Written by: arndxt

Translated by: AididiaoJP, Foresight News

Liquidity expansion remains the dominant macro narrative.

Recession signals are lagging, and structural inflation is sticky.

Policy rates are above neutral levels but below tightening thresholds.

The market is pricing in a soft landing, but the real adjustment is at the institutional level: from cheap liquidity to restrained productivity.

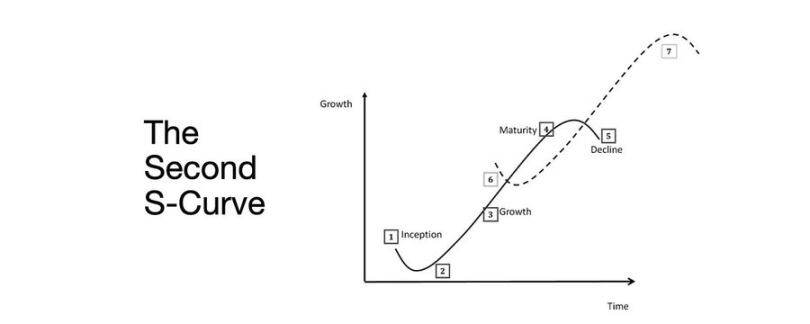

The second curve is not cyclical.

It normalizes the structure of finance under real constraints through yields, labor, and credibility.

Cycle Transition

The Token2049 Singapore conference marks a turning point from speculative expansion to structural integration.

The market is repricing risk, shifting from narrative-driven liquidity to income-supported yield data.

Key shifts:

- Perpetual decentralized exchanges maintain dominance, with Hyperliquid ensuring liquidity at network scale.

- Prediction markets are emerging as functional derivatives of information flow.

- AI-related protocols with real Web2 application scenarios are quietly expanding revenue.

- Re-staking and DAT have peaked; liquidity decentralization is evident.

Macro Institutions: Currency Depreciation, Demographics, Liquidity

Asset inflation reflects currency depreciation rather than organic growth.

When liquidity expands, duration assets outperform the broader market.

When liquidity contracts, leverage and valuations are compressed.

Three structural drivers:

- Currency depreciation: Repaying sovereign debt requires continuous balance sheet expansion.

- Demographics: An aging population reduces productivity, reinforcing dependence on liquidity.

- Liquidity pipeline: Global total liquidity, the sum of central bank and banking system reserves, has tracked 90% of risk asset performance since 2009.

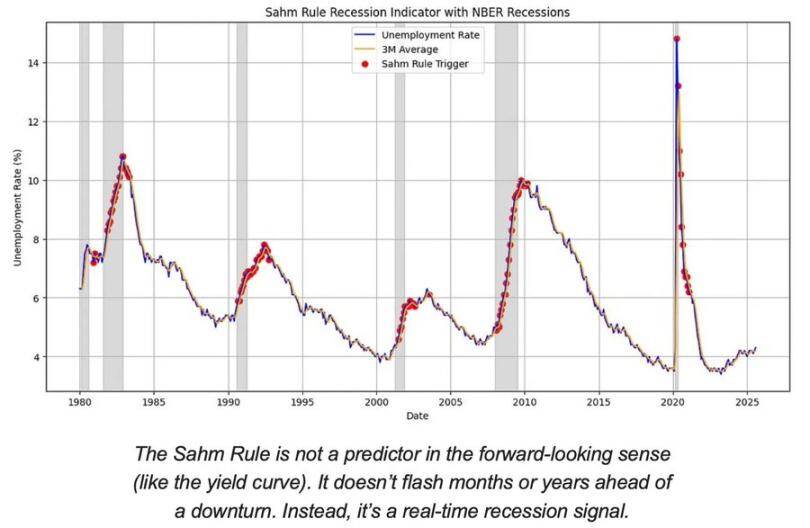

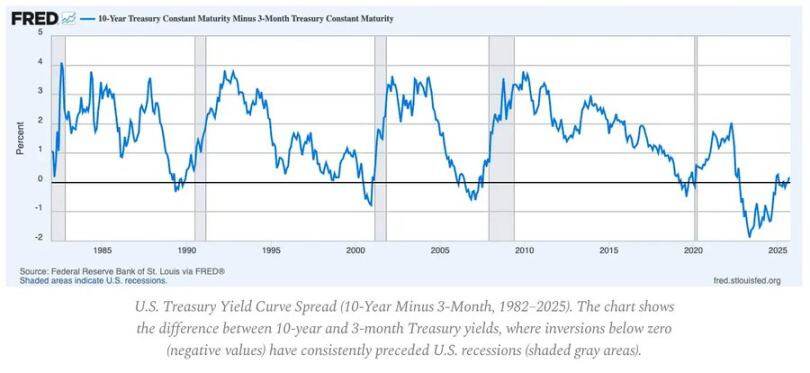

Recession Risks: Lagging Data, Leading Signals

Mainstream recession indicators are lagging.

CPI, unemployment rates, and the Sam Rule confirm only after an economic downturn begins.

The U.S. is in the late stage of the economic cycle, not in a recession.

The likelihood of a soft landing remains higher than the risk of a hard landing, but policy timing is a limiting factor.

Leading indicators:

- An inverted yield curve remains the clearest leading signal.

- Credit spreads are under control, indicating no imminent systemic pressure.

- The labor market is gradually cooling; employment remains tight within the cycle.

Inflation Dynamics: The Last Mile Problem

Commodity disinflation has completed; service inflation and wage stickiness now anchor overall CPI around 3%.

This "last mile" is the most complex phase of disinflation since the 1980s.

- Commodity deflation now offsets part of the CPI impact.

- Wage growth near 4% keeps service inflation elevated.

- Housing inflation is measured with a lag; real market rents have cooled.

Policy Implications:

- The Federal Reserve faces a trade-off between credibility and growth.

- Premature rate cuts risk a renewed acceleration; maintaining rates too long risks excessive tightening.

- The balanced outcome is a new inflation floor close to 3%, rather than 2%.

Macro Structure

Three long-term inflation anchors remain:

- De-globalization: Diversification of supply chains increases transformation costs.

- Energy transition: Capital-intensive low-carbon activities raise short-term input costs.

- Demographics: Structural labor shortages create persistent wage rigidity.

These limit the Federal Reserve's ability to normalize without higher nominal growth or higher equilibrium inflation.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。