Original Title: "Who is Betting Against Common Sense in the Prediction Market?"

Original Author: Golem, Odaily Planet Daily

Recently, I couldn't help but start thinking, who exactly is going against "common sense" to provide the market with "free money"?

Betting against smart people like us doesn't mean it's without chance; there are certainly some individuals who firmly believe in their judgments (for example, there are still people who believe the Earth is flat). However, the prediction market is not a "fool's market." I believe that when players use real money to predict whether something will happen, they will do their utmost to think as "rational individuals," meaning that the decisions they make are the most economical and profitable. Therefore, from this perspective, those users betting "Yes" on seemingly impossible event contracts must have some kind of profit-making strategy; they are not fools providing us with "high certainty" investment opportunities for free.

After some thought and discussion, I believe that the potential liquidity providers in these absurd event markets may include the following three types of people (this article is meant to spark discussion, and corrections are welcome, X@web3_golem):

Lottery Players

The logic of lottery players is simple: they only look at the odds and focus on small bets for big wins.

Sometimes, reality is far more magical than we imagine; even seemingly outrageous events can happen. Moreover, although the prediction market settles based on the real world, the settlement results can sometimes be distorted due to settlement conditions, system failures, and other factors. For instance, Polymarket has experienced multiple instances where the settlement did not match reality due to issues with the UMA dispute resolution mechanism, with a recent example being Polymarket's determination that the U.S. military's actions in Venezuela did not constitute an "invasion."

Thus, long-tail odds deviations occur, where even events with extremely low probabilities of happening still have a "Yes" price of 1%-3%. As long as the odds are high enough, "lottery players" will buy in, becoming one of the firm bottom support buyers.

