Original author: Long Yue

Original source: Wall Street Insights

The IEA announced the largest-ever release of strategic oil reserves, but the market quickly realized that what truly determines oil prices is not "how much is in reserve," but "how much can be released each day."

According to CCTV News, the International Energy Agency (IEA) announced on the 11th that 32 member countries have agreed to release 400 million barrels of strategic oil reserves.

In terms of numbers, this is the largest collective release action in the history of the IEA. After the Russia-Ukraine conflict in 2022, IEA member countries released a total of about 183 million barrels in two actions, while this latest scale has directly doubled. According to reports, many countries have now disclosed their respective contributions:

- United States: 172 million barrels

- Japan: about 80 million barrels

- South Korea: 22.5 million barrels

- Germany: about 19.5 million barrels

- France: up to 14.5 million barrels

- United Kingdom: 13.5 million barrels

(Image: Reserve volumes of IEA member countries)

However, for the energy market, the truly critical information has yet to be disclosed—including the pace of release, duration, and the ratio of crude oil to refined oil. These details are often more important than the total volume itself.

At the same time, the U.S. release of reserves faces significant delays. When the U.S. president issues the release order, the Department of Energy needs about 13 days to bid, award contracts, and begin deliveries. Subsequently, crude oil must be transported via pipelines or tankers to refineries and end consumers. Even if immediate action is taken, reserves will not genuinely enter the market until the end of March at the earliest.

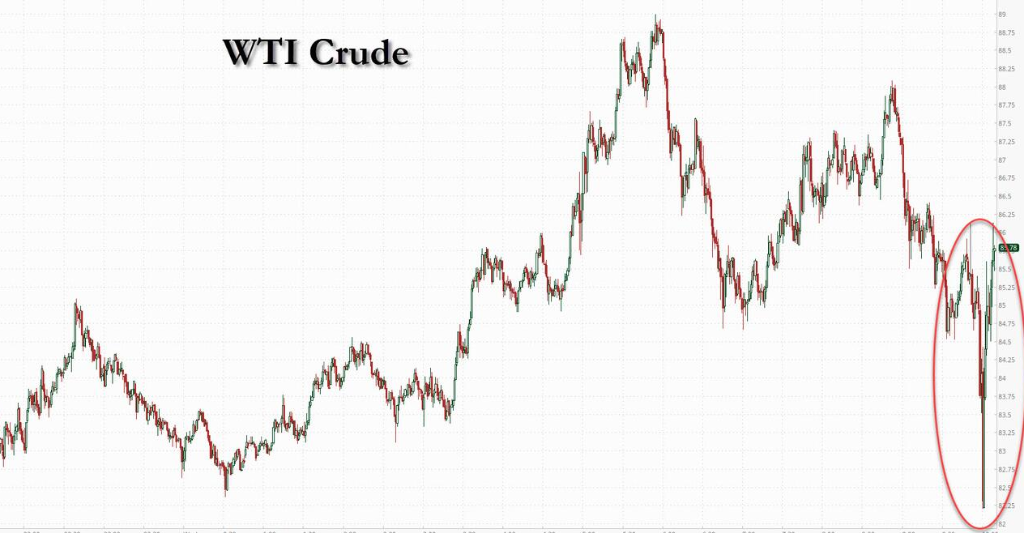

From the market response perspective, traders are clearly also waiting for this information. After the announcement, oil prices briefly fell to around $83, but quickly rebounded, with WTI crude returning to above $90.

The Real Issue: It's Not Inventory, But Supply "Flow"

To understand why the market is indifferent to the release of 400 million barrels, one must clarify the essential distinction between "stock" and "flow." The anchor for pricing in the commodity market is the actual supply and demand of spot deliveries occurring every day, rather than a static inventory figure.

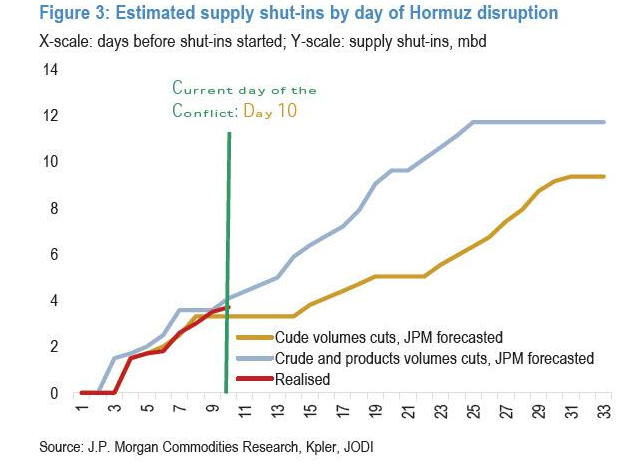

The backdrop for the current surge in oil prices is that shipping through the Strait of Hormuz has nearly halted.

