The year 2025 marks an "industrial revolution" in the financial discipline of the cryptocurrency market. During this year, on-chain protocols demonstrated an unprecedented cash flow generation capability, attempting to reshape the underlying logic of token economics through over $1.4 billion in total buyback expenditures. This figure shows exponential growth compared to previous years, driven not only by the maturity of DeFi protocol business models but also by a structural shift in the U.S. regulatory environment—particularly the advancement of the Digital Asset Market Clarification Act and the GENIUS Act, which provide a compliant path for the supply management of "digital commodities."

However, the influx of capital has not led to equal value capture. This article analyzes the extreme polarization phenomenon in the buyback market of 2025: on one hand, Hyperliquid achieved a buyback scale of over $640 million (accounting for nearly 46% of the market total), resulting in several-fold increases in token prices and establishing "net deflation" as the core anchor for asset pricing; on the other hand, Jupiter and Helium, despite investing tens of millions of dollars, found themselves unable to combat structural inflation on a scale, ultimately discussing the cessation of buyback plans in early 2026 and shifting towards growth incentives. Additionally, the case of Pump.fun reveals how aggressive buybacks can devolve into exit liquidity in the absence of long-term locking mechanisms.

This article uses the "Net Flow Efficiency Ratio" (NFER) as a key indicator to assess buyback effectiveness. Data indicates that buybacks can only effectively transmit to secondary market prices when the flow rate of buyback funds significantly exceeds the flow rates of token unlocks and inflation (NFER > 1.0). Conversely, when NFER is 1.0, buyback funds merely serve as a "buffer" and may even accelerate whale sell-offs.

As Helium and Jupiter shift towards user subsidies, we observe that Web3 protocols are experiencing a division similar to traditional stock markets: "value stocks vs. growth stocks." Mature protocols capture value through buybacks and dividend attributes, while growth-stage protocols need to build network effect moats through capital expenditures.

1. Summary of Buybacks of Leading Crypto Protocols in 2025

In 2025, buybacks were mainly divided into two models:

- Fee Conversion Model: Such as Hyperliquid and Aave. A portion of the protocol's revenue is directly used to purchase tokens. This model has high transparency and is usually proportional to the protocol's usage.

- Treasury/Revenue Burn Model: Such as Helium and Pump.fun. The project team uses earned revenue to buy back and burn tokens or lock them up. This is more viewed as a deflationary measure.

Notably, Hyperliquid dominated with over $640 million in buybacks, becoming the "Buyback King" of the year. Meanwhile, DeFi blue chips like MakerDAO (Sky) and Aave remained robust, continuously delivering buybacks in the tens of millions of dollars. The Solana ecosystem showed active performance, with projects like Jupiter, Raydium, and Pump.fun contributing significant buyback volumes, but also accompanied by substantial controversy.