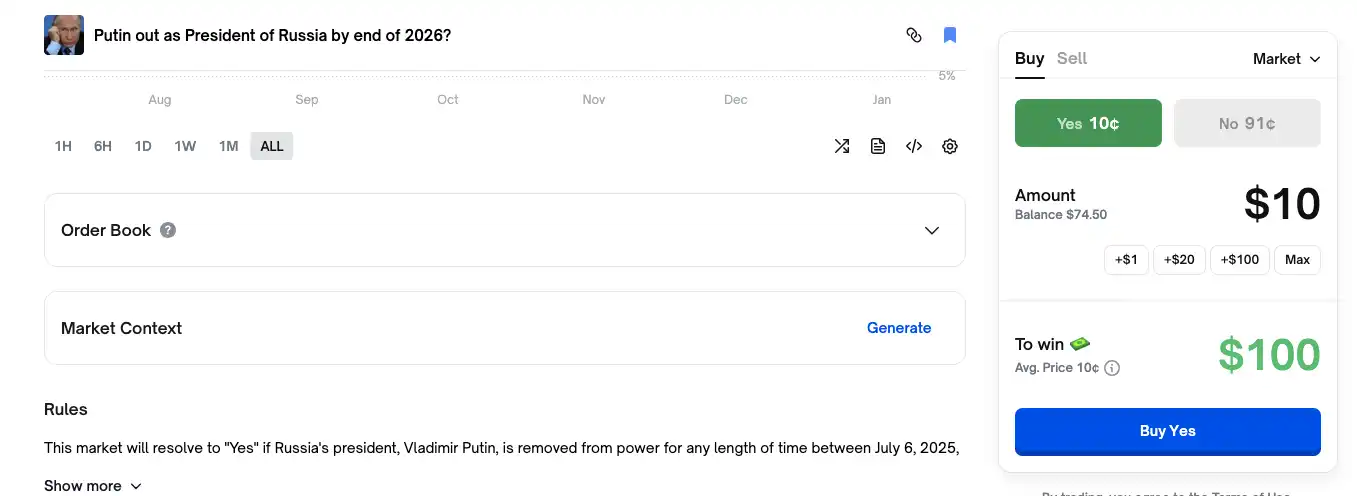

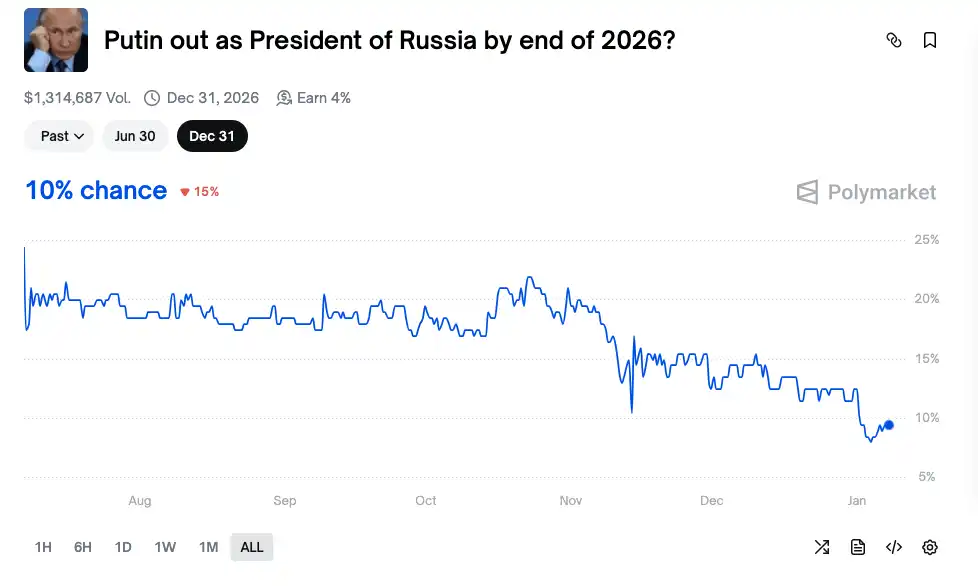

However, the mentality of "lottery players" is also rational. For example, in the event contract "Will Putin resign by the end of 2026?", driven by common sense, most people would buy "No," and the probability already reflects people's attitudes. Yet, the "Yes" side still has a 10% probability, meaning that if you bet $10, you would receive $100 if Putin indeed resigns by the end of 2026, a tenfold return. So why not bet?

Additionally, lottery players do not necessarily place large bets on a single market; since there is no shortage of high-odds events in the prediction market, casting a wide net and hitting a few lotteries still offers a chance to recoup costs or even profit.

They are more eager than normal people for black swan events to occur. Therefore, they are willing to provide buy orders on the "Yes" side of the "against common sense" market (in some markets, Polymarket offers order placement rewards and holding rewards, but this is not the main driving factor for lottery players).

