Author: stein

Translation: Block unicorn

What is Private Credit?

Private credit refers to debt financing provided by non-bank lending institutions, such as direct loans to medium-sized enterprises, real estate loans, trade financing, consumer loans, and structured credit, which are not issued or traded in the public market. Unlike public bonds, these loans are negotiated bilaterally, recorded privately, and are typically held by the originating fund until maturity.

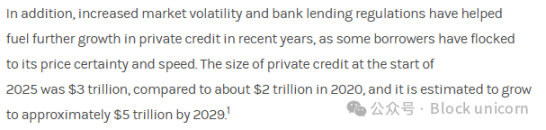

After 2008, with banks shrinking their operations under new regulatory constraints (Basel III), the private credit asset class grew rapidly. Investment funds, private equity firms, and specialized finance companies rushed in to fill the lending gap. By 2020, the global private credit market size had grown to approximately $2 trillion. By early 2025, the market size reached $3 trillion and is expected to reach $5 trillion by 2029 (Morgan Stanley, McKinsey).

Traditional private credit markets face three core structural issues that make them ideal for tokenization.

- Insufficient liquidity: Once a fund grants a loan, it typically holds it until maturity. There are currently no mature trading platforms for trading shares of private loans. Secondary market transactions are customized, slow, and buyers must conduct thorough due diligence.

- Lack of transparency: Fragmented data means that investors often cannot clearly understand leverage ratios, collateral quality, or real-time performance. Reports are released at most quarterly, leading to significant information asymmetry.

- High barriers to entry: Minimum investment amounts range from $5 million to $10 million, with multi-year lock-up periods and accredited investor requirements, effectively excluding everyone except the largest institutional investors.

What is Tokenized Private Credit?

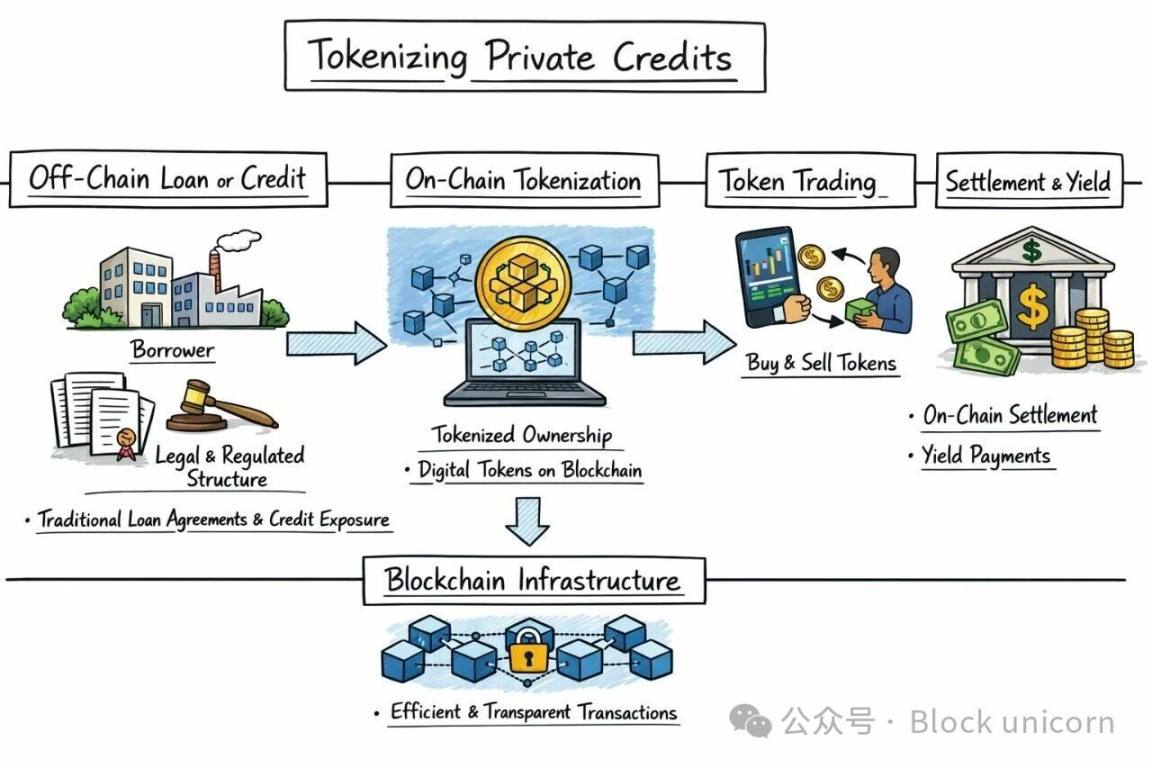

Tokenized private credit is the process of converting private loans or debt instruments into blockchain-based digital tokens, which represent a claim on loan cash flows, ownership of fund shares, or rights to interest and principal payments.