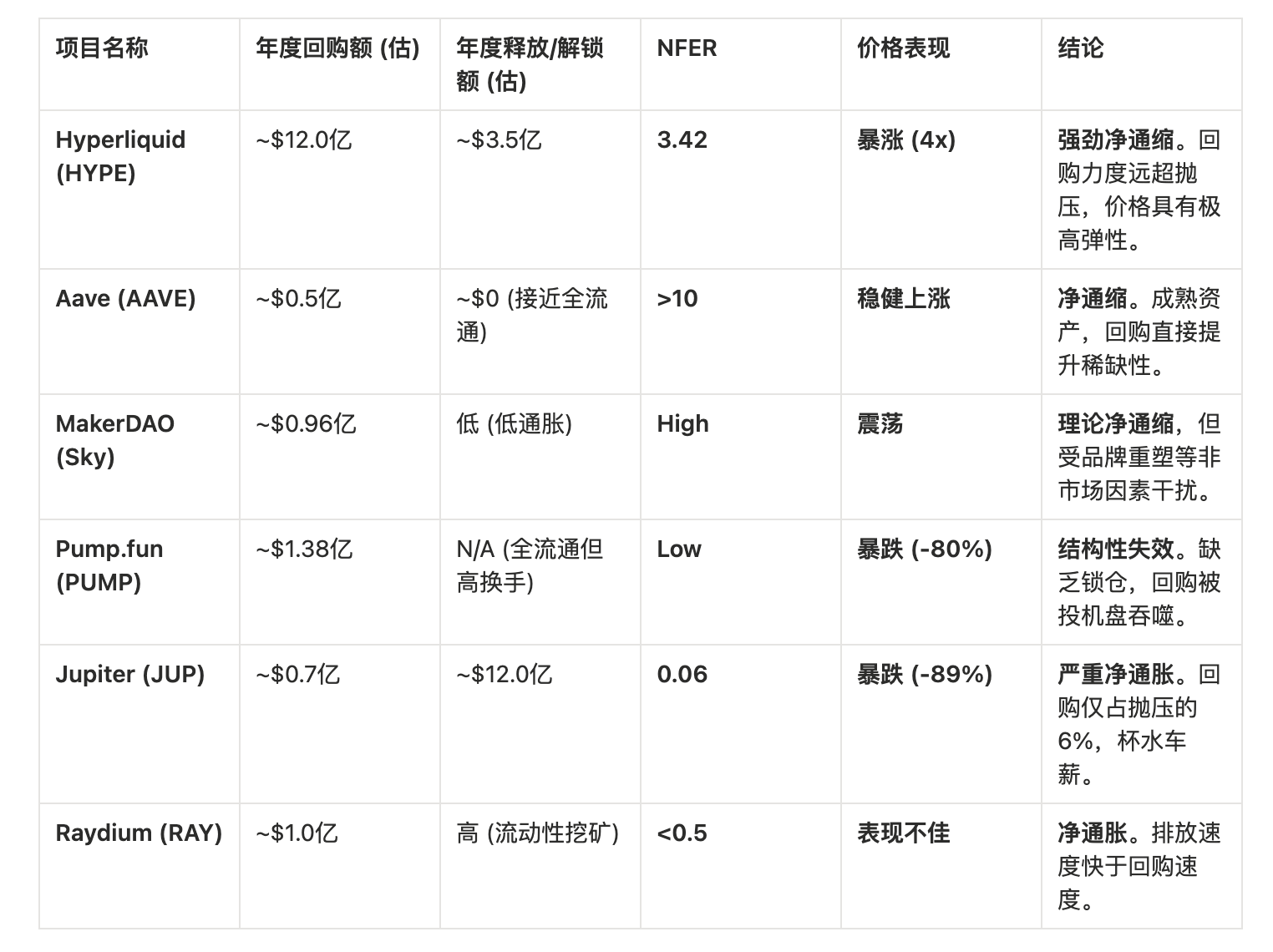

The actual effectiveness of buyback strategies exhibited extreme polarization. On one hand, projects like Hyperliquid (HYPE) and Aave (AAVE) achieved relative price stability through buybacks, following Bitcoin with wide fluctuations rather than plummeting; on the other hand, projects like Jupiter (JUP) and Helium (HNT), despite significant investments (of $70 million and several million dollars in monthly revenue respectively), faced price crashes or market indifference.

Analyzing these projects reveals that simple buybacks, if unable to overwhelm structural selling pressure or lack a strong binding with protocol growth, will devolve into "exit liquidity" for early investors or teams. Of course, this may also be the intended purpose behind some projects initiating buybacks.

From the data in the table, we can see:

- NFER > 1.0 is a necessary condition for price increases. Only when buyback funds are sufficient to cover all structural sell-offs (miners, teams, early investors) will prices rise under the push of marginal buy orders.

- NFER 0.1 means that buybacks are purely wasteful. In this case, stopping buybacks and shifting towards fundamental development is a rational financial decision.

In 2025, there is no simple linear positive correlation between the size of buyback amounts and token price performance.

1.1 Stable Performance Group: Mechanism and Growth Resonance

Hyperliquid (HYPE) • Buyback Scale: ~$644.6 million. • Mechanism: Assist Fund mechanism, using about 97% of exchange fees for buybacks. • Performance: The price performed extremely strongly in 2025, even driving a reevaluation of the entire Perp DEX track. • Success Reason: A very high buyback ratio (almost all income for buybacks) combined with explosive product growth (capturing market share from CEX), forming a "positive flywheel."

Aave (AAVE) • Buyback Scale: Annualized about $50 million (weekly $1 million). • Mechanism: Using the "Fee Switch" to allocate excess protocol reserves for purchasing AAVE. • Performance: The price steadily increased and showed significant resilience in the second half of 2025.

