Author: A Wang

The year 2025 for stablecoins is both exciting and fragmented, from the U.S. "Genius Act" defining stablecoins in regulatory terms, to Hong Kong passing the "Stablecoin Regulation," leading to a heated discussion on offshore RMB stablecoins and the game theory of digital RMB, culminating in the final chapter of stablecoins in mainland China in 2025.

Who is in the Red Mansion, and who is on the Journey to the West? It seems we all have answers in our hearts.

However, we need to look beyond the phenomenon to see the essence. We must clarify the logical context behind stablecoins in 2025 and understand the future development trends.

What fundamentally changes with stablecoins that attract global attention in 2025, and what remains unchanged?

At the 2025 Financial Street Forum Annual Meeting in October, Pan Gongsheng, Governor of the People's Bank of China, stated: "Since 2017, the People's Bank of China, together with relevant departments, has issued multiple policy documents to prevent and address the risks of domestic virtual currency trading speculation, and these policy documents remain effective. In the next step, the People's Bank of China will continue to work with law enforcement agencies to crack down on domestic virtual currency operations and speculation, maintain economic and financial order, and closely track and dynamically assess the development of overseas stablecoins."

We will focus on: "the policy documents remain effective" and "dynamic assessment of the development of overseas stablecoins."

I. The Attitude of Mainland Regulation Towards Virtual Currency Remains Unchanged — Continuous Crackdown

1.1 Mainland Regulation: The Virtual Currency Nature of Stablecoins

Recently, 13 ministries held a meeting to define the legal positioning of stablecoins under the mainland regulatory system definition.

On November 28, 2025, the People's Bank of China held a meeting of the coordination mechanism for combating virtual currency trading speculation. Officials from the Ministry of Public Security, the Central Cyberspace Affairs Commission, the Central Financial Office, the Supreme People's Court, the Supreme People's Procuratorate, the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Justice, the People's Bank of China, the State Administration for Market Regulation, the National Financial Regulatory Administration, the China Securities Regulatory Commission, and the State Administration of Foreign Exchange attended the meeting.

The meeting pointed out that in recent years, various units have earnestly implemented the decisions and deployments of the Party Central Committee and the State Council, and in accordance with the requirements of the "Notice on Further Preventing and Addressing the Risks of Virtual Currency Trading Speculation" jointly issued by the People's Bank of China and ten other departments in 2021, have resolutely cracked down on virtual currency trading speculation and rectified the chaos of virtual currencies, achieving significant results. Recently, due to various factors, speculation in virtual currencies has risen, and related illegal activities have occurred, posing new situations and challenges for risk prevention and control.

The meeting emphasized:

- Virtual currencies do not have the same legal status as legal tender, do not have legal compensation, and should not and cannot be used as currency in market circulation; activities related to virtual currencies are illegal financial activities.

- Stablecoins are a form of virtual currency and currently cannot effectively meet customer identity verification, anti-money laundering, and other requirements, posing risks of being used for money laundering, fundraising fraud, and illegal cross-border fund transfers.

The meeting required all units to adhere to Xi Jinping's Thought on Socialism with Chinese Characteristics for a New Era, fully implement the spirit of the 20th National Congress of the Communist Party of China and the previous plenary sessions, regard risk prevention and control as the eternal theme of financial work, continue to adhere to the prohibitive policy on virtual currencies, and continue to crack down on illegal financial activities related to virtual currencies. All units should deepen cooperation, improve regulatory policies and legal bases, focus on key links such as information flow and capital flow, strengthen information sharing, further enhance monitoring capabilities, severely crack down on illegal activities, protect the property safety of the people, and maintain the stability of economic and financial order.

1.2 No Change in Mainland Regulation's Attitude Towards Virtual Currency

- The meeting yesterday was a concrete implementation of the "Notice on Further Preventing and Addressing the Risks of Virtual Currency Trading Speculation" (Yin Fa [2021] No. 237) issued in 2021, reflecting that "the policy documents remain effective."

