Author: Ignas

Translation: Baihua Blockchain

I really like Ray Dalio's model of "The Changing World Order" because it forces you to step out of a local perspective and see the bigger picture.

You won't get caught up in the daily drama of cryptocurrency X, but rather examine long-term changes. This is also how we should observe cryptocurrencies.

This is not just about the rapid shifts in narratives, but about a complete transformation of the entire industry order.

Cryptocurrency is no longer the market it was in 2017 or 2021.

Here are the ways I believe the order is changing.

01 The Great Rotation

The launch of Bitcoin spot and ETFs is a significant turning point.

Just this month, the SEC approved a universal listing standard for commodity ETPs. This means a faster approval process and more assets entering the market. Grayscale has already applied for related products under this new regulation.

Bitcoin ETFs have set the record for the most successful issuance in history. Ethereum ETFs started slowly, but even in a weak market, they now hold billions of dollars in assets.

Since April 8, spot cryptocurrency ETFs have led all ETF categories with $34 billion in inflows, surpassing thematic investments, government bonds, and even precious metals.

Buyers include pension funds, investment advisors, and banks. Cryptocurrencies now appear in the same portfolio configurations as gold or the Nasdaq.

Bitcoin ETFs hold $150 billion in managed assets, accounting for over 6% of the total supply.

Ethereum ETFs hold 5.59% of the total supply.

All of this has happened in just over a year.

ETFs are now the main buyers of Bitcoin and Ethereum. They are shifting the ownership base from retail to institutional. As I show in my post below, whales are buying while retail investors are selling.

More importantly, old whales are selling to new whales.

Ownership is rotating. Believers in the four-year cycle are selling off. They expect the same script to play out again. But different things are happening.

Retail traders who bought at low prices are selling to ETFs and institutions. This transfer resets the cost basis to a higher level. It also raises the bottom for future cycles, as new holders will not sell at small profits.

This is the great rotation in cryptocurrency. Cryptocurrencies are shifting from speculative retail hands to long-term allocators.

The universal listing standard has opened the next phase of this rotation.

Similar rules in the stock market in 2019 doubled the issuance of ETFs. It is expected that cryptocurrency will follow suit. Many new ETFs targeting SOL, HYPE, XRP, DOGE, and others are set to launch, providing retail investors with the exit liquidity they need.

The big question remains: can institutional buying offset retail selling?

If the macro environment remains stable, I believe those who are selling now in anticipation of the four-year cycle will buy back at higher prices.

