What is the difference between Backpack's IPO (IPOs Onchain) and MSX's Pre-IPO?

Originally, I didn't plan to continue following up, after all, everything that needed to be said has been said. I am just playing an educational role and didn't want to keep chasing after it. However, since the friends from @MSX_CN want me to comment on @Backpack's IPO, I will continue to discuss. This comment will inevitably involve some comparisons.

I would like to declare in advance: I have no financial interest in Backpack and have not participated in any activities related to Backpack.

(1) Difference in cooperation partners

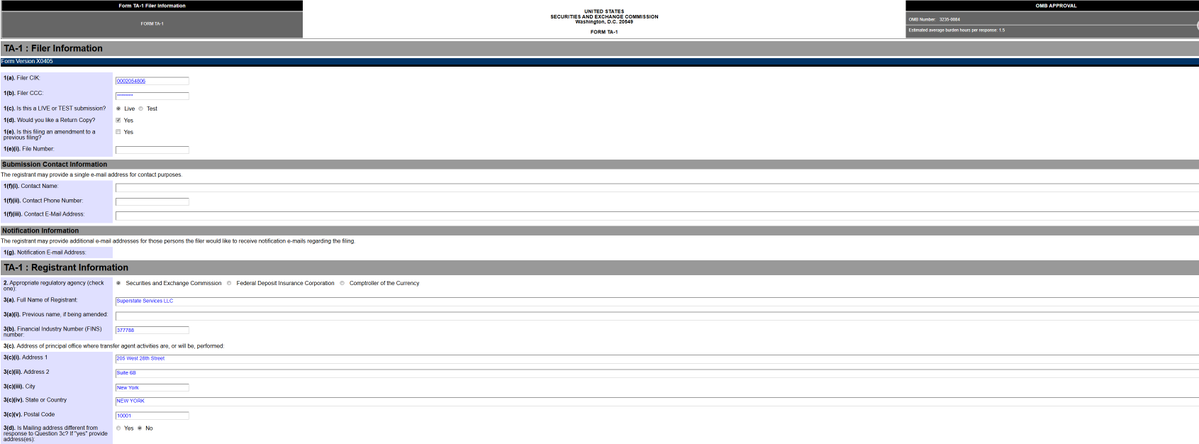

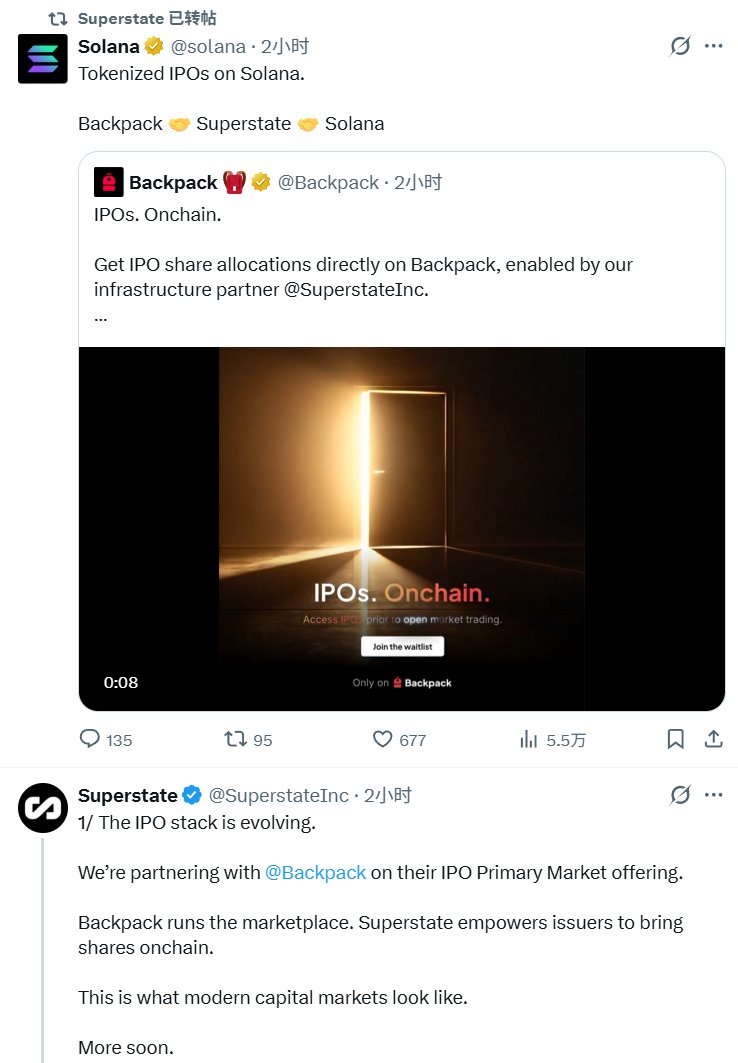

First of all, the provider of Backpack's IPO is not Backpack itself, but a company called Superstate, which provides compliance qualifications, which can be checked on the SEC website.

