Original Title: Specialized Stablecoin Fintechs

Original Authors: Spencer Applebaum & Eli Qian, Multicoin Capital

Translated by: Peggy, BlockBeats

Editor’s Note: Over the past two decades, innovation in fintech has primarily remained at the distribution layer, improving user experience but not changing the underlying logic of capital flow, leading to industry homogenization, high costs, and thin profits. The emergence of stablecoins is reshaping this landscape. With open, programmable on-chain infrastructure, the costs of custody, settlement, credit, and compliance have significantly decreased, allowing fintech companies to build products directly on-chain without relying on banks and card networks.

When infrastructure becomes inexpensive, specialization becomes possible. Future fintech will no longer pursue scale but will instead deeply serve specific groups, creating products that truly meet their needs. The core of competition in Fintech 4.0 will shift from "who can reach customers" to "who truly understands customers."

The following is the original text:

In the past two decades, fintech has changed the way people access financial products, but it has not changed the way capital actually flows. Innovation has mainly focused on simpler interfaces, smoother account opening processes, and more efficient distribution, while the core financial infrastructure has remained largely unchanged. For most of this time, the tech stack has simply been resold repeatedly rather than rebuilt.

Overall, the development of fintech can be divided into four stages:

Fintech 1.0: Digital Distribution (2000–2010)

The first wave of fintech made financial services more accessible but did not significantly improve efficiency. Companies like PayPal, E*TRADE, and Mint digitized traditional systems (such as ACH, SWIFT, and card networks established decades ago) through internet interfaces, packaging them as existing products.

Settlement remained slow, compliance still relied on manual processes, and payments were completed on fixed schedules. This era brought finance online but did not change the way capital flowed. What changed was who could use financial products, not how those products operated.

Fintech 2.0: The Era of Neobanks (2010–2020)

The next breakthrough came from smartphones and social distribution. Chime offered early wage access for hourly workers; SoFi focused on refinancing student loans for upwardly mobile graduates; Revolut and Nubank reached underserved consumers globally with user-friendly experiences.

Each company told a more distinct story targeting specific groups, but essentially sold the same products: checking accounts and debit cards operating on old rails. They relied on sponsor banks, card networks, and ACH, just like their predecessors.

These companies succeeded not because they built new payment rails, but because they reached customers better. Branding, account opening experience, and customer acquisition capabilities were their advantages. Fintech companies during this period became efficient distribution enterprises layered on top of banks.

Fintech 3.0: Embedded Finance (2020–2024)

Around 2020, embedded finance emerged. APIs allowed almost any software company to offer financial products. Marqeta enabled businesses to issue cards through APIs; Synapse, Unit, and Treasury Prime provided banking as a service (BaaS). Soon, almost every application could offer payment, card, or loan services.

But beneath this abstraction, the core remained unchanged. BaaS providers still relied on the same sponsor banks, compliance frameworks, and payment rails. The abstraction layer moved from banks to APIs, but the economics and control flowed back to traditional systems.