Bitget Token (BGB) • Buyback Scale: Quarterly burn, with approximately 1.58 million BNB equivalent value (referencing the BNB model) burned in Q1 2025. Bitget burned 30 million BGB (about $138 million) in Q2 2025. • Mechanism: Strongly tied to centralized exchange business, and BGB is empowered as the Gas token for Layer 2 (Morph). • Performance: The price reached an all-time high (ATH) of $11.62. • Success Reason: Beyond the scarcity caused by buybacks, more importantly, utility expansion. BGB upgraded from a single exchange point to a public chain Gas.

1.2 Controversial Group: The Futility of Counter-Trend Efforts

Pump.fun (PUMP) • Buyback Scale: ~$138.2 million. • Mechanism: 100% of daily revenue used for buyback and burn. • Performance: Price dropped 80% from ATH. • Failure Reason: A typical case of "using buybacks to sustain whales." Due to highly concentrated token distribution, buyback funds became a liquidity outlet for large holders. Additionally, the rapid shift in meme track hotspots made it difficult for infrastructure tokens to capture sustained value.

Sky (formerly MakerDAO) (SKY) • Buyback Scale: ~$96 million. • Mechanism: Smart Burn Engine. • Performance: Neutral to weak, not meeting expectations. • Failure Reason: Confusion in brand restructuring. Concerns arose from the migration process of MKR to SKY (1:24,000 split) and the "freezing function" of the USDS stablecoin. Despite the large buyback amount, uncertainty at the governance level suppressed buying confidence.

Raydium (RAY) • Buyback Scale: ~$100.4 million. • Mechanism: A portion of trading fees used for buyback and burn. • Performance: Highly volatile, failing to form a long-term upward trend. • Reason: As an AMM DEX, Raydium faces severe liquidity mining emissions. To attract liquidity, the protocol must continuously issue RAY. The buy orders from buybacks appear powerless against the massive inflationary sell-offs.

2. Classification and Evolution of Value Capture Mechanisms

In the practices of 2025, we observed that "buybacks" are not a single model but have evolved into various complex variants. Each model has distinctly different roles in token economics and market feedback. Next, we delve deeper into buyback mechanisms, exploring what scale of projects is suitable for which buyback mechanisms, or whether they are suitable to initiate buybacks at all.

2.1 Fee Conversion and Accumulation Model

Representative Cases: Hyperliquid, Aave

The core of this model lies in directly converting the real income generated by the protocol into native tokens and removing them from circulation through burning or locking.

- Hyperliquid's "Black Hole Effect": Hyperliquid designed an on-chain fund called the Assistance Fund, which automatically receives about 97% of the trading fees generated by the exchange.

- Mechanism Details: This fund continuously buys HYPE tokens in the secondary market. By the end of 2025, the fund had accumulated nearly 30 million HYPE, valued at over $1.5 billion.

- Market Psychology: This model creates a visualized, continuously growing buy order. Market participants not only see the current buying but also anticipate future buying pressure that will continue to expand with increasing trading volume. This expectation pushed HYPE to new heights in value discovery.

- Aave's "Treasury Optimization": Aave DAO allocates about $50 million of annual protocol revenue for buying back AAVE through governance proposals.

- Strategy Differences: Aave is not in a hurry to burn these tokens but views them as "productive capital." The repurchased AAVE is used to supplement the ecosystem's security module or as a reserve for future incentives. Although this approach does not immediately reduce the total supply, it significantly decreases the circulating supply and enhances the protocol's risk resistance.

2.2 Aggressive Burn Model

Representative Cases: Pump.fun, MakerDAO (Sky), Raydium

This is the most traditional deflationary model, aimed at increasing the value of a single token by permanently reducing supply.

- Pump.fun's "Zero-Sum Game": As a Memecoin launch platform, Pump.fun uses all its revenue (which once reached millions of dollars daily) to buy back and burn PUMP tokens.

- Limitations: Despite burning tokens worth $138 million, the price of PUMP plummeted by 80%. The reason lies in the lack of a locking mechanism and long-term utility for PUMP, making the buyback funds an excellent exit route for speculators. This proves that without a "reason to hold," simple deflation cannot counteract selling pressure.

