Abstract

• Strategy pioneered the establishment of digital asset treasuries, leading more publicly listed companies to follow in its footsteps and open a new chapter in DAT. By 2025, the scale of DAT experienced explosive growth, with Ethereum DAT igniting a new wave of staking.

• The core logic of the DAT model is the capital cycle of "financing - buying coins - refinancing," which binds traditional capital market financing methods with the price appreciation of digital assets, forming a self-reinforcing flywheel. The market value changes of DAT are primarily determined by the growth in the number of tokens per share, the price of underlying assets, and mNAV, which together influence its attractiveness and risk level in the capital market.

• As institutional funds continue to enter the Ethereum ecosystem, DAT companies have evolved from mere token holders to network participants and revenue creators. Their main entry paths include staking, DeFi, and on-chain operations. Solana DAT may become one of the fastest-growing and strongest tracks within the DAT model.

• By constructing a five-force model for DAT sustainability, we believe that Bitcoin DAT is evolving towards long-term value storage, emphasizing anti-inflation narratives and institutional allocation. Ethereum and Solana DAT are developing into revenue-generating treasuries, creating cash flow through on-chain operations. DATs that can truly withstand cycles must possess a robust capital structure, transparent financial disclosures, and clear strategic positioning. The future winners will not be numerous "shell companies" lacking core business, but rather a few leading firms that can simultaneously create a flywheel effect at both the capital market financing end and the on-chain ecosystem participation end.

1. Introduction

As global attention on digital assets continues to rise, regulatory policies in various countries become clearer, and the underlying technology and ecosystem of blockchain mature, digital asset treasuries (DAT) are becoming a new capital narrative in traditional finance.

DAT companies refer to publicly listed enterprises that use cryptocurrencies as core reserve assets on their balance sheets. Unlike "crypto-native companies," the primary valuation drivers for these companies are not their main business revenues but the value fluctuations of their held digital assets. These companies raise funds from shareholders through equity financing, convertible bonds, and other means, then invest the proceeds into digital assets, boosting investor confidence while driving their stock prices higher, thus forming a cycle of "financing - holding coins - valuation increase" in the capital market.

On the surface, the DAT model seems to be merely "public companies buying coins," but in reality, it has evolved into various sub-forms: from the single asset passive holding model represented by Strategy to the multi-asset portfolio model that achieves active management through staking, liquidity mining, and DeFi yields. The emergence of DAT companies transforms the risk exposure of digital assets, which was previously limited to on-chain investors, into tradable investment targets in the traditional stock market, thereby providing a bridge for a broader range of investors to enter the crypto market. In this process, DAT is no longer just a price follower in the Beta market but may become a source of Alpha driving the continuous growth of the on-chain ecosystem.

However, DAT is not without risks as a "financial innovation model." Its sustainability largely depends on the market cycle of the underlying assets. When digital asset prices plummet and liquidity tightens, DAT shell companies, which lack core business and cash flow, often bear the brunt, struggling to withstand the dual blows of asset depreciation and financing interruption, and may even face liquidation risks. In other words, DAT acts as an amplifier in bull markets and a magnifying glass in bear markets.

This report will evaluate the long-term sustainability of the DAT model from five dimensions, exploring the stability of token prices and treasury scales for the development of DAT.

2. The Origin and Evolution of DAT

When discussing the origin of DAT, one must mention a legendary company—Strategy, which is both a veteran in business intelligence software services and a pioneer in the Bitcoin wave. From its lows to its peaks, Strategy's journey has not only aligned with the trends of the times but also pioneered the establishment of digital asset treasuries. Now, it serves as a classic case in business history, adding more dimensions to discussions in the cryptocurrency industry.

1. Where the DAT Model Began

1.1 Strategy's Bitcoin Strategy

Strategy Inc. (NASDAQ: MSTR) was the first to propose the DAT company strategy, positioning Bitcoin as its corporate reserve asset.

This North American software company, founded in 1989, initially focused on the development and sales of enterprise business intelligence (BI) software. It experienced rapid growth during the internet bubble of the 1990s and went public in 1998. However, in 2000, the company was investigated by the SEC due to a financial fraud scandal involving "premature revenue recognition," causing its stock price to plummet by over 90%, becoming a typical case of the bubble burst. Over the next twenty years, Strategy struggled to make significant progress in competition with much larger software giants like Microsoft, with its market capitalization fluctuating mostly between $1 billion and $2 billion.

The turning point came in 2020 when the company's founder, Michael Saylor, reassessed Bitcoin's value during the COVID-19 pandemic. Prior to this, Michael Saylor was a staunch opponent of cryptocurrencies, believing Bitcoin was worthless and that investing in it was a foolish idea. However, during the pandemic, countries adopted loose monetary policies to stimulate the economy, leading to currency devaluation and heightened inflation risks. Michael Saylor believed that when the money supply grows at a rate of 15% per year, people need a hedge asset that is not tied to fiat cash flows. After thoroughly studying the underlying logic of blockchain, he discovered that Bitcoin, which naturally halves every four years, not only resists inflation but also, due to various restrictions in the cryptocurrency market, some individual and institutional investors cannot directly invest in or leverage Bitcoin. By holding it indirectly through stocks, new markets could be opened. Therefore, Michael Saylor resolutely chose to challenge traditional investment concepts, abandoning traditional quality assets, and while many companies opted to buy bonds and forgo around 7% of shareholder equity, he made the groundbreaking choice of "digital gold" Bitcoin [1].

1.2 From "Corporate Reserve Assets" to "Per Share BTC" Logic

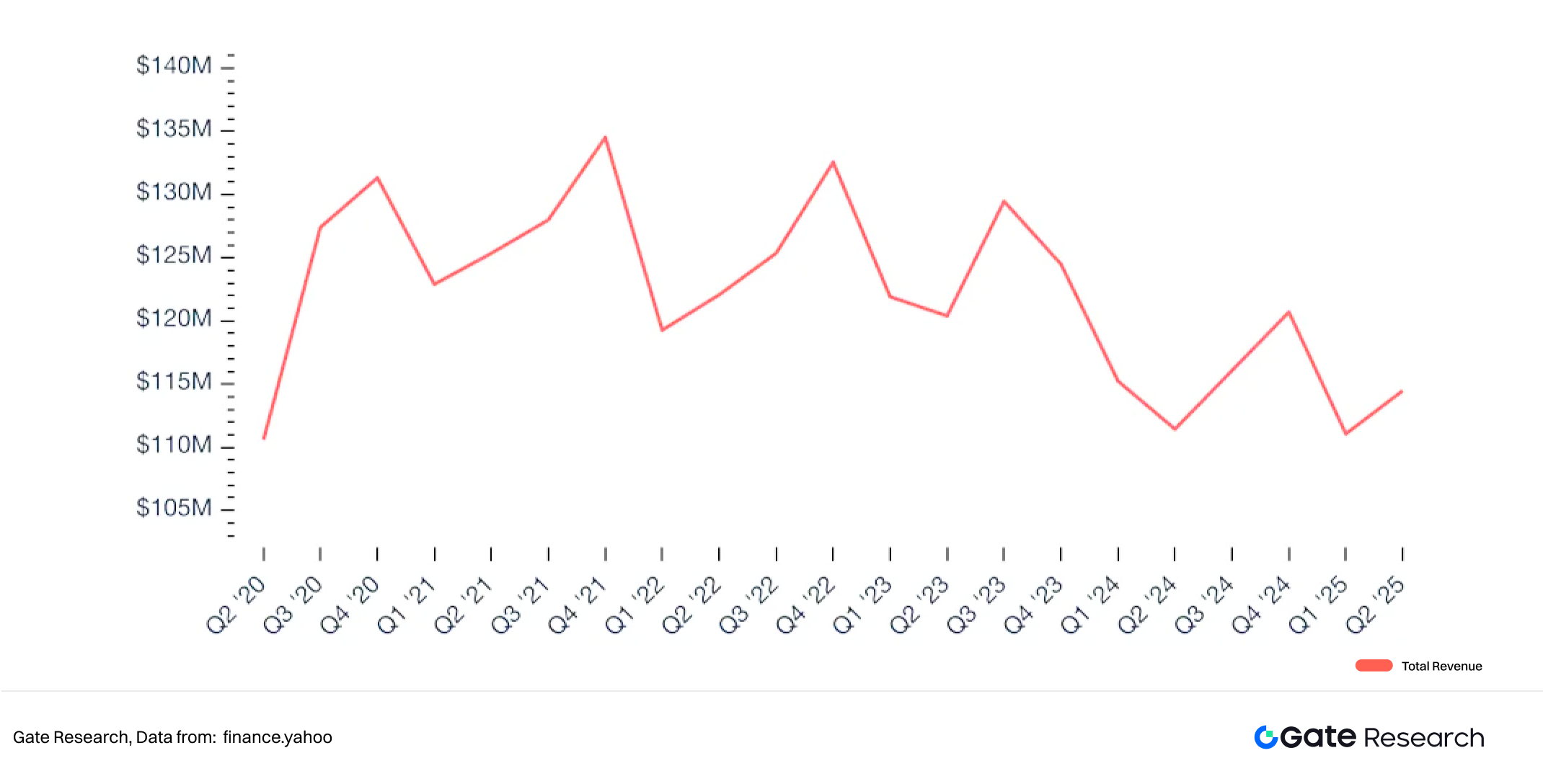

From Strategy's 2020 financial report, the main business revenue from software was only tens of millions of dollars, but considering the operational accumulation over twenty years, the total cash reserves were about $500 million. The initial Bitcoin investment was made using the company's idle funds: in August 2020, it spent $250 million to purchase 21,454 Bitcoins [2], marking Strategy's transformation from a traditional software company to a Bitcoin-holding DAT company.

Figure 1: Strategy's Quarterly Software Business Revenue

If Strategy relied solely on operational cash flow, it would be unable to quickly expand its Bitcoin position, especially since the market was in a zero-interest-rate environment, with investors strongly pursuing high-growth assets. Thus, Michael Saylor thought of utilizing the capital market for low-cost financing. Subsequently, Strategy implemented a Bitcoin flywheel model centered on self-funding and debt financing (including convertible bonds, preferred secured bonds, and equity issuance). In December 2020, Strategy issued $400 million in convertible bonds (0.75% interest rate, maturing in 2025) [3], with all funds used to buy Bitcoin. The advantage of issuing convertible bonds is that, as they are initially debt, they do not dilute equity, protecting shareholder rights. The initial few issuances had interest rates mostly between 0%-0.875%, with typical exercise premiums of 40-50%, indicating that investors recognized Strategy's long-term growth and wanted to become its shareholders. By early 2021, Bitcoin's price soared to $60,000, and the book value of this portion of Bitcoin was approximately five times the initial investment, significantly altering the market's pricing of Strategy. As the Bitcoin strategy began to show results, the stock price continued to rise, and Strategy also adopted market price stock issuance for financing. To greatly reduce shareholders' concerns about stock dilution, Strategy innovatively created a metric called "BTC Yield," which indicates the ratio change between the company's Bitcoin holdings over a certain period and the assumed diluted shares outstanding, helping to assess whether the company has truly converted the financing into more Bitcoin without severely diluting existing shareholders.