The Commoditization of Fintech

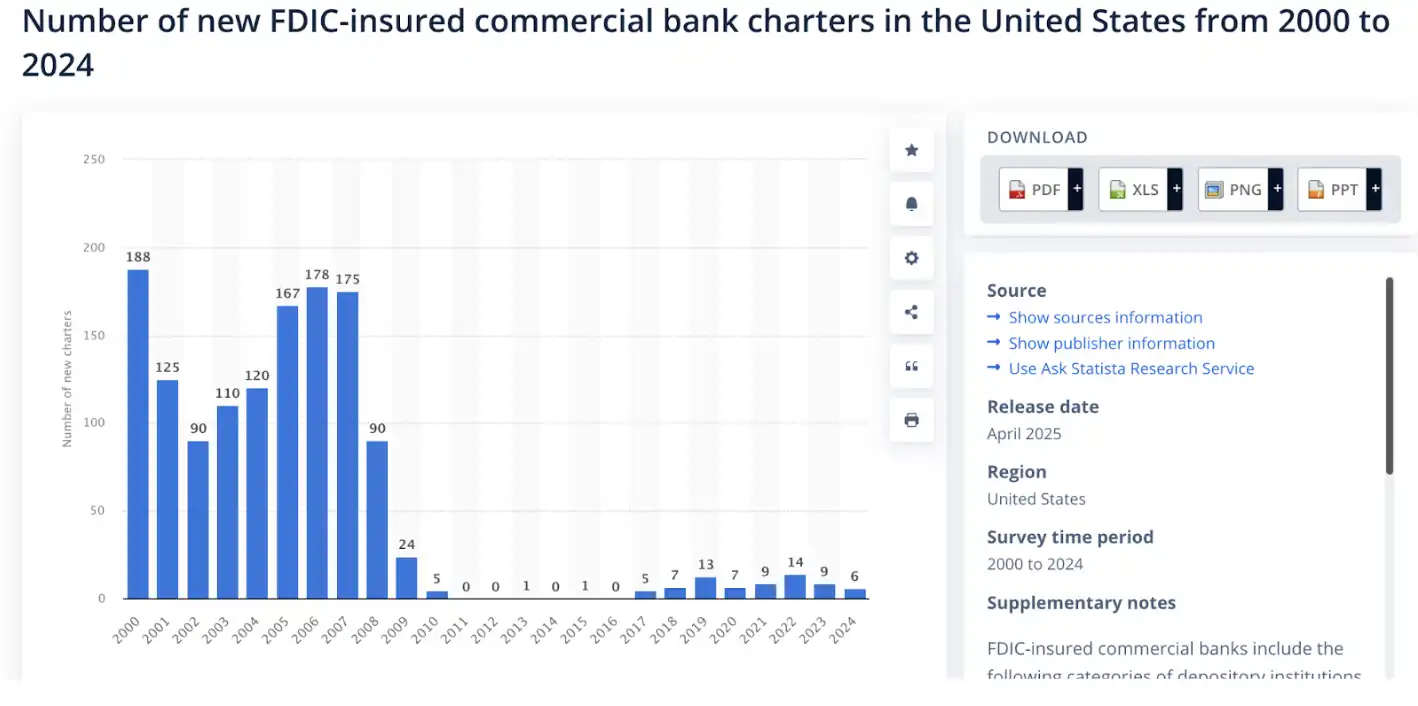

By the early 2020s, cracks in this model were evident. Almost all major neobanks relied on the same small group of sponsor banks and BaaS providers.

As a result, customer acquisition costs soared, and companies engaged in fierce competition through performance marketing, compressing profit margins, while fraud and compliance costs ballooned, making infrastructure nearly indistinguishable. Competition evolved into a marketing arms race. Many fintech companies attempted to differentiate themselves through card colors, signup bonuses, and cashback gimmicks.

Meanwhile, risk and value capture concentrated at the banking level. Giants like JPMorgan Chase and Bank of America, regulated by the OCC, retained core privileges: accepting deposits, issuing loans, and accessing federal payment rails (like ACH and Fedwire). Fintech companies like Chime, Revolut, and Affirm lacked these privileges and had to rely on licensed banks to provide services. Banks earned interest margins and platform fees; fintech companies profited from interchange fees.

