Original Title: "Changes in the Next Chair of the Federal Reserve! Warsh's Policy Proposals: Rate Cuts + Balance Sheet Reduction"

Original Author: Bao Yilong, Wall Street Insights

Rhythm BlockBeats Note: This article was first published on December 16, 2025. On January 30, sources revealed that Trump met with the popular candidate for the new Federal Reserve Chair, former Fed Governor Kevin Warsh, at the White House on Thursday. The White House later stated that Trump would officially announce the Federal Reserve Chair candidate tonight Beijing time.

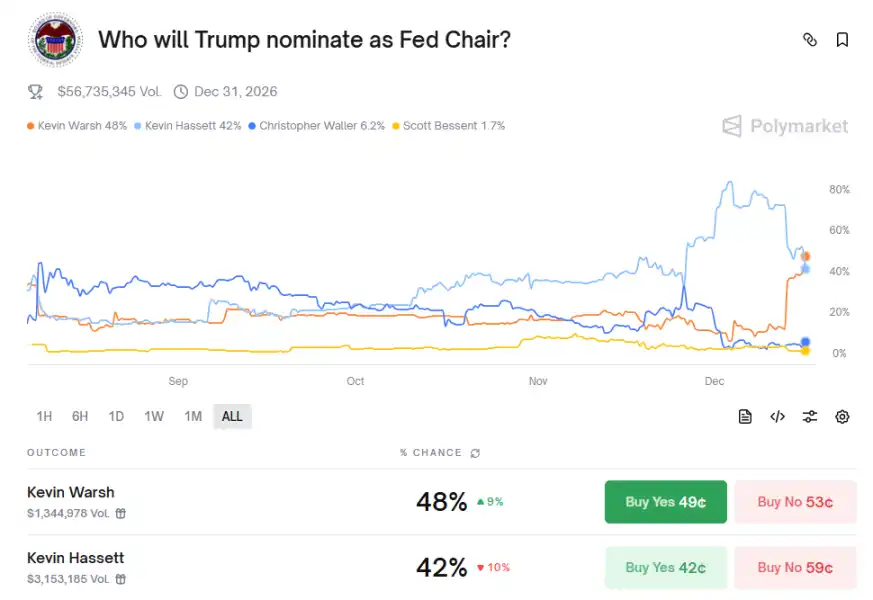

This news quickly ignited market speculation, leading to a dramatic reversal in the nomination probabilities of candidates. Rick Rieder, Chief Investment Officer of BlackRock Global Fixed Income, who was once considered the frontrunner, saw his nomination probability plummet from over 60% to 11%; meanwhile, Kevin Warsh's nomination probability surged to 81%, making him the strongest contender.

It is worth mentioning that Kevin Warsh's father-in-law is Ronald Lauder, the current head of Estée Lauder, and also a long-time friend of Trump, which has drawn public attention to this personal connection. The following is the original content:

Deutsche Bank analyzes that if Warsh is elected as the Federal Reserve Chair, his policy proposals may present a unique combination of "rate cuts and balance sheet reduction."

On December 16, Wall Street Insights mentioned that U.S. President Trump stated in a media interview that former Fed Governor Kevin Warsh has emerged as a leading candidate alongside Kevin Hassett for the Federal Reserve Chair position. He said:

"I think both Kevins are great."

Trump's statement led to a significant decline in Hassett's odds on the prediction market Kalshi. As of Tuesday, data from Polymarket showed that the prediction market believes Warsh has a greater chance of becoming the next Federal Reserve Chair than Hassett.

On December 15, according to news from the Wind Trading Desk, Deutsche Bank's Matthew Luzzetti team published a research report that deeply analyzed Warsh's policy proposals. The report analyzed that if Warsh is elected, he would support rate cuts but would also demand a reduction in the balance sheet.

The report pointed out that the premise of "rate cuts and balance sheet reduction" is regulatory reform that lowers banks' reserve requirements, and its feasibility in the short term is questionable.

Deutsche Bank believes that the market needs to closely monitor whether the new chair can maintain independence under Trump's pressure for significant rate cuts, as well as the process of establishing their policy credibility.

Warsh's Background

Unlike economist Hassett, Warsh comes from a legal background and has extensive experience in both the public and private sectors.