BTC Yield = Total BTC Holdings / Diluted Shares Outstanding

From then on, Strategy became the largest institutional holder of cryptocurrencies, with its stock price highly correlated with Bitcoin, reaching a historical high of $473.83 in November 2024, an increase of 3,734% from when it first began purchasing Bitcoin. Strategy's success also reshaped the narrative in the capital markets, leading more publicly listed companies to follow in its footsteps and open a new chapter in DAT.

Figure 2: Strategy's Stock Price Highly Correlated with BTC After 2020

2. Spread and Wave of the DAT Model

2.1 Explosive Growth of DAT Scale in 2025

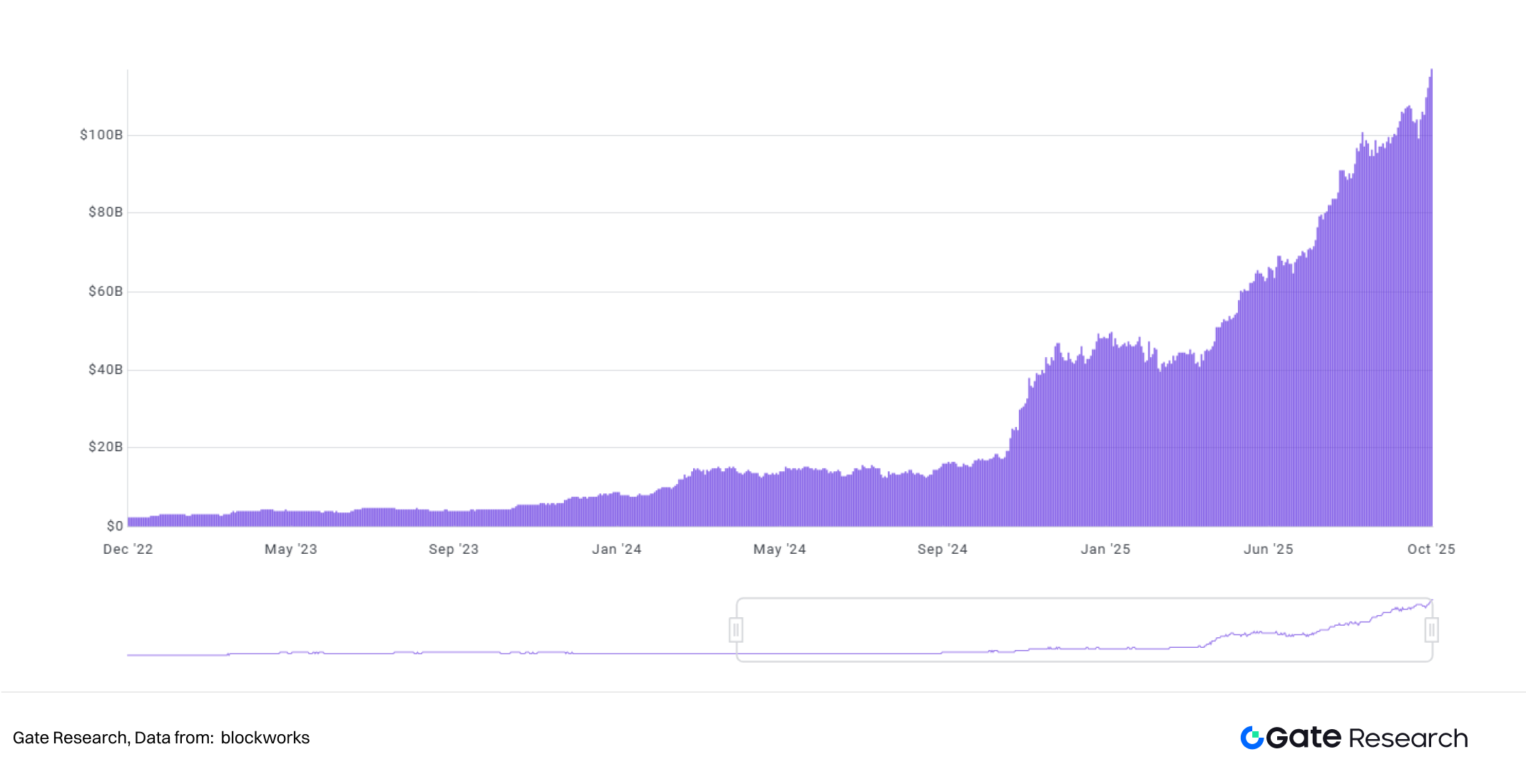

Taking Bitcoin, the most sought-after asset by capital, as an example, in 2020, publicly listed companies globally held a total of 4,109 Bitcoins, which accounted for only 1.49% of all institutional holders (including governments, ETFs, private foundations, etc.), having an extremely limited impact on the overall market. However, as the cryptocurrency ecosystem gradually matured and Bitcoin prices continued to rise, coupled with the emergence of the DAT model, publicly listed companies began to enter the Bitcoin market on a large scale. In 2021, the holdings of publicly listed companies surged to 155,196 Bitcoins, more than tripling from 2020, marking the initial formation of the DAT cryptocurrency trend. With the continued influx of institutional funds, the holdings of publicly listed companies further expanded to 306,765 Bitcoins in 2022. Although market fluctuations in 2023 led some companies to reduce their holdings, bringing the total down to 293,042 Bitcoins, by 2024, the number climbed back up to 361,144 Bitcoins, indicating a more robust overall strategy among publicly listed companies. By 2025, this trend experienced explosive growth, with holdings surpassing one million Bitcoins in July. As of October 2, the total reached 1,130,679 Bitcoins, significantly increasing its proportion of the total circulating Bitcoin supply to 5.38% [4]. This shows that publicly listed companies have shifted from cautious initial explorations to strategic, long-term Bitcoin treasury layouts, reflecting not only the capital market's recognition of Bitcoin as "digital gold" but also signaling that the DAT model is accelerating its diffusion, becoming a new narrative for corporate value management and capital operations.

Figure 3: Significant Increase in Holdings of DAT Companies Starting in 2025

2.2 Dominance Remains in North America, Asian Markets Accelerate Catch-Up

Currently, Bitcoin DAT companies are distributed across 199 countries and regions globally, but the dominant force remains concentrated in the North American market—holding a core position in terms of the number of companies, financing channels, and capital market influence. The United States has 71 DAT companies, which, leveraging the mature disclosure mechanisms of NASDAQ and the stock market, can smoothly incorporate cryptocurrency asset allocations into their treasury strategies through equity, convertible bonds, and other tools. Canada follows closely with 33 DAT companies, benefiting from a relaxed regulatory environment and inclusivity towards crypto funds, making it the second-largest DAT hub.

In the past year, the Asian DAT market has accelerated its catch-up, particularly with localized explorations in Hong Kong and Japan gradually taking shape. Japan has 12 DAT companies, Hong Kong has 10, and mainland China has 9, showing a trend towards gradual decentralization. The Japanese market has seen some companies related to the Tokyo Stock Exchange or financial funds begin to allocate cryptocurrency assets, with the most representative being the Bitcoin tracker Metaplanet Inc., which started publicly disclosing its Bitcoin holdings in 2024 and is regarded as "Japan's MicroStrategy," quickly becoming a benchmark case driving the diffusion of the DAT model in Japan. Meanwhile, Hong Kong has seen the emergence of DAT pilots represented by cryptocurrency exchanges and fund companies, driven by the Hong Kong Stock Exchange and crypto trading platforms, reflecting mutual promotion from both policy and market sides. Notably, DAT companies are no longer limited to technology or finance backgrounds; their main business covers a wide range, from biotechnology and e-commerce to services and even nail salons, demonstrating the universality of this trend.

2.3 Ethereum DAT Ignites a New Wave of Staking

At the same time, the asset categories within the DAT model are also expanding. Initially, almost all focus was on Bitcoin, but the capital market has never ceased seeking the next "Bitcoin-like" asset or even one that surpasses Bitcoin—an asset that possesses both store of value properties and the potential for additional returns. Ethereum and Solana are representatives of this trend: they not only have active smart contract ecosystems and DeFi application scenarios but also provide staking rewards for holders under the PoS consensus mechanism, thus being seen as the next stop in the DAT track.

Figure 4: Significant Increase in Ethereum Holdings of DAT Companies in 2025

The narrative similar to Bitcoin reserves began to shift towards Ethereum in mid-2025, with actions including ecosystem participation and staking, among which BitMine Immersion Technologies and SharpLink Gaming are two key drivers.

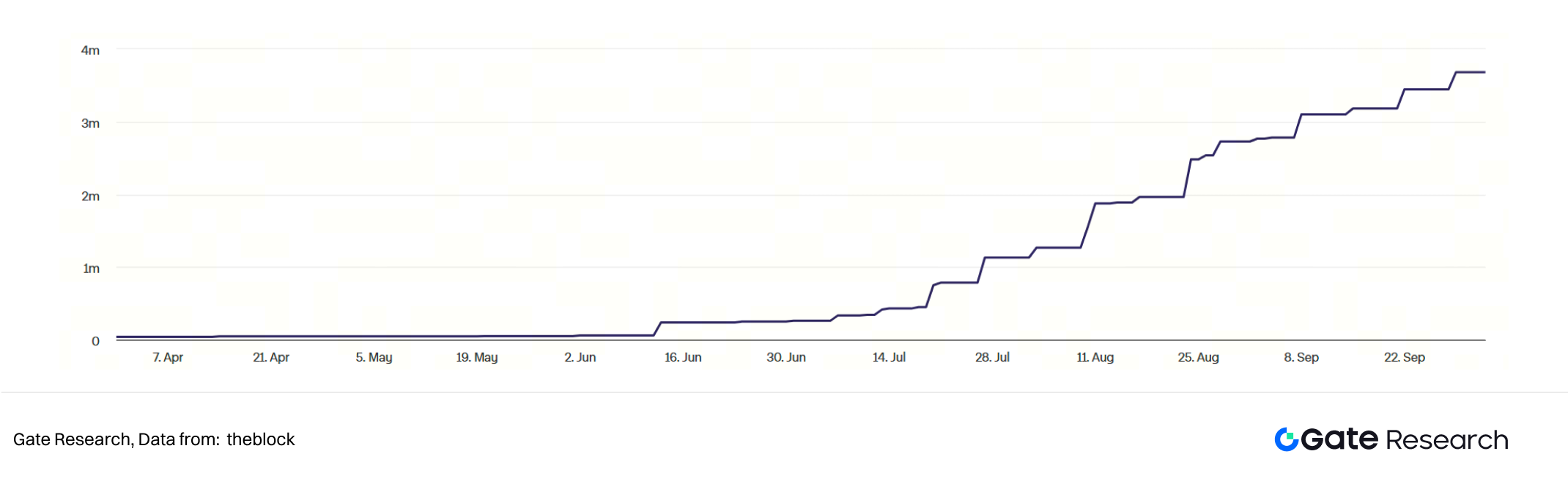

BitMine (NYSE: BMNR) initially focused on Bitcoin mining and infrastructure, also offering crypto mining machine hosting and operations. In July, it transformed into an Ethereum reserve entity through a $250 million private placement (PIPE) [5]. BitMine stated that Ethereum's smart contract capabilities, stablecoin payments, and tokenized assets were key reasons for its ETH reserves. Following the announcement of its Ethereum reserve, BitMine's stock surged significantly in the short term, reflecting market enthusiasm and confidence in this model. As of October 3, 2025, its Ethereum reserves rapidly reached 2,650,900 ETH, accounting for 2.2% of the total Ethereum supply, making it the largest reserve company for Ethereum.