This is similar to the collaboration with Republic that MSX is working with, but there is a significant difference here. First, Superstate is compliant, and Superstate has directly announced its collaboration with Backpack, as did the official Solana announcement.

On the other hand, MSX claims to partner with Republic, but it is actually Republic Ventures, and neither Republic nor Republic Ventures has made any public reports. Even the MSX official has stated that Republic is not responsible for the issuance, only for fund management, which raises questions about MSX's compliance.

Of course, many of MSX's friends say that we are in the era of wildness and do not need compliance, and I completely agree with that. But if compliance is not needed, why do they want to claim themselves as a compliant exchange, and even claim to cooperate with Republic, while also trying to avoid mentioning Republic in promotional materials when questioned?? Can I know the reason??

(2) Difference in compliance

Secondly, according to Superstate's documentation, which is just documentation and does not mean it is correct, they are compliant and cannot casually make grand statements. The SEC is not a decoration. Superstate's IPO plan is:

Native shares + Transfer agent + On-chain settlement

This is not SPV. I have even given a tutorial on SPV, while Superstate's plan directly links the real stocks registered with the SEC on-chain, rather than synthetic assets or packaged derivatives. This is fundamentally different from MSX; what MSX issues is only a token of the same name, which has no real relation to the stock itself, at best it tracks the same price. (Currently unconfirmed)

The issued stock-type tokens are maintained and updated on the shareholder register by Superstate, which acts as the SEC-registered transfer agent, and are updated simultaneously on-chain during transfers. Issuance and fundraising can be executed via a Direct Issuance Program.

(3) Difference in KYC and distribution model

Next, Superstate's model is limited; first, it requires complete KYC. Since it is compliant with the SEC, it must follow American rules, so even if working with Backpack, not all Backpack users should be able to purchase. Of course, Backpack is the provider of KYC.

On the other hand, MXS does not require KYC, and those who understand naturally understand. I don't really need to say much more since it's the wild era, and it doesn't matter. But if they are already operating in the wild, why do they still insist on claiming to be compliant? Isn't that unnecessary?

Also, under the Superstate model, the on-chain tokens must be bound to the shareholder register, which is a complicated flow and is paired with KYC, so when actually implemented, it still depends on Superstate's operations, which are currently difficult to assess.

(4) Difference in risks

Finally, in terms of purchasing, the minimum initial investment for purchasing Superstate's fund (USTB/USCC) is $100,000, whereas there is no minimum unit for purchasing tokenized equity through Backpack. However, in reality, one token should equal one share, and if it is Direct Issuance, meaning Superstate helps a company go public on-chain, there should indeed be a minimum unit.

The minimum unit represents the ability to bear risk. Many such funds can only be sold to qualified investors to avoid risks that ordinary investors cannot bear.

Additionally, Superstate and MSX share one common point: the tokenized tokens cannot be freely transferred, but the difference is that MSX cannot be transferred at all, while Superstate can transfer within a whitelist.

Furthermore, Superstate's real-time updates of the shareholder register are maintained by itself, which may involve some centralization issues, such as failing to update in a timely manner, or allowing unqualified investors access, such as certain tokens not being available for U.S. investors.

Although MSX has this point as well, it does not matter for MSX since they do not have KYC.

Then there is the issuance risk. Each project on Superstate will have its own threshold, locking, transfer rules, scope of investors, etc., all of which may be very complex, especially during delivery when it becomes even more complicated.

Correspondingly, MSX's greatest risk lies in SPV mirroring and opacity, which I have explained before, so I won't elaborate further.

(5) Conclusion

Essentially, MSX's Pre-IPO and Backpack's IPO are completely different content. Although both are called IPO, the difference in presentation is very large. Backpack's IPO is merely a channel, and almost all content, except KYC, is provided by Superstate, which remains to be verified for MSX.

Additionally, there are distinctions between SPV mirroring and native stocks, which is an even larger difference, and compliance is reflected here.

Of course, this is still my personal understanding, and my understanding may be wrong.

End.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。