The US dollar experienced a short-term plunge, while gold quickly surged, as a flawed inflation report dropped a bombshell in the year-end financial markets.

On the evening of December 18, Eastern Standard Time, the US Bureau of Labor Statistics released data showing that the unadjusted CPI year-on-year rate for November was recorded at 2.7%, significantly lower than the market expectation of 3.1%. Equally surprising was the unadjusted core CPI year-on-year rate, which was only 2.6%, not only falling short of the expected 3% but also marking the lowest level since March 2021.

Due to the previous government shutdown, this inflation report was missing data from October, leading analysts to describe it as "full of noise." The market reacted swiftly, with the dollar index dropping 22 points in a short time, while spot gold rose by $16.

1. Data Shock

● The US inflation data for November caught the market off guard. The overall CPI year-on-year growth rate was only 2.7%, and the core CPI year-on-year growth rate was 2.6%, both significantly below previous mainstream market expectations.

● The uniqueness of this report lies in its statistical background. Due to the US government shutdown in October, the Bureau of Labor Statistics was forced to cancel the CPI report for that month and assumed the CPI change for October to be zero when calculating the November data.

● Investment firm UBS pointed out that this statistical treatment could lead to an approximate 27 basis point downward bias in the final report. If this factor is excluded, the actual inflation data might be closer to the market expectation level of 3.0%. Therefore, the data itself contains significant statistical "noise."

● Nevertheless, structurally, there are indeed signs of cooling inflation. Core service inflation has become the dominant factor pulling overall core inflation down, with housing inflation year-on-year dropping significantly from a previous value of 3.6% to 3.0%.

2. Market Reaction

● Following the data release, the financial markets reacted quickly. US stock futures rose across the board, with the Nasdaq 100 index futures gaining over 1%. Meanwhile, US Treasury prices climbed, and yields correspondingly fell.

● The interest rate futures market showed a significant increase in expectations for a shift in Federal Reserve policy. Data indicated that the market believed the likelihood of the Fed cutting rates in January had risen from 26.6% to 28.8%. Additionally, the market expected that by the end of 2026, the policy rate would be loosened by another 3 basis points, with an anticipated easing of about 62 basis points next year.

● The dollar weakened in response, with the dollar index dropping 22 points to a low of 98.20. Meanwhile, non-dollar currencies generally rose, with the euro gaining nearly 30 points against the dollar and the dollar falling nearly 40 points against the yen.

● Brian Jacobson, Chief Economic Strategist at Annex Wealth Management, stated: “Some may view this inflation cooling report as ‘more unreliable than usual’ and disregard it, but ignoring it comes with risks.”

3. Internal Divisions at the Federal Reserve

In light of this unusual inflation report, a new round of debate may unfold between the hawks and doves within the Federal Reserve. The low CPI data undoubtedly provides stronger arguments for the doves.

● In fact, internal divisions have already emerged in recent Federal Reserve meetings. The December rate decision passed with a vote of 9 in favor and 3 against, resulting in a 25 basis point rate cut, marking the first time in six years that three dissenting votes were recorded.

Kansas City Fed President Esther George and Chicago Fed President Austan Goolsbee opposed the rate cut, advocating for maintaining rates, while Fed Governor Michelle Bowman supported a more significant rate cut.

● This division is also reflected in the Fed's latest dot plot. The dot plot indicates that the median rate forecast for 2026 is 3.4%, and for 2027 is 3.1%, consistent with the September forecast, suggesting one 25 basis point rate cut in each of the next two years.

● However, outside of the dot plot, there are significant differences in the personal views of Fed officials. Atlanta Fed President Raphael Bostic even stated that he did not include any rate cuts in his 2026 forecast, believing the economy would perform stronger at around 2.5% GDP growth, thus requiring a restrictive policy.

4. Policy Path Behind the Dot Plot

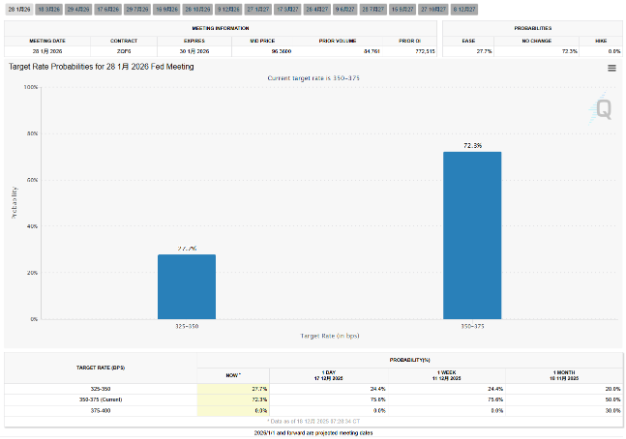

● Although the dot plot provides a collective forecast of future rate paths from Fed officials, it conceals complex policy considerations and economic judgments. The current interest rate range of 3.50%-3.75% is the result of the Fed's third consecutive rate cut.

