"We went from eggs to yen" is a quote from the financial memoir of CME legend Leo Melamed, witnessing that eggs were once one of the most active futures products in the world.

In the first half of the 20th century, egg futures were one of the hottest trading instruments in Chicago. The trading volume in some years was second only to that of grain commodities, and there were even instances where futures trading volumes significantly exceeded physical circulation volumes.

The predecessor of the Chicago Mercantile Exchange (CME) was actually called the "Chicago Butter and Egg Board", which was the foundation of the entire derivatives empire, and as the name suggests, this exchange initially only traded two items: butter and eggs.

After the 1970s, egg production in the United States rapidly industrialized, the cold chain matured, and price fluctuations were gradually "ironed out." As uncertainty began to fade, the voices in the trading pits also quieted. In 1982, egg futures officially exited the Chicago Mercantile Exchange. It didn't collapse with a bang but seemed to be quietly turned off by the times.

In 2013, the Dalian Commodity Exchange on the mainland reignited this commodity. At that time, China's egg production industry was still highly fragmented, with dramatic price fluctuations, and the demand for hedging was real and urgent. Trading moved from the shouting floors in Chicago to the electronic matching screens, and participants transformed from colorful-vested floor traders to industry clients and quantitative accounts focused on candlestick charts.

Egg futures trading did not disappear; it merely migrated. And today, this migration has taken another step forward. The place to trade egg prices has moved to Polymarket.

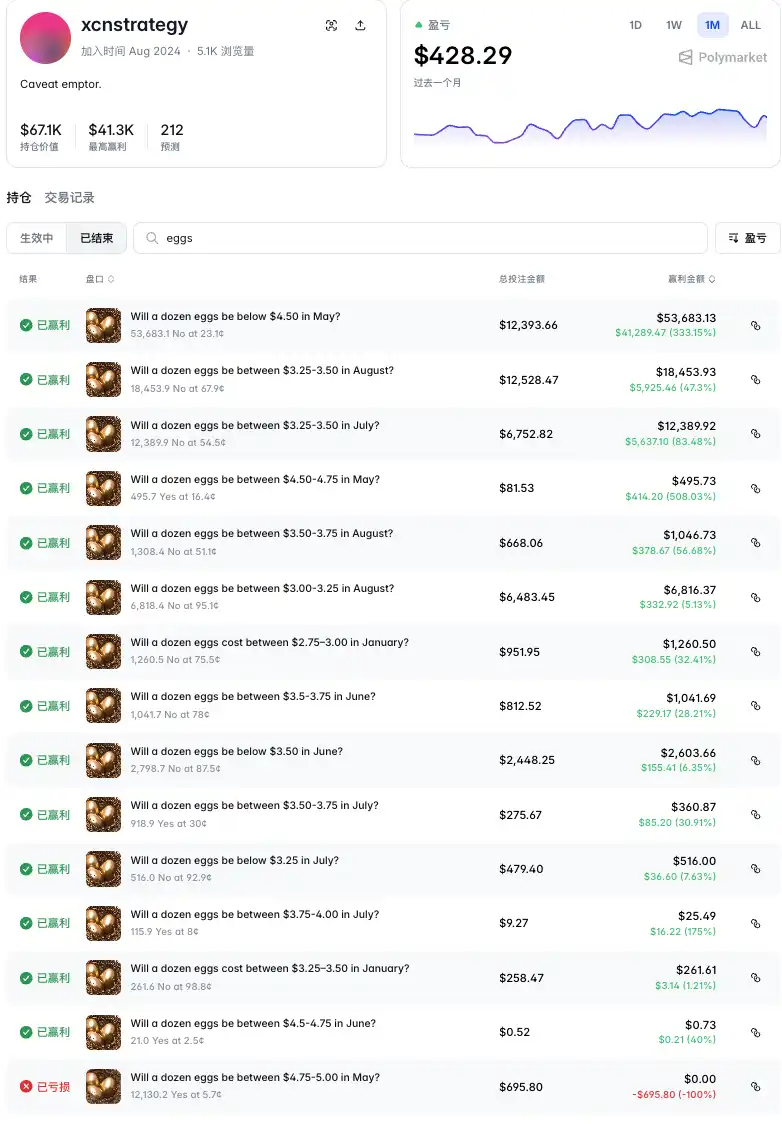

A trader with the ID "xcnstrategy" established positions predicting egg prices for multiple expiration months in January, May, June, July, and August, most of the trades being short "Yes" for certain price ranges, betting that eggs would not be at a certain price level. The total amount bet was $44,800, with profits nearing $100,000, and 15 trades were profitable except for the first one.