On the other hand, SharpLink Gaming (NASDAQ: SBET), the second-largest participant in the Ethereum treasury, primarily operated in online gaming, esports, gambling, and sports entertainment. Although it is not a crypto-native company, it operates flexibly in the capital market. SharpLink Gaming launched its Ethereum treasury strategy in June, acquiring Ethereum outside of Bitcoin through ATM equity financing and allocating over 95% of its Ethereum reserves for staking to generate passive income. SharpLink maintains high-frequency disclosures, providing transparency and traceability to the market. As of October 3, 2025, SharpLink's Ethereum reserves reached 838,728 ETH, accounting for 0.7% of the total Ethereum supply. These two companies represent the leap of the Ethereum DAT model from concept to large-scale capital market practice.

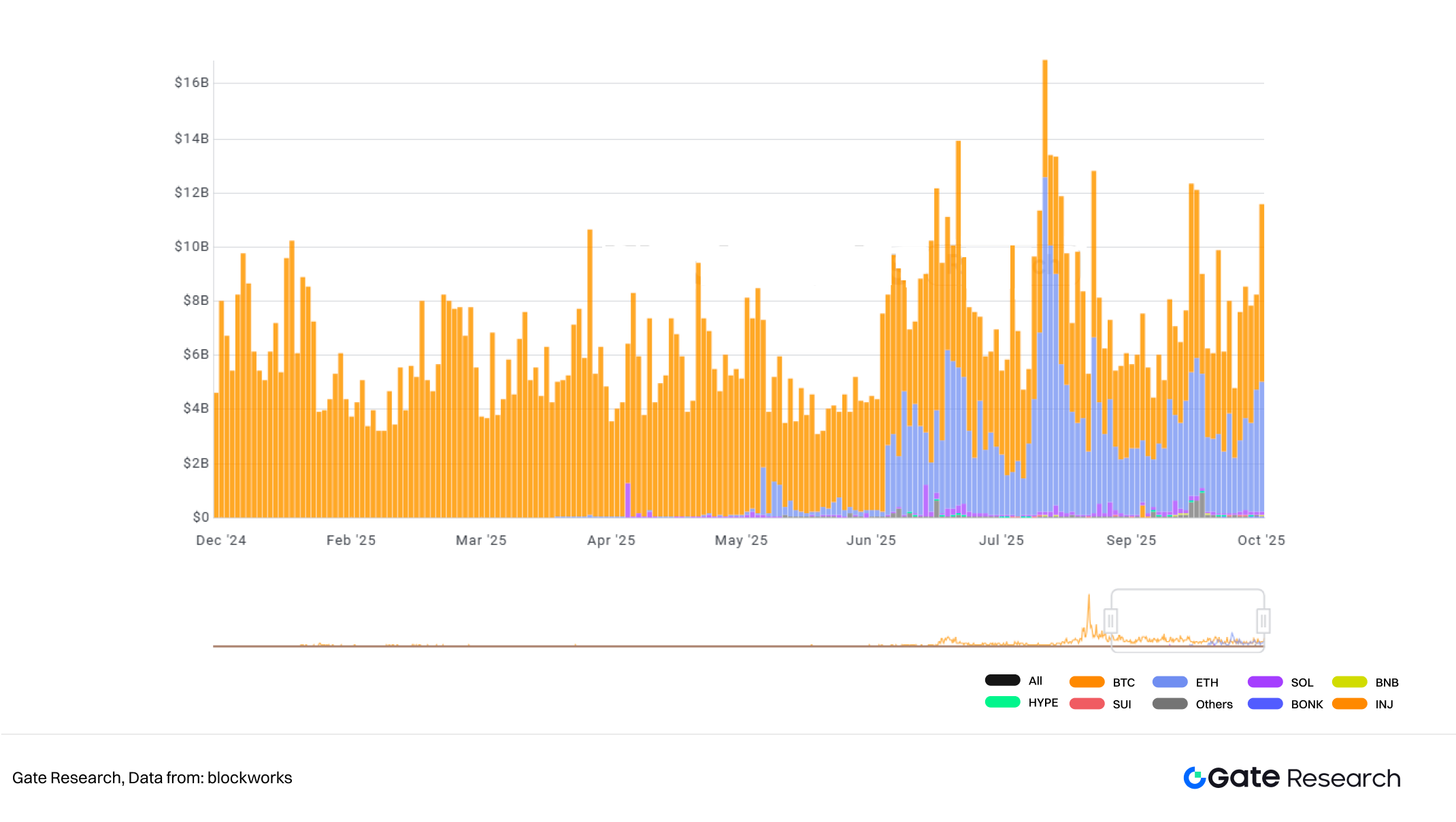

Figure 5: Bitcoin and Ethereum as the Most Popular Targets for DAT Companies

Now, more companies are incorporating other public chain tokens such as Ethereum, Solana, Dogecoin, and Sui into their reserve assets to increase the diversity and potential returns of their portfolios. As of October 2025, 13 companies have disclosed holdings of Ethereum, totaling 4,029,665 ETH, equivalent to 3.33% of the total ETH supply. For Solana, 9 companies have publicly disclosed holdings, totaling 13,441,405 SOL, approximately 2.47% of the total SOL supply. For Dogecoin, 2 companies have publicly disclosed holdings, totaling 780,543,745 DOGE, about 0.52% of the total DOGE supply. For Sui, 2 companies have publicly disclosed holdings, totaling 102,811,336 SUI, approximately 2.84% of the total SUI supply [6]. This multi-chain expansion indicates that DAT is no longer just a "single asset Bitcoin" story but has evolved into a cross-chain, multi-asset corporate capital strategy, laying the foundation for the future position of digital assets in the global capital market.

