Original Title: PURR's HYPE Bid Is Not What You Think

Original Author: @ericonomic

Translated by: Peggy, BlockBeats

Editor's Note: In discussions about HYPE's DAT PURR, the market often focuses on one question: how much "ammunition" does it have left to buy HYPE? However, this article attempts to point out that the key is not the balance, but the mechanism. By interpreting the S-1 document and the issuance logic of DAT, the author reveals a commonly overlooked fact: under the premise of mNAV premium and real liquidity, ATM issuance can allow "firepower" to dynamically expand with transaction volume, rather than being consumed linearly.

This also redefines PURR's behavioral motivation; buying is not just about consuming funds, but may be about maintaining momentum and amplifying future financing capabilities. The article further explains why most DATs fail, while HYPE avoids typical traps in asset attributes and structural design.

The following is the original text:

Most people focus on PURR (formerly known as Hyperliquid Strategies or HSI) for one reason: it is one of the DATs for HYPE (and currently the largest one), continuously accumulating HYPE.

So, the mental model is simple: "PURR has a few million left to hold or push up the price."

This model is useful, but it is not complete.

Because in the background, there is a mechanism that can quietly transform the "remaining firepower" into almost unlimited ammunition.

Once you see this, you will no longer view PURR as a "wallet with a balance." You will start to see it as something else.

Bob Diamond, Chairman of HSI

Before continuing, if you want to delve deeper into PURR and its relationship with HYPE, I recommend first looking at my previous article, especially point 3, where I specifically discuss this issue. Some of the data may be slightly outdated, but we will return to this point later.

As before, all information in this article comes from the official S-1 document. Additionally, I will incorporate some interview content and make reasonable assumptions in the text.

HSI's S-1 Document

Let's get straight to the point.

Besides "PURR may still hold over $100 million to buy HYPE," what else do you need to know?

The core is actually this: their "firepower" may not just be over $100 million; it is not necessarily limited to a fixed-sized treasury; rather, it can be dynamically amplified by mNAV and market liquidity.

To understand this, we need to start with the basic mechanism of DAT.

Basic Mechanism of DAT

Bobby starts calculating

Digital Asset Treasury (DAT) is a type of company whose core goal is to continuously accumulate crypto assets. Their funding sources typically fall into three main categories:

- Investors who want exposure to crypto assets at a discount provide cash, and DAT issues shares to them in exchange, rather than directly giving crypto assets;

- Holders who want to "exit" their crypto positions hand over crypto assets, and DAT pays them cash, but the transaction price is usually below the current market price;

- Issuing and selling new shares (this point is crucial).

PURR's situation is slightly more complex because it is the result of a merger of multiple companies; however, to simplify the discussion, we can assume it primarily raises funds through (1) and (2).

It is important to clarify that their core goal, at least theoretically, should be to maximize shareholder returns, rather than to "pump" a certain crypto asset.

In reality, however, most DATs have followed the old path of "pumping and dumping," ultimately failing almost like a rug pull.

This is where the Market Net Asset Value (mNAV) comes into play. mNAV is an indicator used to determine whether a company's stock is trading at a discount or a premium.

For example, suppose there is a DAT centered around HYPE: holding $1 billion worth of HYPE; with no liabilities and no extra cash; having issued a total of 500,000 shares at a price of $2,000 each.

Then its mNAV calculation is: (500,000 × 2,000) / 1,000,000,000 = 1

mNAV = 1 means the company's stock price is reasonably priced.

If the stock price is higher, mNAV > 1 indicates the company is trading at a premium;

If the stock price is lower, mNAV < 1 indicates a discount.

Now, let's return to the previously mentioned point (3), which is the most critical and easily overlooked aspect of the DAT mechanism: where and how DAT issues new shares. This is where the story truly diverges.

Fork Point: How DAT Issues New Shares

Two paths for issuing new shares

Some DATs choose to issue new shares and sell them at a discount through OTC to specific buyers while setting a short unlock period.

This often triggers the classic "death spiral": once the unlock period ends, buyers sell off in bulk; stock prices drop; if they want to continue financing, they can only offer a larger discount; mNAV further declines; and the cycle repeats.

Another type of DAT chooses to issue new shares through ATM when mNAV is at a premium.

ATM (At-The-Market) issuance refers to: the company gradually issues and sells new shares in the open market while strictly adhering to liquidity and volume constraints.

The pricing of these ATM new shares is not at a discount OTC, but anchored to the market price (usually based on VWAP, volume-weighted average price).

There is a subtle but very important mechanism difference that is particularly critical in practice.

Since ATM issuance references VWAP rather than the latest transaction price, in a strong upward market, the current price often briefly exceeds VWAP. At this point, new shares can be absorbed by the market at a level slightly below the current price without providing any explicit discounts or special terms.

For example: if PURR quickly rises from $10 to $12 in a day, while VWAP is still at $10.80, then ATM new shares are actually sold at a price about 10% lower than the current price. Although, from a regulatory standpoint, they are still "issued at market price."

As higher-priced transaction volumes accumulate, VWAP will naturally rise and catch up with the current price.

As you might expect, PURR chose the second path. It is here that things start to get really interesting.

The next question is: When and how many new shares can PURR issue?

According to some interview content, David Schamis (@dschamis) mentioned that when PURR's trading price exceeds 1 times mNAV, they will consider initiating ATM issuance.

