Written by: Thejaswini M A

Translated by: Block unicorn

Your parents did not see buying a house as an investment. They bought it simply because they needed shelter, because they could afford the mortgage on a single income, because there were good schools nearby, and because everyone was doing it at the time. They painted the living room twice and argued for years over the kitchen renovations, but they never truly remodeled. They raised children here and spent their retirement here. Unconsciously, they created their most valuable wealth in their lives.

Now they are struggling to pay for medical expenses, while this house is valued at $1.2 million.

A figure that has repeatedly appeared in financial studies recently is: $124 trillion.

This is the expected total amount of wealth that will be transferred from the older generation to the younger generation over the next 25 years. Analysts call it the "great wealth transfer." Media coverage seems to present it as entirely good news, especially for those receiving the transferred assets.

Is it really that simple?

The wealth being transferred mostly lacks liquidity, with the majority being real estate. The Baby Boomers bought houses when prices were reasonable, paid off mortgages over decades, and watched their properties appreciate, becoming a major source of their wealth. Meanwhile, the generation inheriting these properties is watching the same property values preventing them from buying homes. Today, these properties may come into their hands, but they lack liquidity, carry heavy emotional burdens, involve complicated legal procedures, and are increasingly difficult to utilize practically.

This is the issue that the headline figure of $124 trillion fails to reflect.

To understand why this matters, one must grasp the changes in the housing market since the 1960s. The nature of housing has transformed. Initially, housing was merely a shelter from the elements, but it gradually evolved into the primary financial tool of the American middle class. For families earning below the highest income levels, housing is no longer one of many assets; it is the most important asset. The net worth of real estate is the largest single expense on the balance sheets of American households, far exceeding the total of retirement accounts, stocks, and all other assets combined.

