Author: FinTax

1 News Overview

On December 22, 2025, the U.S. Securities and Exchange Commission (SEC) launched a rigorous crackdown in the field of cryptocurrency regulation, filing lawsuits against Morocoin Tech Corp., Berge Blockchain Technology Co. Ltd. and other so-called crypto trading platforms, as well as AI Wealth Inc., Lane Wealth Inc. and other investment clubs. The lawsuits accuse them of executing fraudulent trades and misleading issuances through social media, illegally diverting approximately $14 million from retail investors. The SEC has requested permanent injunctions, civil penalties, and the return of illegal gains from the defendants, while warning investors not to rely on group chat information to make investment decisions. This enforcement action highlights the fraud risks present in the crypto market and reflects the SEC's increasingly strict regulatory stance in the crypto space. This article will deeply analyze the key details of the case, examine the SEC's legal basis and regulatory logic, explore its impact on the Web3 financial ecosystem, and provide compliance references for industry participants.

Original complaint link: https://www.sec.gov/files/litigation/complaints/2025/comp-pr2025-144.pdf

2 Dissecting the "Pig Butchering": From Social Group Chats to Fraudulent Trading Platforms

2.1 Fraudulent Platform Trading

According to the complaint, from at least January 2024, AI Wealth, Lane Wealth, AIIEF, and Zenith operated what they called "investment clubs" using WhatsApp, soliciting investors to join group chats through social media advertisements, thereby implementing fraud.

In the WhatsApp group chats, each investment club had one "professor" and one "assistant," where the professor was responsible for posting macroeconomic dynamics or stock market commentary in the group chat, while the "assistant" was responsible for communicating with members. Fraudsters spread investment advice in the group chats, posted screenshots of successful trades, and enhanced retail confidence using AI-generated investment tips and forged endorsement videos from public figures, thereby enticing retail investors to open accounts and invest in the fake crypto trading platforms Morocoin, Berge, and Cirkor. In reality, no transactions occurred on these platforms; they merely designed seemingly professional trading interfaces and fabricated trading data.

2.2 Fraudulent Token Issuance

Subsequently, these investment clubs and trading platforms sold what they called "Security Token Offerings" (STOs), claiming to have obtained government approval and regulatory licenses. They forged issuance qualifications to create an illusion of legitimacy and compliance, deceiving investors into trusting them. In fact, the so-called legitimate issuing companies did not exist; STO products were neither issued on a real blockchain nor had any verifiable transaction history. The STO purchased by investors was merely a digital record on the platform's internal ledger, lacking any actual value or technical support.

2.3 Illegal Fund Diversion

When investors attempted to withdraw their principal and interest, fraudsters further demanded that they pay additional fees such as "prepayments," "taxes," and "margins," and falsely claimed that investors' accounts would be frozen due to SEC investigations, thereby executing a second round of fraud. This not only prevented investors from reclaiming their original funds but also attempted to entice them to invest even more. Through a series of operations, fraudsters illegally diverted at least $14 million from U.S. retail investors and quickly transferred these funds overseas through bank accounts and cryptocurrency wallets. Throughout the process, no real investment activity occurred with these funds.

3 Law and Regulation: Penetrating the Fog of Cryptocurrency "Investment Chaos"

3.1 Why the SEC Intervened in This Case

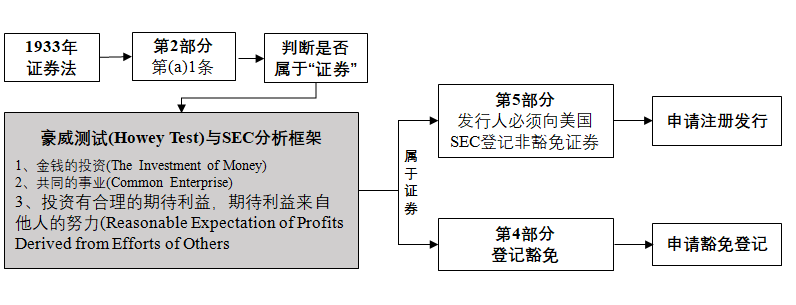

The activities involved in this case essentially fall within the scope of securities regulation and are accompanied by fraud risks, giving the SEC clear grounds for regulatory intervention. The STOs in question claimed to be issued by legitimate companies and used AI investment tips as bait to attract retail investors. Retail investors invested based on trust in the management of investment activities by others and expected returns through project profits. Even though it was later discovered that the STOs and their issuing entities were fictitious, their promotion and operational model conformed to the core elements of the Howey Test — investment in a common enterprise, reliance on the efforts of others to profit — thereby falling under "securities" regulation.

First, the SEC has statutory jurisdiction over fraudulent activities in the issuance and trading of securities, which is the primary prerequisite for its involvement in this case. If crypto assets are determined to be "securities," issuers must fulfill registration obligations with the SEC, unless exemptions apply. The platforms involved did not obtain any licenses, thus evading this obligation, which more easily attracted the SEC's targeted regulation.

Figure 1: The Process Used by the U.S. to Determine Whether Crypto Assets Fall Under Securities Regulation Using the Howey Test

Secondly, the fraud model in question has clear "targeting retail investors" characteristics, aligning with the SEC's recent enforcement direction. On February 20, 2025, the SEC announced the establishment of the Cyber and Emerging Technologies Unit (CETU), whose core responsibilities include "protecting retail investors from the harm of bad actors in emerging technologies," with a focus on retail fraud involving artificial intelligence, blockchain technology, and crypto assets. In recent years, the SEC has had several similar enforcement cases, such as the 2025 SEC's accusations against a Canadian citizen suspected of defrauding Discord retail investors, and the 2024 SEC's accusations of two relationship investment scams involving fraudulent crypto trading platforms NanoBit and CoinW6. These measures have refined the SEC's protections for retail investors and reflect its regulatory emphasis on retail fraud in emerging technology sectors.