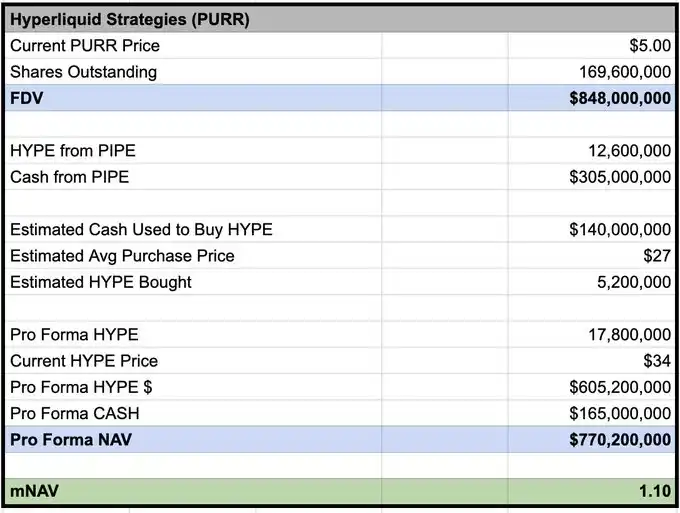

According to calculations by @Keisan_crypto, PURR's current mNAV is about 1.10, which means that if they are willing, they already meet the conditions to issue new shares.

Keisan's mNAV calculation based on the price on 03/02

But the question is, how many can they issue? Most people stop here. And the real advantage starts from here.

The S-1 Mechanism That Most People Don't Understand

According to the disclosures in the S-1 document, as the intermediary selling shares in the market, Chardan's beneficial ownership limit is 4.99%. Based on the current price, this means it can temporarily hold about $50 million worth of PURR stock at most.

But this does not mean they can only issue $50 million worth of new shares.

What it really means is: at any given time, Chardan cannot "accumulate" more than this amount of shares. As long as the shares continue to be sold into the market and distribution is completed, more new shares can be issued.

Additionally, in practice, Chardan will also be constrained by trading rules and market manipulation restrictions. Typically, this limits the daily transaction volume of ATM issuance to about 20% of the daily trading volume.

For example, in the most recent trading day: PURR's trading volume was about 7 million shares (approximately $42 million); based on this pace, Chardan can sell about $8.4 million worth of shares through ATM each day.

PURR price chart

Key Conclusion (The punchline)

In other words: if the trading volume can be maintained at the current level, PURR could potentially add about $8 million of "firepower" daily to buy HYPE.

Again, this does not mean they will mindlessly sweep the market; but the incentive structure here is completely different from PIPE financing.

PIPE financing: funds are in place at once, with no urgency, allowing cash to wait for sell orders to appear.

ATM issuance: the incentive structure changes.

If the issuance capacity expands with transaction volume and momentum, and higher PURR transaction volumes can continuously open the ATM window, then maintaining HYPE's strong momentum may actually enhance future issuance and financing capabilities.

In this structure, actively buying during an uptrend is no longer irrational. It can be a means to maintain liquidity, boost transaction volume, and maximize the amount of funds that the ATM can raise over time.

This is not "blindly pushing orders." It means that under specific conditions, quickly absorbing sell orders, or even adding to positions in the direction of the trend, is a strategically rational choice.

This is precisely what most people overlook.

They model PURR as a buyer with a continuously decreasing balance; however, if the ATM is open (mNAV premium) and real liquidity exists, then the real constraint is no longer: "How much money is left?" but rather: how much liquidity can you continuously provide to the market while maintaining momentum and trading activity without turning yourself into "the entire market"?

If almost all DATs have failed, why might this time be different?

Because the failures of most DATs stem from structural issues and poor asset choices, rather than the idea of "DAT itself being inherently wrong."

They fail, typically because of:

- Poor issuance mechanisms

Discounted OTC + short unlock periods essentially create their own "forced sellers";

- Lack of self-sustaining ability in underlying assets

If the asset has (or nearly has) no intrinsic yield, it must rely on price increases to maintain the cycle; once the price stagnates, the narrative collapses immediately;

- Inflationary supply narratives

If the underlying asset is inflationary (or heavily emitted), it is equivalent to fighting against structural headwinds;

- Catastrophic perceptions at the shareholder level

Issuing new shares at mNAV 1 is self-harm: it leads to severe dilution, destroys sentiment, and makes the next round of financing worse.

HYPE has avoided most of the failure paths mentioned above: protocol revenue will ultimately translate into demand and value capture for HYPE; under continuous use, supply is deflationary rather than structurally inflationary; there are no large holders or VCs with significant positions still unlocking.

This combination is crucial. Because it determines whether this is a story that can only exist if "numba go up," or a structure that can continue to operate as long as the fundamentals remain intact, even amidst market fluctuations.

Of course, there are still paths to failure: mNAV being compressed, transaction volume drying up, ATM being paused, or the HYPE narrative weakening. But structurally, HYPE is one of the few assets where the DAT cycle is not inherently a "scam machine."

I have also "mid-curved" here before

Finally, some may think: PURR is a bad investment because it continuously issues shares, and the issuance will suppress the stock price.

I used to think this way often (a typical mid-curve). But remember: when traditional finance truly understands how this "barbell structure" works, things could get very exaggerated.

Historical cases:

MSTR: 3.3× mNAV

Metaplanet: 8.3×

BMNR: 5.6×

And to be honest, these targets are not that great. Imagine what a "good" one could achieve.

Bobby starts printing money.

Open the money printer, Bobby.

Hyperliquid.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。