This strait carries about 20% of global oil transportation. As the war escalates, a large amount of crude oil from the Persian Gulf is unable to be exported normally.

Data from Citigroup and JPMorgan shows that the blockade of the strait has led to a daily actual loss of 11 to 16 million barrels of crude oil supply globally. In other words, the global oil market has suddenly lost a supply source close to Saudi production levels.

Therefore, the core issue is not whether there is oil globally.

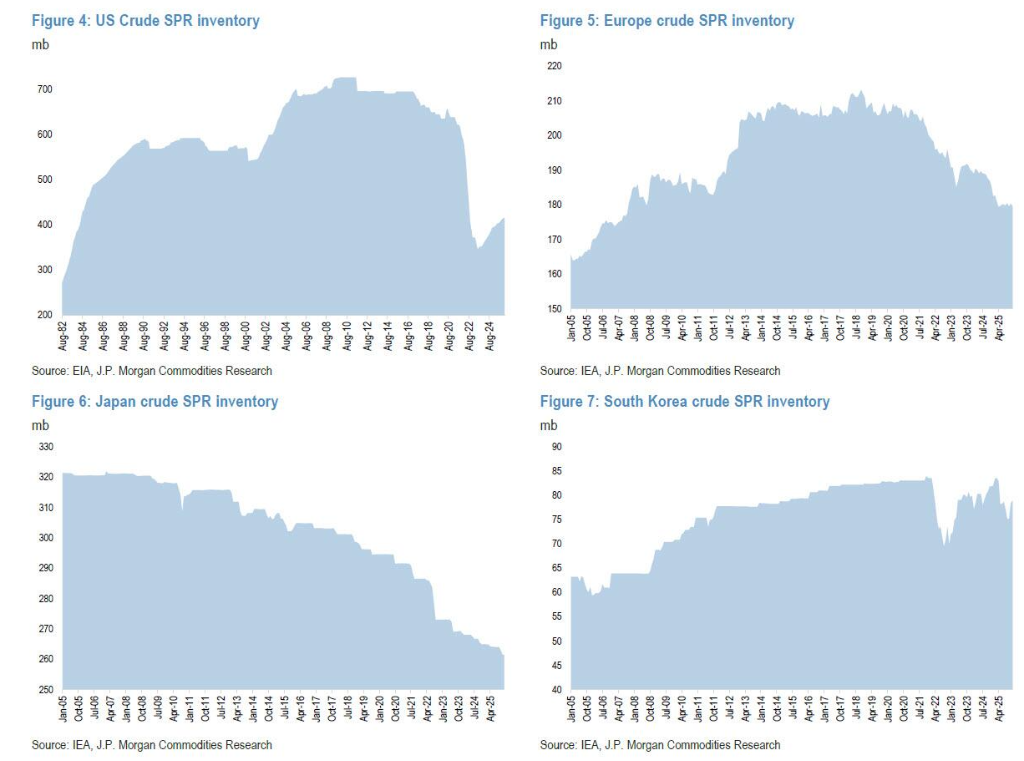

IEA member countries have public strategic reserves exceeding 1.2 billion barrels, with an additional 600 million barrels of corporate inventory under government regulation. From an absolute number perspective, stocks are not scarce.

(As of now, the total strategic oil reserves of the Organisation for Economic Co-operation and Development amount to 1.247 billion barrels, including 935 million barrels of crude oil and 312 million barrels of refined oil)

The real problem is that oil cannot flow from the production areas to the market.

A commodity analyst summed it up in one sentence:

“This is a flow issue, not an inventory issue.”

Releasing reserves can increase inventory supply, but cannot replace the global oil trade that occurs daily via maritime transport.

Simply put, if the 400 million barrels of stock released by IEA member countries cannot be converted into daily flow in the market quickly enough, it will not be able to fill the massive gap of 16 million barrels per day.