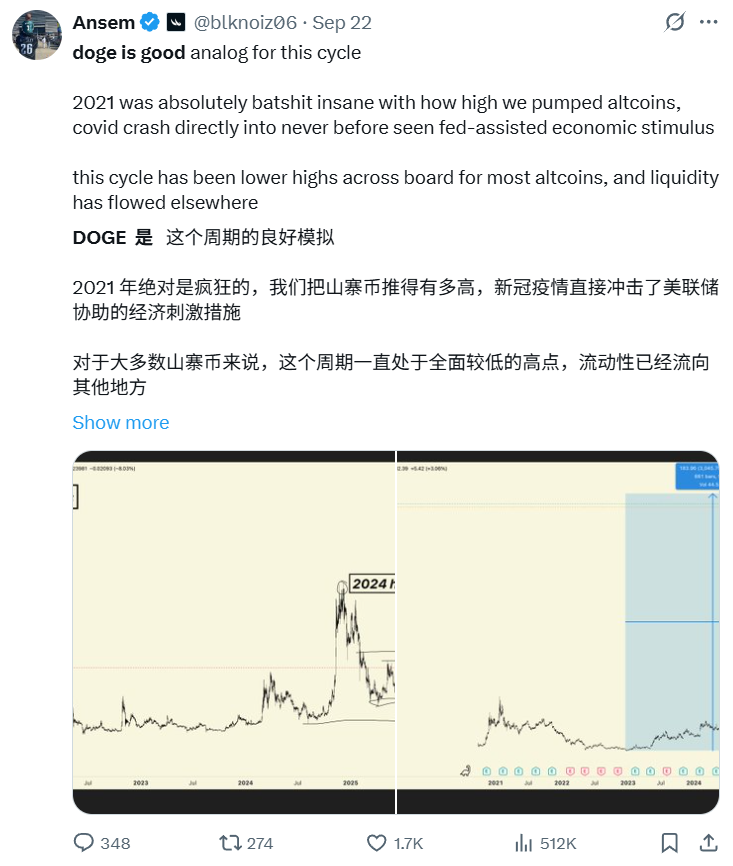

02 The End of Broad Market Surges

In the past, cryptocurrencies would surge together. Bitcoin would move first, followed by ETH, and then all other coins would follow. Small-cap coins would skyrocket as liquidity flowed down the risk curve.

This time is different; not all tokens are surging together.

Now there are millions of tokens. New coins are issued daily on pump.fun, as "creators" shift attention from old tokens to their own MeMe coins. The supply has exploded, while retail attention remains unchanged.

Liquidity is dispersed across too many assets, as issuing new tokens requires almost no cost.

Tokens with low circulation and high fully diluted valuations were once popular, benefiting from airdrops. Now retail investors have learned their lesson. They want tokens that can deliver value or at least have strong cultural appeal (a good example is $UNI, which despite strong trading volume, failed to surge).

Ansem is right; we have reached the peak of pure speculation. The new meta-narrative is revenue because it is sustainable. Applications with product-market fit and fees will surge. The rest will not.

Two things stand out: users are paying high fees for speculation, and the efficiency of blockchain rails compared to traditional finance. The former has peaked, while the latter still has room for growth.

Murad added another good point that I think Ansem missed. Tokens that are still popular tend to be new, strange, and misunderstood, but supported by communities with strong beliefs. I am the type who likes shiny new things (like my iPhone Air).

Cultural significance determines the difference between survival and failure. A clear mission, even if it seems delusional at first, can keep a community alive until adoption snowballs. I would categorize fat penguins, punk NFTs, and MeMe coins in this category.

However, not every shiny new thing will succeed. Runes, ERC404, and others have taught me how quickly novelty can fade. Narratives can emerge and then disappear before reaching critical mass.

I believe these points collectively explain the new order. Revenue filters out weak projects. Cultural carriers support misunderstood projects.

Both are important, but in different ways. The biggest winners will be the few tokens that can combine both.

03 Stablecoin Order Gives Credibility to Cryptocurrency

Initially, traders held USDT or USDC to buy BTC and altcoins. New inflows were bullish as they converted into spot buying. At that time, 80% to 100% of stablecoin inflows ultimately went to purchase cryptocurrencies.

Now that situation has changed.

Stablecoins are entering for lending, payments, yield, treasury, and airdrop mining. Some of this capital never touches BTC or ETH spot buying. But it still enhances the entire system. There are more transactions on L1 and L2. More DEX liquidity. Lending markets like Fluid and Aave generate more income. The funding markets of the entire ecosystem are deeper.

A new development is payment-priority L1s.

Stripe and Paradigm's Tempo is built for high-throughput stablecoin payments, with EVM tools and native stablecoin AMM.

Plasma is a Tether-supported L1 designed for USDT, providing new banking and card services for emerging markets.

These chains are pushing stablecoins into the real economy, not just trading. We return to the meta-narrative of "blockchain for payments."

What could this mean (to be honest, I'm still not sure)?

Tempo: Stripe's distribution capability is immense. This helps with broader adoption of cryptocurrency but may bypass spot demand for BTC or ETH. Tempo could ultimately be like PayPal: huge traffic but little value accumulation for Ethereum or other chains. The open question is whether Tempo will have a token (I think it will) and how much fee revenue will flow back to cryptocurrency.

Plasma: Tether already dominates issuance. By connecting chains + issuers + applications, Plasma could pull a significant portion of emerging market payments into a closed garden. This is like the closed Apple ecosystem compared to the open internet driven by Ethereum and Solana.