- Including stablecoins in the category of virtual currencies = stablecoins / activities related to virtual currencies are illegal financial activities. "Continue to adhere to the prohibitive policy on virtual currencies and continue to crack down on illegal financial activities related to virtual currencies."

- The rhetoric represents a trend towards stricter enforcement; previously, illegal financial activities related to virtual currencies were enumerated, but now they are directly generalized.

Although virtual currencies in China are recognized as a type of "virtual commodity" (partially recognized for their property attributes in criminal and civil judicial practice), as a "financial asset" or "settlement tool," their survival soil in mainland China has been completely eradicated.

1.3 Practitioners Remain Unchanged — Walking on Thin Ice

Despite stablecoins being included in the mainland regulation's category of virtual currencies, what has changed for industry practitioners?

In fact, nothing has changed; we are still going overseas, still on the path of compliance, holding licenses from relevant jurisdictions, and meeting regulatory requirements in various places. We are still walking on thin ice.

II. The Financial Infrastructure Based on Blockchain Has Changed — Dynamic Assessment of the Development of Overseas Stablecoins

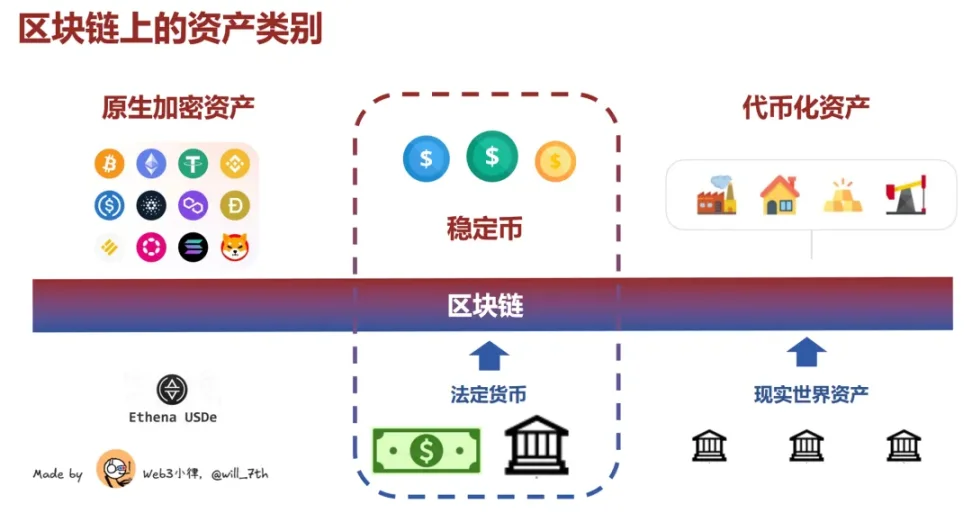

The U.S. "Genius Act" provides a clear definition for stablecoins:

"Payment stablecoins" are digital currencies that rely on distributed ledgers, are pegged to national legal tender, and are used for payments and settlements.

Let’s not discuss the various forms of digital currencies: stablecoins, deposit tokens, CBDCs.

What has changed? — The ledger underlying the assets has changed, becoming more efficient, more convenient, and more globalized.

This is the point that Europe and America are flocking to, as expressed by the CEO of Blackrock, that "asset tokenization" will lead the next financial revolution; it is the "historic" meeting of the Federal Reserve actively discussing embracing innovation; it is the direction of reform for the Nasdaq stock exchange: tokenized trading, tokenized IPOs, and 24/7 trading.

This is also the point that mainland regulation needs to dynamically assess — the financial infrastructure based on blockchain, regardless of what kind of digital assets are running on top of it.

2.1 Starting from the Origin of Blockchain

As Dr. Xiao said, we need to start from the origin of blockchain, looking at it from first principles, from the basics, to examine the currently hotly debated digital currencies / crypto assets, the crypto market, and the underlying blockchain technology.

What is the essence of finance? It is the mismatch of value across time and space. This essence remains unchanged for millennia.

