Original | Odaily Planet Daily (@OdailyChina)

Author | Ethan (@ethanzhang_web3)

On March 4, Trump posted on Truth Social, directly criticizing the banking industry for threatening and undermining the GENIUS Act. He urged Congress to advance the cryptocurrency market structure legislation as soon as possible, warning that if the framework is not implemented promptly, the United States will lose its advantage in the cryptocurrency space to other countries. His words were intense, and his tone urgent, resembling that of a defender who is advocating for the industry.

However, if you know that World Liberty Financial (WLFI), under the Trump family, is actually the issuer of the stablecoin USD1, the implications of this statement become much more subtle. One of the most direct beneficiaries of the GENIUS Act is precisely the family business of the person making this post from the White House.

This is not the first time. Since Trump returned to the White House in January 2025, his cryptocurrency empire has never truly separated from his presidential identity. The two hats have always been worn by the same person—only in the past few weeks, the overlap between them has been more difficult to ignore than ever.

On one side, the family project USD1 faced coordinated attacks in late February, briefly losing its peg. The WLFI team then transferred large amounts of tokens to centralized exchanges for two consecutive days, with on-chain signals prompting market speculation; on the other side, the president himself was fighting for stablecoin legislation in Washington, launching a direct counterattack against the banking lobbying groups.

These two lines operate simultaneously, converging on the same family, in the same timeframe, on the same issue. This is where the current Trump crypto story becomes truly interesting.

Pressure Testing of USD1

In March 2025, World Liberty Financial officially launched USD1, a stablecoin pegged to the US dollar at a 1:1 ratio, backed by reserve assets such as short-term US Treasury securities, dollar deposits, and cash equivalents, held in custody by the crypto custodian BitGo, with monthly reserve attestations provided by the accounting consulting firm Crowe. In its design framework, it benchmarks against regulatory compliance routes rather than those offshore stablecoins with unclear reserves and questionable transparency.

The timing of its market entry was precise. Just as discussions around the GENIUS Act were heating up, and market expectations for compliant stablecoins were rising, USD1 made its debut in a striking manner: I am the dollar, I am compliant, I have the endorsement of the president’s family. In May 2025, the Abu Dhabi sovereign fund MGX announced a $2 billion strategic investment in Binance using USD1, propelling USD1 overnight from being a newcomer in the crypto sphere to an undeniable player in the global stablecoin landscape.

