Author: arndxt

Translation: AididiaoJP, Foresight News

The view that the economy is re-accelerating is actually quite one-sided, currently relying mainly on the assets of wealthy families and investments driven by artificial intelligence. For investors, this cycle cannot simply expect a broad market rally:

- The core of long-term growth is semiconductor and AI infrastructure.

- Increase holdings in scarce physical assets: gold, metals, and certain promising real estate markets.

- Remain cautious about broad market indices: the high proportion of the "seven giants" in U.S. stocks masks the overall fragility of the market.

- Closely monitor the dollar's movements: its direction will determine whether this cycle continues or is interrupted.

Just like from 1998 to 2000, the bull market may continue for a while, but volatility will become more intense, and asset selection will be key to becoming a market winner.

Economic Divergence

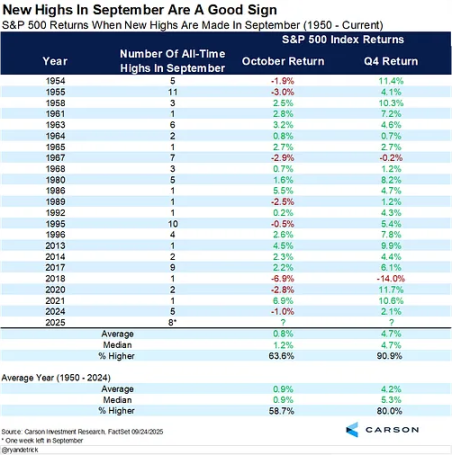

Market performance is a true reflection of the economy; as long as the stock market remains near historical highs, the notion of economic recession is hard to believe.

We are in a clearly divergent economic environment:

- The top 10% of income earners contribute over 60% of consumption, accumulating wealth through stocks and real estate.

- Meanwhile, inflation continues to erode the purchasing power of middle- and low-income families. This widening gap explains why, on one hand, the economy is "re-accelerating," while on the other hand, the job market remains weak, and the cost of living crisis persists.

Uncertainty from Federal Reserve Policies

Be prepared to face policy fluctuations. The Federal Reserve must address inflationary appearances while considering the political cycle. This creates conditions for seizing opportunities but also means that once market expectations change, there may suddenly be a risk of decline.

The Federal Reserve is currently in a dilemma:

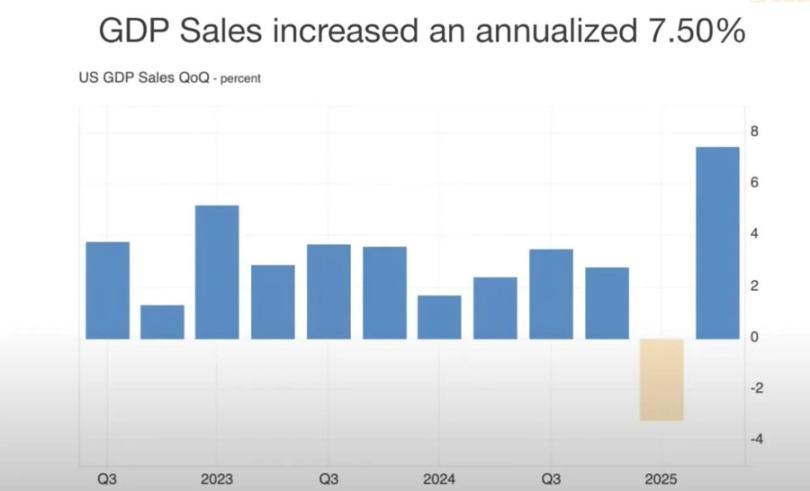

- On one hand, strong GDP growth and resilient consumption support a slower pace of interest rate cuts;

- On the other hand, high market valuations may trigger "growth concerns" if rate cuts are delayed.

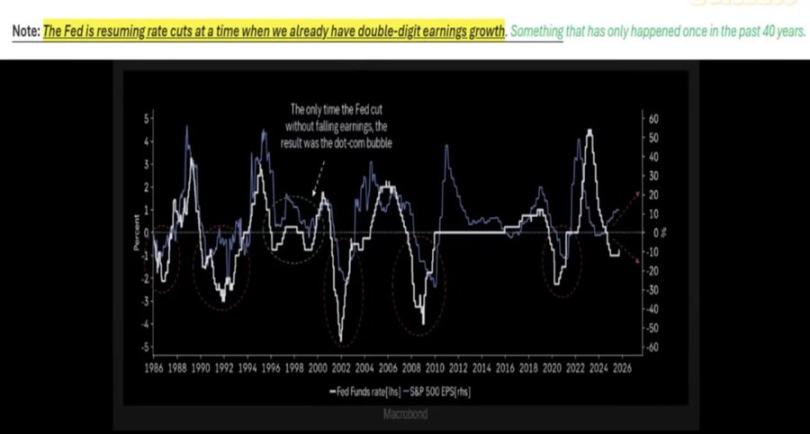

Historical experience shows that cutting rates during strong earnings (like in 1998) can extend a bull market. But this time is different: inflation remains stubborn, the "seven giants" of U.S. stocks are performing well, while the other 493 companies in the S&P 500 are underperforming.

