Original Title: "Web3 Lawyer In-Depth Policy Interpretation | New Regulations for Virtual Asset Trading Platforms in Hong Kong (Part 2): New Circular Released, Are the Boundaries of Virtual Asset Business Redefined?"

Original Source: Crypto Salad

Introduction

At the end of the year, riding the wave of HashKey's listing, the Hong Kong Financial Services and the Treasury Bureau and the Securities and Futures Commission jointly announced that, in addition to advancing the licensing regulation of "virtual asset trading" and "virtual asset custody" services under the original regulatory framework as planned, they are also preparing to introduce new licenses for these two services: one for "providing advice on virtual assets" and another for "virtual asset management," and public consultation has already begun. If all goes well, the mainstream core services of virtual assets—"trading," "custody," "investment advisory," and "asset management"—will all be streamlined through separate licensed regulation.

At this point, do any readers find it strange that these services cannot currently be performed in Hong Kong? It feels like the train has already left the station, but upon looking back, the tickets haven't even gone on sale yet?

As of now, only 11 specialized platforms holding a VATP license in Hong Kong can operate as virtual asset trading platforms, while separate services for virtual assets, such as trading, investment advisory, and asset management, are achieved through upgrades of traditional licenses (1, 4, 9), essentially building a temporary structure on the foundation of traditional licensed rules. The significance of the new regulations lies in the fact that these important separate services are now being licensed individually, each with its own responsibilities. Crypto Salad believes that the signal being released is quite clear: the regulation of virtual assets needs to pave its own road and should indeed pave its own road.

However, the formal issuance of separate licenses is likely to wait until 2026. Looking back, this year, for licensed virtual asset trading platforms, the Securities and Futures Commission issued two key circulars on November 3, 2025. Crypto Salad has previously analyzed one of them, the article: Interpretation of New Regulations for Virtual Asset Trading Platforms in Hong Kong (Part 1): "Circular on the Sharing of Liquidity by Virtual Asset Trading Platforms." Today, we will discuss the second part in detail: "Circular on Expanding the Products and Services of Virtual Asset Trading Platforms."

What Does the Circular Say?

Those on the front lines of the industry can feel that the reality of virtual asset business has clearly exceeded the original VATP regulatory framework's expectations. The initial licensing system was purely designed around "centralized virtual asset trading platforms," with core focuses on trade matching, customer asset segregation, and basic market order maintenance. However, with the continuous emergence of stablecoins, tokenized securities, RWAs, and various investment products linked to digital assets, the role that platforms play in practice has long since expanded beyond that of a mere trading venue.

In this context, the real contradiction faced by regulators is no longer "should these businesses exist," because if they continue to be excluded from a clear regulatory framework, it will only allow the market to evolve in a gray area. Rather than letting practitioners find ways to circumvent the rules, it is better to clearly outline what can be done while also solidifying the corresponding responsibilities. We believe this is the starting point of this circular.

From the specific content, the circular brings several seemingly "loosened" measures at the platform level, but in reality, it redistributes various responsibilities.