The Speed of Release is the Key Variable Deciding Oil Prices

In this context, the most concerning question for the market has become: How quickly can these reserves enter the market?

Kpler Senior Analyst Homayoun Falakshahi bluntly stated: “The devil is in the details; the key issue is the speed of release.”

Currently, the IEA has not announced a unified release pace, only stating that member countries will arrange their timelines based on their own situations.

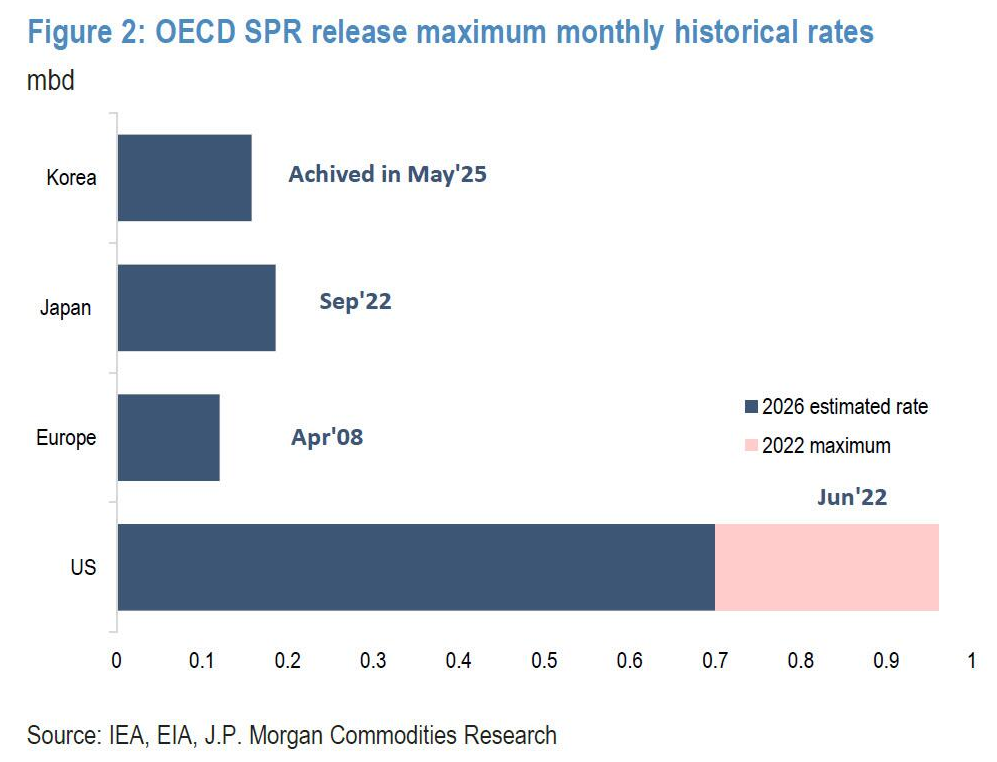

Large commodity traders privately estimate that the actual market entry rate of this batch of reserves is only 1.2 to 4 million barrels per day.

JPMorgan’s head of commodity market strategy, Natasha Kaneva, has more pessimistic estimates: The coordinated actual release rate of the G7 can only reach a maximum of 1.2 million barrels per day.

If calculated at this rate, even if all 400 million barrels are released, it would take nearly a year.

U.S. Strategic Petroleum Reserve: The Largest Scale, But Obvious Limitations

In this action, the U.S. is expected to bear the largest share.

U.S. Energy Secretary Chris Wright stated that the U.S. will release 172 million barrels of strategic oil reserves, with the entire release process expected to last for about 120 days.

He stated in an interview: “This is to buy time for the world during the supply disruptions caused by Iran.”