Bots

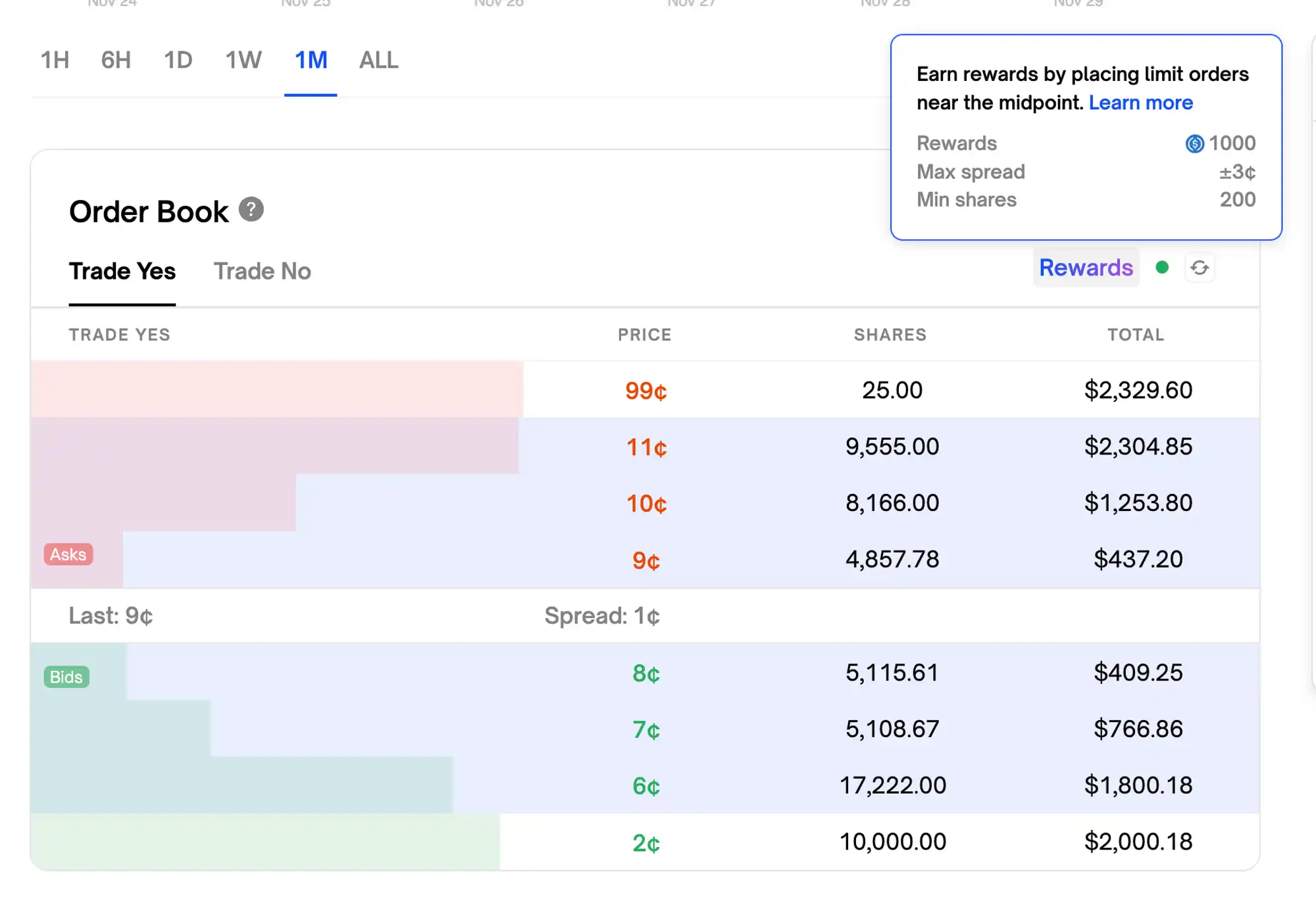

If an event contract has strong certainty, the involvement of tail-end players' funds will further push one side's probability to 99%-100% before settlement. The existence of "lottery players" can partially explain why there are still players betting on the "Yes" sell side in these "against common sense" markets (because Polymarket uses a shared order book, meaning when there is a buy order of 1 share at $0.99 on the "No" side, there will correspondingly be a sell order of 1 share at $0.01 on the "Yes" side), but they remain a minority and cannot explain why these markets have large transaction volumes and good depth.

So, who else injects significant liquidity into these markets? The answer is bots.

Market-making bots on Polymarket have developed rapidly. Bots that trade automatically through the Polymarket API actively monitor all newly created markets and often become the first participants. These bots can profit by actively trading in these markets.

In these "against common sense" markets, when the "No" side price is $0.99, due to the shared order book, there will be a sell order at $0.01 on the "Yes" side. Market-making bots will also consume these $0.01 sell orders like "lottery players," but immediately afterward, they will place sell orders at $0.02, $0.03, or even higher on the "Yes" side, waiting for "lottery players" or other bots to transact. The "No" side will also see buy orders at $0.98, $0.97, or even lower (Odaily Note: still due to the shared order book), thus creating significant depth in the order book.

However, after discussions with the crypto VC Jsquare team (who invested in the prediction market aggregator Rocket), they believe that there are not many bots executing this strategy in the market, and in this "against common sense" market, the speculative psychology of "lottery players" or players is sufficient to support most of the betting orders.

The existence of some volume-filling bots also provides market liquidity and trading volume for these "against common sense" and somewhat niche markets (compared to events like the U.S. elections). One volume-filling bot places a buy order at $0.02 on the "Yes" side, while another volume-filling bot places a buy order at $0.98 on the "No" side to transact.

This behavior is mainly to seek future airdrops in the prediction market; in high-frequency markets, orders may be matched by other players, so these "against common sense" event contracts are the ideal tools for volume filling.

Prediction Platforms

In addition to the "lottery players" and bots mentioned above, prediction platforms themselves have made significant contributions to the liquidity of these markets.

Polymarket has liquidity incentive measures such as order placement rewards and holding rewards built into its mechanism. Order placement rewards mean that in certain specific markets, as long as players place orders within the maximum allowed price difference, they can receive rewards; holding rewards mean that in certain specific markets, as long as players hold shares of either Yes or No, they can receive a 4% annualized holding reward.

The highlighted part indicates the maximum price difference range for order placement rewards.

According to statistics, Polymarket has invested about $10 million in market maker incentives, paying over $50,000 daily at peak times to maintain order book liquidity. Nowadays, these incentives have decreased to only $0.025 for every $100 traded.

These investments have indeed been effective, driving trading in many "against common sense" markets. For example, the event contract "Will Putin resign by the end of 2026?" has seen over $1.3 million in trading volume, and holding this contract will yield a 4% annualized return. For players holding Yes shares, this translates to a final annualized return of 14% (10% tail-end return + 4% platform reward), which is highly attractive. For players holding No shares, the order placement rewards and holding rewards also hedge some of the risks.

There is also speculation that, in addition to openly providing liquidity incentives, prediction markets themselves act as market makers to provide liquidity for these "against common sense" and niche markets to facilitate advertising and marketing effects. But this is purely speculation and open for discussion.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。