- Sky (MakerDAO): Utilizes a "Smart Burn Engine" to buy and burn SKY using the surplus stablecoins generated from over-collateralization. Although the mechanism is robust, the benefits of the burn are overshadowed by uncertainties at the governance level during a chaotic brand restructuring period.

2.3 Trust Locking Model

Representative Case: Jupiter

Jupiter attempts to balance deflation and reserves through a middle path: buying back tokens but not immediately burning them, instead locking them in a long-term trust called "Litterbox."

- Mechanism Design: Jupiter commits to using 50% of fees to buy back JUP and lock it for 3 years.

- Market Feedback: Ineffective. The market views the "3-year lock" as "delayed inflation" rather than "permanent deflation." Faced with significant unlocking pressure, even if tokens temporarily exit circulation, the market tends to factor in future selling pressure in its pricing.

3. Net Flow Theory: The Mathematical Essence of Buyback Success or Failure

By comparing Hyperliquid, Aave with Jupiter, Pump.fun, we can distill three core variables that determine the success or failure of buybacks: Net Deflation Rate, Market Game Psychology, and Project Lifecycle Stage.

3.1 Variable One: Net Deflation Rate (Buyback Amount vs. Emission Amount)

Whether buybacks can drive up prices does not depend on the absolute amount of buybacks but on "net flow." $$\text{Net Flow} = \text{Buyback Burn Amount} - (\text{Team Unlock} + \text{Investor Unlock} + \text{Staking Emission})$$

Hyperliquid is the only top protocol in 2025 to achieve "net deflation."

- Buyback Side: Annualized buyback amount reaches $1.2 billion (based on Q3/Q4 data).

- Release Side: For most of 2025, HYPE was in a low circulation, low release phase. Although in November, about 9.92 million tokens (approximately 3.66% of circulation) were unlocked by core contributors, this selling pressure was completely covered by its massive buyback volume.

- Calculation result:

- $$\text{Net Flow} \approx \$100M/\text{month (buy orders)} - \$35M/\text{month (unlock selling pressure)} = +\$65M/\text{month (net buying)}$$

3.2 Sailing Against the Wind: Jupiter's Inflation Trap

Jupiter demonstrates the helplessness when buybacks encounter massive inflation.

- Buyback Side: Annual expenditure of about $70 million.

- Release Side: JUP faces an extremely steep unlocking curve. At the beginning of 2026, JUP faces approximately $1.2 billion in token unlocking pressure, with about 53 million tokens (approximately $11 million) unlocking linearly each month.

- Arithmetic result:

- $$\text{Net Flow} \approx \$6M/\text{month (buy orders)} - \$10M+/\text{month (unlock selling pressure)} = -\$4M/\text{month (net selling pressure)}$$

- Market Game: In this huge negative net flow, the $70 million buyback funds effectively became "exit liquidity" for early investors and team-unlocked tokens. Market participants realized this and chose to sell when buybacks occurred rather than hold. Solana co-founder Anatoly pointed this out: the protocol should accumulate cash and conduct a one-time large buyback in the future, forcing currently unlocked tokens to trade at "future expected prices" rather than directly giving money to the unlocking pressure now.

4. Strategic Shift: From "Market Support" to "Infrastructure"

At the beginning of 2026, as Jupiter and Helium announced the cessation or reassessment of their buyback plans, the industry underwent profound reflection. This trend indicates that Web3 projects are returning from simple "financial engineering" (pulling up prices through buybacks) to the logic of "business management" (investing for growth).

4.1 Helium (HNT): User Acquisition Costs Outweigh Buybacks

On January 3, Helium founder Amir Haleem announced the cessation of HNT buybacks, with a simple and direct reason: "The market does not care whether the project team buys back."

- Data Background: Helium Mobile's monthly revenue reached $3.4 million. Previously, part of this money was used for buying back HNT, but the token price remained weak.

- New Strategy: Redirect this funding to subsidize hardware, acquire new users, and expand network coverage.

- Logic Reconstruction: For DePIN projects, network effects (number of nodes, user scale) are their core moat. By subsidizing to lower user thresholds, more active users can be brought in, who will continuously consume data credits in the future, creating endogenous, rigid token burn demand. This "organic burn" is far more valuable than the artificial "buyback burn" initiated by the project team.

