In addition to the possible reasons related to China, I also saw a piece of data that might be a trigger for the decline in the risk market. Of course, I am not certain; I am just sharing what I observed. Logically speaking, I actually think the possibility of the yen being the trigger point is greater, after all, it won't be China's cryptocurrency policy that drives down the U.S. stock market.

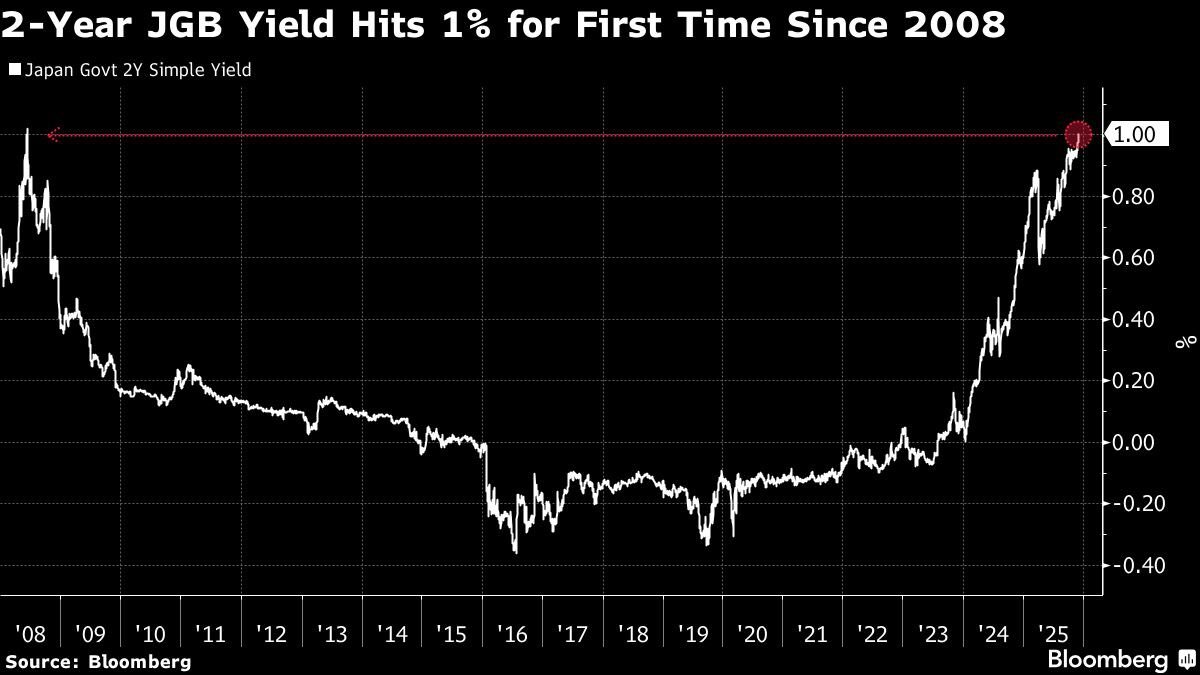

Japan's 2-year government bond yield has surpassed 1%, marking the first time since 2008, and the last time Japan's 2Y reached 1% was before the financial crisis. This means that Japan has effectively entered an interest rate hike era, and the framework of zero interest rates and YCC is being repriced.

The change in Japan's interest rate structure is not just a problem for Japan, but the starting point for changes in global capital flows. The yen is the largest funding currency globally, and the rise in Japanese interest rates is leading to a marginal contraction in carry trades.

Over the past decade, a significant portion of global liquidity has come from the low-interest borrowing of yen, flowing into high-yield assets such as U.S. Treasuries, stocks, credit bonds, and even $BTC. The combination of low financing costs and a stable exchange rate has made the arbitrage space very stable.

However, now that Japan's short-term yields have returned to 1%, the interest rate differentials are being rapidly compressed, and cross-currency arbitrage is no longer cost-free, with the possibility of turning into losing trades (although it is still cheap currently, the direction has changed).

Institutions are forced to reduce their positions in risk assets to lower leverage, leading to a global "de-leveraging" reflex effect. The return of yen funds means a decrease in marginal demand for U.S. Treasuries, U.S. stocks, and crypto assets, while the attractiveness of domestic Japanese assets is rising. The narrowing interest rate differential between the dollar and the yen also puts greater pressure on the dollar. Once the exchange rate begins to adjust directionally, systemic funds will preemptively reduce risk.

The breaking of Japan's short-term yield above 1% is not just an ordinary interest rate event; it could trigger a re-pricing of global arbitrage structures, subsequently affecting U.S. Treasury yields, the strength of the dollar, the volatility of risk assets, and ultimately feedback into the overall market's risk appetite. The tweet I referenced is about why Japan's YCC would impact the risk market; interested friends can take a look.

Especially in a high-leverage carry trade state, strategy funds will be highly sensitive to changes in yen interest rates, and the market often experiences short-term selling pressure during these marginal changes in liquidity structures.

In simpler terms, Japan's effective interest rate hike increases the costs for investors who previously borrowed in yen, as they fear that further cost increases may offset profits, leading them to exit early.

Of course, this is just speculation!

Bitget VIP, lower fees, better benefits

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。