In practice, the underlying loans or credit exposure remain off-chain, retaining the same legal structure and regulatory manner as traditional markets. However, ownership claims or revenue rights are represented in the form of tokens on-chain. These tokens can be issued, traded, and settled more efficiently using blockchain infrastructure.

The process works as follows

- Initiation: The initiating institution constructs private credit products (SME loans, structured credit, trade financing, home equity lines of credit, etc.).

- Legal Packaging: Create a legal entity (usually a special purpose entity) to hold the loan exposure.

- Tokenization: Mint digital tokens representing ownership of that credit or cash flow rights.

- Subscription: Investors subscribe using fiat currency or stablecoins and receive tokens in return.

- Performance: Loans continue to perform off-chain, but payments, investor reports, and ownership records are managed on-chain.

Two Tokenization Models

This is a key distinction that most articles overlook.

Representational Tokenization: The blockchain merely acts as a transparent record system for off-chain loans. These tokens are non-transferable or tradeable, and the blockchain only provides operational upgrades (immutable ledger, real-time tracking). Figure primarily adopts this model.

Figure's data

Distributable Tokenization: Loans are natively issued and held on-chain in transferable token form. Investors can hold, trade, and manage these tokens within the DeFi ecosystem. Platforms like Maple, Centrifuge, and Tradable are closer to this model.

Data from Tradable, Maple, and Centrifuge

According to research data from HTX_Global, of approximately $19 billion in active on-chain private credit loans, only about 12% are held in transferable, distributable tokenized form. The rest are "recorded but non-transferable." This is an important nuance in assessing the true state of the market.

Evolution Process

Stage 0: Prehistory (2017-2019)

2017: Centrifuge was founded as one of the first DeFi projects to integrate RWA. Initially focused on tokenizing invoices and receivables through its Tinlake protocol (an open asset pool driven by smart contracts).

2018: Figure was founded by Mike Cagney (former CEO of SoFi). The company focuses on integrating blockchain into financial services and first launched a blockchain-based home equity line of credit (HELOC). Figure developed the Provenance Blockchain Foundation (Layer 1 based on Cosmos SDK) as its infrastructure.

2019: Cadence (later renamed Percent) launched its first tokenized private debt product, attempting to reduce backend costs by standardizing and reusing structured product smart contract templates. Early challenges arose, such as on-chain contract mirroring costs being higher than expected and insufficient demand for tokenized debt due to a lack of a sufficient number of crypto-native investors for effective investment.

Stage 1: DeFi Integration and Early Development (2020 - 2021)

2020 (Centrifuge V1): Centrifuge proved that tokenized private credit could serve as collateral in DeFi, notably integrating with SkyEcosystem.

Early 2021: Goldfinch launched, focusing on decentralized credit in emerging markets. The protocol allows cryptocurrency investors to provide capital to fintech companies in developing countries (Indonesia, Mexico, Peru, Kenya). It adopts a dual pool model: retail funds enter a senior pool for stable returns (annual yield of 7-10%), while junior supporters elected by the community provide first-loss capital in exchange for higher yields.

2021: Maple launched as an institutional lending platform on Ethereum, using "pool representatives" for credit assessment. Initially serving institutional borrowers like hedge funds, trading firms, and cryptocurrency market makers. TrueFi and Clearpool also entered the market.

2021: Figure began settling home equity lines of credit (HELOC) on Provenance Blockchain Foundation, shortening financing cycles from months to days and eliminating intermediaries.