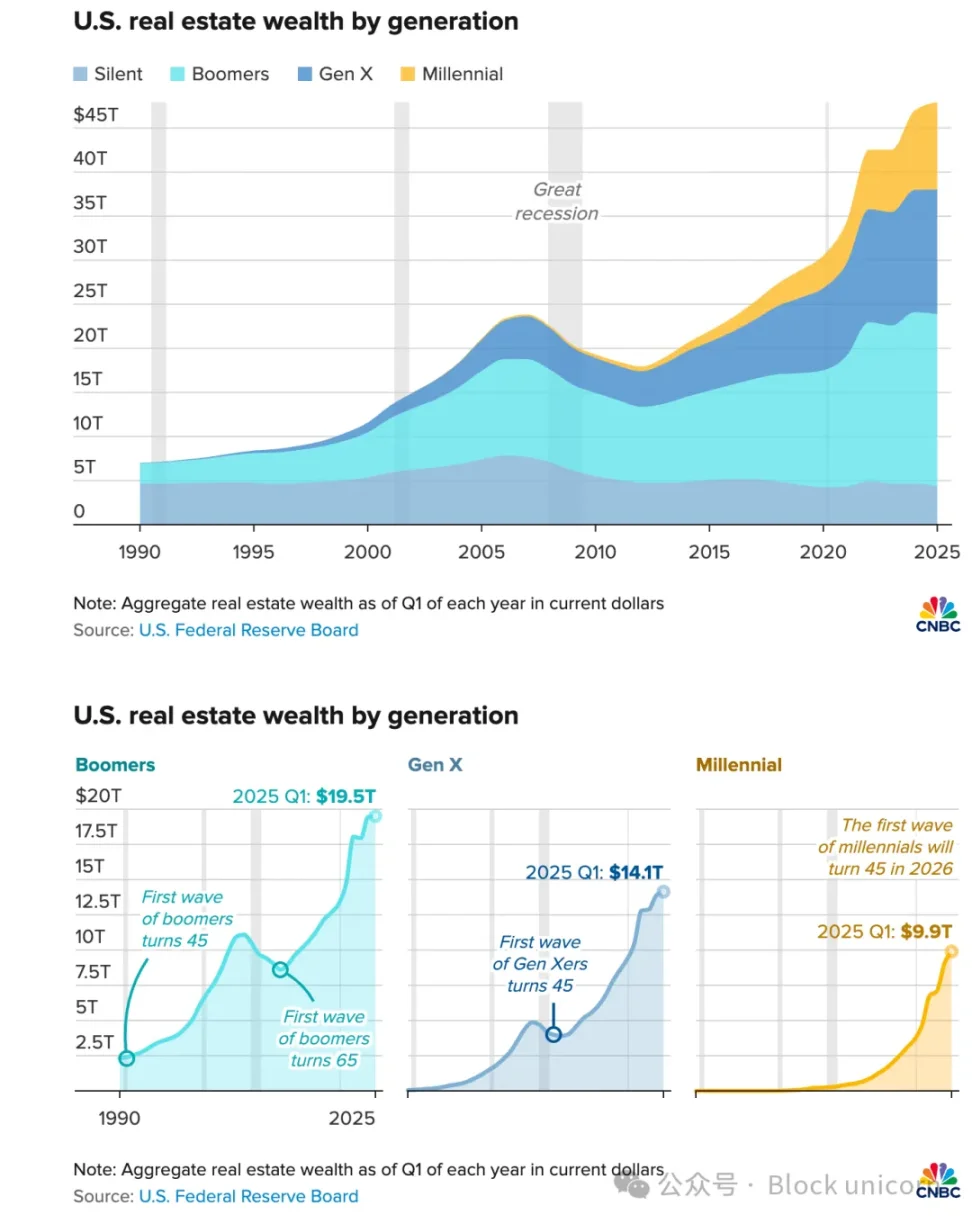

The Baby Boomers accumulated wealth under conditions that no longer exist today. When they bought their homes, the price-to-income ratio was between 2 and 3.5. Over the next few decades, with the growth of real wages, they paid off their mortgages. By the first quarter of 2025, the Baby Boomers' real estate holdings had reached $19.5 trillion, a small fraction of which was the case in 1990.

Now, the Millennial generation entering the housing market faces a situation where the price-to-income ratio is more than double what it was when their parents bought homes. They carry student loans that their parents did not have. The mortgage rates they face make monthly payments on moderate-priced homes nearly unaffordable for middle-income households. Just the down payment, combined with the speed of home price increases far outpacing savings accumulation, creates a natural trap.

The result is a generational divide that is no longer cyclical. Those who can afford to buy have bought, while those who cannot are about to inherit the wealth created by the first generation.

Real estate is one of the least liquid assets an individual can hold.

When you urgently need money, you cannot sell 10% of your ownership of a house. When your job changes, you cannot just move the house. You also cannot easily distribute a house among four siblings without triggering a legal process that could last 18 months, which might deplete the already strained funds of the estate. Inheriting a million-dollar property in a city you cannot afford is not a good thing. It presents a choice: sell it; keep it and bear all the costs; rent it out and become a landlord; or spend years negotiating with siblings to determine which option to take.

The Baby Boomers currently hold about 40% of the housing wealth in the United States.

Of these, 61% say they will never sell their homes, but once you understand the underlying incentives, I think this is not stubbornness. Selling a house would trigger capital gains tax from decades of appreciation. It would reset a 3% mortgage rate to 7%. In California, property tax bills can multiply tenfold overnight. Furthermore, there are no affordably priced homes available for them to downsize to anyway.

So they hold on. The homes do not enter circulation. Young homebuyers are locked out and can only wait to inherit wealth—this has become the only realistic way to buy a home in many cities. Yet when the inheritance finally comes, the issue of liquidity is simply transferred rather than resolved.

Alex Svanevik, co-founder of Nansen, describes the coming developments as a tsunami. He stated in January 2026 that around $100 trillion in assets will be inherited over the next 20 years, and the factors driving this wealth into the cryptocurrency space are structural, not speculative. He estimates that even if only 3% of inherited assets flow into the cryptocurrency market, its scale could double from where it is now.