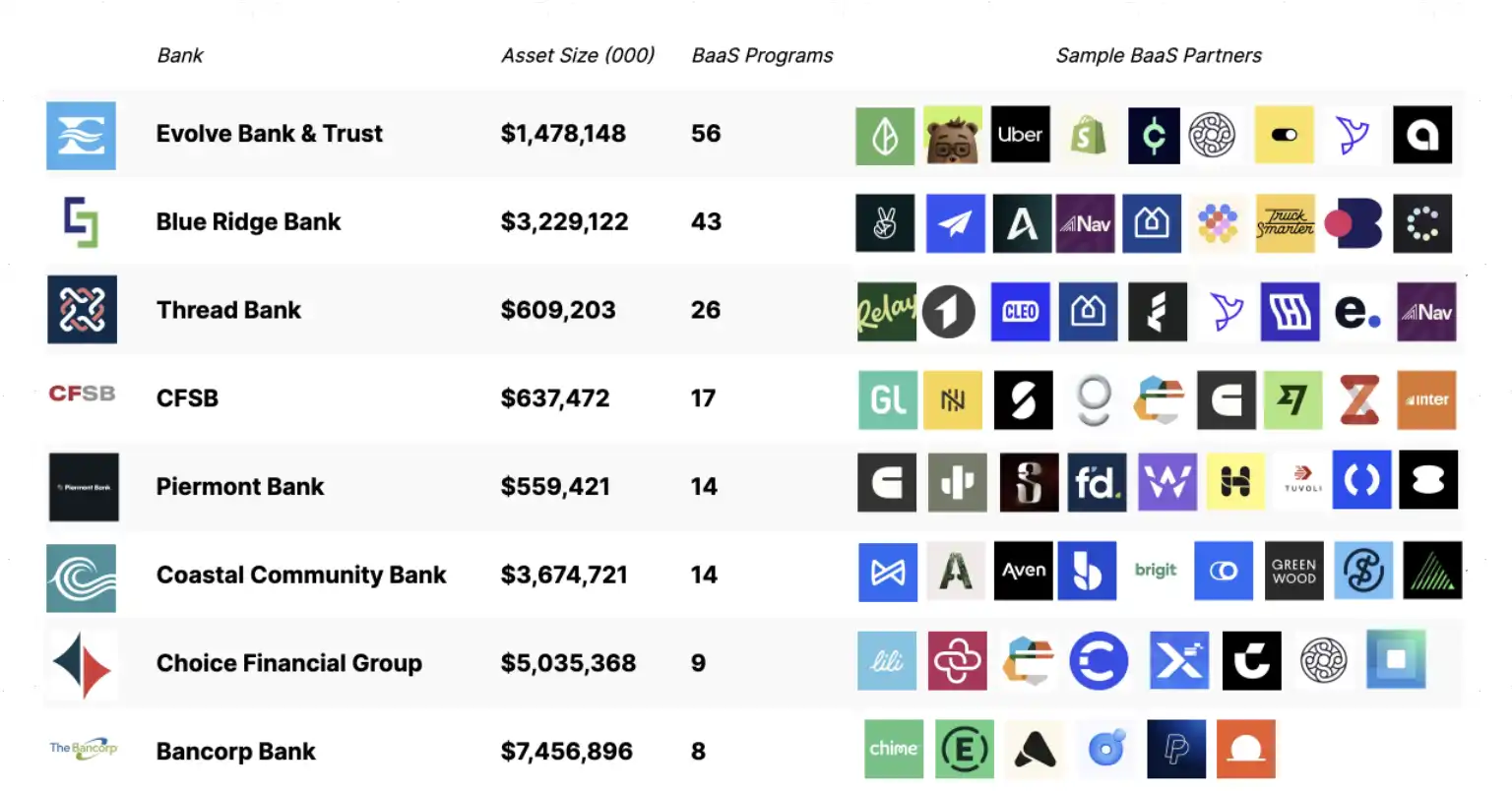

With the surge in fintech projects, regulators increasingly scrutinized the sponsor banks behind them. Regulatory orders and heightened oversight requirements forced banks to invest heavily in compliance, risk management, and oversight of third-party projects. For example, Cross River Bank signed a regulatory order with the FDIC, Green Dot Bank faced enforcement actions from the Federal Reserve, and the Federal Reserve issued a ban on Evolve.

The banks' response was to tighten account opening processes, limit the number of supported projects, and slow down product iteration. Models that once allowed experimentation increasingly required scale to justify compliance burdens. Fintech became slower, more expensive, and tended to develop broad, generic products rather than specialized ones.

In our view, the reasons for the stagnation of innovation at the top layer of the tech stack over the past 20 years can be summarized in three points:

The infrastructure for capital flow is monopolized and closed. The ACH networks of Visa, Mastercard, and the Federal Reserve leave little room for competition.

Startups require significant capital to build finance-centric products. Launching a regulated banking application requires millions of dollars for compliance, fraud prevention, and capital management.

Regulatory restrictions prevent direct participation. Only licensed institutions can custody funds or transfer funds through core rails.

Under these constraints, building products became more reasonable than challenging the payment rails themselves. The result is that most fintech companies are merely elegant wrappers around bank APIs. Despite two decades of innovation, the industry has produced almost no truly new financial primitives. For a long time, there have been few viable alternatives.