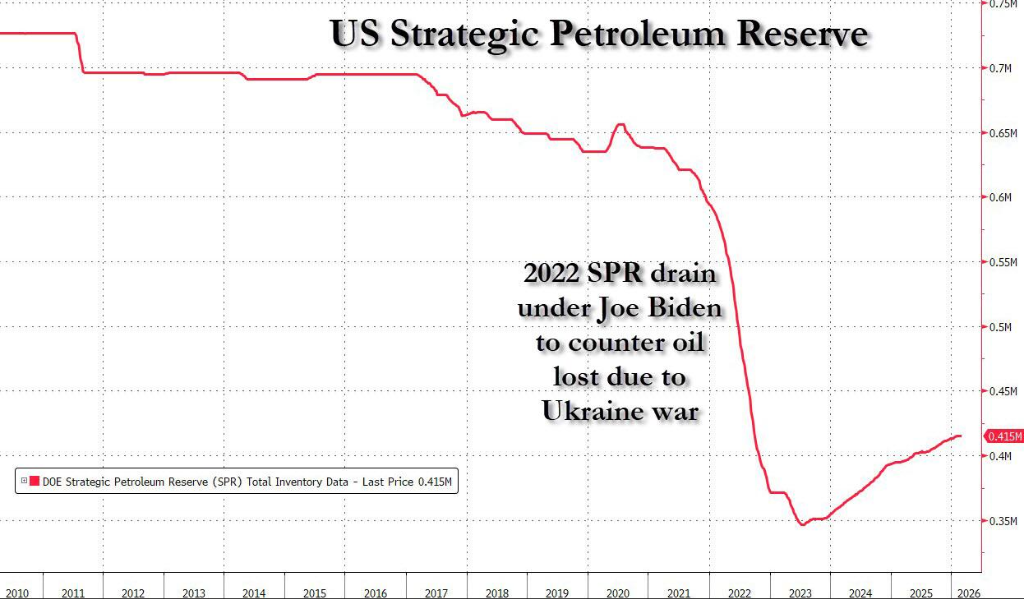

But the U.S. Strategic Petroleum Reserve (SPR) itself faces real limitations.

Currently, the U.S. Strategic Petroleum Reserve has about 415 million barrels, which is only about 60% of its maximum storage capacity. Previously, after the Russia-Ukraine conflict in 2022, the U.S. released 180 million barrels of reserves, resulting in a significant decrease in the inventory.

Theoretically, the U.S. SPR has a maximum release capacity of about 4.4 million barrels per day. However, an assessment by the U.S. Department of Energy in 2016 determined that the actual sustainable release capacity is only 1.4 to 2.1 million barrels per day.

In 2022, the actual release speed did not exceed 1.1 million barrels per day.

The Fatal Time Lag

Distant water cannot quench a nearby fire. In addition to the slow speed, the release of reserves also faces significant time lags.

From the implementation of policy to the circulation of spot supplies requires a cumbersome commercial process. When the U.S. president issues the release order, the Department of Energy needs about 13 days to bid, award contracts, and begin deliveries. Subsequently, crude oil must be transported via pipelines or tankers to refineries and end consumers.

This means that even if it is initiated immediately, the SPR crude oil will not genuinely enter the market as effective supply until the end of March. During this period, the daily supply gap of 16 million barrels will continue to accumulate. JPMorgan estimates that by the end of March, the accumulated crude oil deficit caused by geopolitical conflicts will exceed 100 million barrels. A mere 1.2 million barrels of supplementation per day is like a drop in the bucket.

More critically, the blockade effects of the Strait of Hormuz are rebounding upstream. Crude oil cannot be exported, and the oil-producing countries along the Persian Gulf are rapidly filling their tanks. Once the "storage pressure" reaches its limit, oil-producing countries will have to shut down wells.

Latest data revealed by Bloomberg shows that major oil-producing countries like Saudi Arabia, the UAE, Iraq, and Kuwait have already begun to significantly cut production, with total shut-ins reaching up to 6.7 million barrels per day, accounting for about 6% of global total production. Furthermore, as long as the blockade of the strait continues for one more day, this number will continue to rise. This has directly turned a logistics transportation problem into a capacity destruction issue.

For the Market, More Like a "Stabilizing Signal"

From the investors' perspective, this IEA action seems more like a policy stability signal.

On one hand, it conveys to the market that major consuming countries will jointly intervene in energy prices, attempting to lower risk premiums.

On the other hand, it buys time for the market—waiting for the resumption of shipping through the Strait of Hormuz.

However, if the blockade of the strait continues, the release of reserves is unlikely to genuinely fill the supply-demand gap.

As one energy trader put it:

“Strategic reserves can buffer shocks, but cannot replace normal global oil trade.”

Therefore, for the market, the true significance of this record release plan still depends on one question:

When will the Strait of Hormuz resume navigation?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。