Author | Kaori

Editor | Sleep.txt

At the end of last year, JPMorgan Chase froze the accounts of two stablecoin payment startups funded by YC, BlindPay and Kontigo, which focused on the Latin American market but triggered the bank's sanctions and compliance red lines due to their operations in high-risk jurisdictions like Venezuela.

Coincidentally, another bank that has always been seen as crypto-friendly, Lead Bank, has also recently tightened its cooperation with some stablecoin payment companies, adding customer identity verification, and extending transaction settlement times and account opening durations.

With compliance becoming a necessity, many entrepreneurs in the payment industry and stablecoin sector have realized that they are often not dealing with the banking system as a whole, but rather with a very small number of banks that are willing and able to keep their doors open.

However, Lead Bank and JPMorgan Chase have different backgrounds. As one of the first banks to participate in Visa's USDC settlement on the Solana chain, Lead Bank has not chosen to abruptly cut off banking services to startups. On the contrary, this bank plans to achieve a leap forward by providing native support for crypto enterprises.

The Rise and Fall of Garden City Bank

To understand Lead Bank's present, we must first look back at its past.

In 1928, before the shadow of the Great Depression loomed over the United States, a small institution named Garden City Bank was established in Cass County, Missouri.

It was an era reliant on handshake deals and trust as collateral. As a typical community bank, its fate was closely tied to the surrounding farmland, livestock, and family businesses. Over the following decades, it witnessed the boom and bust of the American agricultural economy and survived the Great Depression of the 1930s. This was a significant achievement, as thousands of similar institutions across the country failed at that time.

For the next 77 years, this bank quietly made a living, much like the small town of Garden City it was located in.

In 2005, Garden City Bank experienced its first turning point.

Landon H. Rowland, a business legend from Kansas City, and his wife Sarah decided to buy Garden City Bank after retiring. Landon Rowland was not an ordinary banker; he was the former chairman and CEO of Southern Industries in Kansas City. During his tenure, he expanded the railroad company into Mexico and was instrumental in the spin-off of financial giants Janus Capital and DST Systems.

Landon bought this sleepy rural bank out of a sense of old-fashioned business idealism, fully aware of the power of infrastructure, whether it be rail tracks or financial flows, fundamentally aimed at connection and circulation.

In 2010, the Rowland family renamed the bank Lead Bank. The name itself hinted at a certain ambition, no longer limited to the geographical Garden City but aiming to become a leader in the industry.

Subsequently, Landon's son Josh Rowland took over as CEO. Josh, a banker with a legal background and a strong humanistic influence, grew tired of the cold, bureaucratic design of traditional bank counters and wondered why banks couldn't be a third space for the community, like Starbucks or public libraries.