Cryptocurrency, on the other hand, has taken a completely opposite path. Builders first focused on the underlying primitives. Automated market makers, bonding curves, perpetual contracts, liquidity vaults, and on-chain credit emerged from the ground up. Financial logic became programmable for the first time.

Fintech 4.0: Stablecoins and Permissionless Finance

Although the first three eras of fintech brought a wealth of innovation, the underlying pipelines changed little. Whether products are offered through banks, neobanks, or embedded APIs, capital still flows on closed, permissioned rails controlled by intermediaries.

Stablecoins break this model. Native stablecoin systems no longer overlay software on top of banks but directly replace key banking functions. Builders interact with open, programmable networks. Payments settle on-chain. Custody, lending, and compliance shift from contractual relationships to software logic.

Banking as a Service (BaaS) reduces friction but does not change the economic structure. Fintech companies still need to pay compliance fees to sponsor banks, settlement fees to card networks, and access fees to intermediaries. Infrastructure remains expensive and constrained.

Stablecoins completely eliminate the need to rent access. Builders no longer call bank APIs but write directly into open networks. Settlement occurs directly on-chain. Fees belong to the protocol rather than intermediaries. We believe the cost baseline will drop significantly: from millions of dollars required to build through banks or hundreds of thousands through BaaS, to just thousands of dollars using smart contracts on permissionless chains.

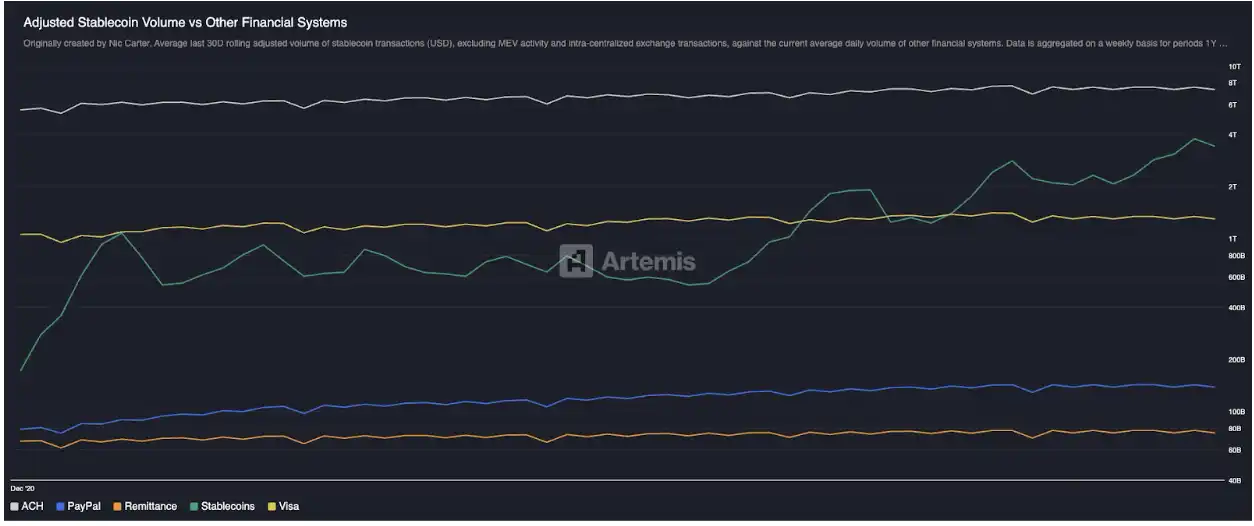

This shift has already manifested at scale. In less than a decade, stablecoins have grown from nearly zero to about $300 billion in market capitalization, and in terms of processing real economic transaction volumes, they have surpassed traditional payment networks (like PayPal and Visa), even excluding inter-exchange transfers and MEV. For the first time, non-bank, non-card rails are truly operating globally.