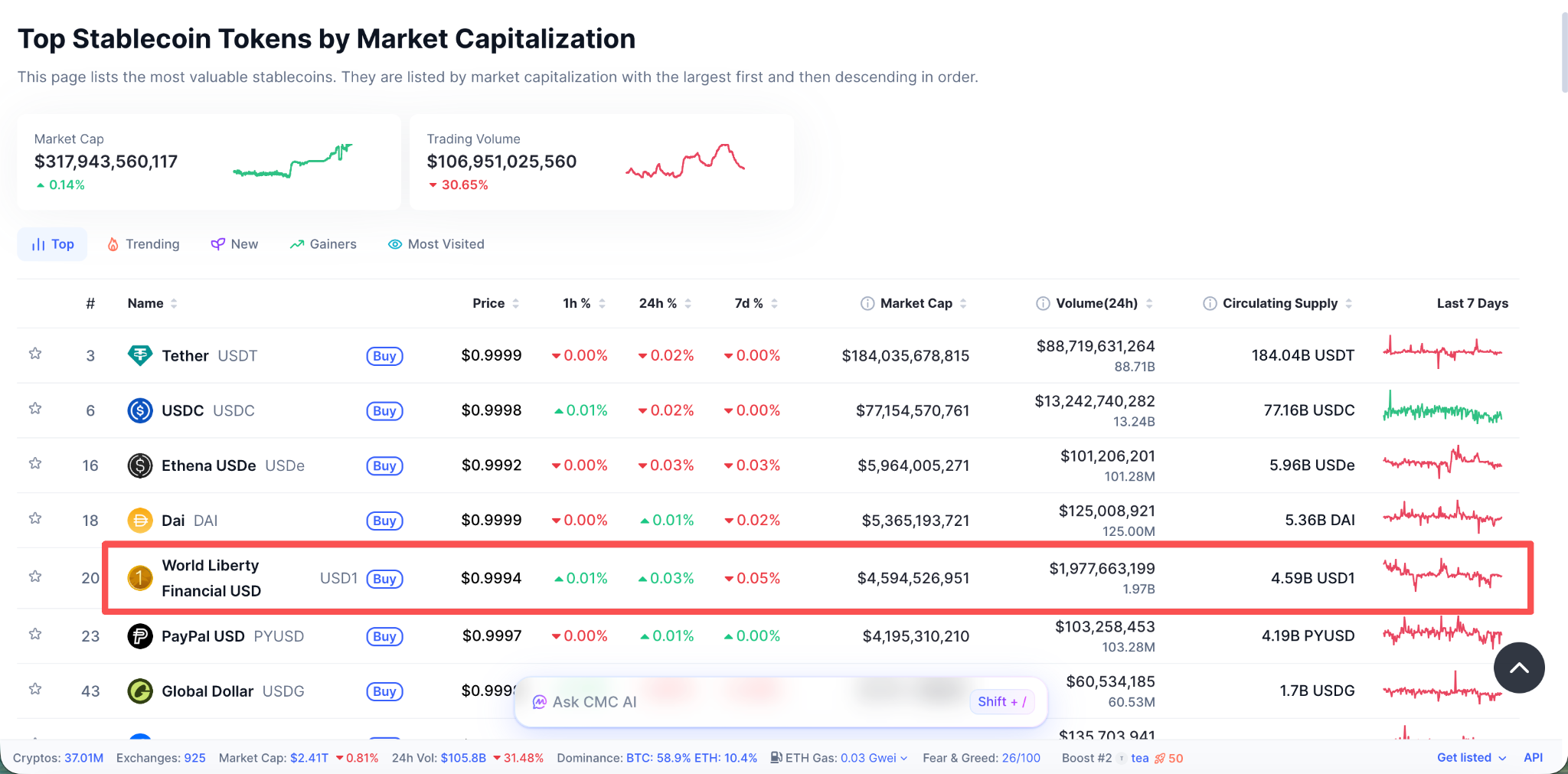

By March 2026, USD1 had a circulating market cap of approximately $4.5 billion, comfortably ranking among the top five stablecoins globally. However, behind this scale, some details are noteworthy: According to research from data analysis platform Kaiko, over half of USD1's liquidity on PancakeSwap comes from market maker wallets associated with the WLFI team, rather than genuine market trading demand; the number of monthly active users priced in USD still shows a significant gap compared to older players like USDT and USDC. Political endorsement is the strongest marketing resource, but it cannot replace real market depth.

On February 23, 2026, an unexpected pressure test broke this subtle balance.

That morning, USD1 briefly lost its peg, dropping to $0.994, deviating from the $1 pegged price by about 0.6%. WLFI quickly issued an alert on platform X, characterizing this fluctuation as a coordinated attack involving multiple points: attackers had hacked the social media accounts of several WLFI co-founders, employed KOLs to disseminate panic-inducing information, and simultaneously shorted WLFI tokens, attempting to profit in the chaos they created.

WLFI spokesperson David Wachsman subsequently stated to the media that the project's engineering and security teams successfully thwarted coordinated attacks from multiple directions; the event proved that USD1's design was robust and could be relied upon under any conditions. USD1 then recovered to around $0.998, and the 1:1 redemption mechanism played its anchoring role without triggering a deeper trust crisis.

From the outcome, this attack indeed failed. However, from the context, this attack occurred at a highly sensitive time—just days earlier, WLFI had hosted a high-profile crypto summit at Trump's Mar-a-Lago estate, attended by government officials, traditional banking executives, and former Binance CEO CZ.

The decoupling was brief, but it exposed a structural issue: Political endorsement can bring market value, but it does not necessarily bring resilience against pressure. When a stablecoin's biggest selling point is the name of a presidential family, any attack against that name will simultaneously become an attack against that stablecoin.

Is the Team Starting to Offload?

About ten days after the attack, another set of data on-chain emerged, amplifying the market's interpretive space once again.

