Author | @AvgJoesCrypto

Compiled by | Odaily Planet Daily (@OdailyChina)

Translator | Dingdang (@XiaMiPP)

Note from the editor: Recently, Haseeb Qureshi, a well-known partner at Dragonfly, published a long article rejecting cynicism and embracing exponential thinking, unexpectedly bringing the community discussion back to the core question: How much value does L1 still have? The following content is excerpted from @MessariCrypto's upcoming "The Crypto Theses 2026," organized by Odaily Planet Daily.

Cryptocurrency Drives the Entire Industry

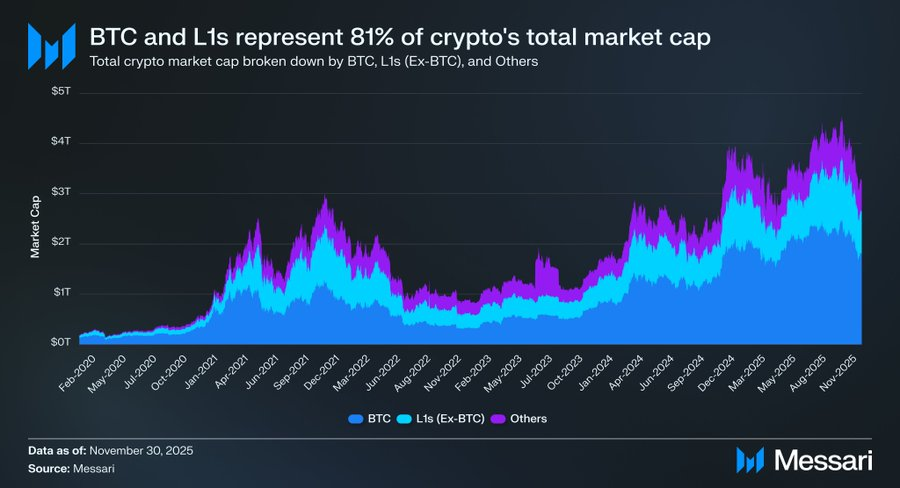

It is crucial to refocus the discussion on "cryptocurrency" itself, as most capital in the crypto industry is ultimately seeking exposure to "monetized assets." The current total market capitalization of the crypto market is $3.26 trillion, with BTC accounting for $1.80 trillion, or 55%. Of the remaining $1.45 trillion, approximately $0.83 trillion is concentrated in various L1 public chains. In other words, about $2.63 trillion, roughly 81% of the entire market, is invested in assets that the market already views as currency or believes may gain currency premiums in the future.

In this context, whether you are a trader, investor, capital manager, or developer, understanding how the market grants or withdraws currency premiums is essential. In the crypto industry, nothing drives valuation changes more than the market's willingness to regard an asset as "currency." Therefore, predicting which assets will gain currency premiums in the future is arguably the most critical variable when constructing a portfolio.

So far, we have mainly focused on BTC, but it is also necessary to discuss the L1 assets among the remaining $0.83 trillion that "may or may not be currency." As mentioned earlier, we expect BTC to continue to absorb market share from gold and other non-sovereign stores of value in the coming years. But this raises a question: How much space is left for L1? When the tide rises, do all boats (assets) float (benefit)? Or will BTC, in its pursuit of gold, also siphon off some currency premium from L1 public chains?

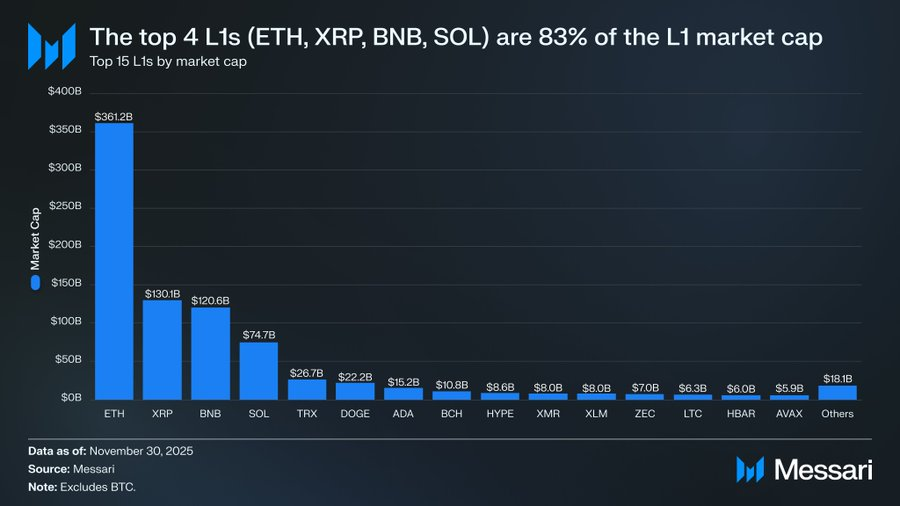

To answer these questions, we first need to look at the current valuation landscape of L1. The top four L1s by market capitalization—ETH ($361.15 billion), XRP ($130.11 billion), BNB ($120.64 billion), and SOL ($74.68 billion)—have a combined market capitalization of $686.58 billion, accounting for 83% of the entire L1 sector. After these top four, there is a significant gap in market capitalization (for example, TRX is $26.67 billion), but the tail still has a considerable size. The total market capitalization of L1s ranked 15th and below is still $18.06 billion, accounting for 2% of the total L1 market capitalization.