This raises competition with Solana, Tron, and EVM L2s to become the default USDT chain. I think Tron is the most likely to fail here, while Ethereum was not originally designed for payments. But the launch of Aave and others on Plasma poses a big risk for ETH…

Base: The savior of ETH L2. As Coinbase and Base drive payments through the Base application and generate yield through USDC, they will continue to bring fees to Ethereum and DeFi protocols. The ecosystem remains fragmented but competitive, which broadens liquidity distribution.

Regulation is keeping pace with this shift. The GENIUS Act is now pushing other countries to catch up in the global stablecoin game.

The CFTC has just allowed the use of stablecoins as tokenized collateral in derivatives. This adds non-spot demand from capital markets beyond payment needs.

Overall, stablecoins and new stable L1s give cryptocurrency credibility.

What was once just a gambling venue now has geopolitical significance. Speculation is still primary, but stablecoins are clearly the second-largest use case in cryptocurrency.

The winners will be the chains and applications that can capture stablecoin flows and convert them into sticky users and cash flow. The biggest unknown is whether new L1s like Tempo and Plasma will become leaders in locking value within their ecosystems or whether Ethereum, Solana, L2s, and Tron can push back.

04 DAT: New Leverage and IPOs for Non-ETF Tokens

Digital Asset Treasuries worry me.

In every bull market cycle, we find new ways to leverage tokens. This pushes prices to levels that cannot be reached by spot buying alone, but liquidations are always brutal. When FTX collapsed, forced selling from CeFi leverage destroyed the market.

The leverage risk in this cycle may come from DAT. If they issue stocks at a premium, raise debt, and invest funds into tokens, they will amplify the upside potential. But when sentiment shifts, the same structure could also amplify the downside.

Forced redemptions or stock buybacks could trigger heavy selling pressure. Therefore, while DAT expands access and brings in institutional capital, they also introduce new layers of systemic risk.

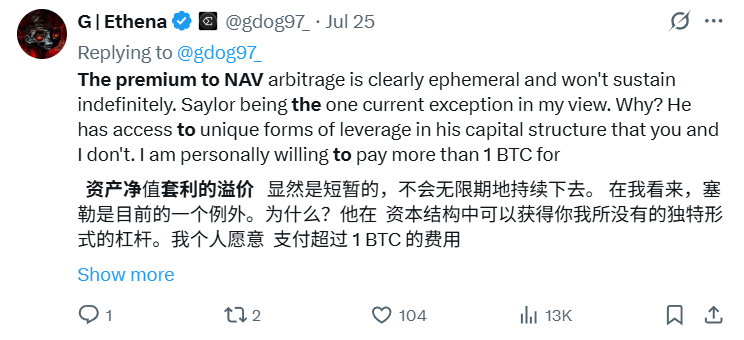

We have an example of what happens when mNAV > 1. In short, they give shareholders ETH, and shareholders are likely to sell. However, despite the "airdrop," the trading price of BTCS remains at 0.74 mNAV. Not great.

On the other hand, DAT is a new bridge between token economics and the stock market.

As Ethena founder G wrote:

This is the context for the importance of DAT.

Retail capital may have peaked, but tokens with real businesses, real revenue, and real users can enter the larger stock market. Compared to global stocks, the entire altcoin market is just a rounding error. DAT opens a door for new capital inflows.

Moreover, since few altcoins have the expertise required to launch DAT, those that do will refocus attention from millions of tokens to a few Sheldon's point assets.

His other point, that NAV premium arbitrage is not important… is bullish.

Aside from Saylor, who can use leverage in the capital structure, most DATs will not maintain a sustained premium relative to NAV. The real value lies not in the premium game but in access. Even a stable one-to-one NAV with continuous inflows is better than having no access at all.

DATs like ENA and even SOL are hated because they are "cash-out tools" for VC tokens.

ENA is particularly vulnerable to attacks due to the large VC holdings. However, the capital mismatch issue, where private VC funds far exceed the liquidity secondary demand, makes exiting to DAT bullish, as VCs can then allocate capital to fund other crypto assets.

