Abstract

This article analyzes how an escalating geopolitical event, specifically the U.S.-Iran conflict, can rapidly transform into a global risk variable within the contemporary financial system. Occurring over the weekend when traditional financial markets are closed, the on-chain markets continued to operate. Cryptocurrency assets and on-chain commodity contracts experienced significant volatility first, completing the initial round of risk expression; prediction markets directly quantified the probabilities of war and political changes, achieving real-time pricing of the event’s trajectory. After the traditional markets opened on Monday, the system confirmed the risk across energy, the U.S. dollar, U.S. Treasury bonds, and risk assets, with risk premiums transmitting layer by layer along the macroeconomic chain. The article notes that in a digital market environment that operates 7×24 hours, risks are no longer priced only after the market opens. Geopolitics are being financialized in real-time, with the market actively participating in the pricing of risk as events unfold rather than merely responding passively to them.

1. Escalation of Conflict: How Geopolitical Events Turn into Global Risk Variables

Recently, tensions between the U.S. and Iran have escalated abruptly. Multiple media outlets reported that Iran’s Supreme Leader, Ali Khamenei, was killed in an airstrike, leading to a rapid deterioration of the regional situation. The combination of military actions and hardline statements transformed the situation from a regional friction point into a global focal point of concern.

Subsequently, the Iranian Islamic Revolutionary Guard Corps announced restrictions on ships passing through the Strait of Hormuz. As one of the world's most important energy transportation routes, this key hub, which has long facilitated the transport of about one-fifth of the world's crude oil and liquefied natural gas, faced severe restriction risks, leading several shipping companies to suspend transit or choose alternative routes.

The impact of the conflict is no longer confined to military dimensions. The Middle East is a core region for global energy supply; disruptions in the Strait of Hormuz directly increase energy risk premiums, which quickly transmit through oil prices, inflation expectations, and capital flows to the global market.

Therefore, this conflict has become a globally significant risk variable with systemic implications. It affects not only the regional security landscape but also the balance of energy supply and demand, the liquidity environment of the U.S. dollar, and the valuation systems of risk assets.

When war escalates to systemic risk, where is this risk first traded? In the structural context where traditional markets operate intermittently while on-chain markets run 24/7, the sequence of price discovery is changing.

2. Weekend Time Window: On-Chain Markets Complete the First Round of Price Discovery

Notably, this escalation of conflict occurred over the weekend. When news broke, most traditional financial markets around the world had already closed: spot gold suspended quotes, crude oil futures ceased trading, and stock markets were closed. Risks had emerged, but the traditional system could not complete pricing instantly. However, on-chain markets continued to operate, shifting risk sentiment to an open pricing venue.

Cryptocurrency Assets Experience First Volatility

Following the conflict news, Bitcoin prices briefly approached $63,000, then rebounded to around $66,000, completing noticeable fluctuations in a short time. This volatility was not merely a reaction to safe-haven buying or panic selling, but a concentrated market game of risk expectations in the absence of traditional anchors like gold and crude oil. When other assets were not tradable, the cryptocurrency market became one of the outlets for expressing risk.

On-Chain Commodity Contracts: Instant Formation of Risk Premium

During the weekend, multiple media outlets reported that on the Hyperliquid platform, perpetual contracts linked to crude oil, gold, and silver saw significant price increases: crude oil perpetual contracts rose approximately 5% to about $70.6 per barrel; gold perpetual contracts increased around 1.3% to about $5,323 per ounce; silver perpetual contracts climbed by about 2% to about $94.9 per ounce. Trading volumes also expanded significantly. The 24-hour trading volume of silver contracts exceeded $227 million, and gold contracts approached $173 million, indicating real capital participation. These prices were genuinely formed in the 24/7 on-chain market, reflecting market participants' immediate judgment of supply risks and geopolitical premiums during traditional market closures.