Finally, from a regulatory logic perspective, the SEC's enforcement actions are not targeting any specific technological path or business model, but rather based on its core responsibilities — protecting investors, maintaining a fair, orderly, and efficient market, and promoting capital formation. The SEC's intervention in investigations is not only to hold accountable, but also to curb the spread of similar fraud through enforcement actions, preventing further harm to retail investors. With the development of the digital economy, the SEC's responsibilities have extended from traditional securities markets to the trading of crypto assets and other emerging financing and trading models that have securities attributes.

3.2 Legal Basis and Legal Responsibilities

The SEC's accusations revolve around two core securities regulatory laws — the Securities Act of 1933 and the Securities Exchange Act of 1934. The complaint shows that the behaviors of the involved platforms and investment clubs violate the investor protection mechanisms of these laws. First, under Section 17(a) of the Securities Act of 1933, the subjects of the case fabricated platform and trading facts, which meets the criteria for fraud during the issuance and sale stages as stipulated. Secondly, according to Section 10(b) of the Securities Exchange Act of 1934 and its implementing regulation Rule 10b-5, the involved platforms violated the aforementioned anti-fraud provisions, with illegal actions including fraud in the securities trading process and manipulation of investor funds. From the applicable scope, Section 17(a) of the Securities Act of 1933 focuses on fraudulent activities in the issuance and sale phases of securities, emphasizing the issuers' responsibility for false statements or omissions in information disclosure; while Section 10(b) of the Securities Exchange Act of 1934 and its implementing regulations encompass both buyers and sellers in securities transactions with a broader regulatory scope.

As of now, the case is still under trial, and the SEC has requested the court to issue a permanent injunction prohibiting all defendants from continuing any securities issuance or trading activities, while also demanding the defendants return illegal gains and pay civil fines.

3.3 U.S. Regulation Attitude towards ICOs and STOs

In the realm of crypto assets, Initial Coin Offerings (ICOs) and Security Token Offerings (STOs) are two common fundraising methods. ICOs typically issue "utility tokens," which investors purchase primarily to access project platforms or services in the future, theoretically not relying on third-party efforts to profit; whereas STOs issue "security tokens," the value of which is usually tied to traditional securities (such as equities, debts, or revenue rights), and investors rely on the efforts of issuers or managers to obtain profits.

ICO (Initial Coin Offering) | STO (Security Token Offering) | |

Legal Attributes | Generally viewed as "commodities" or "virtual assets" | Clearly defined as "securities" |

Regulatory Authorities | Primarily regulated by the Commodity Futures Trading Commission (CFTC) | Primarily regulated by the U.S. Securities and Exchange Commission (SEC) |

Compliance Requirements | Relatively flexible, must comply with anti-money laundering requirements | Strict, must meet securities registration or exemption requirements |

Investor Threshold | Usually lower, open to the public | Higher, usually limited to accredited investors |

Figure 2: Core Differences Between ICO and STO in the U.S.

For ICOs, the SEC implements differentiated regulatory rules. For non-security ICOs, on one hand, U.S. regulatory authorities have clarified the exemption standards for non-security tokens, simplifying regulatory requirements for utility tokens that only serve functional purposes and do not rely on third-party operations for revenue; on the other hand, regulatory agencies also clearly delineate token classification standards and regulatory boundaries, providing compliance guidance for market participants.

On May 12, 2025, SEC Chairman Paul Atkins proposed a token classification framework, placing network tokens, NFTs, and other non-securities under CFTC jurisdiction to avoid excessive multi-layered regulation stifling technological innovation. At the same time, the CLARITY Act establishes digital commodity standards, whereby tokens that meet decentralization standards will gradually be classified as having commodity attributes, falling under CFTC regulation and exempting certain securities registration requirements, providing a clear path for compliant ICOs and reducing market compliance pressure. For those ICOs determined to be securities via the Howey Test, SEC regulatory rules apply, requiring completion of S-1 registration or meeting Reg D, Reg A+ exemption conditions.

The SEC's stance on the regulation of STOs adheres to a principle of "technology neutrality." On January 28, 2026, three major divisions of the SEC jointly issued a statement on tokenized securities, emphasizing that the issuance format or holder records (such as on-chain/off-chain) do not affect the applicability of federal securities laws. In other words, technology cannot change the economic substance of securities; if a certain type of token aims to provide exposure to the risks of specific securities, or its issuance and trading logic aligns with securities attributes, it should be included under federal securities law regulation.

Overall, the U.S. regulatory authorities' attitude towards token issuance has moved away from a "one size fits all" or purely enforcement-dependent approach, entering a governance phase where categories are clear, and the boundaries between securities and non-securities are more defined, while adhering to the core of substance over form in regulation. Whether ICO or STO, compliant platforms must meet regulatory requirements for anti-money laundering and customer identity verification (KYC/AML), prohibit false statements and misleading promotions, and fully disclose risks.

4 Conclusion

The healthy development of the crypto market relies on the cornerstone of trust. Through this case, we can see that when fraudsters weave scams using crypto shells and complex technologies, they destroy not only the wealth of retail investors but also the market's confidence in the Web3 financial ecosystem. Every successful cash-out of "bad money" may impose a heavier trust cost on the "good money" genuinely dedicated to technological innovation and compliant operations. Avoiding this vicious cycle depends on the joint efforts of regulatory agencies, industry participants, and investors; only in this way can a transparent and robust market environment be established, pushing crypto assets towards a broader stage.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。