This is important because VCs have been severely impacted in this cycle and are unable to exit their investments. If they can sell and gain new liquidity, they can ultimately fund new innovations in cryptocurrency and drive the industry forward.

Overall, DAT is bullish for cryptocurrency, especially for tokens that cannot access ETFs. They allow projects like Aave, Fluid, and Hype, which have real users and revenue, to transfer risk exposure to the stock market.

Of course, many DATs will fail and have spillover effects on the market. But they also bring IPOs to ICOs.

05 The RWA Revolution Means We Can Have Financial Lives On-Chain

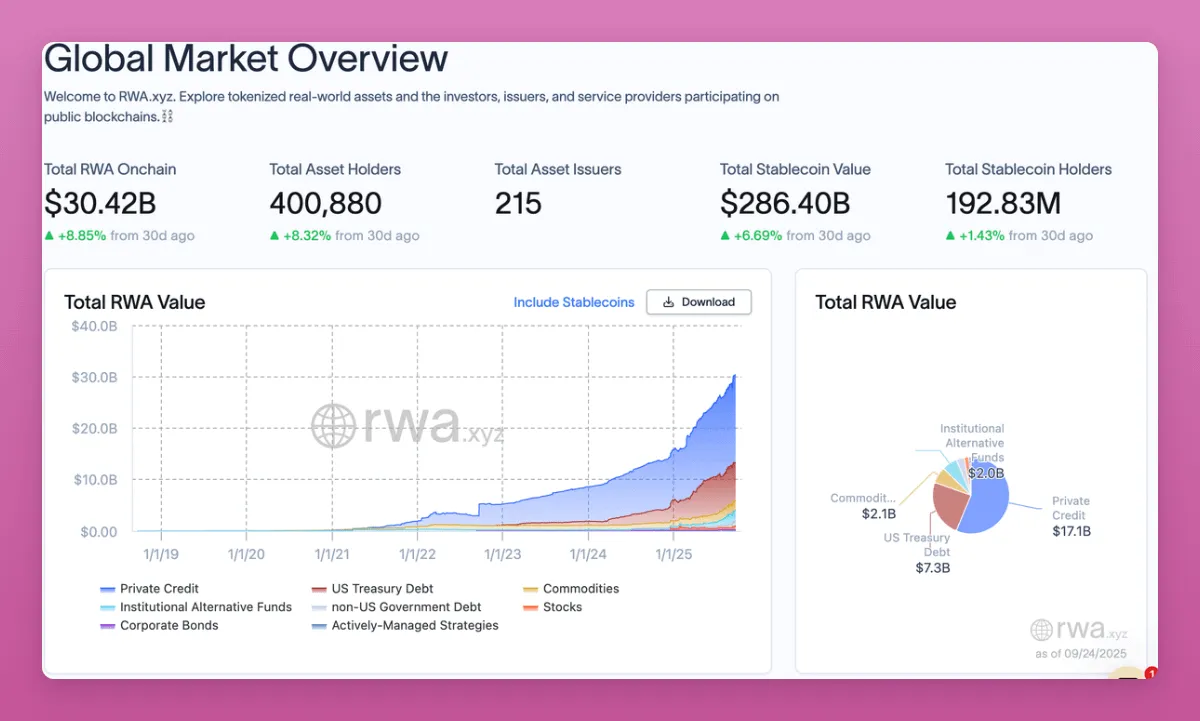

The total market for on-chain RWAs has just surpassed $30 billion, rising nearly 9% in just one month. The chart is only going up.

Government bonds, credit, commodities, and private equity are now all tokenized. The escape velocity is rapidly curving upwards.

RWAs are bringing the world economy on-chain. Some significant shifts are:

Previously, you had to sell cryptocurrency into fiat to buy stocks or bonds. Now you can stay on-chain, hold BTC or stablecoins, transfer into government bonds or stocks, and maintain self-custody.

DeFi has moved away from "circular Ponzi" games, which were the growth engines for many protocols. It brings new revenue streams to DeFi and L1/L2 infrastructure.