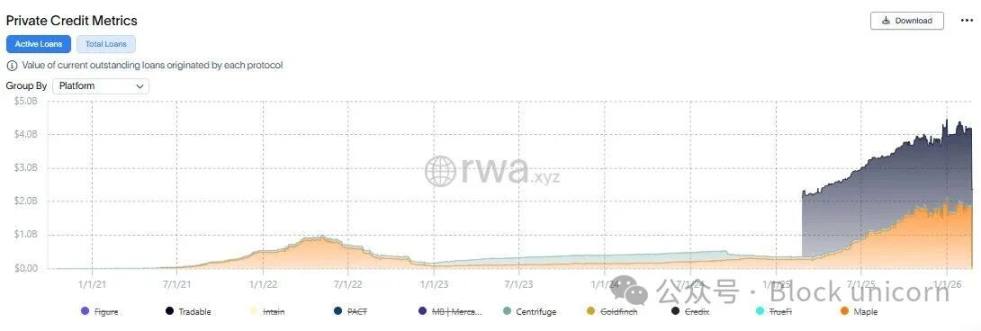

Mid-2021 to end of 2022: The on-chain private credit market peaked at nearly $1.5 billion in active loans, primarily driven by cryptocurrency trading and market makers.

Stage 2: Crypto Winter and Reset (2022)

2022: The crypto winter severely impacted on-chain private credit. Maple defaulted on $69.3 million in debt during institutional turmoil (FTX/Alameda/3AC collapse). Low collateral loans to crypto companies proved disastrous.

Goldfinch faced bad debts through its emerging market products.

The total value of on-chain private credit plummeted from its peak.

Lending to crypto-native companies (trading desks, market makers) created circular risk. The market began to shift towards real-world loans as a catalyst for recovery.

Stage 3: Real World Transformation and Institutional Investor Entry (2023 - 2024)

2023 (Centrifuge V2): Multichain expansion and institutional-grade fund structural tools. New growth primarily comes from real-world loan businesses.

2023: Hamilton Lane tokenized its Senior Credit Opportunities (SCOPE) private credit fund on Ethereum and Polygon through Securitize, lowering its minimum investment from $5 million to $20,000.

2022 (earlier): KKR launched its healthcare strategic growth fund on the Avalanche blockchain via Securitize.

2024: Hamilton Lane expands SCOPE to the Solana chain through the Libre platform.

Mid-2024: Centrifuge's outstanding loan balance reaches $289 million, mainly invested in consumer asset-backed securities (ABS), real estate bridge loans, and trade financing. Over 85% of loans issued through Centrifuge are financed by the Sky protocol (originally MakerDAO).

2024 (Centrifuge V3): Interoperability, standards, and composability. Development of ERC-7540, an extension of ERC-4626, standardized for asynchronous investments and redemptions.

End of 2024: BlackRock launches BUIDL (tokenized money market fund), reaching an asset management scale of $1.2 billion within six months.

Early 2024: The scale of tokenized private credit reaches approximately $8 billion, primarily driven by Figure, Centrifuge, Maple, Goldfinch, Clearpool, and Credix.

Stage 4: Institutional Accelerated Development (2025)

January 2025: Apollo launches a tokenized diversified credit fund (ACRED) on six blockchains via Securitize. By November 2025, its asset management scale reaches $170 million.

February 2025: Figure partners with Sixth Street to establish a joint venture (Sixth Street commits to provide $200 million equity to Figure Connect for ongoing private credit liquidity).

Mid-2025: Figure has tokenized over $13 billion in loans (mainly home equity lines of credit) and has become the largest non-bank home equity line of credit lender in the U.S., settling over $600 million in loans monthly on Provenance.

September 2025: Figure is listed on NASDAQ with the stock code FIGR, raising $787.5 million through its IPO, achieving a valuation of $5.3 billion (later reaching $7.6 billion).

October 2025: The total amount of tokenized real-world assets (RWA) reaches approximately $33 billion, with private credit accounting for $16-18 billion.

By November 2025: Active on-chain private credit exceeds $18.91 billion, with cumulative issuance amounting to $33.66 billion (data from RWA.xyz). The value increased by 82% compared to the end of 2024, reaching $17.9 billion by October 2025 (data from PwC).

Securitize has issued nearly $4 billion in tokenized assets and is a tokenization partner of BlackRock, Apollo, Hamilton Lane, KKR, and VanEck.