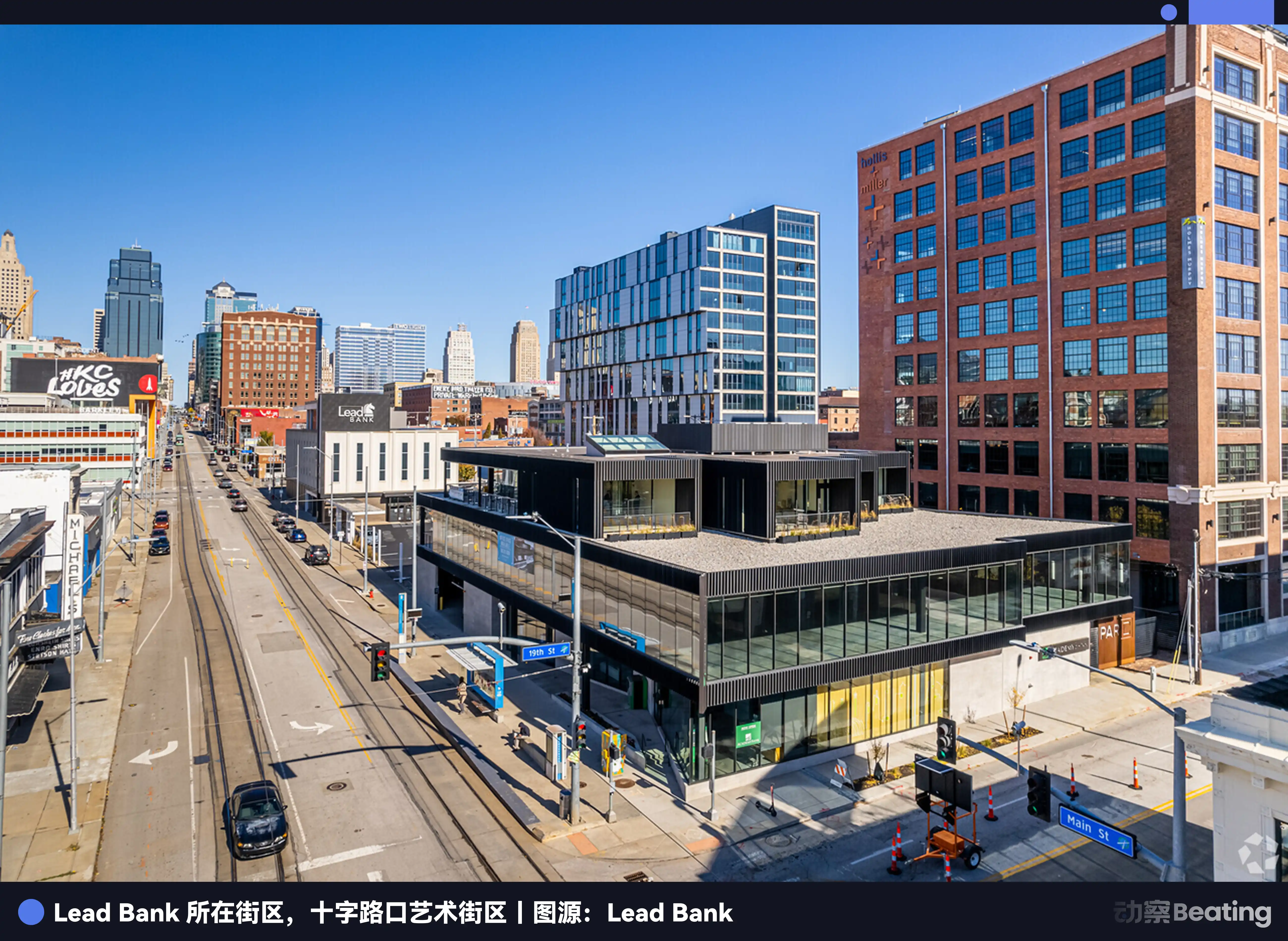

To realize this vision, Josh recognized that the bank needed to leave its comfortable rural setting and move into the heart of economic activity. In 2015, Lead Bank made a bold decision to relocate its headquarters to the Crossroads Arts District in downtown Kansas City.

The Crossroads Arts District was once a dilapidated industrial warehouse area but was revitalized in the early 2000s by artists, galleries, and tech startups, becoming the heart of innovation in Kansas City. Lead Bank created a non-traditional space in this avant-garde neighborhood.

No bulletproof glass, no queue ropes; Josh even commissioned students from the Kansas City Art Institute to hold art exhibitions in the bank lobby and designed a rooftop terrace for yoga classes and cocktail parties.

During this period, Lead Bank, while stylish on the outside, remained a traditional community bank at its core. It served local small business owners, relying on a warm network of local relationships to survive.

The Woman from Silicon Valley

While the Rowland family was reshaping Lead Bank's physical form, a powerful woman in finance named Jackie Reses was experiencing deep frustration.

Jackie Reses's career is a textbook on capital efficiency. She spent seven years at Goldman Sachs, focusing on mergers and acquisitions and private equity, honing her top-notch deal-making instincts.

Reses then joined Yahoo, where she led one of its most significant and complex asset management deals—Yahoo's stake in Alibaba. Through extremely complex negotiations and structural designs, Reses ultimately unlocked over $50 billion in value for Yahoo, establishing her status as a top dealmaker.

In 2015, Twitter founder Jack Dorsey recruited her to his payment processing company Square, where she was responsible for the small business loan department Square Capital, which had been established only 18 months prior. This department aimed to provide loans to millions of small businesses using merchants' transaction data. This should have been a perfect business loop, but the U.S. regulatory system kept tech companies firmly outside the banking industry.

