The recent signals of interest rate cuts from the Federal Reserve have further heated market expectations for liquidity easing, prompting some funds to flow into the cryptocurrency market in advance. As an emerging asset class, its narrative of hedging traditional risks and serving as a store of value continues to attract institutional interest.

In the current intertwining of global economic recovery and uncertainty, every move of the Federal Reserve's monetary policy consistently captures investors' attention.

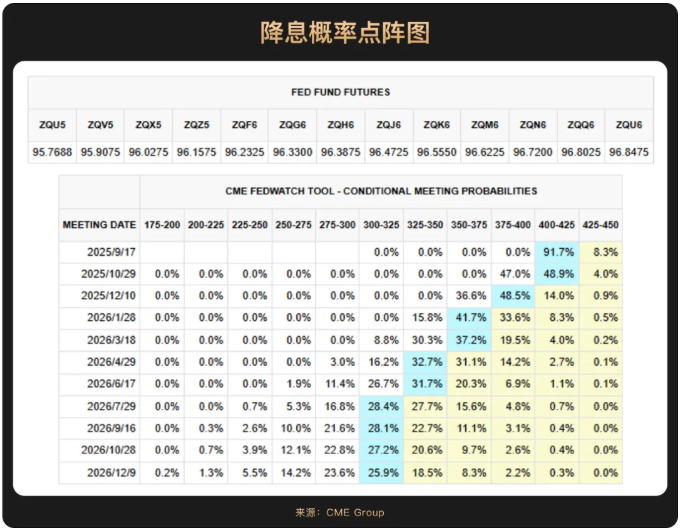

At the end of August, Federal Reserve Chairman Powell sent a clear signal to the market regarding a shift in monetary policy. He not only changed his hawkish stance from July, where he emphasized that "inflation risks outweigh employment risks," but also warned of the downside risks to employment leading to "significant increases in layoffs and rising unemployment rates." This statement caused market expectations for a rate cut in September to soar from 75% to over 90%, marking a shift in the Federal Reserve's policy balance towards promoting employment.

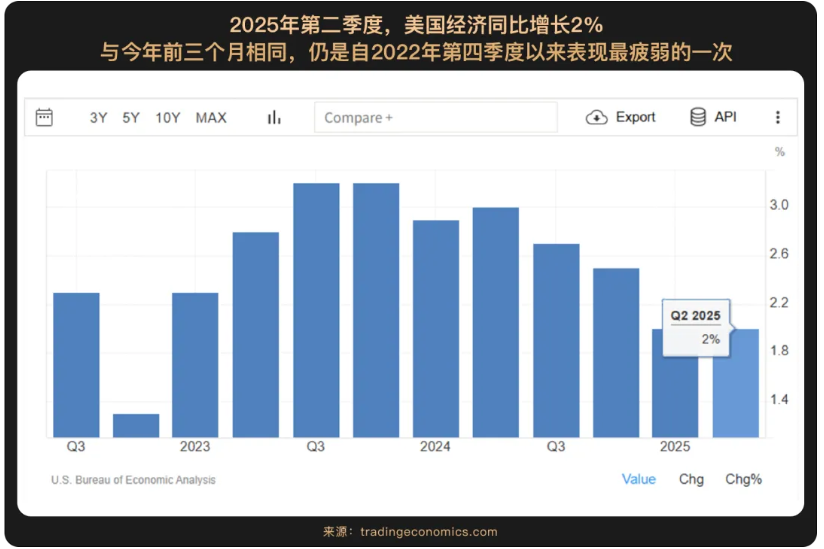

Powell's shift is not without reason; it reflects the significant slowdown in U.S. economic momentum. In the first half of 2025, the annualized GDP growth rate in the U.S. averaged 1.2%, far below the 2.5% of the same period in 2024. More critically, while the unemployment rate appears stable at 4.2%, underlying weaknesses are evident: the U.S. added only 73,000 non-farm jobs in July, significantly below the expected 104,000, marking the smallest increase since October of the previous year, and the non-farm employment figures for May and June were revised down by a total of 258,000. This indicates that the strength of economic expansion has diminished considerably.

However, the path to rate cuts is not without obstacles, as inflation remains a variable that the Federal Reserve cannot ignore. Although Powell assessed that the price impact from tariffs is more likely a "one-time shock" rather than persistent inflation, and the expected value of the five to ten-year inflation rate for August fell to 3.5% (below the expected 3.9%), the CPI data for August (which had not been released at the time of writing) will be the "deciding factor" for whether a rate cut occurs in September. If the August inflation data rises significantly above expectations (for example, if the CPI month-on-month growth exceeds 0.5%), it could still force the Federal Reserve to reassess its decision.

Moreover, the U.S. economy is still shrouded in the shadow of "stagflation." On one hand, economic growth is slowing; on the other hand, inflationary pressures have not completely dissipated due to tariffs and tightened immigration policies. This complex situation of "slowing growth alongside price pressures" suggests that Powell's dovish turn lacks confidence, and his language has become more cautious.