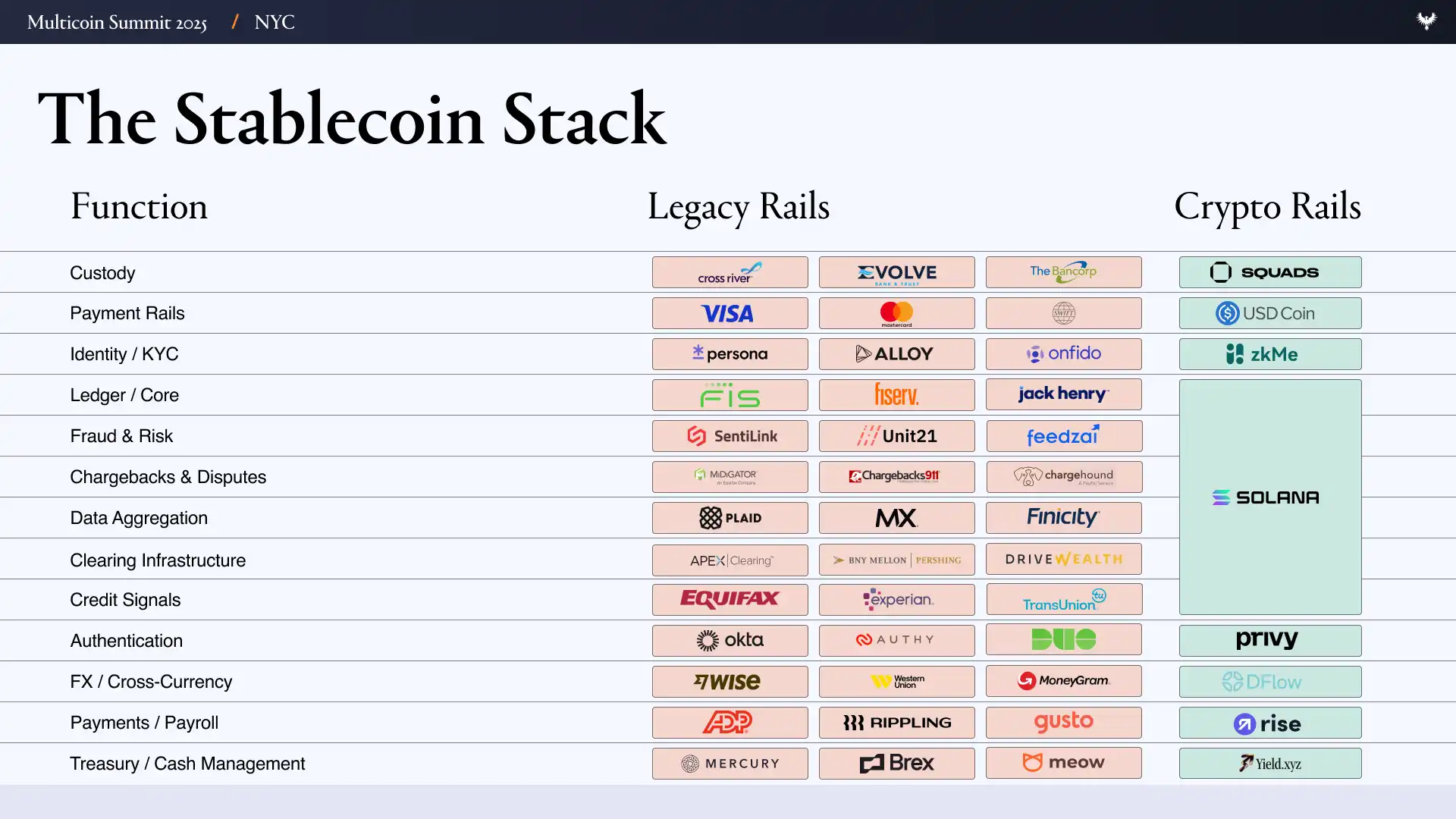

To understand the practical implications of this shift, one must first look at how today’s fintech is built. A typical fintech company relies on a vast vendor tech stack:

- User Interface / User Experience (UI/UX)

- Banking and Custody Layer: Evolve, Cross River, Synapse, Treasury Prime

- Payment Rails: ACH, Wire, SWIFT, Visa, Mastercard

- Identity and Compliance: Ally, Persona, Sardine

- Fraud Prevention: SentiLink, Socure, Feedzai

- Credit / Lending Infrastructure: Plaid, Argyle, Pinwheel

- Risk and Capital Management Infrastructure: Alloy, Unit21

- Capital Markets: Prime Trust, DriveWealth

- Data Aggregation: Plaid, MX

- Compliance / Reporting: FinCEN, OFAC Checks

Launching a fintech company on this tech stack means managing contracts, audits, incentives, and failure modes across dozens of partners. Each layer adds costs and delays, with many teams spending as much time coordinating infrastructure as they do building products.