- Return on Investment (ROI) Analysis: $1 million in buybacks may only stabilize the token price for a few days; however, $1 million used for subsidies could bring in 10,000 long-term paying users, who will contribute far more than $1 million in value over their lifetime (LTV).

4.2 Jupiter (JUP): Growth Incentives vs. Capital Return

Jupiter co-founder Siong Ong also initiated discussions in the community about stopping buybacks, proposing to redirect the $70 million fund to "growth incentives."

- Core Argument: When the token is still in a high inflation phase, buybacks are an inefficient capital allocation. Funds should be used to build moats, such as developing new features (like JupUSD), incentivizing developers, or subsidizing users' trading slippage.

- Strategic Significance of JupUSD: Jupiter launched the stablecoin JupUSD, supported by the BlackRock BUIDL fund. If buyback funds are used to incentivize the liquidity and adoption of JupUSD, it will build a deeper moat for the Jupiter ecosystem, which will have a far greater long-term impact on JUP token value than short-term price support.

4.3 Optimism (OP): Counter-Trend Buybacks

Interestingly, while Jupiter and Helium retreated, Optimism proposed a plan in January 2026 to use 50% of its superchain revenue to buy back OP tokens.

- Why Counter-Trend? This reflects the differences in project lifecycle stages. Optimism has passed the early stage of ecosystem growth through inflation subsidies, and now its superchain has generated considerable real income (Sequencer Fees).

- Strategic Intent: Optimism aims to shed the label of "useless governance token" by establishing a hard connection between "revenue and tokens" through buybacks. This indicates that buybacks are not wrong at all stages. When a protocol has a solid moat and cash flow, and the token valuation needs to shift from "market dream rate" to "price-earnings ratio," buybacks are a reasonable means.

5. Conclusion and Outlook: A New Paradigm for 2026

Financial engineering cannot solve structural inflation; income itself is not a moat; net flow is.

5.1 Conclusion

- Buybacks are not a panacea: For projects in a high inflation period (with many tokens not unlocked), buybacks are not only ineffective but also a plunder of the protocol's treasury. They deliver precious cash flow to early profit-takers who are exiting.

- Stage Determines Strategy:

- Growth Stage: Funds should be used for user acquisition and network expansion. At this time, buybacks will be seen as "management's lack of investment imagination."

- Mature Stage: With strong cash flow and controllable inflation, buybacks or dividends should be used to reward holders and establish value anchors.

New Tracks Brought by Regulation: The passage of the CLARITY Act and GENIUS Act allows "digital commodity" tokens to manage supply more compliantly. In the future, we will see more cases like Aave, which finely manage treasury and token supply within a legal framework.

5.2 Investor Recommendations

When evaluating crypto projects in 2026, one should not buy simply because of an "announced buyback." The following checks must be executed:

- Calculate NFER: Is the buyback amount greater than the future year's unlocking value?

- Examine Holder Structure: Is it dominated by long-term believers or "mercenaries"?

- Understand Funding Sources: Are buyback funds coming from real protocol income, or are they merely consuming financing?

In 2026, the market will no longer reward simple "burn" narratives but will reward those protocols that can utilize cash flow to build real moats and ultimately achieve net deflation.

About Movemaker

Movemaker is the first official community organization authorized by the Aptos Foundation, jointly initiated by Ankaa and BlockBooster, focusing on promoting the construction and development of the Aptos ecosystem in the Chinese-speaking region. As the official representative of Aptos in the Chinese-speaking area, Movemaker is committed to building a diverse, open, and prosperous Aptos ecosystem by connecting developers, users, capital, and numerous ecological partners.

Disclaimer:

This article/blog is for reference only, representing the author's personal views and does not represent the position of Movemaker. This article does not intend to provide: (i) investment advice or recommendations; (ii) offers or solicitations to buy, sell, or hold digital assets; or (iii) financial, accounting, legal, or tax advice. Holding digital assets, including stablecoins and NFTs, carries high risks, with significant price volatility, and they may even become worthless. You should carefully consider whether trading or holding digital assets is suitable for you based on your financial situation. For specific issues, please consult your legal, tax, or investment advisor. The information provided in this article (including market data and statistics, if any) is for general reference. Reasonable care has been taken in compiling this data and charts, but no responsibility is accepted for any factual errors or omissions expressed therein.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。