The future policy path of the Federal Reserve will heavily depend on data, especially when inflation and employment targets conflict. If subsequent inflation risks surpass employment risks, Powell may also halt rate cuts. Therefore, while we embrace the short-term asset price euphoria brought by rate cut expectations, we must remain clear-headed about the complexities of the economic fundamentals and the volatility of monetary policy.

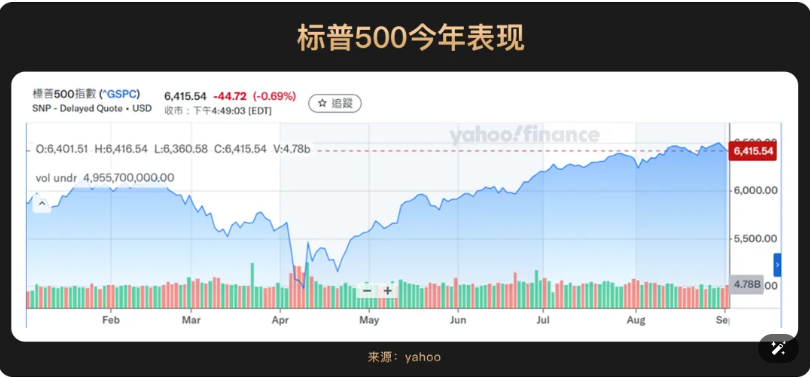

Since the beginning of this year, the U.S. stock market has performed strongly under the dual drivers of the AI revolution and expectations of policy shifts. In the first half of the year, U.S. stocks have repeatedly hit new highs, with technology and growth stocks leading the charge. By the end of August, the S&P 500 index had risen nearly 10% year-to-date, repeatedly setting historical records, and at one point breaking through the 6,500-point mark.

From the earnings report data, corporate profits are a key factor supporting market capitalization, with AI-related companies performing exceptionally well. The Q2 earnings reports of U.S. stocks in 2025 were outstanding, with AI companies becoming the core driving force behind this round of market upturn. Nvidia (NVDA), as a bellwether in the AI field, reported a significant year-on-year revenue increase of 56% in its second-quarter earnings. Although data center revenue was slightly below expectations, the overall performance confirmed the sustainability of the AI boom, boosting market confidence. Other chip stocks also performed well, with Broadcom (AVGO) and Micron Technology (MU) rising by 3%. AI concept stock Snowflake (SNOW) saw its stock price soar by about 21% due to better-than-expected earnings.

HSBC's analysis pointed out that AI has a significant impact on companies, with 44 S&P 500 companies achieving 1.5% operational cost savings and an average efficiency improvement of 24% through AI, which has somewhat offset the pressures from tariffs. The Federal Reserve's monetary policy expectations have also provided important support to the market, with a high probability of a rate cut in September boosting the performance of risk assets like U.S. stocks.

However, despite the strong performance of U.S. stocks, their valuations are at historical highs. As of August, the expected price-to-earnings ratio of the S&P 500 index is about 22.5 times, which, although lower than historical peaks, is still far above the average level of 16.8 times since 2000.

Overall, the U.S. stock market in August 2025, driven by AI innovation, relatively robust economic fundamentals, and expectations of loose monetary policy, has seen a significant increase in risk appetite. Although high valuations suggest that the market should remain vigilant, the strong growth in corporate profits and the potential upcoming rate cut cycle make U.S. stocks still considered attractive.

The Bitcoin market demonstrated unprecedented maturity in August 2025.

On one hand, according to analysis from JPMorgan, Bitcoin's six-month rolling volatility has plummeted from nearly 60% at the beginning of the year to about 30%, marking a historical low. At the same time, the volatility ratio of Bitcoin to gold has also dropped to a historical low, significantly enhancing Bitcoin's appeal to institutional investors.

The decrease in volatility is primarily attributed to the influx of institutional funds into regulated investment tools such as the U.S. spot Bitcoin ETF, which now accounts for over 6% of Bitcoin's total supply, as well as the ongoing allocation of Bitcoin by corporate treasuries (the DAT trend). These factors have collectively "locked in" a portion of the circulating supply, reducing market float.