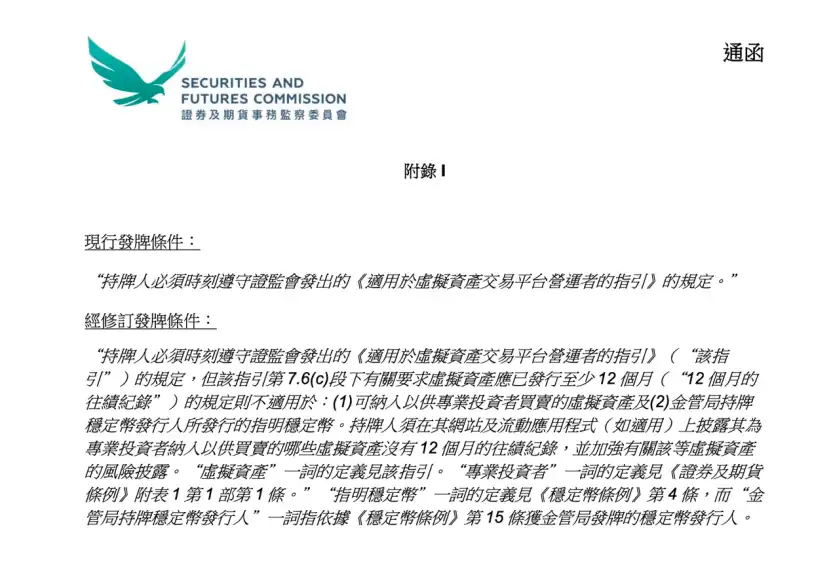

First, there is an adjustment regarding the rules for token inclusion. In the past, for a virtual asset to be listed on a VATP platform, it typically needed to meet a minimum trading track record requirement of at least 12 months, which essentially used time to filter risk. However, in practice, this approach is not always reasonable: a project that has been around for a long time does not necessarily mean that information is sufficient or that risks are controllable; conversely, a newly launched project may not lack adequate disclosure and prudent assessment.

It is important to note that this circular does not completely eliminate the 12-month track record requirement but rather specifies exemptions in two particular circumstances:

First, for virtual assets offered only to professional investors, and second, for designated stablecoins issued by licensed issuers from the Monetary Authority. In other words, the Securities and Futures Commission does not deny the value of track records but acknowledges that risk assessment methods should not be one-size-fits-all for different investor groups and asset types. Rather than using a formal time threshold to "block risks" for platforms, it is better to require platforms to take on more substantive judgment responsibilities.

Correspondingly, the circular also strengthens disclosure requirements. For virtual assets that do not have a 12-month track record but are offered only to professional investors, licensed platforms must clearly indicate this situation on their websites or applications and provide adequate risk warnings.

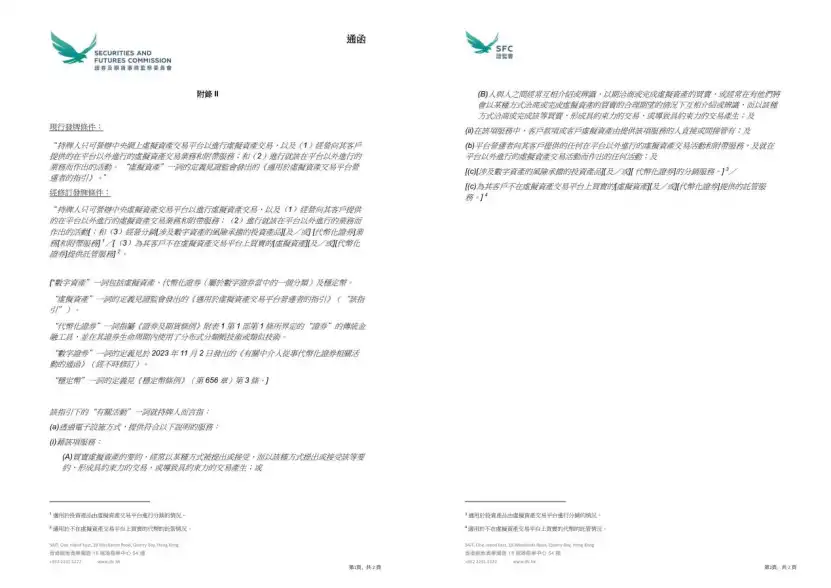

The second important change is that the Securities and Futures Commission has, for the first time, explicitly stated at the licensing condition level that VATP platforms can distribute tokenized securities and investment products related to digital assets, provided they comply with the existing regulatory framework.

Currently, VATPs have already taken on a function similar to "product entry." Once they enter a new distribution role, the risks they face are no longer just counterparty risks but typical financial product distribution responsibilities, including product understanding, suitability assessment, and information disclosure obligations. This is not a concession from regulators but a change in responsibilities brought about by a change in roles.