Monday Opening: Traditional Markets “Catching Up”

When traditional markets reopened, prices quickly adjusted toward the levels reached in the weekend’s chain market. International oil prices opened higher on Monday, with Brent crude soaring to $82.37 per barrel and WTI crude jumping above $75; spot gold broke through $5,300 per ounce; major global stock index futures generally weakened, putting pressure on risk assets. The price sequence was clear: weekend risks emerged; on-chain markets experienced initial fluctuations; traditional markets confirmed and spread the risk on a larger scale on Monday.

Within the traditional market closure window, the on-chain market assumed the role of the first wave of risk expression. This structural time lag is changing the pricing rhythm of global risk events.

3. Prediction Markets: War is Probabilistically Quantified for the First Time

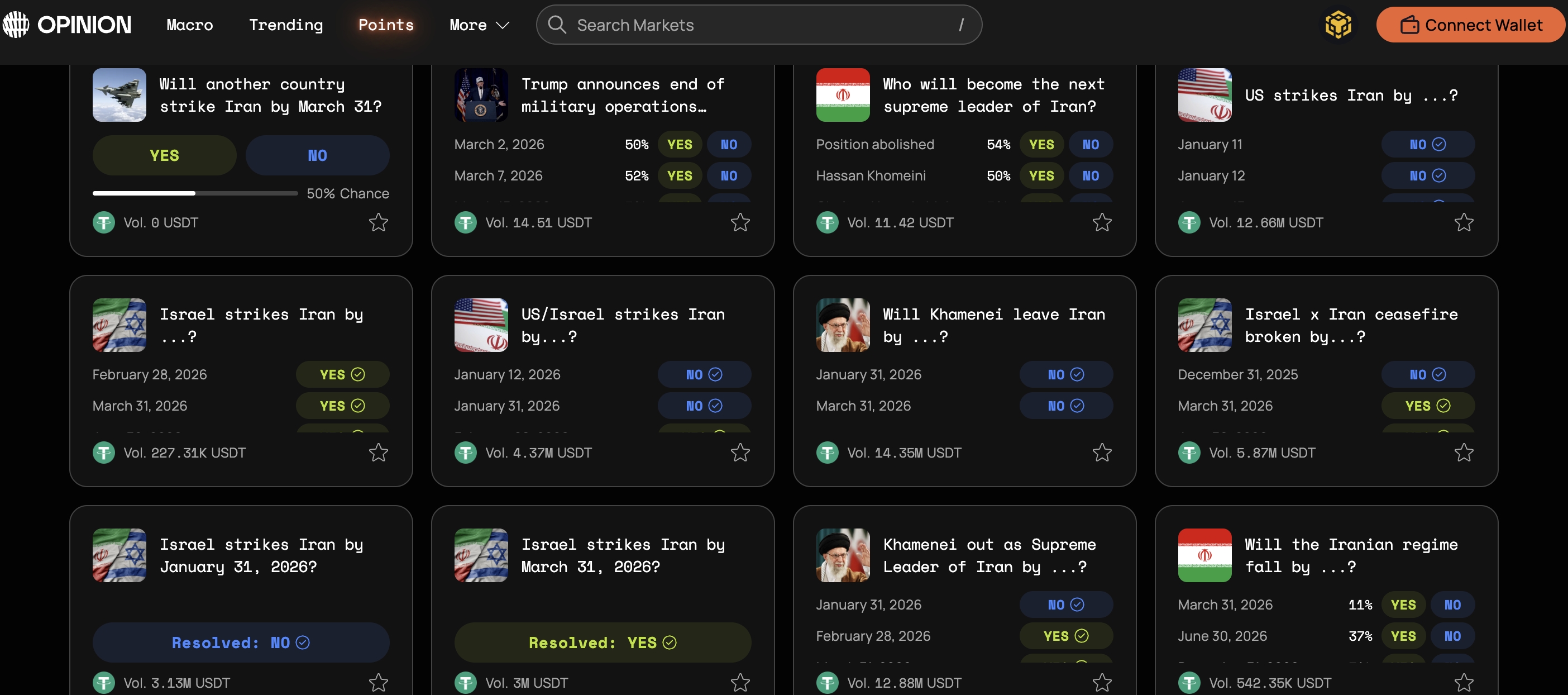

Polymarket: Explosive Pricing at Conflict Nodes

In this incident, the trading volume of contracts related to the escalation of conflict on the on-chain prediction platform Polymarket significantly increased.