Native stablecoin systems compress this complexity entirely. Functions that previously required six or seven vendors can now be consolidated into a few on-chain primitives.

In the world of stablecoins and permissionless finance: banks and custody are replaced by Altitude; payment rails are replaced by stablecoins; identity and compliance remain necessary, but we believe they can be implemented on-chain and kept confidential and secure through technologies like zkMe; credit and lending infrastructure will be restructured and migrated on-chain; capital market companies will lose significance after all assets are tokenized; data aggregation will be replaced by on-chain data and selective transparency, utilizing technologies like fully homomorphic encryption (FHE) to complete compliance and OFAC checks at the wallet level (for example, if Alice's wallet is on the sanctions list, she will not be able to interact with the protocol).

This is the true difference of Fintech 4.0: the underlying pipelines of finance are finally changing. People are no longer just developing an application that "quietly requests permission from banks" in the background, but are directly replacing large banking functions with stablecoins and open rails. Builders are no longer tenants; they are starting to own the "land."

Opportunities in "Specialized Stablecoin Fintech"

The first-order effect of this transformation is simple: fintech companies can do much more. When custody, lending, and fund transfers are almost free and instantaneous, starting a fintech company begins to resemble launching a SaaS product. In a stablecoin-native world, there are no sponsor bank integrations, card issuance intermediaries, multi-day settlement windows, or repetitive KYC audits to slow down progress.

We believe that launching a "finance-first" product will see fixed costs plummet from millions of dollars to thousands of dollars. Once infrastructure, customer acquisition costs (CAC), and compliance thresholds disappear, startups will be able to profitably serve smaller, more specific social groups through what we call "specialized stablecoin fintechs."

There is a clear historical analogy here. The previous generation of fintech began by serving specific customer groups: SoFi refinanced student loans, Chime offered early wage access, Greenlight launched debit cards for teenagers, and Brex served entrepreneurs who could not access traditional business credit. However, this specialization did not become a sustainable operating model: interchange capped revenue, compliance costs grew with scale, and reliance on sponsor banks forced teams to step out of their original niche markets. To survive, they were pushed to expand horizontally, and the additional products were not driven by strong user demand but were necessary to make the infrastructure scalable.

As crypto rails and permissionless finance APIs significantly lower startup costs, a new wave of stablecoin neobanks will emerge—each focusing on specific demographics, much like the early innovators in fintech. With significantly lower management costs, these new banks can focus on narrower, more specialized markets and maintain specialization: such as adhering to Islamic finance principles (Sharia-compliant), catering to the lifestyles of crypto "heavy players," or serving athletes with unique income and expenditure patterns.

The second-order effect is even stronger: specialization improves unit economics. CAC decreases, cross-selling becomes easier, and customer lifetime value (LTV) increases. Specialized fintech can precisely match products and marketing to high-conversion niche groups and cover specific demographics through stronger word-of-mouth. These companies achieve clearer paths to "more revenue per customer" while managing lower overhead than the previous generation of fintech.

As anyone can launch a fintech company within weeks, the focus of the question will shift from "who can reach customers?" to "who truly understands them?"

Exploring the Design Space of Specialized Fintech

The most attractive opportunities often arise where traditional rails fail.

Take adult creators and performers as an example: they generate billions of dollars in revenue each year but are often shut out by banks and card organizations due to reputation and chargeback risks. Payments are delayed for days, held up due to "compliance reviews," and they must pay 10-20% fees through high-risk payment gateways (like Epoch, CCBill, etc.). We believe that stablecoin-based payments can provide instant, irreversible settlements and programmable compliance, allowing practitioners to self-custody their income, automatically route portions of their income to tax or savings wallets, and receive payments globally without relying on high-risk intermediaries.

