and compliance levels (for example, through front-end scrutiny or IP blocking), or if their business activities are deemed to involve the US market, they will still face severe regulatory penalties.

Chapter Five External Variables: Dual Impact of NYSE 24/7 Plan

The news that ICE, the parent company of the New York Stock Exchange (NYSE), plans to launch a 24/7 trading market constitutes the largest external variable for the RWA perpetual contract sector. If this transformation materializes, it will have profound dual impacts on DeFi. If users can legally and safely trade Tesla stock around the clock on regulated exchanges like the NYSE or Interactive Brokers, the "around-the-clock trading" advantage that DeFi relies on may be somewhat affected. At that point, DeFi may need to seek new value propositions such as higher leverage, permissionless access mechanisms, or complex financial products built on composability to survive in direct conflict with traditional financial giants.

Core Motivations and Mechanism Innovations: Moving from "T+2" to "On-Chain 24/7"

The NYSE’s planned 24/7 trading platform aims to utilize blockchain technology for the tokenization of US stocks and ETFs. Its core innovation lies in using stablecoins for deposit, instant clearing and settlement (T+0), and multi-chain custody, completely breaking the traditional market’s "separation of trading and settlement," thereby eliminating the settlement risks exposed in events like GameStop. This move is NYSE's strategic defense response to competition from Nasdaq and others, satisfying the global capital demand for around-the-clock liquidity, marking an evolution of traditional exchanges from "electronic order books" to "fully on-chain infrastructure," attempting to integrate the efficiency advantages of DeFi under the highest regulatory standards.

Catalyst and Challenges for the RWA Ecosystem: Ending the Liquidity Bottleneck

The NYSE’s entry provides top-tier endorsement for RWA tokenization, resolving the "liquidity exhaustion" and "pricing discontinuity" issues caused by traditional markets shutting down over weekends. For the RWA perpetual contract market, the 24/7 spot price flow will significantly lower arbitrage costs and funding rate fluctuations, enhancing market depth. While the compliance "walled garden" model of the NYSE may squeeze the survival space of some non-compliant, synthetic asset-type projects, it also clarifies the direction for compliant stablecoins and clearing facilities. Crypto-native RWA projects need to leverage the window period before 2026 to create differentiation (such as high leverage, no threshold, cross-protocol interoperability) in order to form complementary or competitive relations with traditional giants.

Future Landscape Outlook: Deep Integration of Traditional and Crypto Finance

Although there is controversy within the crypto community regarding the investment pressure and regulatory surveillance brought by "24/7 constant monitoring," the trend of financial on-chain is irreversible. In the medium to long term, the involvement of traditional giants will reshape the value chain, forcing brokers, custodians, and other intermediaries to transform. In the future, the market will evolve into an ecology of coexistence and competition: compliant platforms like the NYSE will provide highly credible underlying spot liquidity, while DeFi protocols will continue to exhibit flexibility in innovative derivatives and global asset allocation. As the lines between crypto and traditional assets blur, the global capital markets will enter an entirely new era driven by AI, real-time pricing, and atomic settlements.

Conclusion

- Structural Upgrade in the Demand for Delta One (Linear Derivatives). Currently, retail traders often rely on inefficient trading tools for directional leverage. The US 0DTE (zero days to expiration options) exposes pure directional bets to unnecessary Theta (time value) decay; meanwhile, the offshore CFD (contract for difference) market, valued at $30 trillion, poses issues like lack of transparency in broker mechanisms and counterparty risk. RWA perpetual contracts strip away time decay and centralized risks, providing a transparent, mathematically linear on-chain alternative for this real market demand.

- Architectural Trade-offs in Asynchronous Markets. Connecting 24/7 crypto infrastructure with traditional markets constrained by physical trading hours forces protocols to compromise between high leverage, continuous trading, and risk externalization. To address the closure of traditional markets, two distinct models have evolved: Ostium’s actively hedged liquidity pool prioritizes solvency by suspending trades during market closures to entirely eliminate gap risk, while Trade.xyz (based on Hyperliquid) transforms weekend volatility risks into dynamic funding rates and market maker spreads, thus maintaining 24/7 uninterrupted trading.

- Offshore Distribution Strategy. Given the dual jurisdiction of SEC and CFTC, launching compliant retail stock perpetual contracts domestically in the US is currently unrealistic. Therefore, the early core growth engine for RWA Perps will rely on offshore markets (through Regulation S exemption clauses). In terms of distribution, RWA Perps Dex may explore a model of cooperation with traditional CFD brokers, not needing to acquire retail customers directly at the front end but acting as the "back-end clearing engine" for regional offshore brokers—outsourcing KYC and customer acquisition to traditional financial entities, while itself focusing on margin management and atomic settlements on-chain.

- Adapting Traditional Financial Infrastructure to 24/7. Traditional institutions such as the NYSE are advancing continuous trading plans for US stocks, which may soon break DeFi's monopoly advantage in "around-the-clock trading." Although this change can completely eliminate weekend gap risks for on-chain protocols, it also forces DeFi to diversify competitive strategies. In the long run, RWA perpetual contracts must establish differentiated advantages in areas such as permissionless access, capital efficiency, and higher leverage to evolve into a "high-speed execution layer" built on regulated traditional spot markets.

Looking to the future, RWA Perps is not merely a shadow market benchmarking against Nasdaq or CME; it is a fundamental reconstruction regarding pricing power, liquidity global distribution, and risk transfer mechanisms. As liquidity facilities continue to improve, it will become the best carrier for global leverage demand flowing on-chain.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。