Does the 3% figure sound low? But think about who will inherit this wealth. According to a recent survey by OKX, Generation Z's trust in cryptocurrency is five times that of the Baby Boomers. Millennials hold more digital assets than their parents. We do not need to prove the validity of cryptocurrency to them. They have grown up using cryptocurrency just as their predecessors used savings accounts. What they need is for the wealth they inherit to match their current level of wealth.

This is where the gap lies. Tokenization is the key to bridging this gap.

Tokenization of real-world assets refers to representing ownership of physical assets on the blockchain. Once achieved, ownership can be divided, transferred without brokers, stored in wallets, used as collateral, or traded with the consent of none of the involved stakeholders. This makes currently difficult friction points manageable.

Specifically, tokenization provides a solution for inheriting real estate that addresses four questions currently lacking good answers.

Liquidity: Tokenized properties can be partially sold. For example, an heir in need of $50,000 who owns a property worth $500,000 can sell 10% of their ownership instead of having to sell the entire property or end up with nothing. Furthermore, since the underlying real estate can be freely bought and sold, lenders can underwrite it, making it easier to secure loans against the asset. For the same reason, loans secured against the property also become simpler.

Fractionalization: When four siblings inherit a property, tokenization technology allows each to hold their exact share digitally, which can be traded, sold, or independently held without needing to agree on how to dispose of the physical asset. When ownership is programmable, legal disputes arising from inheritance will be greatly simplified.

Mobility: Tokenized assets can be included in portfolios alongside stocks, cryptocurrencies, and other assets. They can be managed remotely, transferred across borders, and ultimately used as collateral for decentralized finance (DeFi) protocols. The geographical constraints of real estate no longer hinder the financial flexibility of heirs.

Accessibility: For heirs who cannot afford to purchase properties but are about to inherit them, tokenization allows partial participation. For younger siblings inheriting smaller shares, fractional ownership enables them to hold physical assets instead of having to cash out immediately.

The market is already moving in this direction. By early 2026, the total value of tokenized real-world assets has reached $26 billion in distributed assets and $388 billion in representative assets, and it is still growing rapidly. Real estate currently represents only a small fraction of this, but the infrastructure being built, such as wallets, on-chain settlements, and programmable ownership, has reached functional capabilities that were unattainable two years ago. Svanevik points out that the products being developed today at Nansen were simply not possible two years ago because the infrastructure was not yet mature. But things have changed now.

This does not mean that tokenization will solve the housing affordability crisis. Housing prices will not decrease simply because ownership is easier to transfer. Structural issues in the market, such as supply constraints, interest rate lock-ins, and the long-term disconnection between housing prices and wages, still exist. We also do not know whether financializing the last remaining illiquid asset owned by most households genuinely improves their lives or merely makes their issues easier to transfer.

Tokenization addresses a more specific, urgent concern. It deals with what happens when $25 trillion in real estate wealth changes hands between two generations: one generation having invested all their wealth in real estate, while the other sees wealth as liquid, digital, and not necessarily tied to a physical address.

For most individuals with home equity, existing home equity extraction tools are impractical. Cash-out refinancing involves giving up a 3% mortgage rate to opt for a 7% rate. Home equity lines of credit (HELOCs) and home equity loans require qualifying income, which retirees often struggle to meet. Reverse mortgages carry a 30-year stigma and create complex issues regarding inheritance. Selling a home triggers a tax trap and resets interest rates. Every choice brings losses that the holder cannot bear.

The wealth transfer has already begun at a scale of approximately $1.5 trillion a year and is accelerating. The first cohort of Millennials will turn 45 in 2026. JPMorgan, BlackRock, and Franklin Templeton have all invested in the tokenization asset space over the past two years to build infrastructure for this moment. Robinhood CEO Vlad Tenev pointed out last year that this wealth transfer is accompanied by technological change and will be critical in the coming years.

The generation inheriting this wealth is accustomed to keeping financial assets in wallets, not filing cabinets. The real question is how they will navigate the current system that relies on paper documents and transactions through brokers.

Each generation accumulates wealth in languages they understand. The next generation needs to translate it into another language.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。