Looking at professional athletes, especially those in individual sports like golf and tennis, they face unique cash flow and risk structures. Income is concentrated in a short career window and often needs to be distributed among agents, coaches, and teams; they must pay taxes across multiple states and countries, and injuries can abruptly halt income. A stablecoin-native fintech could help them tokenize future income, make team payments using multi-signature wallets, and automatically withhold taxes by jurisdiction.

Luxury goods and watch dealers represent another market underserved by traditional financial infrastructure. These businesses often complete six-figure transactions via wire transfers or high-risk payment processors while waiting days for settlement when circulating high-value inventory across borders. Working capital is often locked in inventory in safes or display cases rather than bank accounts, making short-term financing both expensive and hard to obtain. We believe that stablecoin-native fintech can directly address these constraints: instant settlement for large transactions, credit lines secured by tokenized inventory, and programmable custody built into smart contracts.

When you see enough cases, you will find the same constraint repeatedly: banks are not good at serving users with globalized, uneven, or unconventional cash flows. But these groups can become profitable markets on stablecoin rails. We believe attractive theoretical examples of "specialized stablecoin fintech" include:

Professional athletes: income concentrated in the short term; frequent travel and relocation; may need to file taxes in multiple locations; team payments involve coaches, agents, trainers, etc.; may wish to hedge against injury risks.

Adult creators and performers: excluded by banks and card organizations; audiences spread globally.

Unicorn company employees: cash shortages, net worth highly concentrated in illiquid equity; high tax burdens when exercising options.

On-chain builders: net worth concentrated in highly volatile tokens; difficulties with fiat inflows and outflows and tax handling.

Digital nomads: no need for traditional passport banking relationships; automatic currency conversion; automated tax handling based on location; frequent travel and relocation.

Remittance scenarios for families/friends of incarcerated individuals: difficult and expensive to send funds through traditional channels.

Sharia-compliant: avoiding interest.

Generation Z: light credit banking services; gamified investing; socially-driven financial experiences.

Cross-border SMEs: high foreign exchange costs; slow settlements; working capital frozen.

Crypto heavy players (Degens): payment and credit experiences centered around high-risk preferences (like managing bills with a "gambling table" mindset).

Foreign aid: slow movement of aid funds, layered intermediaries, and lack of transparency; costs, corruption, and mismatches lead to significant "leakage."

Tandas / rotating savings clubs: naturally cross-border for global families; collective savings earn returns; potential to accumulate income history based on on-chain records for credit.

Luxury goods/watch dealers: working capital tied up in inventory; need for short-term loans; frequently conduct high-value, cross-border transactions; often transact via chat applications like WhatsApp and Telegram.

Conclusion

For most of the past two decades, innovation in fintech has focused on the distribution layer rather than the infrastructure. Companies have competed on branding, account opening experiences, and paid customer acquisition, but the capital itself still flows along the same closed rails. This has indeed expanded the accessibility of financial services but has also led to product homogenization, rising costs, and inescapably thin profits.

Stablecoins have the potential to change the economic logic of building financial products. By transforming functions like custody, settlement, credit, and compliance into open, programmable software, they significantly lower the fixed costs of launching and operating a fintech company. Capabilities that previously relied on sponsor banks, card networks, and large vendor stacks can now be built directly on-chain, with dramatically reduced management costs.

When infrastructure becomes inexpensive, specialization becomes possible. Fintech companies no longer need millions of users to become profitable; they can focus on those underserved by "one-size-fits-all" products. Groups like athletes, adult creators, K-pop fans, or luxury watch dealers share context, trust, and behavior patterns, making products easier to spread naturally rather than through paid marketing.

Equally important, these communities often exhibit similar cash flow characteristics, risks, and financial decision-making. This consistency allows products to be designed around people's actual income, expenditure, and capital management practices rather than based on abstract demographic categories. Word-of-mouth spreads not only because users know each other but because the products genuinely fit the operational ways of that group.

If our vision becomes a reality, this economic shift will be significant. As distribution becomes community-native, CAC decreases; as intermediaries exit, profit margins increase. Markets that once seemed too small or uneconomical will become sustainable, profitable businesses.

In this world, the advantages of fintech will shift from "scale and marketing spend" to "true contextual understanding." The next generation of fintech will not win by trying to serve everyone but by building infrastructure that aligns with the actual flow of capital while providing exceptional service to a specific group.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。