Bitcoin should be at least $150,000 now; everyone knows this in their heart.

But why can't the actual price reach this? A federal lawsuit filed yesterday in Manhattan provides the answer.

Let’s connect three things for the first time: a federal insider trading case involving a private group chat called "Bryce's Secret"; a program that suppresses Bitcoin prices by selling off at 10 a.m. on the dot every day until the end of 2025; and an undisclosed derivatives book — which could turn the largest Bitcoin ETF holdings in the world into a tool for suppressing Bitcoin.

All three clues point to the same name: Jane Street Capital.

Intern

The story begins with an intern named Bryce Pratt.

Bryce interned at Terraform Labs, the Singapore company behind the algorithmic stablecoin UST and its token Luna. In September 2021, he left Terraform and joined Jane Street as a full-time employee.

Jane Street is also where SBF learned to trade before he founded FTX and Alameda Research. Many of his colleagues either came from Jane Street or have deep ties to it.

According to a lawsuit filed by Terraform's bankruptcy trustee Todd Snyder, Bryce became a bridge between his old employer and his new employer through a chat group referred to as "Bryce's Secret" in court documents.

The lawsuit alleges that Jane Street used this group to gain significant non-public information about Terraform's internal funding movements.

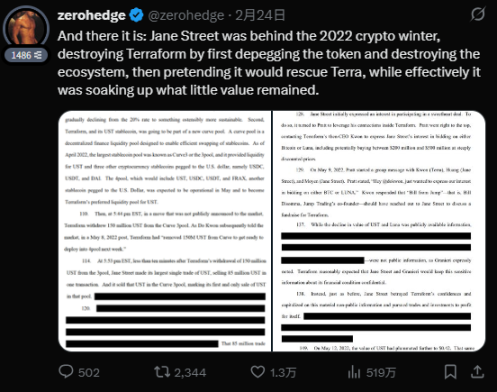

A crucial moment occurred on May 7, 2022. Terraform withdrew $150 million in UST from a decentralized trading platform called Curve 3pool — this was the main liquidity pool for the stablecoin. Within ten minutes of the withdrawal, before Terraform had publicly announced any news, a wallet linked to Jane Street pulled $85 million in UST from this pool.

Then, everyone is familiar with what happened next. The selling pressure caused UST to start decoupling, and within days, Luna's algorithmic mechanism completely broke down, leading to rampant token issuance, a $40 billion market cap evaporation, and retail investors losing everything.

The lawsuit states that Jane Street precisely closed its positions "a few hours before the collapse of the Terraform ecosystem," avoiding over $200 million in potential losses. The documents state clearly: these trades "could not have been executed without insider information."

Jane Street's response was that the lawsuit is "ridiculous" and "unfounded," claiming that the losses of Terra and Luna holders were the result of fraud by Terraform itself.

By the way, Do Kwon is currently serving a 15-year prison sentence. Snyder also sued Jump Trading for the same reason, seeking $4 billion in damages — it seems this is a systematic investigation into the behavior of institutions during the Terra crash, not just targeting Jane Street alone.

The Clock Starts Ticking

Starting from the end of 2024, intensifying into 2025, a phenomenon emerged in Bitcoin pricing that left traders baffled:

Every day at 10 a.m. (Eastern Time), just as the U.S. stock market opens, Bitcoin would consistently face a fierce sell-off. This drop is very precise; it is clearly the work of a program, and the magnitude is outrageous, completely unrelated to the overall market movements. It specifically blows up highly leveraged long positions, triggering a chain reaction of liquidations, and then within hours, the price bounces back up.

The founders of blockchain analytics firm Glassnode recorded this pattern. They tracked several months of trading data and concluded that the trend was incredibly obvious. Charts from last December showed that Bitcoin dropped from $89,700 to $87,700 within minutes of the market opening at 10 a.m., with $171 million in long positions evaporating instantly, and then the price gradually climbed back up.

This happened every day, without fail.

As a designated market maker and authorized participant for multiple Bitcoin ETFs, Jane Street has both the spot market and the infrastructure for large-scale sell-offs. By opening and hammering the market at the thinnest liquidity, they can depress prices, trigger a cascade of liquidations among leveraged traders, and then buy back at a lower price. This operation is seamless: first create the drop, then scoop up the low.

Then something interesting happened.

The founders of Glassnode stated that just after the lawsuit documents from Terraform were made public early last year, this daily flash crash stopped. Bitcoin prices appeared to stabilize significantly. This was no coincidence — it was clear that the company suddenly realized that lawyers would come investigating.

However, this stability did not last long. By the third quarter of 2025, the 10 a.m. sell-offs returned, and by the end of the year, they had completely resumed their former "glory."

In short: Jane Street was hesitant to hammer prices when under lawyer scrutiny, but resumed their actions once the coast was clear.

Quantitative Machines

In the 13F filing for the fourth quarter of 2025, Jane Street disclosed that it held over 20.31 million shares of IBIT (BlackRock's Bitcoin ETF), valued at about $790 million. In just that quarter, they added 7.1 million shares, valued at $276 million. At one point last year, their total holdings of IBIT approached $2.5 billion.