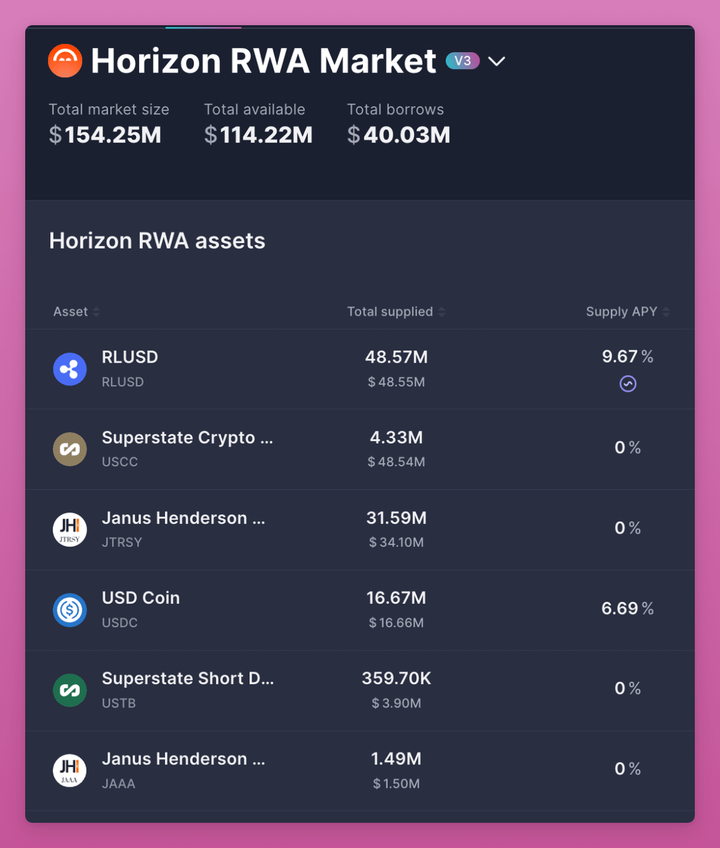

A significant shift is collateral.

Aave's Horizon allows you to deposit tokenized assets like the S&P 500 and borrow against them. However, the TVL is still small, at only $114 million, indicating that RWAs are still relatively early. (Note: Centrifuge is working to bring the official SPX500 RWA on-chain. If successful, CFG may perform well. I hold a position).

Traditional finance makes this nearly impossible for retail investors.

RWAs ultimately make DeFi a true capital market. They set benchmark interest rates with government bonds and credit. They expand global coverage, allowing anyone to hold U.S. Treasuries without needing a U.S. bank (which is becoming a global battleground).

BlackRock has launched BUIDL, and Franklin has introduced BENJI. These are not fringe projects. They are bridges for trillions of dollars to enter the crypto space.

Overall, RWAs represent the most important structural revolution happening now. They connect DeFi with the real economy and build the rails for a world that can remain entirely on-chain.

06 The Four-Year Cycle

The most important question for crypto natives is whether the four-year cycle has disappeared. I hear people around me are already selling, expecting it to repeat. However, I believe that with the changes in the crypto order, the four-year cycle will not repeat.

This time is different.

I am betting with my position because:

ETFs are transforming BTC and ETH into assets that institutions can allocate.

Stablecoins have become geopolitical tools, now entering payments and capital markets.

DAT opens a path for tokens without ETFs to access equity liquidity, allowing VCs to exit while funding new enterprises.

RWAs are bringing the world economy on-chain and creating benchmark interest rates for DeFi.

This is not the casino of 2017, nor the frenzy of 2021.

This is a new era of structural change and adoption, where cryptocurrency merges with traditional finance while still being driven by culture, speculation, and belief.

The next winners will not come from buying everything.

Many tokens may still repeat the four-year sell-off. You need to be selective.

The real winners will be those projects that adapt to macro and institutional changes while maintaining cultural appeal with retail investors. This is the new order.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。