Author: Farmer Frank

The reconstruction of geopolitical order + the compliance of virtual assets is a significant change for Hong Kong in the 21st century.

Last week, a rare "negative premium" appeared in Dubai's gold market.

According to sources cited by Bloomberg, due to the ongoing impact of conflicts in the Middle East, many gold traders in Dubai are selling off their inventory at a wholesale price that is $30 lower per ounce than the London benchmark price because they cannot ensure timely delivery and want to avoid bearing storage and financing costs indefinitely.

Although this "negative premium" of gold is mainly concentrated at the wholesale level and has not yet affected retail gold prices, it almost never occurs in normal markets because gold has always been viewed as one of the most liquid physical assets globally. Theoretically, as long as there is a significant price difference, arbitrage funds will quickly transport it to markets with higher prices, eliminating any price discrepancies.

However, this time, the arbitrage channel was brutally cut off by the realities of the world.

This easily brings to mind the "negative oil prices" that occurred in the oil market in 2020. The underlying logic is similar: When the delivery of physical assets incurs high transportation, insurance, and storage costs and faces significant uncertainties, there will be a misalignment between "paper price" and "actual value."

In other words, gold is just a facet; behind it, the entire asset flow channel has encountered problems, which also means that Dubai, as a global offshore financial center, is facing a functional stress test.

1. The flames of war reach Dubai, a cool reflection on the "offshore financial center"

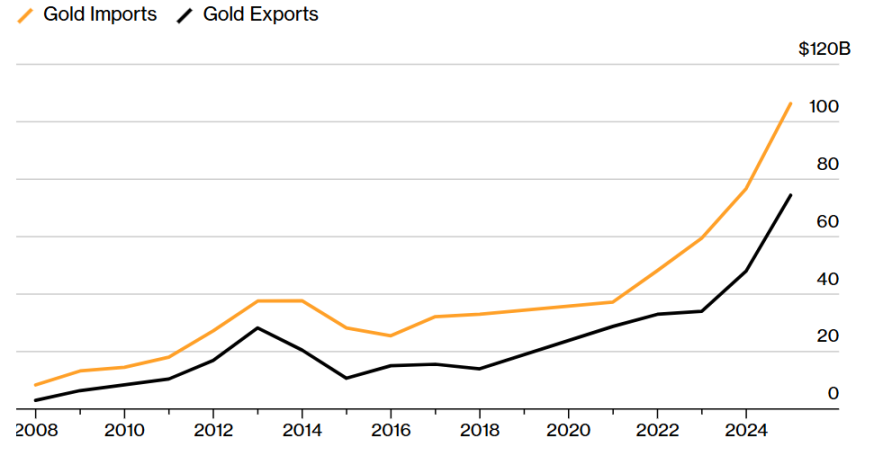

First, some cold knowledge: Dubai is not only a "haven" for global wealth but also one of the most important re-export trade hubs in the global gold market.

According to customs and trade data, Dubai imported 1,392 tons of gold in the entirety of 2024, with a total value exceeding $10 billion, and the export scale reached as high as $7.4 billion, making the UAE the second-largest gold import and export center globally. For instance, gold mined in Africa and refined in the UAE, and gold transshipped from Switzerland and London to Asia, passes through Dubai at a substantial rate.

It is worth noting that if we pull back the historical curve of Dubai's gold trade volume, we find that 2022 was a significant turning point. At that time, following the outbreak of the Russia-Ukraine conflict, the scale of gold imports and exports in Dubai accelerated sharply. A large amount of capital and physical assets that originally flowed through the European system sought an alternative route through Dubai due to sanctions, compliance issues, and geopolitical divisions.

This is a microcosm of Dubai's rise logic: Someone's crisis is precisely its window of opportunity.

As a trade hub connecting three continents—Asia, Europe, and Africa—Dubai has attracted wealth from around the world over the past twenty years due to the free flow of capital, low tax rates, and a relatively stable political and business environment—from Russian oligarchs to global family offices and Middle Eastern oil capital—viewing it as a significant node for asset storage, settlement, and circulation. More critically, every time external geopolitical turbulence occurs, Dubai often benefits.