More importantly, L1 market capitalization does not equate to pure "currency premium." The valuation framework for L1 primarily consists of three components:

(i) Monetary Premium

(ii) Real Economic Value (REV)

(iii) Economic Security Demand

Thus, a project's market capitalization is not solely determined by the market's perception of it as currency.

Driving L1 Valuation is Monetary Premium, Not Revenue

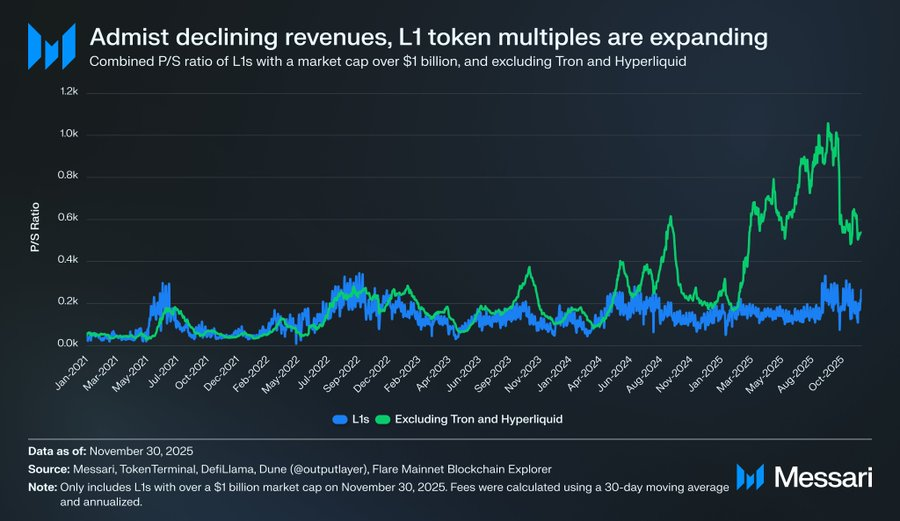

Despite the various valuation frameworks, the market increasingly tends to evaluate L1 from the perspective of "monetary premium," rather than from an "income-driven" angle. Over the past few years, all L1s with a market capitalization exceeding $1 billion have maintained an overall price-to-earnings ratio roughly between 150x and 200x. However, this overall data is misleading because it includes TRON and Hyperliquid. In the past 30 days, TRX and HYPE contributed 70% of the revenue for this group, yet only accounted for 4% of the total market capitalization.

After excluding these two outliers, the real story emerges. Despite declining revenues, L1 valuations have been rising. The adjusted price-to-earnings ratio shows a clear upward trend:

- November 30, 2021: 40x

- November 30, 2022: 212x

- November 30, 2023: 137x

- November 30, 2024: 205x

- November 30, 2025: 536x

If interpreted from the perspective of REV, one might think the market is pricing in future revenue growth. However, this explanation does not hold, as within the same group (still excluding TRON and Hyperliquid), L1 revenues have been declining almost every year:

- 2021: $12.33 billion

- 2022: $4.89 billion (YoY -60%)

- 2023: $2.72 billion (YoY -44%)

- 2024: $3.55 billion (YoY +31%)

- 2025: Annualized $1.70 billion (YoY -52%)

In our view, the simplest and most direct explanation is: These valuations are primarily driven by monetary premiums, rather than current or future revenues.

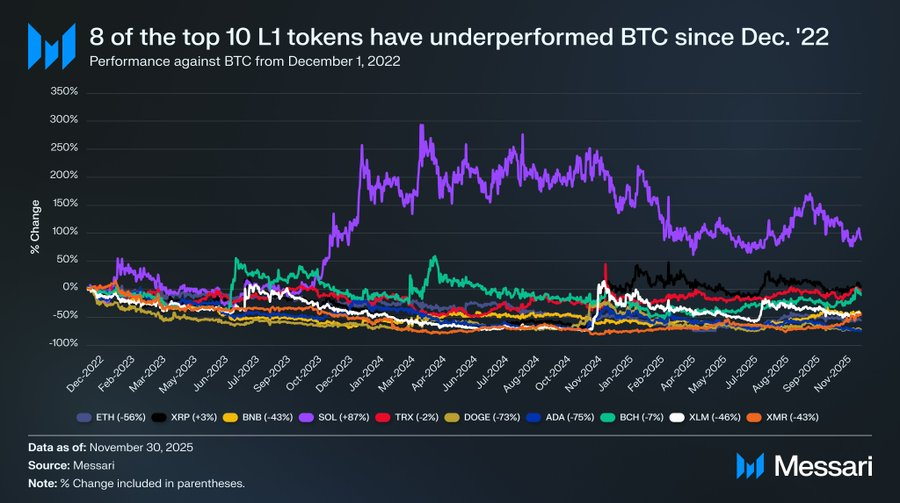

L1 Has Been Continuously Underperforming Bitcoin

If L1 valuations are mainly driven by the market's expectations of their monetary premiums, the next question is: What shapes these expectations? A simple method is to compare them with BTC's price performance. If changes in monetary premiums primarily reflect BTC's movements, then the performance of these assets should resemble BTC's "beta coefficient"; if the monetary premium comes from unique factors of each L1, then their correlation with BTC should be weaker, and their performance should be more distinctive.