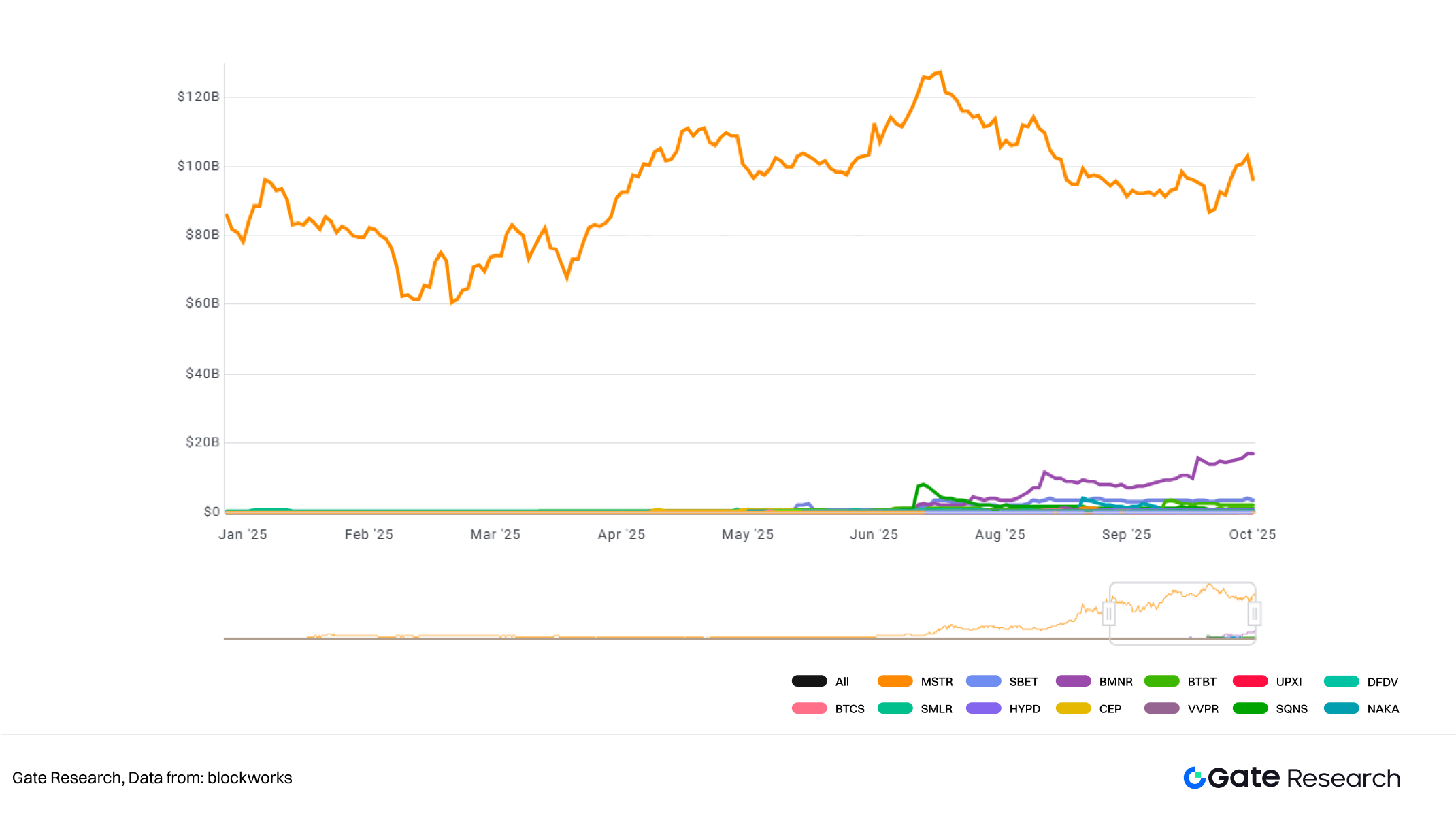

Figure 6: Market Capitalization Comparison of Popular DAT Companies

3. The Operational Logic of DAT

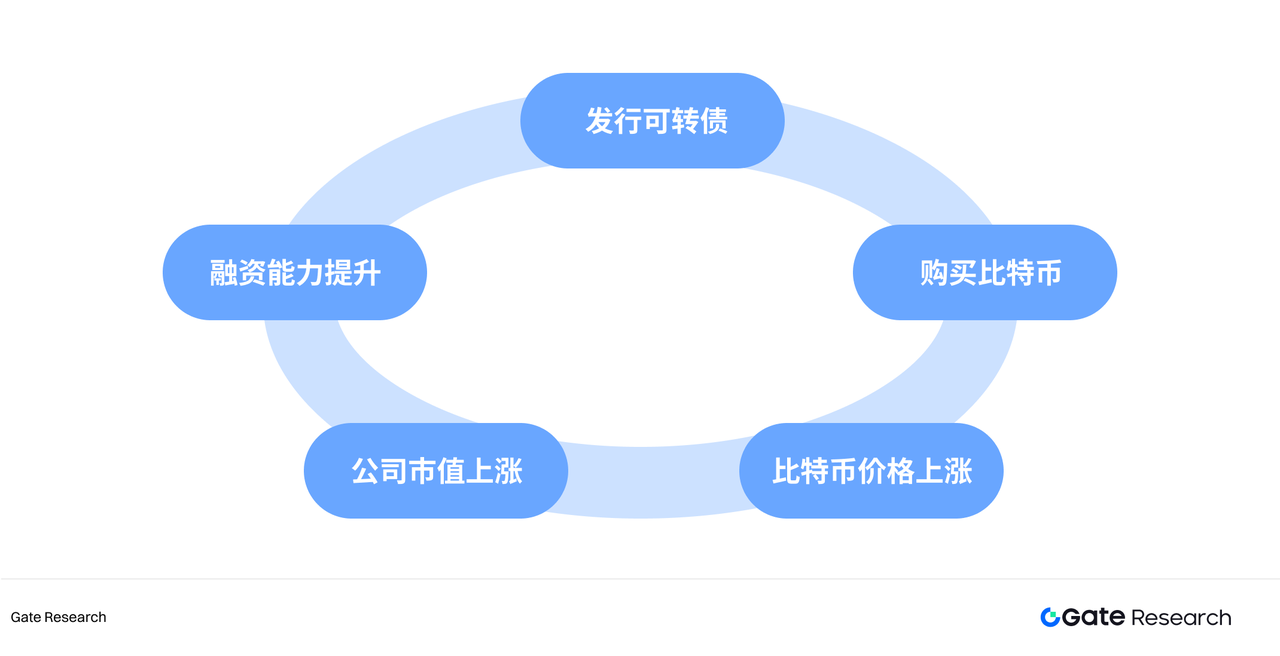

Some crypto companies have opened public market financing channels through shell resources in the capital market, completing the capital cycle through the core logic of the DAT model of "financing - buying coins - refinancing." DAT companies bind traditional capital market financing methods with the price appreciation of digital assets, forming a self-reinforcing flywheel.

1. Operational Methods

1.1 Acquiring Listings Through Shell Companies

Some companies do not start from scratch but quickly gain "entry tickets" to the capital market through special purpose acquisition companies (SPACs), reverse takeovers (RTOs), and other channels. For cryptocurrency companies, going public through a shell is an attractive alternative to regulatory hurdles and the lengthy IPO process. Once the acquisition is completed, these companies gain access to public market financing channels, allowing them to conduct equity financing as "compliant public companies" and use the raised funds to directly purchase Bitcoin, Ethereum, and other digital assets.

Representatives of such operations are mainly concentrated in emerging North American DAT companies. For example, on July 8, 2025, the newly established crypto asset management company Reserve One announced it would go public through a merger with M3-Brigade Acquisition V Corp. (NASDAQ: MBAV). This transaction is valued at $1 billion, including $298 million in trust capital, and has attracted strategic investors such as Galaxy Digital, Pantera Capital, and Kraken, who have committed to invest $750 million. Reserve One aims to accumulate a reserve of crypto assets covering Bitcoin, Ethereum, and Solana, and plans to use these assets for staking and lending [7].

The logic of this shell company acquisition is akin to a combination of "capital shell + crypto assets": while the use of shell resources in the capital market lowers entry barriers, this method of rapidly expanding the asset side by bypassing the traditional entrepreneurial cycle often comes with higher risks, as it lacks fundamental support. Shareholders may not only face dilution but also amplify the company's dependence on the price fluctuations of digital assets.

1.2 Financing Cycles Through Issuance, Bonds, and Convertible Bonds

Strategy pioneered the flywheel of "financing - purchasing tokens - valuation increase - refinancing," and this model has since been emulated by traditional publicly listed companies and shell-listed public chains, forming the operational model of the vast majority of DAT companies today. Specifically, DAT companies first utilize capital market financing, whether through stock issuance (ATM/PIPE) or issuing convertible bonds and corporate bonds, to obtain new cash inflows; subsequently, these funds are directly used to purchase Bitcoin, Ethereum, and other digital assets, thereby expanding the treasury scale. This cycle accelerates the binding of capital and digital assets. Strategy's successful case demonstrates the amplifying effect of this model in bull markets and provides a template for subsequent DAT companies (such as BMNR, BitMine, SharpLink, etc.).

Figure 7: DAT Company Flywheel Diagram

This model is particularly prominent among Ethereum-related DAT companies in 2025. BitMine's model is similar to Strategy: it continuously expands its balance sheet through convertible bonds and PIPE financing, becoming a milestone in shaping the institutionalization of Ethereum. SharpLink has adopted a more aggressive and frequent financing strategy. Since announcing the inclusion of Ethereum in its treasury in June 2025, SharpLink has rapidly raised funds through ATM equity financing and public stock issuance, and has allocated its Ethereum reserves to staking or liquid staking, transforming Ethereum's "productive" characteristics into sustainable cash flow. While critics argue that "full staking" increases exposure to on-chain protocol risks, supporters emphasize that this establishes a new paradigm for DAT companies exploring Ethereum as a productive asset.

2. Classification of DAT Strategy Operational Models

DAT is not just about "holding coins"; different models correspond to different management costs and requirements. Currently, DAT companies mainly operate under the following models:

Passive Single Asset Holding Model: Focused on a single cryptocurrency (usually Bitcoin or Ethereum), held long-term without selling. This model is relatively simple, with low management and decision-making costs, allowing for a consistent strategy regardless of asset price fluctuations. Its returns primarily come from capital gains from the appreciation of the cryptocurrency. Strategy is the most typical passive Bitcoin DAT, publicly committing to "buy and not sell," viewing Bitcoin as the company's main asset and strategic core.

Active Single Asset Trading Model: Although it also holds only one cryptocurrency, the management strategy involves active trading or dynamic allocation, such as timing trades, hedging strategies, and options strategies. This requires assessing the trading capabilities of the managers. Some Ethereum reserve companies may actively adjust their positions, reduce holdings, or switch assets during market fluctuations.

Multi-Asset Portfolio Management Model: Companies do not limit themselves to a single cryptocurrency but hold multiple coins (e.g., BTC + ETH + SOL + BNB, etc.). Managers need to dynamically adjust the proportions of each asset in response to market changes, resulting in higher management costs and greater demands on asset allocation and risk control capabilities. For example, Mega Matrix Inc. (NYSE: MPU) announced in 2025 that it would expand its DAT strategy from a single asset (such as ENA tokens or ETH) to a multi-asset portfolio, including several leading stablecoins and their governance tokens, attempting to allocate risks and returns across multiple chains or protocols [8].

Ecological Investment Construction Model: This is the most complex model. In addition to holding coins, companies also invest a portion of their funds to support ecological construction, such as on-chain infrastructure, DeFi project investments, node/validator operations, protocol governance, ecological subsidies, and fund investments. This model positions the company as both an asset holder and an ecological participant, potentially influencing the development direction of the ecosystem of the chain it holds. In the Ethereum direction, some DAT companies allocate part of their Ethereum for staking, validator operations, governance voting, or supporting DeFi application development, which itself is an ecological investment behavior, such as the previously mentioned SharpLink. Under this model, DAT companies often receive additional income from staking, investment incubation, transaction fees, etc., in addition to the appreciation of their cryptocurrency assets.

3. Market Pricing Logic of DAT Companies

The valuation fluctuations of DAT companies, unlike traditional enterprises that rely on revenue and profit, depend more on the market performance of their held cryptocurrency assets and their financial leverage strategies. From an investment perspective, the changes in DAT's market capitalization are primarily driven by three core variables: the growth in the number of tokens per share, the price of underlying assets, and the mNAV (Market Value to Net Asset Value) premium/discount. Together, these three form the "valuation triangle" of DAT, determining its attractiveness and risk level in the capital market.

Price increase ≈ Token quantity growth rate × Asset price growth rate × Market premium factor

Here, the market premium factor refers to the market sentiment and valuation premium relative to NAV, which can typically be quantified directly using mNAV, i.e., "market premium factor = mNAV − 1."

3.1 Growth of "Tokens per Share"

It has been previously mentioned how Strategy created the "tokens per share" metric to help assess whether the company has genuinely converted the raised funds into more Bitcoin without severely diluting existing shareholders. Following Strategy's success, many DAT companies have emulated this, with BitMine being a classic example—BitMine also raised funds and reinvested profits to purchase Ethereum, thereby increasing the number of tokens represented by each share.

When the "tokens per share" increases, it indicates that the net asset value (NAV) per share is rising. Theoretically, if the market is efficient, the stock price of DAT companies should rise in sync with NAV. Based on this, if the prices of underlying assets like Bitcoin are also rising, the market typically assigns a higher valuation multiple to DAT, which also causes the DAT stock price to exhibit a "price × tokens per share × market premium" triple leverage effect, leading to increases far exceeding the asset price itself.

3.2 Price Push of Underlying Assets

The most direct driver of DAT company valuations comes from the price fluctuations of underlying assets. When the prices of core tokens like BTC and ETH rise, the company's book asset scale expands, and the market naturally assigns a higher valuation premium; conversely, a price drop directly erodes book value.