At the same time, they also aggressively bought MicroStrategy’s stock, increasing their holdings by 473%, holding over 950,000 shares worth approximately $121 million. In contrast, BlackRock and Vanguard were offloading MicroStrategy shares, selling billions.

Many crypto media outlets saw this 13F filing and remarked, "Wow, institutions are getting involved!" But those who truly understand market structure immediately recognized something was off.

Does this look like a bullish stance on Bitcoin, ramping up the position? That's because you don’t understand what Jane Street is doing.

Jane Street is one of only four firms that can "create and redeem" IBIT in kind, the other three being Virtu Americas, JPMorgan, and Marex. It is also an authorized participant for Fidelity and WisdomTree's Bitcoin ETFs. What does this position mean? It means they have direct access to the pipeline that connects ETF prices to real Bitcoin. They can enter and exit ETFs using actual Bitcoin, arbitraging between fund prices and spot prices, and can accumulate what regular people would have no chance of hoarding.

In other words, Jane Street holds the "pipeline" linking Bitcoin ETFs and real Bitcoin, while others do not.

Invisible Books

Former hedge fund manager Michael Green said those interpreting Jane Street's 13F filing as a bullish signal make him feel "uneasy." He pointed out that Jane Street's IBIT holdings are "almost certainly offset by undisclosed options and futures positions," adding, "They are definitely not building a position in Bitcoin; this is standard market-maker operation."

Former proprietary trader Ryan Scott was more direct: "Anyone who takes this as good news is essentially a 'death row inmate' in finance. This should be understood as: 'Guess who else is holding undisclosed hedging derivatives?'"

Nicolas Batiat summarized it in one sentence: Jane Street holds IBIT to sell options, arbitrage, and engage in various quantitative trading strategies.

What does this mean for anyone holding Bitcoin or IBIT?

The 13F filing only discloses long equity positions, but does not need to disclose options, futures, or swaps. So when Jane Street claims to hold $790 million in IBIT stock, you have no idea if these stocks are hedged with put options, if they are offset by short futures, or if they are bundled in some options combination — it’s possible that their actual risk exposure to Bitcoin is zero, or even negative (that is, they are short).

The public only sees them buying and buying. But their actual position could likely be a massive short — because that half that’s been hedged is invisible under the current disclosure rules.

The 13F is like a photo that only captures half of a person’s body; only Jane Street knows what the other half looks like.

So every Bitcoin holder must ask an unavoidable question: If Jane Street is holding $790 million in IBIT, and also hedged with $790 million in put options or short futures, then the net position is zero. If their derivatives position is larger than their equity position, then the net position is negative — meaning they would profit if Bitcoin drops.

In this scenario, they have ample motive to leverage their privileged status as an authorized participant to hammer the spot prices, triggering others' liquidations, and pocketing the middle margin.

The question arises: Is Jane Street bullish or bearish on Bitcoin? Under the current disclosure rules, they don't have to answer.

Precedent

Jane Street's behavior in the Bitcoin market has not been examined by regulators, but it has been scrutinized in other markets.

In 2025, the Indian Securities and Exchange Board issued a lengthy 105-page penalty order accusing Jane Street of manipulating the BANKNIFTY index options in the Indian market.

The Indian SEC found that Jane Street made 365 billion rupees (about $4.3 billion) over two years by coordinating trades in the spot and derivatives markets, making as much as 73.5 billion rupees (about $8.8 billion) in a single day. The regulators stated bluntly: this behavior would be illegal in any country with normal financial regulation. They then restricted Jane Street's trading activities.

Take a look at their operational pattern in the Indian index derivatives: using speed and scale advantages, they created turmoil in one market and then harvested profits in the derivatives market above it.

The question now is, is the Bitcoin market the same?

21 Million

The hard cap of 21 million is maintained collectively by a network of Bitcoin nodes around the world.

But for this cap to be effective, there is a premise: price discovery must be genuine, and the market must reflect real supply and demand. Institutions hold Bitcoin or Bitcoin-related products because they genuinely believe in them, not because they use them as "raw materials" for invisible derivatives strategies.

In other words, the 21 million cap only has meaning if it is established on the basis of "the market is honest."

But what about now?

Jane Street is one of the four companies holding the keys to Bitcoin ETF infrastructure. It is facing federal lawsuits, accused of insider trading to take advantage, contributing to a $40 billion market cap loss. It has also been charged with systematically suppressing Bitcoin prices for several months using programmed sell-offs. It holds the largest publicly accessible ETF positions, while also maintaining a derivatives book — one that could make it appear bullish, but in reality make it bearish.

So, the 21 million cap is just a number in front of Jane Street. Because it can create "synthetic" Bitcoins above its ETF inventory through undisclosed derivatives.

Bitcoin is indeed scarce at the protocol level, but the price discovery mechanism built on top of it has already been disrupted by a company that treats privileges as a cash machine. And the current disclosure rules conveniently allow it to continue this way, with no one able to see.

Every Bitcoin holder should know the answer: What is Jane Street's true position — bullish or bearish?

Until we know this, what determines Bitcoin prices is not the market, but Jane Street.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。