Thus, to comply with lending regulations, Square had to adopt a model of renting licenses, partnering with industrial banks like Celtic Bank in Utah to issue loans in the bank's name, which Square would then buy back.

In an interview, Reses mentioned that working with traditional banks was extremely challenging. For example, traditional banks typically have very few software engineers and rely on a rigid, patchwork legacy system, making it difficult for user-experience-focused fintech companies to customize their transaction methods as needed. Every new product launch had to go through a lengthy tug-of-war between the bank's compliance and technology departments.

This dependent existence was incredibly painful. After leaving Square in 2020, Jackie Reses was determined to own her own bank. When choosing an acquisition target, she avoided the crowded markets of California and New York, setting her sights on Lead Bank in Kansas City.

Thanks to the Rowland family's prudent management, Lead Bank had a clean balance sheet and a management team willing to innovate. More importantly, she did not want to spend all her time mingling with CEOs; she wanted to get close to real small business owners, which was the core customer group of Lead Bank.

On August 1, 2022, the acquisition was officially completed. This was a rare transaction that received rapid approval from regulatory agencies, including the Federal Reserve and the Missouri Division of Finance, largely thanks to Reses's good regulatory relationships.

It is worth noting that Reses's brother, Jacob Reses, a young political rising star, previously served as JD Vance's chief of staff in the Senate. With JD Vance set to become the Vice President of the United States in early 2025, Jacob Reses continues to serve as his core aide, becoming one of the key figures in White House policy-making.

This secret pipeline to the power center in Washington, while not a get-out-of-jail-free card, provides Lead Bank with very low misunderstanding costs and smooth communication mechanisms under the regulatory pressure of Chokepoint 2.0, allowing it to dare to venture into innovative areas that other banks avoid.

Reses's vision for Lead Bank is to layer a fintech layer on top of an already existing community bank in Kansas City, creating a banking infrastructure that can be sold to other fintech companies.

At that time, Lead Bank attracted well-known fintech clients like Affirm and began to engage with clients in the crypto industry. Although the fintech industry was still in a winter phase, Lead Bank's growth had already begun to accelerate. In the third quarter of 2023, revenue grew by 9% compared to the second quarter, reaching $37 million; net profit surged by 50% to $5 million, and total assets reached $951 million, an increase of over $100 million from a year ago.

Aftershocks in the BaaS Industry

Jackie Reses brought not only Wall Street capital and Washington's attention to Lead Bank but also almost directly moved a core team from Square.

This included CTO Ronak Vyas, Chief Legal Officer Erica Khalili, and Chief Product Officer Homam Maalouf, along with former Meta design director Albert Song. This team covers the complete loop from underlying code development, compliance risk management, to front-end user experience design, giving Lead Bank the core capability to independently build financial products without relying on external vendors.

When Vyas first examined the core systems of traditional banks, he felt a shock from the last century. Most American banks still operate on mainframes based on COBOL from the 1970s. These systems use batch processing; if you swipe your card today, the bank has to wait until after closing to run the program, and only then will it know the balance changes the next day. This is prehistoric civilization for fintech companies that pursue millisecond-level responses.

After taking office, Vyas made an extremely hardcore decision: not to buy off-the-shelf solutions but to develop everything in-house. This self-developed system is built directly on AWS cloud services and Snowflake databases, serving as a parallel ledger and risk control orchestration layer, reducing reliance on traditional intermediary black boxes and achieving true real-time accounting.

While other banks are still purchasing middleware software to patch old systems, Lead Bank has transformed itself into a tech company disguised as a bank. Although this heavy model was once mocked as inefficient, time quickly proved the foresight of Reses and Vyas.

In 2024, the well-known middleware service provider Synapse declared bankruptcy, triggering a chain collapse in the BaaS industry.

As mentioned earlier, many fintech companies neither have banking licenses nor the capability to interface with the outdated mainframe systems of banks. Synapse acted as an intermediary, providing fintech companies with simple and user-friendly interfaces while managing the complex underlying accounts for banks. Before its collapse, Synapse supported over 100 fintech companies, indirectly managing accounts for 18 million end users, with an annual transaction volume reaching $76 billion.