However, compared to traditional "asset-driven companies," DAT companies often amplify this price sensitivity. On one hand, most DAT institutions do not set up hedging mechanisms, resulting in asset exposure that closely tracks market prices; on the other hand, financing leverage and convertible bonds amplify the positions held, causing stock prices to become highly elastic to the prices of underlying assets. Therefore, the prices of underlying assets not only affect book value but can also create a positive feedback loop through "refinancing expectations - reserve expansion - valuation enhancement."

3.3 mNAV Flywheel Mechanism

mNAV is the core valuation metric under the DAT model, calculated as follows:

mNAV = P Market Cap / NAV Digital Asset Value

Where P represents the company's market capitalization, NAV represents the net asset value of the company's held cryptocurrency assets valued at market prices, and mNAV refers to the market net asset value ratio.

When the stock price P is higher than the net asset value per share NAV, i.e., mNAV > 1, it indicates that the market assigns a valuation premium to the company that exceeds the market value of its held coins, reflecting investors' recognition of the DAT company's management capabilities, refinancing potential, or strategic value of cryptocurrency assets. The company can continue to raise funds, and each issuance to buy more will push up the per-share holdings and book value, further reinforcing market confidence in the company's narrative and driving the stock price higher. Thus, a closed-loop positive feedback flywheel begins to turn.

However, mNAV is a double-edged sword; a premium can represent high market trust but may also indicate a bubble created by capital speculation. Once confidence collapses and mNAV significantly converges or even drops below 1, the flywheel will shift from a positive cycle to a negative cycle, with the market switching from "the logic of increasing book value" to "the logic of net asset dilution," forming a negative feedback loop of "valuation decline - financing constraints - reserve shrinkage - further market cap decline." If this coincides with a drop in the cryptocurrency's price, it undoubtedly exacerbates the negative flywheel, resulting in a double blow to market cap and confidence. Theoretically, when mNAV is at 1, a more reasonable choice for the company is to sell holdings to repurchase stock to restore balance.

Taking Strategy as an example, during the Bitcoin bull market, MSTR's market cap once reached over twice its book BTC holdings, i.e., mNAV ≈ 2.0. This indicates that investors not only bought "Bitcoin reserves" but also paid a premium for the company's future financing capabilities and capital efficiency. However, during the bear market phase, its mNAV once fell below 1, but the company chose not to sell coins to repurchase; instead, it insisted on retaining all Bitcoin through debt restructuring.

In summary, the financing of DAT companies is built on the mNAV premium flywheel. The mNAV premium is not only a barometer of the heat in the DAT market but also constitutes an important reference for investors to judge buying and selling timing. However, when mNAV remains in a discount state for an extended period, the space for issuance will be blocked, and the businesses of small and mid-cap shell companies that are already stagnating or on the verge of delisting will be completely overturned, causing the established flywheel effect to collapse instantly.

4. Transition of DAT from "Holding" to "Staking"

In contrast to the passive holding strategy of Bitcoin DAT, the Ethereum DAT, which utilizes staking and DeFi infrastructure, may ultimately direct some funds on-chain. This allows DAT companies to not only complete the capital cycle flywheel but also earn additional interest through on-chain staking, enabling the productive use of their held assets.

1. Ethereum Yield-Generating DAT Model

As a blockchain operating system capable of running various DApps, Ethereum's three-layer architecture provides multi-level revenue and risk management space for the DAT model. DAT companies primarily participate at the L1 and DeFi layers (L2 is mainly more active for crypto-native institutions and DAOs): putting the reserved Ethereum on-chain to create "on-chain interest income," transforming coin holdings into productive assets.

Table 1: DAT Strategies Operating on Ethereum's Three-Layer Structure

1.1 Ethereum Staking: From Static Holding to Interest Income

As institutional funds continuously enter the Ethereum ecosystem, DAT companies have evolved from mere token holders to network participants and yield creators. Staking is the primary pathway for DAT companies to enter the Ethereum ecosystem, currently participating in staking mainly through two methods:

Running Validator Nodes Independently: Companies lock their held Ethereum in validator nodes, providing consensus security and transaction verification services for the network. Through the staking reward mechanism, they can earn an annualized block reward yield of about 2.5-3.0%. However, this method has high operational complexity, low liquidity, and risks of node penalties.

Utilizing Liquid Staking Protocols: Companies can delegate their Ethereum to third parties for staking and receive tradable "receipt tokens," such as Lido's stETH. For example, BTCS earns yields through Rocket Pool. Liquid staking resolves the issue of traditional staked assets being locked, allowing companies to maintain asset liquidity while earning staking rewards by issuing tradable tokens (representing staked ETH), enabling DAT companies to generate income without sacrificing operational flexibility.

Assuming the current corporate treasury holds approximately 1 million Ethereum, with 50% staked, and based on the current nominal yield of about 3% and an Ethereum price of $4,000, it can generate approximately $60 million in staking income annually.

1.2 DeFi: Making Ethereum "Move"

Building on the staking of Ethereum, DAT companies can further participate in DeFi protocols, using Ethereum or staking receipts (such as stETH) for DeFi lending or liquidity provision, achieving secondary utilization of funds. Common methods include:

Depositing stETH into DeFi lending protocols like Aave to earn interest;

Using stETH as collateral to borrow stablecoins for reinvestment;

Joining liquidity pools to earn additional transaction fees, etc.

This approach can increase returns from a single staking yield of 3% to 5-10%, injecting institutional-level liquidity into the Ethereum ecosystem.

2. Solana's High Yields Provide New Options for DAT

In 2024, as Solana became the top-ranked ecosystem for new developers, the potential space for Solana DAT companies is also an overlooked new direction, with some institutions even believing it may surpass Ethereum to become the mainstream DAT model. The reasons can be summarized in three aspects:

Higher Yields: Solana's staking yield is around 6-8%, generally higher than Ethereum's approximately 3% yield, making it more attractive for DAT companies seeking passive income or cash flow.

Ecosystem Growth and Infrastructure Promotion: Solana's network activity and developer growth rate have surpassed ETH during certain periods. In the second quarter of 2025, the Solana network processed over 8.9 billion transactions, supporting nearly $3 billion in daily DEX trading volume, generating over $1.1 billion in network revenue, more than 2.5 times that of Ethereum [9]. Additionally, Solana's transaction throughput (TPS), low fees, and fast confirmations make it more appealing for DAT model companies seeking "fast on-chain + high-frequency interaction/low fees."

Rapid Market Recognition: Cantor Fitzgerald has given "overweight" ratings to several Solana DAT companies, citing rapid developer growth and swift ecosystem expansion [10]. Multiple PIPE or private/strategic investments are being made around SOL DAT, for example, in August 2025, Sharps, Pantera, and Galaxy planned to invest $2.65 billion in Solana DAT [11].

Not only holding coins, but Solana DAT companies are also participating in validator operations, infrastructure construction, or ecological subsidies and other on-chain activities. For instance, SOL Strategies (NASDAQ: STKE) started from scratch in the past year to establish its Solana treasury and increase revenue sources through DAT combined with validator income and other infrastructure operations.

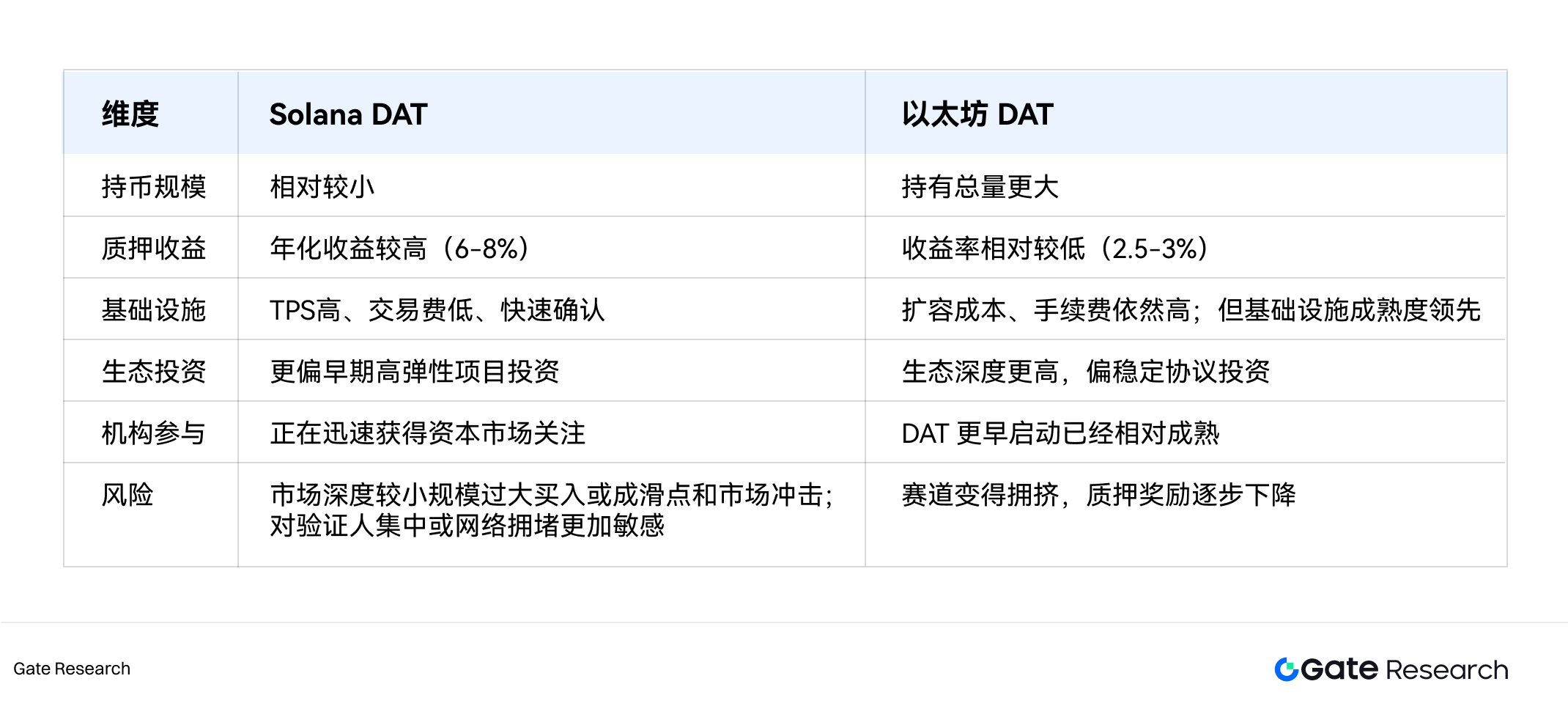

3. Comparison of Advantages Between Ethereum and Solana DAT

In the medium to long term, Solana DAT is expected to continue growing rapidly and may become one of the fastest-growing and strongest upward tracks in the DAT model. However, in terms of absolute scale and institutional maturity, Ethereum still holds a leading advantage, with Ethereum DAT's influence being more mature in terms of quantity, asset scale, and frequent participation in DeFi ecosystems and on-chain activities. If certain key factors continue to optimize, such as the stability of Solana's mainnet, infrastructure security, and clarity of the regulatory environment, Solana DAT could potentially become a main direction alongside Ethereum in the future, especially favored by DAT companies that require high speed and low gas fees.