The most recent trade was also the most profitable, investing $12,393 betting on "No" that "a dozen eggs will be below $4.50 in May," yielding a profit of $41,289 (+333%).

Speculation about the true identity of xcnstrategy has led many to believe he is likely someone with a background in commodities markets or agricultural data analysis, concluding that the surge in egg prices in the U.S. due to avian influenza in 2025 is a short-term phenomenon and the market has overestimated the probability of sustained high prices; others believe he is a stakeholder in the egg industry, hedging against the volatility brought by the industry itself.

Eggs are just one example; the traditional asset classes that can be traded on Polymarket are far more than we can imagine: from crude oil (CL), gold (GC), and silver (SI) to various foreign exchange prices and housing data, all can be found in the market on Polymarket.

The continuous 24/7 trading is one of the biggest advantages of trading such markets on Polymarket; this advantage becomes particularly evident when traditional financial markets are closed, as seen last weekend when tensions escalated between the U.S. and Iran.

In this respect, the advantages of Hyperliquid are also the same. The perpetual contracts linked to crude oil and gold on Hyperliquid have no expiration dates and operate continuously 24/7.

This leads to an increasingly hard-to-ignore phenomenon: the crypto market is quietly taking over the pricing function of traditional financial markets, especially when the latter are closed.

Traditional futures markets have fixed trading hours, with CME's oil and gold contracts not trading on weekends, and the foreign exchange market experiencing liquidity depletion late at night. This means that when geopolitical shocks erupt suddenly after Friday's close, participants in the traditional markets can only wait in the dark, unable to hedge, express opinions, or price.

Last weekend's escalation of the U.S.-Iran conflict is the latest validation of this. According to Bloomberg, a large number of traders rushed into Hyperliquid around the outbreak of the conflict, trading perpetual contracts linked to crude oil and gold to respond to geopolitical shocks—while the traditional markets were closed, the crypto derivatives market became the only place with lights on. Investment firm executive Avi Felman previously predicted that "Hyperliquid will become indispensable for fund managers due to its 24/7 trading." This assessment was specifically validated during this round of conflict.

At the same time, the tokenization of gold is accelerating another line of logic: when gold exists in the form of on-chain tokens and is continuously priced in decentralized markets, it no longer needs to wait for the London Metal Exchange or CME to open. To some extent, the tokenized gold market is acting as a "shadow pre-market" for traditional gold markets, providing early pricing for gold over the weekend, with price discovery occurring before traditional markets open.

In 2020, FTX, then still the world's second-largest trading platform, launched stock tokens, allowing platform users to trade shares of Tesla and Nvidia using stablecoins. The idea was to gain pricing power, so when the U.S. stock market was closed, FTX's Tesla tokens could fill the market gap, allowing users to trade Tesla stocks when the company announced its latest model on Saturday, thus impacting NASDAQ's opening on Monday.

Unfortunately, due to liquidity issues, the pricing effect ultimately did not materialize. Six years later, this vision has returned with a twist. Nowadays, Polymarket and Hyperliquid are positioned far beyond mere cryptocurrency trading platforms; Polymarket is now an officially recognized polling agency and information exchange center, while Hyperliquid has also been regarded as a new type of fully-owned product trading platform.

The right to price discovery has always been one of the core powers in financial infrastructure. The butter and egg merchants in Chicago established CME because they needed a place to discover prices and transfer risks.

More than a hundred years later, the same logic is being replayed on-chain, only the medium has changed.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。