Its failure revealed a terrifying black box, where the sub-ledgers recording accounts in middleware often did not match the general ledgers of the actual funds held by banks. Tens of millions of dollars vanished into thin air, leaving thousands of depositors unable to withdraw their funds. Subsequently, BaaS banks like Evolve Bank and Blue Ridge Bank, which had previously expanded aggressively, received severe penalties from regulators and were forced to suspend new business.

The entire industry fell into panic as fintech founders were horrified to discover that their seemingly rock-solid banking partners were built on quicksand.

This was the moment Reses had been waiting for; by insisting on not using middleware and building its core systems, Lead Bank emerged unscathed from the storm.

Those shaken unicorn companies began to seek safe havens, with one of the world's largest digital banks, Revolut, fully migrating its U.S. operations to Lead Bank, and corporate spend management giant Ramp also abandoning its old partners to embrace Lead Bank.

More importantly, this hardcore technology combined with a complete license model garnered enthusiastic support from the capital markets. In September 2025, Lead Bank completed a $70 million Series B funding round, led by ICONIQ and Greycroft, with top venture capital firms like a16z and Ribbit Capital participating. At this point, Lead Bank's valuation had soared to $1.47 billion, making it one of the few bank-like unicorns.

The New Era of Crypto-Friendly Banks

If Lead Bank is only seen as a partner for fintech, it underestimates Jackie Reses's ambition; this bank is quietly becoming a key valve between the crypto economy and the fiat world.

After the collapses of Silvergate and Signature Bank, the crypto industry lost two major pillars for U.S. dollar settlements. Lead Bank keenly filled this vacuum, but its approach is smarter and more discreet than its predecessors.

By the end of 2025, Visa announced the launch of USDC stablecoin settlement functionality on the Solana chain, and one of the two initial banks supporting this functionality was Lead Bank. This means that when you swipe your Visa card for a purchase in some corner of the world, the flow of funds behind it may no longer go through the slow SWIFT system but instead be settled through a Lead Bank account in USDC within seconds.

Lead Bank not only helps crypto companies store money; it also maps fiat accounts to on-chain addresses. Through its API, compliant crypto enterprises can achieve 24/7 real-time inflow and outflow of fiat currency.

Looking at Lead Bank's financial statements, one can see that its growth logic is entirely different from that of traditional community banks.

As of the third quarter of 2025, Lead Bank's total assets had surged to $1.97 billion, more than double what they were before the acquisition, with the key being the restructuring of its deposit structure. Traditional banks seek to have the public deposit fixed-term savings while paying 4%-5% interest.

In contrast, Lead Bank has gained a large amount of commercial demand deposits by serving fintech and crypto clients. This money typically stays in accounts for payment settlements and is insensitive to interest rates, meaning Lead Bank has a very low cost of funds on the liability side.

On the asset side, Lead Bank is most restrained; it did not, like Silicon Valley Bank, use customers' short-term deposits to buy long-term government bonds, nor did it issue high-risk commercial loans extensively. Instead, it allocated a large amount of funds to highly liquid short-term assets or quickly circulated short-term credit through its fintech partners.

Data from 2024 shows that its primary non-interest income sources, such as payment fees, API call fees, and card issuance commissions, grew by 39%, far exceeding the growth rate of traditional interest income.

This creates a flywheel effect: low-cost settlement funds come in, earning risk-free fees, and funds circulate quickly, resembling a transaction-based revenue model rather than the traditional interest margin model of banks.

Reading this, you will understand that during the current turbulent transformation period in the financial and crypto industries, the language of regulation, the language of banks, and the language of tech companies have never been consistent, and every inconsistency could one day turn into a rectification order.

Lead Bank proves that in the era of AI and blockchain, the most radical innovations do not necessarily come from destroying the old world but from the old world's self-awareness. By merging a century of banking credibility with Silicon Valley's engineering capabilities and the humanistic care of modern art, Lead Bank not only survived but also defined what a 21st-century bank is.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。