Table 2: Comparison of Advantages Between Solana DAT and Ethereum DAT

5. Discussion on the Sustainability of the DAT Model

1. Evolution and Risks of DAT Growth Logic

In essence, the core of DAT has never been the profitability of its main business but rather the growth achieved through holding and operating cryptocurrency assets, realizing a cycle of market capitalization and asset amplification. The growth logic of DAT can be divided into three points: First is narrative-driven, where DAT "securitizes" cryptocurrency assets, allowing traditional capital to gain crypto Beta in the stock market, providing valuation premiums through indirect coin holdings. Second is asset appreciation, where the underlying coin price rises, driving balance sheet expansion, increasing mNAV, and ultimately triggering market revaluation. Finally, there is the financing flywheel, where high valuations support the company to issue more shares to buy coins, expanding holdings and boosting market confidence, further elevating valuations. Therefore, during bull markets, DAT rapidly accumulates attention and valuation premiums through "narrative + asset appreciation + financing flywheel," attracting more capital inflow.

However, entering 2025, the market began to reassess the sustainability of the DAT model. Although there is Strategy, which once leaped from a marginal software company to a leading Nasdaq stock, since the stock price peaked at the end of 2024, the myth of the stock price created by Strategy seems to no longer be repeated, and the market began to criticize the DAT strategy as merely a magnifying glass in a bull market, while in a bear market, "tokens per share" would become worthless. At the same time, Michael Saylor's faith in Bitcoin has also come under scrutiny—does refusing to liquidate to maintain tokens per share truly align with shareholder interests? Meanwhile, more and more companies are beginning to replicate Strategy's model, quickly crowding the DAT space, which gradually weakens the "market capitalization amplification effect" originally supported by scarcity and narrative tension. In other words, when DAT is no longer scarce, the marginal effect of its "asset-driven + valuation premium" model is diminishing.

Figure 8: Strategy's Stock Price Fluctuations in 2025

Against this backdrop, the rise of the Ethereum ecosystem has ushered in the second phase of the DAT model—active DAT participating in the on-chain economy. Unlike the passive holding of Bitcoin treasuries, Ethereum DAT can create compound returns through staking, DeFi protocols, and on-chain liquidity operations, forming a second growth curve of "asset monetization." However, this trend has also sparked new controversies: will large-scale staking by institutional treasuries lead to a decline in overall staking returns and an increase in systemic risk? Is DAT's participation promoting ecological prosperity or accelerating bubble formation?

Based on this, the sustainability of the DAT model depends not only on the performance of a single asset but also on its interaction with the blockchain ecosystem, the company's operational quality, financing structure, and investor trust. Below, we will systematically analyze the challenges and evolutionary directions faced by DAT from both "endogenous" and "exogenous" dimensions.

2. Five Forces Model of DAT Sustainability

The endogenous dimension refers to the company itself, specifically whether the company has sufficient fundamentals and financial resilience to "weather" the price cycle fluctuations. The exogenous dimension pertains to the ecosystem and market, meaning whether the participating crypto ecosystem and market environment can provide stable sources of income and liquidity for treasury assets. Based on the previously mentioned market pricing logic of DAT's "tokens per share, underlying asset prices, and mNAV," combined with the new model of on-chain monetization, we have constructed a "Five Forces Model of DAT Sustainability," which will systematically assess the long-term viability of DAT from five dimensions: asset value, asset operation, company fundamentals, regulatory compliance, and investor liquidity.

2.1 Target Asset Value Force

As the foundation of the DAT model, the nature of the target asset determines its long-term value. Currently, there are three main types of DAT models in the market:

Bitcoin Type: Bitcoin, as the earliest and most widely accepted cryptocurrency, holds the status of "digital gold," with its supply cap ensuring scarcity and anti-inflation logic. Additionally, the increasing holdings by global institutions and nation-states enhance its reserve attributes, allowing Bitcoin to serve as a value anchor during macroeconomic cycles. However, risks also exist; Bitcoin's limitation lies in its lack of yield, relying entirely on price appreciation for book value growth. Furthermore, in recent years, Bitcoin has begun to be associated with political maneuvering, gradually evolving from a purely financial asset to a symbol of policy stance and ideology, with its price fluctuations increasingly influenced by election cycles, regulatory attitudes, and party policy expectations.

Ethereum Type: Compared to Bitcoin, Ethereum has a more complete economic internal circulation, with its PoS mechanism providing additional comprehensive yields, making it an asset that can both appreciate and generate income. However, the rise of competing chains may pose a threat to its market share in the future, and the complexity of the protocol may also introduce technical and security risks.

New Public Chain Type: Emerging public chains like Solana, with high performance and a strong developer ecosystem, have become the new "growth-oriented Layer-1" pursued by capital. Additionally, Solana's high staking yields and potential for ecosystem expansion provide DAT with potential high-return opportunities. However, the technological and ecological stickiness of emerging public chain tokens may be less mature, leading to significantly higher volatility compared to Bitcoin and Ethereum; narrative shifts or ecological security events could cause substantial asset value retracement, and long-term risk resistance still needs to be observed.

The long-term sustainability of DAT must focus on the market recognition, utility value, technological maturity, ecological network effects, security, and market capitalization stability of the underlying assets. Overall, Bitcoin represents a strong consensus on value storage logic, but its passive holding characteristics also amplify volatility; Ethereum embodies ecological and yield logic, providing DAT with a "margin of safety," while tokens from emerging public chains like Solana represent high growth and high-risk logic.

2.2 Asset Operation Capability of Holding Coins

The rise of ecosystems like Ethereum and Solana has provided DAT companies with new models for on-chain monetization, meaning that DAT strategies no longer depend on "whether to hold coins," but rather on "how to operate holding assets." Transitioning from passive beneficiaries of the market to active participants in the ecosystem, the stability of asset operations, governance capabilities, and risk management will become key determinants of long-term sustainability.

For companies, compared to Bitcoin DAT's "passive holding," Ethereum and Solana DATs that participate in staking and on-chain financial activities have a certain margin of safety. When coin prices are stable or slightly decline, as long as on-chain yields > cost of capital, the DAT model can self-generate; conversely, it will need to rely on price appreciation to maintain valuation.

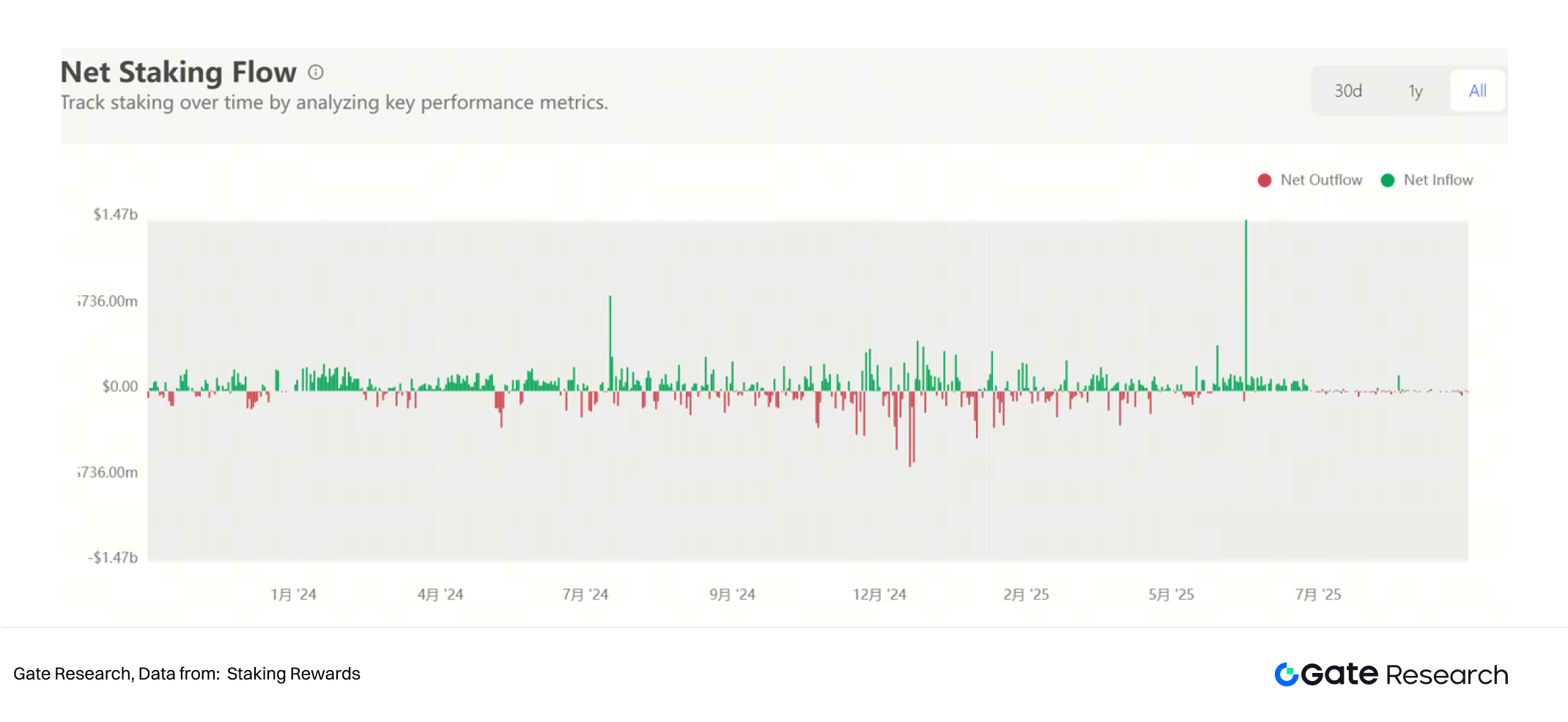

For on-chain ecosystems, DATs like Ethereum and Solana enhance network transaction volume and security, contributing to long-term price stability. The large-scale inflow of institutional funds into the Ethereum ecosystem not only expands the scale of financial activities such as lending and trading but also enhances the liquidity of DeFi protocols, further promoting Ethereum to become the "standard for on-chain collateral assets." Taking Aave v3 as an example, ETH and wrapped stETH form a deep liquidity pool, and the participation of DAT companies can further enhance the depth of this pool, achieving compound interest while improving market liquidity. Additionally, through mechanisms like staking, DeFi, and LP, more Ethereum is locked in staking, reducing market circulation and increasing network decentralization and security, while long-term locked funds also help stabilize prices and reduce speculation.