However, unexpectedly, this time, the wind has blown towards Dubai itself.

Source: Bloomberg

The essence of "finance" is the flow of funds, and the premise of flow is that assets can move efficiently and safely.

Thus, when physical circulation channels are blocked, it will not only be the gold market that is impacted; all physical and financial assets that rely on cross-border movement will face the same predicament. Behind this lies a more fundamental question: what is the first principle of an offshore financial center?

The answer is quite simple: safety.

It is neither tax rates, nor ease of registration, nor light regulation; these are all second-tier competitive advantages. The primary reason funds are willing to dock in a financial center is a fundamental issue: can you withdraw your money at any time? Can you safely transfer it when needed?

If this underlying assumption cracks, the entire value system will begin to loosen. The inability to move gold is just the first visible signal of a crack in this "certainty."

It is essential to know that the status of an offshore financial center has never been stabilized merely by a "Global Financial Center" plaque; instead, it is continually verified and repeatedly selected through one crisis after another. Every significant geopolitical shock is, in fact, a hidden "re-tendering," where capital reevaluates where is safer and which "certainty" is more trustworthy, then irreversibly shifts its chips in that direction.

Historically, such migration has occurred more than once.

Beirut was once the financial center of the Middle East until the war devastated it; Hong Kong experienced a wave of capital flight before 1997, only to rebuild trust later due to system stability. The rise and fall of offshore financial centers is never a slow linear process; it often appears calm for a long time and then shifts focus at an unexpected speed after a certain critical point.

From this perspective, offshore financial centers like Dubai, Singapore, the Cayman Islands, and Switzerland thrive on a common historical backdrop of "peaceful globalization." They often lack extensive local industrial systems and do not possess the military power to support financial hegemony. Their financial status largely derives from the stability of the global order, in a sense, they reap the "peace dividend" amidst the great power competition.

However, when the world transitions from "peaceful globalization" to a new model of "great power competition, rule reconstruction, and geopolitical priorities," the risk premiums of these financial nodes will inevitably be repriced.

As this Middle East conflict reveals, a city that heavily relies on continuous external supply for food, water, energy, and even financial clearing will exponentially amplify its vulnerabilities once the external channels are systematically severed.

There has never been real neutrality detached from power structures. Offshore, in the end, must rely on a more extensive order and stronger security backing.

When this logic is re-understood, the paths of capital flight will change accordingly, leading to the question: if cracks appear in Dubai, where will be the next stop?

2. Dubai falls, who qualifies to thrive?

Theoretically, there are not many options.

Will it flow back to Europe and America?

That may not be realistic since a large amount of capital already flowed out of Russia, Europe, and the US to avoid the risks of sanctions, political instability, and stronger regulatory pressures. Settling in Dubai was a choice to escape those risks, so "returning" would mean being re-exposed to the very risk structure they tried to evade.

Turning to Singapore?

On the surface, it seems logical, as Singapore has always been Dubai's most direct competitor, but this also means that to some extent, it is the "Southeast Asian version of Dubai"—smaller in size, lacking strategic depth, and highly dependent on external factors, all the while remaining within range of the US political system. Additionally, under the compliance pressure of FATF, the entry thresholds and review requirements for setting up accounts in recent years have become progressively stricter. While Singapore may not lack attractiveness for high-sensitivity and highly cross-border capital, it may not be able to accommodate all overflow demands.

Under such a backdrop, Hong Kong has started to appear in more and more discussions. Friends from licensed virtual asset institutions in Hong Kong have reported to me that the volume of business inquiries from the Middle East and related regions is visibly increasing, and these are mainly not from retail speculators but rather from family offices, cross-border trade settlement platforms, and business enterprises.

Hong Kong is quietly absorbing the inflow of safe-haven capital from the Middle East conflict.