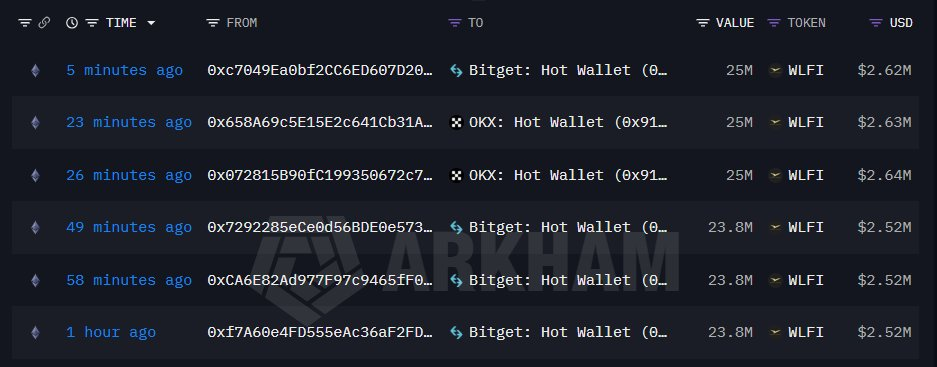

On-chain analysis showed that, starting March 4, WLFI transferred large amounts of WLFI tokens to centralized exchanges over two consecutive days: On the first day, approximately 146.4 million WLFI were transferred to OKX and Bitget, worth about $15.4 million at the time; on the second day, about 16.71 million WLFI were further transferred to OKX, worth about $1.74 million. The total value of the two transfers exceeded $17 million.

In the on-chain world, transferring tokens to centralized exchanges is often seen as a signal of high intent, typically indicating potential selling intentions. While not all tokens transferred will be immediately liquidated, the action itself is enough to trigger associations and alertness among market participants, especially in the context of the project facing multiple pressures.

Such associations appear particularly reasonable at this moment. The USD1 stablecoin had just experienced a brief decoupling event on February 23, 2026, where its price briefly dropped to about $0.994, even reaching $0.98 at certain moments. Although the price recovered to around $0.998 within hours, the event had exacerbated external doubts about WLFI’s project stability.

Simultaneously, political controversies surrounding WLFI had not subsided—the U.S. House of Representatives launched an investigation on February 4, 2026, demanding WLFI provide ownership records, funding flows, governance documents, and details of board changes, focusing on the Emirati royal family member Sheikh Tahnoon bin Zayed Al Nahyan's secret acquisition of approximately 49% of WLFI shares for $500 million (signed four days before Trump's second inauguration on January 16, 2025), with a deadline of March 1, 2026. Additionally, Senators Elizabeth Warren and Andy Kim requested the Treasury to review the transaction on February 13, citing national security risks and potential conflicts of interest.

Notably, WLFI did not release any public explanation regarding this recent batch of on-chain transfers. This silence has in itself become part of the market's interpretation.

Of course, another interpretation is equally valid: the project is strategically positioning itself to enhance CEX liquidity in preparation for future market operations; or, this is a preordained liquidity management maneuver within the token economic design, unrelated to external conditions. Both narratives cannot be completely ruled out, which is precisely the paradox of on-chain data—it provides facts but does not offer intent.

Moreover, according to WLFI's operational agreement, entities controlled by the Trump family can receive 75% of the project's profit sharing. Trump's holding entity DT Marks Defi LLC owns approximately 60% of WLFI, and Trump family members and related parties have been allocated around 22.5 billion WLFI tokens. Any market movements involving this batch of tokens are not simply project-level financial decisions; they also represent this family's asset monetization pathway in the crypto market.

Currently, the price of WLFI tokens has fallen over 50% from its historical high. At this juncture, any large-scale transfer action inevitably comes under scrutiny against the backdrop of this decline.

Another Battle for the President in Washington

On March 4, Trump posted on Truth Social, using language more urgent than usual. He specifically criticized the banking industry for threatening and undermining the GENIUS Act, demanding that Congress advance the cryptocurrency market structure legislation without delay and warning that if the U.S. acts slowly, its advantages in crypto will be relinquished to other countries.

This rhetoric is familiar—packaging domestic policy disputes into great power competition, framing the opposing side as traitors. Trump has used this tactic many times, and it has always been effective.

He is speaking up for the industry while also speaking up for himself. It’s just that these two matters are wrapped into the same statement.