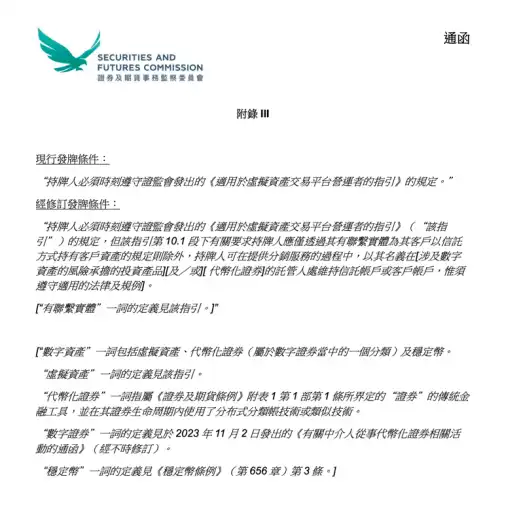

The third adjustment focuses on custody rules. The circular allows licensed platforms to provide custody services for virtual assets or tokenized securities that are not traded on the platform through their affiliated entities.

What changes will this bring? In current practice, many projects' assets do not necessarily need to be traded on the platform, but clients still wish for regulated institutions to hold or manage the relevant assets. Therefore, the design of such demands has not been smooth and often requires multi-layered arrangements to barely achieve compliance. After the circular takes effect, it essentially supplements a clearer compliance path for these existing business needs.

If the main body of the circular outlines the overall policy direction, then the three appendices reflect the Securities and Futures Commission's considerations on "how to implement" at the operational level.

Appendix I revises the rules for token inclusion, superficially lowering the entry threshold for some products, but in essence, it does not weaken the platform's prudential obligations. The threshold has not disappeared; VATPs need to support their judgments with more solid due diligence and disclosure.

Appendices II and III further clarify the boundaries of the platform's operational scope and the arrangements for holding client assets during the distribution process. By redefining "related activities," the Securities and Futures Commission formally includes the distribution of investment products related to digital assets, tokenized securities, and custody services for non-platform traded assets within the practice scope of VATPs. Additionally, in distribution business, platforms are allowed to open and maintain trust accounts or client accounts in their own name with relevant custodians to hold these assets on behalf of clients. These adjustments do not lower the requirements for client asset protection but rather ensure that the business structure can truly "run smoothly" from a legal and regulatory perspective.

What Changes Should Practitioners Pay Attention to After the Circular?

The issuance of the new circular means that for VATPs, previously, activities such as trading, custody, research, product introduction, and even some distribution activities could be uniformly categorized under "platform services," as long as they were included under VATP license regulation. Now, it is necessary to more clearly distinguish which actions belong to the core functions of a trading platform and which are approaching independent custody, distribution, or advisory activities, and to achieve compliance through different entity arrangements and business boundary delineations.

For other participants, such as OTC and custody service providers, the space that previously relied on ambiguous roles or functional overlaps is rapidly narrowing, and now they must more clearly answer the question: What specific type of virtual asset service are they engaged in? And under what regulatory framework should they assume corresponding responsibilities?

Conclusion

Overall, the circular reflects not a sudden shift in regulatory attitude but a more realistic choice: VATP platforms are gradually evolving from a single trading venue into compliant nodes that connect trading, products, and asset management, while regulation is correspondingly shifting its focus from formal conditions to whether platforms are truly taking on their due responsibilities.

This circular does not mean that business has been "loosened" overnight, but the change in regulatory attitude is clear: compliance is no longer just about "staying within the lines," but about being responsible for one's own judgments; for project parties and investors, it also means that regulatory expectations are gradually becoming clearer, rather than continuing to rely on ambiguous spaces for survival.

Moving forward, how far the market can go will no longer depend on whether regulators provide space, but on whether participants are truly ready to operate under a clearer and more serious rule system.

This article is from a submission and does not represent the views of BlockBeats.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。