Structurally, Hong Kong indeed possesses a unique "combinatory advantage" under the current international market landscape as a free port of financial capital with a robust financial governance and regulatory system.

- The first card is the institutional foundation of a free port for capital: Hong Kong maintains a currency peg between the Hong Kong dollar and the US dollar, with highly free capital movement. More critically, compared to other purely globalization-dependent offshore nodes, Hong Kong is backed by large economies and mature financial systems, providing stronger institutional continuity and security expectations;

- The second card is a highly mature monetary governance system and linked exchange rate system: For global funds, the US dollar remains the core unit of transaction valuation, whether for corporate clearing, trade financing, or foreign exchange conversion. Hong Kong adopts a linked exchange rate system pegged to USD and HKD, possessing mature US dollar liquidity infrastructure, ensuring that it retains natural advantages in receiving cross-border funds today;

Furthermore, Hong Kong's current opportunity hides a deeper layer of logic—this layer precisely highlights the most intriguing aspect of the Dubai gold discount event.

As previously mentioned, the reason Dubai gold can only be sold at a discount is not that gold has lost its value, but that the transfer of physical assets heavily depends on physical world channels—flights, ports, insurance, and storage. If any of these conditions encounter problems, even the most standardized and "hard currency" assets can lose liquidity in an instant.

Then, is there an asset that can achieve instantaneous transfers and around-the-clock settlements without relying on traditional logistics and cross-border frictions, thus reducing various funding losses and obtaining maximum cost efficiency, even when flights are grounded and transportation is hindered?

Indeed. On-chain virtual assets, especially stablecoins.

Stablecoins represented by USDT/USDC can complete cross-border value transfers within minutes without depending on logistics, requiring no storage, and facing almost no border friction. When the review chains of traditional banking systems are lengthened due to geopolitical risks, compliance costs soar, and clearing efficiencies decline, or even face chain break risks in extreme cases, this "de-friction, borderless, 24/7" settlement mode reveals an almost dimensional advantage.

This is another core logic behind Middle Eastern funds reevaluating Hong Kong.

They are not necessarily speculating on cryptocurrencies; they are more likely seeking a more efficient and secure clearing and foreign exchange alternative outside the traditional banking system. In this context, Hong Kong possesses one of the world's clearest, most compliant, and most financially connected digital asset markets. For many Middle Eastern funds, what they genuinely want to find is a financial node that combines a stable regulatory environment, US dollar liquidity, and on-chain settlement capabilities.

As the competition of offshore financial centers intensifies alongside this new variable of virtual assets, the hand that Hong Kong holds is becoming increasingly difficult to replicate.

3. Hong Kong × Virtual Assets' "Historic Opportunity"

It is not an exaggeration to say that since the Hong Kong SAR government released its virtual asset policy declaration on October 31, 2022, Hong Kong may be迎来一次"天时地利"难得叠加的历史窗口, a truly historic opportunity.

In the global financial system, Hong Kong has long played an important role in connecting capital between the East and the West. Its expertise has never been merely to create a local market, but to organize funds with different systems, currencies, and risk preferences into a calculable, connectable, and clearable framework that allows for efficient flows.

This capability is equally applicable in the era of crypto finance, and it has become even scarcer.

It is well-known that Hong Kong has been continuously building new digital financial infrastructure for over three years, striving to connect the preliminary financial infrastructure ecology, which includes local licensed trading platforms (VATP) such as OSL HK and Hashkey Exchange, along with their accompanying custody, tokenization services, and deep connections with traditional financial systems, resulting in a burgeoning of licensed virtual asset service platforms (VASP).

More intriguingly, at the same time the global geopolitical order is rapidly restructuring, Hong Kong's virtual assets, especially the regulatory framework for stablecoins, have been gradually reaching the "last mile" after years of deliberation:

- Regulatory consultations began in 2022;

- A regulatory sandbox test will launch in 2024;

- On May 21, 2025, the Legislative Council passed the "Stablecoin Regulation Draft";

- On August 1, 2025, the "Stablecoin Regulation" will officially take effect;

- By March 2026, the first batch of stablecoin licenses will also approach the edge of opening.