● Analysis from BlackRock suggests that the most likely policy path for the Fed is to lower rates to near 3% by 2026. This forecast differs from the median rate of 3.4% shown in the dot plot, reflecting a gap between market expectations and official guidance.

● The evolution of the Fed's policy framework is also noteworthy. In the fourth quarter of 2025, the Fed officially halted quantitative tightening (QT) that had been in place for nearly three years, and starting in January 2026, a new mechanism called "Reserve Management Purchases" (RMP) will begin operation.

● Although the Fed officially defines RMP as a "technical operation" to ensure sufficient liquidity in the financial system, the market tends to interpret it as a form of "covert easing" or "quasi-quantitative easing." This mechanism transition could become another important variable affecting future rate paths.

5. Rate Cut Threshold and Economic Observations

● With the unexpected cooling of inflation data, the threshold for further rate cuts by the Fed has become a focal point for the market. The Fed's December statement indicated that the threshold for continuing rate cuts has clearly increased, and the "magnitude and timing" of future cuts will depend on changes in the economic outlook.

● The performance of the labor market will be a key decision variable. Although the November inflation data showed an unexpected slowdown, the number of initial jobless claims reported at the same time was 224,000, lower than the expected 225,000, reversing the previous week's surge trend, indicating that the labor market remained stable in December.

● Analysis from CMB International Securities pointed out that the US job market has weakened slightly but has not deteriorated significantly. The number of first-time and continuing jobless claims remains low and has shown slight improvement since October.

● The institution predicts that in the first half of 2026, inflation may continue to decline due to falling oil prices and a slowdown in rent and wage growth, and the Fed may cut rates once in June as a political statement. However, in the second half of the year, inflation may rebound, and the Fed may keep rates unchanged.

6. Diverse Predictions from Wall Street

● For the rate path in 2026, Wall Street analysis shows unprecedented divergence. ICBC International expects the Fed to cumulatively cut rates by 50-75 basis points in 2026, bringing rates down to around 3% as a "neutral" level.

● In contrast, JPMorgan holds a cautiously optimistic view, believing that the resilience of the US economy, particularly the strong performance of non-residential fixed investment, will support economic growth. Therefore, it anticipates a more limited rate cut, with the policy rate stabilizing around 3%-3.25% by mid-2026.

● ING has outlined two extreme scenarios:

One is a substantial deterioration in economic fundamentals, prompting the Fed to decisively ease in response to recession risks, in which case the yield on 10-year US Treasuries could fall significantly to around 3%.

The other is the Fed, under political pressure or misjudgment, may prematurely and excessively ease monetary policy without a clear economic slowdown, which could severely damage the Fed's credibility and trigger deep market concerns about uncontrolled inflation, leading to a surge in 10-year Treasury yields, potentially challenging the 5% mark.

7. Future Outlook and Investment Insights

● Looking ahead, changes in the Fed leadership may bring new uncertainties to monetary policy. Fed Chair Jerome Powell's term will end in May 2026, and the appointment of a new chair may influence the Fed's policy direction and communication style.

● Analysis from Guotai Junan Securities suggests that while the November CPI is unlikely to change the Fed's decision to pause rate cuts in January, it will undoubtedly amplify the dovish voices within the Fed. If December data continues the current low growth trend, it may prompt the Fed to reassess its rate cut path for next year.

● For investors, BlackRock recommends considering several fixed-income investment strategies in the current macro backdrop: investing cash in 0-3 month Treasury bills or diversified short-term bonds; increasing allocations to some intermediate-duration bonds; constructing a bond ladder to lock in yields; and seeking higher returns through high-yield bonds and emerging market bonds.

● Kevin Flanagan, Head of Fixed Income Strategy at WisdomTree, noted that the Fed has become a "divided house," and the threshold for further easing is very high. He emphasized that with inflation still about one percentage point above the target, the Fed is unlikely to make consecutive rate cut decisions unless the labor market significantly cools.

As the dollar index dipped shortly after the data release and gold surged, traders are reassessing the rate path for 2026. Despite the statistical flaws in this inflation report, it at least offers the market a glimmer of hope.

Whether this is a statistical anomaly or a genuine inflation retreat, the Fed's next actions will depend on economic data in the coming months. The seemingly smooth rate cut path in the dot plot faces dual challenges from economic realities and market expectations.

Join our community to discuss and grow stronger together!

Official Telegram community: https://t.me/aicoincn

AiCoin Chinese Twitter: https://x.com/AiCoinzh

OKX benefits group: https://aicoin.com/link/chat?cid=l61eM4owQ

Binance benefits group: https://aicoin.com/link/chat?cid=ynr7d1P6Z

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。