The series of contracts questioning “Will the U.S. or Israel strike Iran by a certain date?” (U.S./Israel strike Iran by…?”) had a cumulative trading volume exceeding $500 million, with around $90 million traded on the day of the airstrike, becoming one of the largest geopolitical markets in the platform’s history.

After the confirmation of the leader's death, contracts related to “Will Khamenei lose his position as Iran's Supreme Leader before March 31?” (Khamenei will lose position by March 31?) rapidly settled with a trading volume of about $57 million. Contracts questioning “Will the Iranian regime collapse by June 30?” (Iran regime collapse by June 30?) saw implied probabilities near 50%, indicating that the market was beginning to price deeper institutional risks. These data illustrate that the betting is not a scattered activity, but rather forms concentrated and high-intensity capital participation.

Source: https://polymarket.com/event/khamenei-out-as-supreme-leader-of-iran-by-march31

Opinion: Multidimensional Pricing of Conflict Pathways and Institutional Risks

On Opinion, contracts related to the U.S.-Iran conflict also showed high activity levels. One type of market precisely defines military triggers. For instance, the contract “US strikes Iran by…?” stipulates that it will be considered “Yes” only if U.S. military strikes directly hit Iranian territory or official consulates via drones, missiles, or airstrikes, while intercepted weapons or other forms of military actions are not counted. The trading volume of this contract has exceeded $12.6 million, showing the market's high attention to specific military trigger conditions.

Source: https://app.opinion.trade/search?q=Iran

Another type of market is attuned to institutional risks. The contract “Khamenei out as Supreme Leader of Iran by…?” prices whether Iranian Supreme Leader Ali Khamenei will lose power within a specific time frame. The rules consider resignation, detention, loss of position, or inability to perform duties as criteria, with credible media consensus serving as the basis for settlement, and the trading volume is around $12.9 million. Additionally, similar markets asking “Will the Iranian regime fall by…?” and “Israel × Iran ceasefire broken by…?” probabilistically express regime stability and ceasefire continuity, respectively.

Although the number of related contracts and overall trading volume remain lower than Polymarket, Opinion presents a clearer risk stratification structure: military actions, ceasefire status, leadership changes, and regime dynamics are disaggregated into multiple independent variables priced concurrently. Therefore, war is no longer merely a question of “whether it will happen,” but a risk trajectory that can be segmented, quantified, and continuously adjusted. Prediction markets thus become real-time measuring tools for sovereign risk and institutional stability.

Probability Curves as "Risk Thermometers"

Unlike crude oil or gold, prediction markets do not express risks indirectly through asset prices but directly price the probability of “whether the event will occur.” When the probability of escalation rises, odds increase; when the situation calms, probabilities fall. The odds curve itself becomes an immediate metric for risk sentiment. Some analyses indicate that in the few hours before the airstrike news spread widely, a small number of new wallets concentrated on buying related contracts and profited after the event's confirmation. This phenomenon has sparked discussions on whether information entered the market in advance, highlighting the time sensitivity of prediction markets.

Traditional markets usually reflect outcomes through rising oil prices or falling stock markets; prediction markets directly trade “whether it escalates” or “whether it spreads.” The former influences pricing, while the latter shapes the pricing path. When traditional markets have not yet opened, risks have already been quantified and betted on in the on-chain space.

4. Traditional Asset Opening Confirmation: How is Risk Premium Transmitted?

When the on-chain market first fluctuates, actual cross-asset linkages occur after the traditional market reopens.

Energy: The First Station of Risk Premium

Energy remains the first station of risk premium. The Strait of Hormuz carries approximately 20% of global crude oil transportation; as long as the market is concerned about potential supply disruptions, oil prices will factor in risk premiums ahead of time. The escalation of conflict drives oil prices upward, thus raising inflation expectations and influencing interest rate policies and corporate cost structures.