New finance based on blockchain can greatly enhance financial efficiency:

- Across time. On one hand, it reflects the time value of money; on the other hand, it reflects transactions and settlements.

- Across space. Globally, it enables cross-space value allocation.

- The way of value transmission.

Just as the essential attributes of currency (value scale) and core functions (medium of exchange) remain unchanged, despite experiencing various forms of currency such as shells, tokens, cash, deposits, electronic money, and stablecoins, the essence of finance also remains unchanged. The question is how to provide better financial services in a distributed, digital, and time-space-crossing scenario.

2.2 New Financial Infrastructure

Compared to traditional finance, the biggest innovation of new finance is the change in accounting methods — the blockchain as a public, transparent global public ledger. The way humans keep accounts has only changed three times in thousands of years, each time profoundly shaping economic forms and social structures, and each breakthrough reflects the co-evolution of technology and civilization.

- The single-entry bookkeeping of the Sumerian period (around 3500 BC) allowed humans to break through the limitations of oral communication for the first time, facilitating early trade and the formation of states, as there was a need to record taxes and trade. The "Code of Hammurabi" from ancient Babylon included clauses on commercial disputes.

- Double-entry bookkeeping played a role in the commercial revolution of the Renaissance (14th-15th centuries), as the trade prosperity of Mediterranean city-states, investments by the Genoese fleet, and the Medici family's multinational banking required complex financial tools, thus promoting the emergence of banks and multinational companies and the establishment of commercial credit.

- Following this was the distributed ledger driven by Bitcoin in 2009, which facilitated decentralized finance, changes in trust mechanisms, and the rise of digital currencies.

This new finance, based on the transformation of distributed ledger methods, is inevitably intertwined with blockchain, smart contracts, digital wallets, and programmable currencies. The structure of blockchain as a financial infrastructure ledger settlement layer was initially designed to solve the final consistency problem of payment and settlement. The combination of digital currencies built on distributed ledgers and smart contracts can bring infinite possibilities to new finance: near-instant settlement, 24/7 availability, low transaction costs, and the programmability, interoperability, and composability of digital currency tokens with DeFi.

Thus, new finance mainly presents three major changes:

- First, the accounting method has changed from centralized double-entry bookkeeping to decentralized distributed bookkeeping;

- Second, accounts have changed from bank accounts to digital wallets;

- Third, the unit of accounting has changed from legal tender to digital currency.

The most important distributed bookkeeping arises from the digital characteristics of crossing time, space, and organizations.

2.3 The Huge Change in Financial Infrastructure

Therefore, regardless of the various forms of digital currencies: stablecoins, deposit tokens, CBDCs, the financial infrastructure based on blockchain has undergone tremendous changes.

What seeds are sown here?

The uniqueness of digital currencies lies in their simultaneous presence at the intersection of three massive markets: payments; lending; capital markets. Not to mention the future value channels of AI silicon-based civilization.

Despite the waves of de-globalization caused by geopolitical factors, we will still be aligned by the unified ledger of blockchain, and you will find that this world is indeed flat. Just like what is said in that book: "We wanted transoceanic flights, but we invented Zoom."

III. In Conclusion

In fact, the key points of "the policy documents remain effective" and "dynamic assessment of the development of overseas stablecoins" still guide us in the right direction. Although the reality of stablecoins in 2025 seems to present a magical scenario of "you are in the Red Mansion, I am on the Journey to the West."

"I am on the Journey to the West" — it is about leaving, about cultivation, about the obsession of enduring 81 hardships, and about the ambition to explore the next generation of financial infrastructure.

In 2008, Modern Sky released a music compilation titled "You Are in the Red Mansion, I Am on the Journey to the West," inspired by "Dream of the Red Chamber" and "Journey to the West," reinterpreting classic tracks, forming a cultural dialogue between the classical and the modern, the East and the West, the dreamlike and the real.

You walk your old dreams in the mortal world, and I embark on my journey of thousands of miles.

But in the end, we may all arrive at the same destination through different paths.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。