Asset Selection in a Nominal Growth Environment

One should hold scarce physical assets (gold, key commodities, real estate in supply-constrained areas) and sectors that represent productivity (AI infrastructure, semiconductors), while avoiding excessive concentration in stocks driven up by internet hype.

The upcoming period is unlikely to see widespread prosperity; it will be more like a localized bull market:

- Semiconductors remain the core of AI infrastructure, with related investments continuing to drive growth.

- Gold and physical assets are re-emerging as valuable hedges against currency devaluation.

- Cryptocurrencies currently face pressures from deleveraging and an excess of government bonds, but structurally, they are closely related to the liquidity cycle that drives up gold.

Real Estate and Consumption Dynamics

If real estate weakens in sync with the stock market, the "wealth effect" supporting consumption will be impacted.

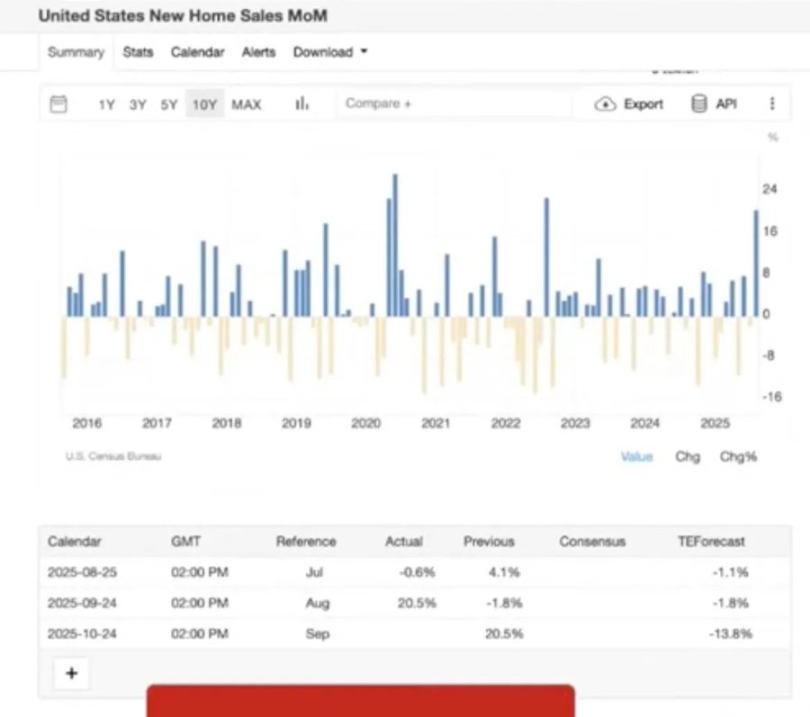

Real estate may see a brief rebound with slight interest rate cuts, but deeper issues remain:

- Supply-demand imbalances caused by demographic changes;

- Rising default rates due to the end of student loan and mortgage forbearance periods;

- Significant regional disparities (older populations have asset buffers, while young families face heavy pressures).

Dollar Liquidity and Global Layout

The dollar is a key factor influencing the overall situation. If the global economy is weak while the dollar strengthens, weaker markets may face problems before the U.S.

One overlooked risk is the contraction of dollar supply:

- Tariff policies reduce trade deficits, limiting the scale of dollar inflows into U.S. assets;

- The fiscal deficit remains high, but foreign buyers' interest in U.S. government bonds is waning, which may trigger liquidity issues.

- Futures market data shows that dollar short positions have reached historical extremes, which could lead to a dollar short squeeze, thereby destabilizing risk assets.

Political Economy and Market Psychology

We are in the late stage of a financialization cycle:

- Policymakers strive to "maintain the status quo" until important political milestones (such as elections, midterm elections) pass;

- Structural inequality (rising rents outpacing wages, wealth concentrating among the elderly) fuels populist pressures, prompting policy adjustments in areas like education and housing;

- The market itself has reflexivity: capital is highly concentrated in seven large-cap stocks, which supports valuations but also sows the seeds of fragility.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。