Figure 9: Ethereum Staking Liquidity Stabilizes Since the Second Half of 2025

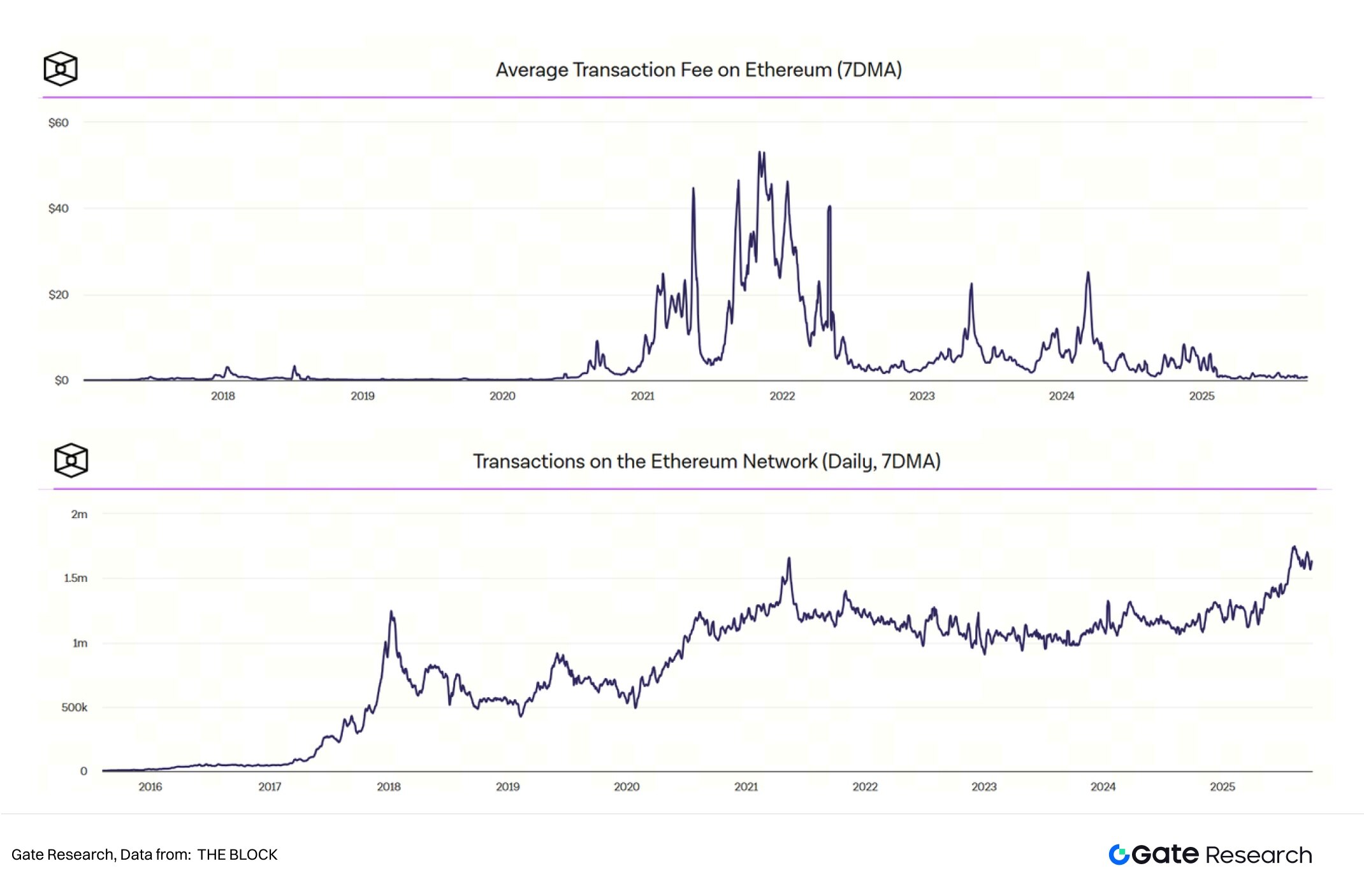

With the popularity of the DAT model, the daily transaction count on the Ethereum mainnet reached a new high in August 2025 (currently slightly falling back to 1.55–1.7 million transactions/day), but thanks to most transactions migrating to L2 and blob expansion, total fees remain at a near three-year low. If corporate treasury capital enters the chain on a large scale, its high-value transactions on the Ethereum mainnet (L1) may drive overall block space demand and fee income, forming a positive cycle of "treasury activity - liquidity enhancement - on-chain usage increase."

Figure 10: ETH Transaction Volume vs. Fees

In summary, the DAT "on-chain" has the following ecological feedback mechanisms:

Increased block space demand → Enhanced validator income → Strengthened network security;

Enhanced fund liquidity → Reduced DeFi protocol risks → Increased user retention;

Increased on-chain transparency → Enhanced trust from institutional investors → More capital inflow.

However, the potential for gains brought by automation coexists with systemic risks. Large-scale institutional staking and leveraged participation may also drive up on-chain yield competition, leading to a decline in staking returns as overall network participation increases. At the same time, DeFi protocols still face potential threats such as smart contract vulnerabilities and liquidation risks. In a bear market, if institutional treasuries withdraw concentrated liquidity, the depth of decentralized exchanges may not be sufficient to support large sell-offs, potentially triggering "on-chain cascading."

Therefore, a sustainable DAT model needs to establish risk diversification and yield balancing mechanisms, such as: reducing exposure to a single cryptocurrency through multi-asset portfolios; implementing tiered staking strategies (partially locking long-term, partially retaining liquidity); or collaborating with CeFi platforms to build a hybrid yield structure of on-chain + off-chain. These measures will be key safeguards for DAT to achieve robust "asset operation capability" in the on-chain ecosystem.

2.3 Company Fundamental Support

The sustainability of DAT also depends on whether it has a healthy operational foundation, which determines the company's ability to "self-generate survival" during downturns in the crypto market and the long-term establishment of investor confidence. We categorize them into strong support and weak support DAT types:

Strong support DAT, such as Strategy, has stable software business cash flow, maintaining debt repayment capability even during crypto bear markets. Similarly, if SOL ecosystem DAT relies on staking yields as a long-term cash flow source, it can also partially hedge against asset price volatility risks.

Weak support DAT refers to pure shell companies or SPAC structures, where the absence of core business and insufficient cash flow can easily lead to a cycle of "maintaining through debt issuance." Once the market cools or financing is interrupted, such companies often become high-risk targets for failure.

When analyzing company fundamentals, it is essential to carefully assess the following points: First, does the company have non-crypto-related cash flow sources? Second, can it cover financing interest and operating expenses? Third, is the financial structure robust (leverage ratio, cash position)? If DAT lacks fundamental support and relies solely on asset price appreciation or capital narratives, a fragile "shell" will struggle to withstand market volatility, facing liquidation risks even in bear markets.

2.4 Regulatory and Compliance Strength

As DATs are publicly traded companies, they face strict regulations regarding investor protection and transparency, similar to other listed companies. The evolution of the regulatory framework is gradually becoming a key variable for the sustainability of the DAT model.

With the increasing recognition of compliance for crypto assets in recent years, some jurisdictions have begun to acknowledge the legality of holding crypto assets, providing DATs with a more stable disclosure and auditing environment. Starting in 2024, updates to FASB accounting standards changed the strategic significance for DAT companies—allowing businesses to measure crypto assets at fair value, directly enhancing financial report transparency and asset valuation space. Before this change, companies like Strategy classified their held cryptocurrencies as intangible assets, meaning that a drop in Bitcoin prices would permanently reduce the value of their holdings, with gains only recognized upon token sale (though Michael Saylor vowed never to do so). This change means that DAT companies using GAAP can recognize unrealized changes in the value of their crypto holdings. However, the change in accounting standards is a double-edged sword, as significant price fluctuations in cryptocurrencies could lead to substantial increases in quarterly earnings, but also potentially result in massive losses.

Some market analysts believe that the formation of future DAT companies may no longer occur through SPACs but rather through mergers with legitimate businesses, although the "de-SPAC" process may be chaotic, requiring shareholder votes, regulatory filings, and various efforts [12]. As more DATs continue to enter the market, consolidation has already begun. In September 2025, Strive (NASDAQ: ASST) announced an all-stock acquisition of Semler Scientific (NASDAQ: SMLR), marking the first merger of two publicly traded Bitcoin treasury companies. After the merger, the new entity will integrate both parties' Bitcoin assets, increasing "tokens per share" and enhancing financing capabilities in the capital markets. This transaction is seen as a landmark event signaling the entry of the DAT field into a "consolidation phase," indicating that DAT may be entering the next stage of development [13].