U.S. Dollar and Treasury Bonds: Tug of War Between Safety and Inflation

In times of rising uncertainty, funds typically flow into the most liquid assets, leading to short-term benefits for the U.S. dollar and Treasury bonds. The dollar strengthens, and Treasury yields temporarily decline, reflecting increased safe-haven demand. However, if the conflict persists and inflation expectations rise, Treasury yields may face a tug-of-war between safe-haven buying and inflationary pressures.

Positioning of Risk Assets and Bitcoin

Gold fulfills traditional safe-haven functions, crude oil embodies risk premiums, and Treasury bonds provide liquidity safety nets. Bitcoin’s performance is more akin to a highly elastic risk asset. In the early stages of the conflict, it did not rise unilaterally but rather fluctuated significantly, revealing its high sensitivity to liquidity and risk appetite. Therefore, in the initial phase of extreme uncertainty, Bitcoin resembles a high-beta risk asset rather than a pure safe-haven instrument.

Overall, the on-chain market first expresses risk, prediction markets quantify that risk, and traditional assets confirm it systematically after opening. Risk premiums transmit layer by layer through energy, interest rates, and asset valuations, ultimately forming a linked response across global markets.

5. Structural Change: Is the Risk Pricing Mechanism Migrating?

The significance of this event may lie not only in the conflict itself but in how risk is priced.

Geopolitics are being Financialized in Real-Time

In the past, geopolitics remained largely within the realms of news and diplomacy; today, it is being real-time financialized. Whether war escalates, sanctions are implemented, or election outcomes evolve can all be betted on, hedged, and quantified in the market. Risks are no longer interpreted only in hindsight but are traded during their occurrence.

On-Chain Markets Become 7×24 Hour Risk Buffers

On-chain markets have begun to assume a new function. Traditional markets have weekend closures and holiday suspensions. When major events occur during these gaps, prices cannot reflect sentiment instantaneously. However, the on-chain market, functioning 7×24 hours, serves as the buffer for the first wave of emotional release. Prices and probabilities fluctuate there first, and when traditional markets open, larger-scale confirmations and spreads occur.

Price Discovery Authority is Marginally Migrating

This difference in time structures is leading to a deeper transformation: the marginal migration of price discovery authority. If on-chain contracts fluctuate first, and if prediction market odds curves shift ahead of oil prices and stock indexes, will institutional investors begin to monitor these data? Will macro models incorporate on-chain volatility as a reference variable? Will media and traders view prediction market probabilities as early warning signals of risk?

These questions are yet to reach conclusions, but the direction is becoming clear. The “first expression” of risk is migrating from the opening bell of traditional exchanges to the 24/7 running digital markets. When war can be traded in real-time, markets no longer passively respond to event outcomes, but actively participate in the risk pricing process itself.

References

1.Crypto market hedges Iran war risks with 24/7 oil and gold trading: https://www.thestar.com.my/business/business-news/2026/03/02/crypto-market-hedges-iran-war-risks-with-247-oil-andgold-trading

2.Polymarket u.s./israel strike iran by…?”: https://polymarket.com/search?_q=u.s.%2Fisrael-strike-iran-by%E2%80%A6%3F%E2%80%9D

3.Khamenei will lose position by March 31?: https://polymarket.com/event/khamenei-out-as-supreme-leader-of-iran-by-march-31

4.Iran regime collapse by June 30?: https://polymarket.com/event/will-the-iranian-regime-fall-by-june-30

5.Oil surges 8% as Iran conflict disrupts Middle Eastern flows: https://www.reuters.com/business/energy/oil-jumps-us-iran-conflict-escalates-disrupts-shipping-2026-03-01/

6.Prediction markets find war profitable — $529 million traded on US-Iran bets, insider trading suspected by some accounts: https://www.livemint.com/market/polymarket-sees-529-million-traded-bets-tied-us-strike-iran-war-profit-insider-trading-concern-1-million-wallet-accounts-11772330241264.html

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。