Stage 5: Current Status (Early 2026)

February 2026: Figure Technologies currently leads the market with approximately $15 billion in active loans, accounting for 75% of the market’s total active loan amount of around $20 billion (data from RWA.xyz). The total amount of tokenized assets on the Provenance platform reaches $1.2 billion in TVL.

Hamilton Lane and Securitize launch an RWA-backed stablecoin on the X Layer platform of OKX, which is supported by tokenized exposure from Hamilton Lane's SCOPE fund and adopts a dual-token structure that separates revenues from the stablecoin itself.

The tokenized private credit market continues to expand into the realm of DeFi composability: Apollo's ACRED fund is being used in leverage cycles on platforms such as Morpho and Kamino, demonstrating that on-chain assets can be combined in ways that traditional finance cannot achieve.

Industry expectations for 2026 include major institutions "transitioning from pilot phases to large-scale, production-ready products," and on-chain credit potentially receiving ratings from traditional rating agencies.

How Tokenized Private Credit Actually Works

Token Standards and Structures

Loan-specific tokens: Each loan is tokenized into one or more ERC-20 tokens, representing a claim on the cash flows of that asset. For example, a real estate loan institution issues tokens that entitle holders to mortgage repayments. These tokens often constitute securities and must be issued under exemption rules (qualified investors are subject to Reg D, broader but limited retail investors are subject to Reg A+).

Lending pool model: Lenders contribute to a public funding pool, which allocates loans to borrowers. Loans are presented on-chain in the form of debt certificates (non-tradable tokens) associated with NFTs, while lenders receive ERC-20 tokens representing their share of the funding pool. Smart contracts enforce terms, meaning that if the borrower fails to repay the loan, it goes into default and triggers predetermined remedies.

Fund tokenization: The fund structure itself is tokenized (e.g., Hamilton Lane's SCOPE). Investors hold tokens representing fund shares rather than direct claims on individual loans. This is the current mainstream institutional model.

Key Standards

ERC-20: Standard fungible tokens used for lending pool shares and fund tokens

ERC-721 (NFT): Used to represent certain loans in some protocols

ERC-4626: Standard for tokenized vaults for yield-bearing positions

ERC-7540: An extension of ERC-4626 for asynchronous investments and redemptions, leading DeFi RWA standard developed by Centrifuge

Tranching: Senior/junior tranching structure (Centrifuge's DROP/TIN model) allows for risk-return differentiation

Lifecycle Management

Smart contract handling:

- Loan issuance and interest accumulation

- Payment collection and distribution to token holders

- Maturity redemption and principal return

- Compliance checks (whitelisting, KYC/AML, jurisdiction restrictions)

- Default trigger mechanisms and waterfall repayment mechanisms

Transparency Issues

This section of the article applies the RWA transparency framework, which distinguishes between what is actually allocated and what is merely represented on the chain.

What Figure's Dominance Really Means

Figure accounts for approximately 75% of tokenized private credit share. However, Provenance is a purpose-built chain whose smart contracts require governance approval. As Glider co-founder Brian Huang pointed out:

"Unless assets have composability, on-chain assets are no more useful than off-chain. Provenance lacks composability."

This means that, measured in dollar value, the vast majority of tokenized private credit is essentially an operational upgrade rather than a distributable, DeFi-composable asset. These loans are not tradable tokens that investors can freely transfer, combine, or use across ecosystems. This is critical for transparency analysis.

The 12% Issue

According to research data from HTX, only about 12% of on-chain private credit is held in transferable tokenized form. The rest are recorded but non-distributable. When someone says tokenized private credit is worth $20 billion, the more accurate figure for truly distributable, composable tokenized credit should be between $2 billion and $3 billion.

On-Chain Content That is Actually Verifiable

Fully verifiable: Token ownership, transfer history, fund share balances, smart contract terms, compliance status (whitelisting), and payment and distribution status.

Partially verifiable: Total outstanding loan value (depends on oracle/report accuracy), collateral ratios (for over-collateralization models).

On-chain unverifiable: Borrower's credit status, actual loan performance (still reliant on off-chain reporting), collateral quality of off-chain assets, real default rates, recovery rates.

Underlying credit risk assessment, underwriting, and counterparty assessment still occur entirely off-chain. Blockchain provides transparency at the token layer but does not necessarily provide transparency at the asset layer.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。