In comparison to major global financial centers, this has emerged as one of the most systematic and robust regulatory frameworks for compliant fiat-pegged stablecoins to date, and it is ahead of many major economies, including the United States, in similar legislative implementations.

According to signals previously released by the Hong Kong Monetary Authority, the first batch of stablecoin issuer licenses is expected to be issued gradually starting in early 2026, and since the initial number of licenses will be limited, the entry thresholds and ongoing regulatory requirements will be exceptionally high, aligned with banking-level standards. For this reason, Hong Kong's stablecoin licenses are likely to become some of the most valuable compliance credentials in the global digital finance sector. On-chain stablecoins are no longer just a niche topic in the crypto-native world but are rapidly becoming new mainstream tools for reshaping cross-border payments and global trade settlement infrastructure.

For cross-border funds flowing into Hong Kong from the Middle East, this emerging stablecoin ecosystem signifies much more than a new investment category; it represents the formation of a new clearing and settlement channel that operates around the clock, unbound by physical borders, backed by sovereign-level compliance.

As previously mentioned, the business inquiries from the Middle East are primarily not about simple retail-oriented cryptocurrency trading but rather large-scale transactions and cross-border trade settlements at the enterprise and institutional levels.

These demands are also prompting a new role for licensed local institutions in Hong Kong.

At present, in terms of meeting institutional and enterprise trade settlement needs, the singular observation is OSL Group (863.HK), which possesses the first compliant licensed trading platform in Hong Kong and has a compliance channel and payment and trading network globally. Just before the official effectiveness of Hong Kong's "Stablecoin Regulation" last year, OSL Group launched three new products targeting institutions: a compliant stablecoin management platform called StableX, asset tokenization services called Tokenworks, and a corporate-level crypto payment solution named OSL BizPay. This year, OSL Group has also launched a compliant USD stablecoin (USDGO) which aligns with US federal regulations and can be compliantly distributed in Hong Kong, primarily focused on cross-border e-commerce, bulk trade, and interactive entertainment sectors.

This is clearly no longer limited to the traditional notion of exchange business; it is extending toward compliance stablecoin management, asset tokenization, and corporate payment solutions. In a sense, this highlights the essence of the issue. In this round of competition, compliant virtual asset platforms are not just competing on trading match-making capability but on who can recognize and become the next generation's infrastructure node for cross-border global fund movement.

Final Remarks

The more chaotic the world, the more valuable are the assets, systems, and paths that provide certainty.

The chain reactions brought by the Iranian situation are still brewing; this time, no one knows where the endpoint lies, but it is almost certain that: some opportunities, once lost, are hard to regain; some paths, once formed, will create strong inertia.

In the past, discussions about Hong Kong's virtual asset market often remained within the narrative framework of a "compliance model"—in a sense, it is a policy testing ground, the frontier of regulatory exploration, but it has not yet deeply aligned with the underlying logic of global fund movement.

In the early stages of launching a compliant Hong Kong dollar stablecoin, retail demand and scenario expansion from the consumer end will likely be the initial focus for regulators and licensed institutions. However, this does not preclude stablecoins issued or distributed compliantly in Hong Kong from seeking broader real landing demands and possibilities. This is not something that can be achieved overnight, but sometimes, the arrival of opportunities comes much faster than expected, and the ability to seize and break through hinges on who can make sufficient preparations.

With the accelerated restructuring of geopolitical landscapes, rapid changes in financial markets, and the formal establishment of stablecoin regulation, the meaning carried by licensed virtual asset platforms in Hong Kong is being rewritten. This is not only an opportunity for Hong Kong; to some extent, it could be a historic moment for Hong Kong and numerous licensed virtual asset institutions to deeply embed themselves in the global trade cross-border payment and settlement system.

The objective conditions are already in place, the policy framework is closing, and the infrastructure is rapidly taking shape. The only question remaining is:

Can Hong Kong truly play this hand well?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。