The GENIUS Act itself is not complex. It is the first bill in the history of the United States to establish a federal-level regulatory framework for stablecoin issuance, clarifying issuance qualifications, reserve requirements, and anti-money laundering obligations. After multiple rounds of revisions, it was signed into law in 2025; the direction is positive, but controversies lie in the details.

The banking lobby group is focused on one particular clause: whether stablecoins can provide returns to holders. The logic is straightforward—if stablecoins can pay interest, why would people keep their money in banks? Deposit outflows are the last outcome banks want to see. Thus, the lobbying group began to mobilize to push for the modification of relevant clauses, extending this resistance to another piece of cryptocurrency legislation, the CLARITY Act, forming a bundling: if you want stablecoin legislation, you must first agree to my terms.

Trump's reaction was to directly criticize the banking industry on social media. This posture sends a signal: the legislative process is not going smoothly. A genuinely confident proponent does not need to pressure through posts; they need to post to show that the bargaining chips at the negotiation table are still inadequate.

However, what truly complicates this game is not the banking industry's resistance but a blank space in the GENIUS Act text.

This law contains no provisions restricting the president or family members from profiting from stablecoin issuance. This gap sparked controversy during the legislative process, with some senators attempting to add prohibitive clauses, but ultimately, they were left out. This resulted in a peculiar structure: a president who is both a proponent of the legislation and a potential beneficiary of it, who may exercise veto power due to how the legislation affects his own interests—this logical closed loop may be the deepest hue of this Washington game.

Conclusion: The Intersection of Two Lines

Place the three events above on the same timeline: February 23, USD1 lost its peg amid a coordinated attack, then quickly recovered; days after the attack, WLFI transferred a large amount of tokens to CEXs for two consecutive days; on March 4, Trump posted on Truth Social, launching a direct counterattack against the banking industry that is blocking the GENIUS Act.

These three events occurred within less than two weeks, and while there is no simple causal relationship between them, they all feature the same family—the cryptocurrency empire of current U.S. President Trump: on one side, the family project is facing real pressures in the market, whether from external attacks, opaque on-chain actions, or political investigations from Congress; on the other side, the president is using his most mobilizable resource—White House discourse and political credibility—to protect stablecoin legislation.

The intersection of these two lines is Trump himself. He is not switching between his identity as a businessman and that of a president; he is fighting on two battlefields simultaneously, and these two battlefields are aimed in the same direction: making USD1 and WLFI survive, allowing them to gain legitimacy, scale, and profits under a regulatory framework that he personally promotes.

External scrutiny of this overlap has always existed and has notably intensified in early 2026. An investigation led by Representative Ro Khanna focuses on a transaction in which the Emirati royal family secretly acquired approximately 49% of WLFI shares for $500 million, questioning the flow of funds, governance transparency, and potential national security risks—especially since shortly after the Emirati royal family's investment in WLFI, the Trump administration approved the export of hundreds of thousands of advanced chips to the UAE's Tahnoun-controlled company G42, despite this decision being previously shelved on national security grounds.

The legal community considers this transaction a potential constitutional violation (contravening the constitutional prohibition against the president receiving foreign gifts). The White House's response is that Trump himself has never participated in any transactions or decisions related to WLFI and has distanced himself from the company since taking office.

This statement may hold up legally, but in reality, it describes a state that is almost impossible for outsiders to independently verify. When a presidential family’s business continues to appreciate due to policy benefits, while the president himself continuously creates favorable policies for the industry, the question of whether interests exist and whether connections are established becomes a structural gray area.

The deeper question is not whether Trump has violated the law but whether existing institutions have adequate tools to handle this new type of power-business overlap. Stablecoins are a sector that heavily relies on regulatory clarity, and when the promoter of regulatory clarity is itself a market participant, the rules of the entire game become a topic that requires re-examination.

Trump's dual hats are no longer a deliberately hidden secret. They exist with a degree of openness, under the surveillance of the market, the media, and some members of Congress.

This persistence is precisely because the mechanisms theoretically able to constrain it—Congressional legislation, the president's signature, regulatory rule-setting—each step has his hand in it. The constraining mechanism itself is controlled by the person who needs to be constrained.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。