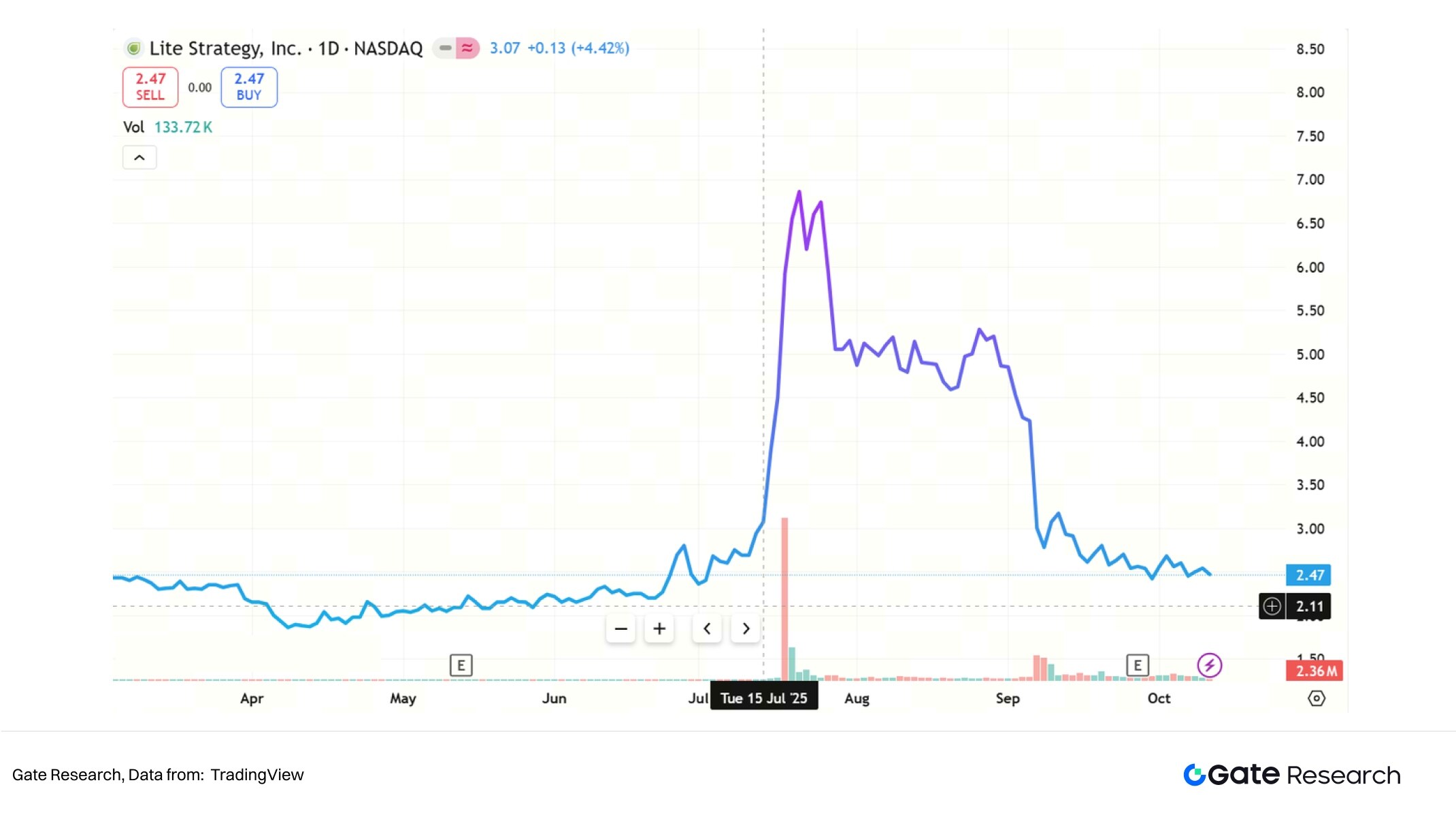

However, announcing a strategic reserve of crypto assets does not mean obtaining the key to unlock wealth. Nasdaq or NYSE has high requirements for market capitalization and information disclosure; if shell-type DATs fail to meet the standards, they may ultimately be forced to delist. For example, the stock price of BNB treasury company Windtree Therapeutics fell by more than 90% within a month, no longer meeting Nasdaq's minimum price of $1.00 per share and facing delisting [14]. Additionally, there are ongoing doubts regarding asset bubbles and insider trading related to DAT companies. On September 24, 2025, the SEC and the Financial Industry Regulatory Authority (Finra) jointly announced that they would investigate over 200 publicly traded companies that had announced crypto treasury plans, citing "abnormal stock price fluctuations" occurring just before the release of related news [15]. Similarly, the potential existence of insider trading has led to a collapse of trust among some investors in DAT. For instance, MEI Pharma (later renamed Lite Strategy Inc.) announced on July 18, 2025, the launch of a $100 million Litecoin treasury strategy, but its stock price had already experienced abnormal increases around July 16, just before the announcement.

Figure 11: Abnormal Stock Price Fluctuations of Lite Strategy

Despite over 200 companies announcing crypto treasury strategies in 2025, covering multiple chains like BTC, ETH, SOL, BNB, and TRX, capital and valuations are rapidly concentrating towards a few companies and assets, with a head effect accelerating formation. We believe that while Bitcoin DAT and Ethereum DAT occupy a significant portion of DAT companies, ultimately, only one or two companies in each asset category may truly emerge, while the remaining projects may struggle to form competitive scale.

2.5 Investor and Liquidity Strength

The valuation level of DAT ultimately depends on market liquidity and investor structure. From the current investor structure, although some larger DAT companies attract institutional buyers by including their stocks in tracking funds, most DAT buyers are retail investors. For retail investors, buying DAT stocks allows them to indirectly participate in the crypto market while avoiding the risks of direct coin holding, but this may also be one of the factors leading to greater trading volatility.

Strategic capital, such as crypto funds and family offices, also has a demand for leveraging returns through DAT to allocate Web3 assets, but the proportion of these institutional investors varies significantly among different DAT companies. Specifically, large-cap, liquid companies are more likely to be allocated by public funds, pension funds, and quantitative funds, with leading Bitcoin DAT Strategy being representative, having a relatively high proportion of institutional holdings. As of October 8, 2025, institutional investors accounted for 58.84% [16]. Before Ethereum and other public chain ETFs are fully opened, institutional investors often view DAT as a compliant exposure to crypto assets, but relatively, the institutional proportion in some Ethereum DAT and small-cap DAT remains generally low; for example, Sharplink's institutional investor proportion is 13.75%, while BTCS's is only 3.48%.

From a liquidity structure perspective, the liquidity of DAT does not solely depend on the scale of its on-chain asset holdings but rather on the differences in investor structure. Institutionally dominated DATs typically possess stronger capital stability and trading depth, with their institutional investors often aiming for long-term allocation or asset substitution, showing lower sensitivity to short-term market fluctuations, thus being able to buffer the concentrated release of asset sell pressure to some extent. During market volatility, these DAT companies are more likely to manage risks through over-the-counter trading or hedging, thereby maintaining a more stable market capitalization performance during periods of volatility.

In contrast, retail-dominated DAT companies have more dispersed float shares, but trading sentiment fluctuates dramatically. When market expectations shift or token prices decline, synchronized emotional sell-offs are likely to occur. Therefore, once these retail-dominated DATs collectively reduce their positions, their on-chain holdings may be rapidly magnified through decentralized exchanges with insufficient liquidity, leading to "stair-step" price declines. Especially in assets like Ethereum, which have relatively layered liquidity, the on-chain release of large treasury holdings often triggers nonlinear price reactions— even if the sell-off scale accounts for only a tiny proportion of the token's circulation, it may trigger severe volatility due to insufficient market absorption capacity.

Overall, the future financing sustainability of DAT depends on its ability to attract institutional, long-term investors (such as ETFs, family offices, and sovereign funds) to reduce financing sensitivity under market volatility. We believe that as the compliance and regulatory mechanisms for crypto assets and DAT improve, the liquidity structure of institutional funds entering DAT is expected to shift from being driven by sentiment to being driven by asset allocation, leading to a convergence in market volatility.

VI. Conclusion

The DAT model, as a new trend combining crypto and traditional finance, essentially represents a "mapping mechanism between capital markets and on-chain assets." During bull market cycles, the rise in underlying asset prices, smooth financing, and increased investor risk appetite make DAT a typical amplifier of both valuation and sentiment. However, historical experience shows that this model is highly susceptible to dual pressures of financing interruption and asset depreciation in bear market environments, potentially turning the flywheel from positive feedback to negative cycles.

The sustainability of DAT ultimately depends on five key pillars: 1. Whether the chosen crypto asset targets of DAT companies possess long-term value and sustainable income capabilities; 2. Whether DAT is passively held or can actively operate assets to generate cash flow; 3. Whether the quality of DAT companies includes core business and stable cash flow to buffer against asset volatility; 4. Policy changes regarding compliance disclosure, accounting standards, and fair value measurement will determine whether DAT can be accepted by mainstream capital in the long term; 5. The concentration and specialization of the investor structure in DAT companies must withstand significant liquidity fluctuations.

Despite over 200 companies announcing crypto treasury strategies in 2025, covering multiple chains such as BTC, ETH, SOL, BNB, and TRX, capital and valuations are rapidly concentrating towards a few companies and assets, with a head effect accelerating formation. Looking ahead, the winners in DAT will not be numerous speculative "shell companies," but those that can establish a solid flywheel at both ends of ecological construction and capital markets. They will not only effectively allocate capital and generate on-chain returns but also earn the trust of institutional investors through transparent governance and robust finances. Similarly, in each mainstream asset track, there may ultimately be only one or two winners.

DAT is still in the early stages of financial innovation, and its path is destined to be accompanied by high volatility and uncertainty. However, from a longer-term perspective, the value of DAT lies not in short-term price leverage but in its ability to become a stable bridge connecting the crypto economy and traditional capital markets.

References

•[1] YouTube, https://www.youtube.com/watch?v=b0KU4cJgj6g

•[2] Cointelegraph, https://cointelegraph.com/news/worlds-biggest-business-intelligence-firm-buys-21k-btc-for-250m

•[3] Bloomberg, https://www.bloomberg.com/news/articles/2020-12-07/microstrategy-to-raise-400-million-to-buy-even-more-bitcoin

•[4] Bitcointreasuries.net, https://bitcointreasuries.net/

•[6] Coingecko, https://www.coingecko.com/zh/treasuries/%E4%BB%A5%E5%A4%AA%E5%9D%8A/companies

•[7] CoinDesk, https://www.coindesk.com/business/2025/07/08/crypto-treasury-firm-reserveone-going-public-in-1b-spac-deal

•[8] NASDAQ, https://www.nasdaq.com/press-release/mega-matrix-announces-diversify-dat-strategy-basket-leading-stablecoins-and

•[10] Yellow, https://yellow.com/news/cantor-fitzgerald-sees-dollar250-million-potential-in-solana-treasury-companies

•[11] Coinrank, https://www.coinrank.io/crypto/2-65-billion-solana-dat-plan/

•[12] CoinDesk, https://www.coindesk.com/markets/2025/09/28/from-spacs-to-cash-flow-buys-how-dats-are-plotting-the-next-growth-phase

•[13] Yahoo!Finance, https://finance.yahoo.com/news/strive-semler-scientific-merge-stock-145427057.html

•[14] The Block, https://www.theblock.co/post/367721/nasdaq-to-delist-bnb-token-treasury-company-windtree-therapeutics-for-noncompliance

•[15] Cryptopolitan, https://www.cryptopolitan.com/sec-finra-probe-crypto-treasury-stock-spikes/

•[16] MarketBeat, https://www.marketbeat.com/stocks/NASDAQ/MSTR/institutional-ownership/

Gate Research Institute is a comprehensive blockchain and cryptocurrency research platform that provides readers with in-depth content, including technical analysis, hot insights, market reviews, industry research, trend forecasts, and macroeconomic policy analysis.

Disclaimer

Investing in the cryptocurrency market involves high risks. Users are advised to conduct independent research and fully understand the nature of the assets and products they are purchasing before making any investment decisions. Gate is not responsible for any losses or damages resulting from such investment decisions.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。