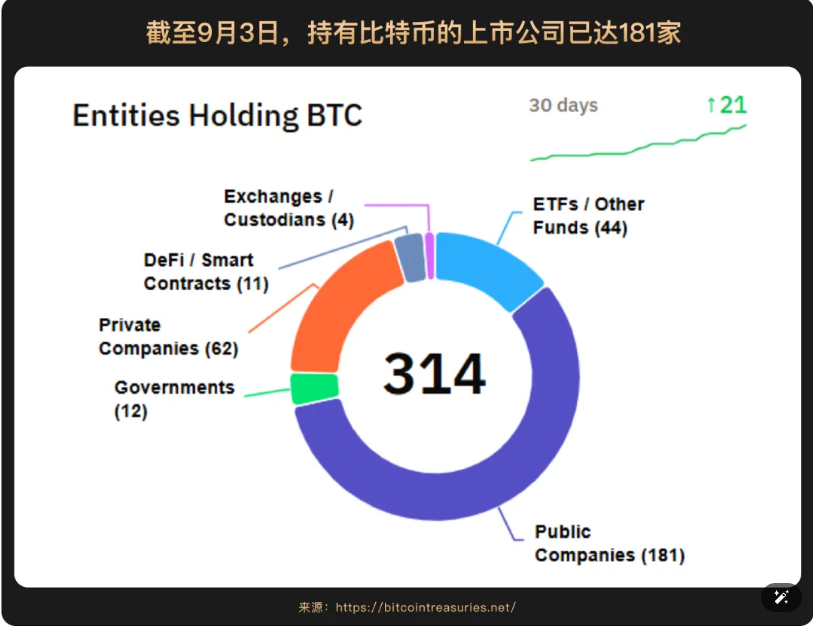

The DAT (Digital Asset Treasury) trend deepened in August, with its core being that publicly traded companies and institutions are using cryptocurrencies like Bitcoin as strategic reserve assets. Particularly for publicly traded companies, their capital allocation has shifted from project investments to holding cryptocurrencies on their balance sheets, effectively "endorsing" cryptocurrencies with their own balance sheets. This not only provides sustained purchasing power to the market, making them one of the strongest buyers, but also offers strong support for cryptocurrency prices. For companies, taking Strategy (MSTR) as an example, as long as the company's market value exceeds the actual value of Bitcoin on its balance sheet, there is an opportunity to raise funds from the market through methods such as private placements, issuing convertible bonds, or selling preferred shares, and then use these funds to purchase more Bitcoin. This way, the company can accumulate more coins at a lower cost. Statistics show that by mid-August, DAT cumulative financing has exceeded $15 billion, significantly higher than the scale of crypto VC during the same period. In 2025, leading institutions view DAT as an alternative/supplement to ETFs, emphasizing liquidity and flexibility advantages. At this year's Bitcoin Asia 2025 event in Hong Kong, the DAT trend also became a hot topic of discussion in the industry.

Meanwhile, favorable policies continue to emerge. Bitcoin, as the only cryptocurrency officially included in sovereign reserves, has a progressively clearer global regulatory framework. For example, the passage of the U.S. CLARITY Act and the repeal of SAB 121 accounting guidelines have paved the way for traditional financial institutions like banks to hold Bitcoin directly. This has also prompted other countries, such as Norway and the Czech Republic, to consider including Bitcoin in their foreign exchange reserves. In August, U.S. President Trump officially signed an executive order allowing $12.5 trillion in 401(k) retirement accounts to invest in Bitcoin and other digital assets, amounting to billions of dollars. This move opens the door for the massive U.S. pension system to enter the cryptocurrency market. Market analysis suggests that even a small allocation of retirement funds could bring significant potential incremental demand to the market, and the long-term purchasing power it brings should not be underestimated.

It is worth mentioning that in August, there was a significant rotation of funds within the cryptocurrency market. Bitcoin ETFs experienced significant outflows, with a net outflow of over $2 billion and a net inflow of about $4 billion. In contrast, Ethereum ETFs attracted a large amount of institutional funds. This reflects that some investors, after Bitcoin reached a historical high, shifted their focus to exploring the growth potential of Ethereum and other ecosystems. However, the rotation pace was also quick, as by the end of August, Ethereum ETFs also saw significant outflows, indicating short-term fluctuations in market sentiment.

Despite the short-term rotation of funds, the continued entry of top financial institutions signifies that cryptocurrencies have officially been integrated into the traditional financial ecosystem. According to Bloomberg, BlackRock's Bitcoin spot ETF attracted several top global financial institutions in the second quarter of 2025, with holdings spread across proprietary and client funds from hedge funds, market makers, and large banks. JPMorgan's analysis indicates that based on risk-adjusted valuations, Bitcoin's "fair price" should be around, showing potential upside compared to gold.

In summary, the significant decrease in Bitcoin's volatility, the evolution of institutional adoption models, and the acceleration of internal capital rotation in August all indicate that the cryptocurrency market is undergoing profound structural changes. While short-term capital flows may still fluctuate, the institutional foundation and macro drivers supporting the long-term value of cryptocurrencies have become increasingly solid.

In the long run, against the backdrop of a rate cut cycle boosting risk appetite and the continuous improvement of the crypto ecosystem, the resilience of Bitcoin as a core asset will continue to attract capital inflows, and the short-term volatility brought by market rotation will instead provide better positioning opportunities for bullish funds.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。