As representatives of L1, we selected the top ten L1 tokens by market capitalization (excluding HYPE) and tracked their performance relative to BTC since December 1, 2022. These ten assets account for about 94% of L1 market capitalization, making them highly representative. During this period, eight assets underperformed BTC in absolute returns, with six lagging by over 40%. Only two assets outperformed BTC: XRP and SOL. However, XRP's excess return was only 3%, and given its historical dominance by retail funds, we won't overinterpret this. The only asset with significant excess returns is SOL, outperforming BTC by 87%.

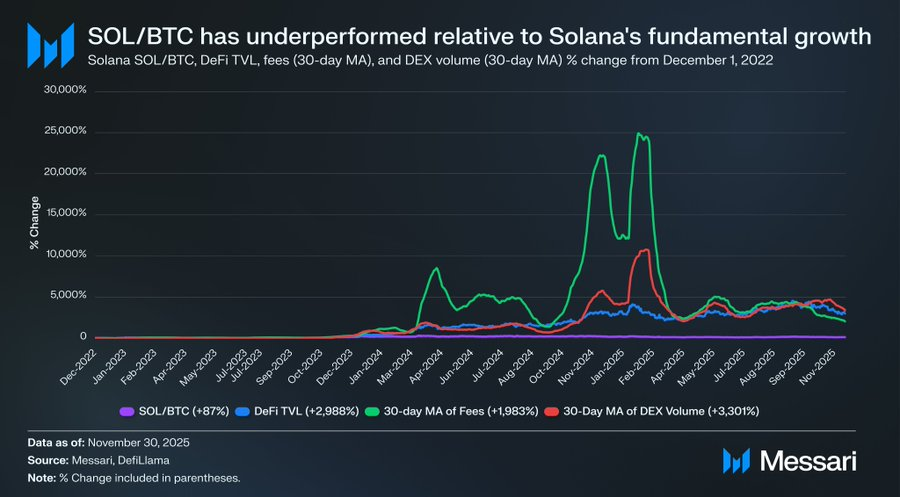

However, a deeper analysis reveals that SOL's "outperformance" may not be as strong as it appears. During the same period that SOL outperformed BTC by 87%, the fundamentals of the Solana ecosystem experienced exponential growth: DeFi TVL increased by 2,988%, transaction fees grew by 1,983%, and DEX trading volume surged by 3,301%. By any reasonable standard, Solana's ecosystem has expanded 20 to 30 times since the end of 2022, but the corresponding SOL price only outperformed BTC by 87%.

Please read that sentence again.

To achieve truly significant excess returns in the competition with BTC, an L1 does not need to grow its ecosystem by 200% or 300%—it needs to grow by 2,000%-3,000% to barely achieve a few percentage points of excess performance.

In summary, our judgment is: While the market continues to price L1 based on the expectation of "potential future monetary premiums," confidence in these expectations is quietly waning. Meanwhile, the market's confidence in BTC as the "cryptocurrency" has not wavered, and it can even be said that the lead of BTC over various L1s is continuing to expand.

Although cryptocurrencies themselves do not require transaction fees or revenue to support their valuations, these metrics are crucial for L1. Unlike BTC, the narrative of L1 depends on building ecosystems (applications, users, throughput, economic activity, etc.) to support its token value. However, if an L1's ecosystem is showing annual decline (partially reflected in declining revenues and transaction fees), it loses its unique competitive advantage relative to BTC. Without real economic growth, its "cryptocurrency" narrative will become increasingly difficult for the market to accept.

Looking Ahead

Looking ahead, we do not believe this trend will reverse in 2026 or beyond. With few possible exceptions, we expect the L1 sector to continue losing market share, further squeezed by BTC. As its valuation primarily relies on expectations of future monetary premiums, as the market gradually recognizes BTC's strongest claim to the "cryptocurrency" narrative, L1 valuations will continue to contract. Although BTC will also face challenges in the coming years, these issues are still too far from reality and have too many variables to provide effective support for the monetary premiums of competing L1s.

For L1, the threshold for proving its value has been raised. Its narrative is no longer sufficiently attractive compared to BTC and can no longer rely on market enthusiasm to support its valuation in the long term. The era where the story of "we may become currency in the future" could support a trillion-dollar market capitalization is closing. Investors now have a decade of data to prove: L1's monetary premium can only be sustained during extreme growth in the ecosystem. Once growth stagnates, L1 will continue to underperform BTC, and the monetary premium will dissipate accordingly.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。