In the public sector, he served as a Federal Reserve Governor from 2006 to 2011, during which time the Fed was responding to the global financial crisis, and he played an important liaison role between the Fed and the markets.

He has been a strong critic of the Fed's aggressive balance sheet operations over the past 15 years, arguing that quantitative easing has deviated from the central bank's core responsibilities.

Warsh is currently a partner at the Duquesne family office of Stan Druckenmiller, as well as a distinguished visiting scholar at the Hoover Institution and a lecturer at Stanford Business School.

This experience spanning academia, regulatory agencies, and the investment community gives him a profound understanding of financial markets and monetary policy.

Warsh's Attitude Towards QE

Deutsche Bank points out that in recent years, Warsh has made numerous criticisms of the Federal Reserve, involving both short-term policy decisions and long-term strategic considerations.

First, Warsh has consistently criticized the Fed's aggressive use of its balance sheet over the past fifteen years.

While he supported the Fed's quantitative easing (QE) program in response to the global financial crisis, he warned that continuing QE thereafter was inappropriate, as it could trigger inflation and financial stability risks, and cause the Fed to deviate from its core responsibilities by intervening in credit allocation policies that could distort market signals.

The report cites Warsh's recent remarks:

"In the summer and fall of 2010, during a period of strong economic growth and financial stability, I was extremely concerned that the decision to purchase more government bonds would entangle the Fed in the complex political affairs of fiscal policy. The second round of quantitative easing was introduced, and I disagreed with that decision, shortly thereafter resigning from the Fed."

Warsh further believes that the Fed's active use of its balance sheet may have ushered in a "monetary-dominated" era. He argues that by artificially keeping interest rates low for an extended period, the Fed has played a leading role in facilitating the accumulation of U.S. government debt.

Warsh's Criticism of Other Policies

In addition to the balance sheet, Warsh has also criticized the Fed on multiple fronts.

For example, he believes the Fed relies too heavily on data and lacks foresight, while also criticizing the Fed's routine use of forward guidance. He recently pointed out:

"Forward guidance, a tool that was prominently introduced during the financial crisis, has almost no effect during normal times."

Warsh has also questioned other aspects of the Fed's formulation and interpretation of monetary policy, including the erroneous belief that "monetary policy is unrelated to money," "black box DSGE models are grounded in reality," and "Putin and the pandemic are responsible for inflation, rather than government spending and the surge in money printing."

The report analyzes that these criticisms imply that Warsh hopes to focus more on the size of the Fed's balance sheet and money supply in the execution of monetary policy, and may seek comprehensive reforms of the Fed's research team.

Finally, while he describes the Fed's independence as a "valuable" endeavor, he also believes that the Fed itself has invited questions about its independence. Warsh pointed out:

"The Fed's oversized role and poor performance have weakened the important and valuable rationale for monetary policy independence."

Additionally, Warsh condemns the Fed's mission creep, including considerations of climate and inclusivity issues.

Recent Policy Impact Outlook

Although Warsh has recently advocated for rate cuts, Deutsche Bank believes he is structurally not dovish.

His views during his tenure as a governor during the global financial crisis were sometimes more hawkish than his colleagues, especially on balance sheet issues. Recently, he expressed opposition to the Fed's decision to cut rates by 50 basis points last September.

In terms of policy decision-making, Warsh's recent remarks suggest he may support lowering the policy rate, although this move may come at the cost of reducing the size of the bank's balance sheet.

However, given that reserves are already at ample levels and the Fed has recently restarted its reserve management purchase program, this trade-off would only be feasible if regulatory reforms lower banks' reserve requirements.

While several Fed officials, including Vice Chair Bowman and Governor Milan, have recently made this argument, it is unclear whether these changes are realistic in the short term.

The report concludes that, from a broader perspective, regardless of whom President Trump chooses, the market may test the independence of the next Federal Reserve Chair and the credibility of their commitment to achieving inflation targets.

Deutsche Bank emphasizes that the new chair will always need to earn this trust. Given Trump's demand for significant rate cuts from the Fed, this demand may be more urgent.

Therefore, Deutsche Bank is skeptical about whether there will be substantial changes in policy after the leadership transition at the Fed in June, especially since the new chair only has one vote in a particularly divided committee.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。