Original Author: Sam, IOSG

Introduction

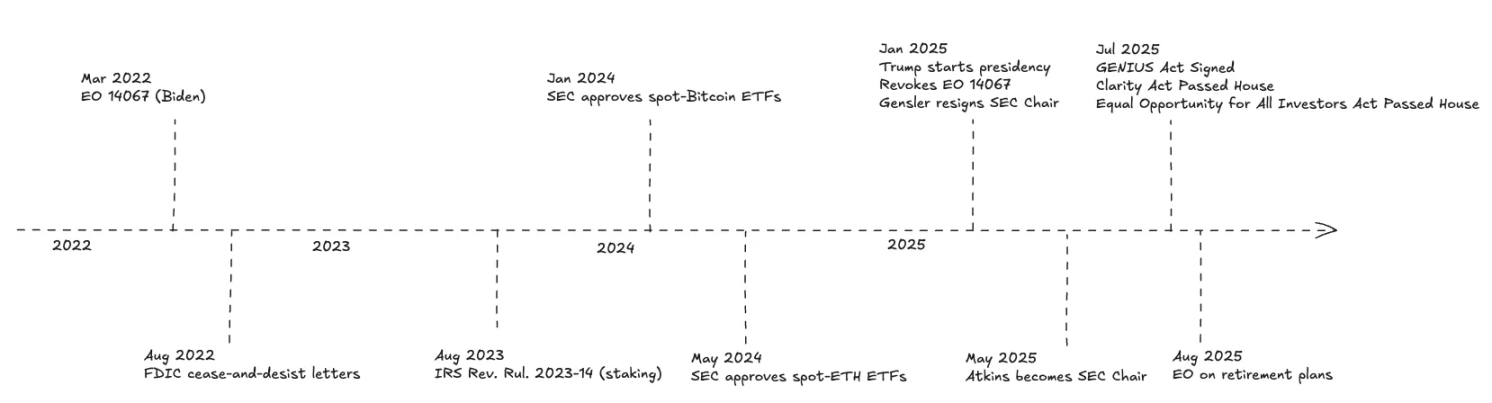

In the past three years, the United States' stance on cryptocurrency has undergone a significant shift—from an early focus on law enforcement and a relatively unfriendly attitude to a more constructive regulatory model that prioritizes rule-making. This policy shift is not only a crucial driver for the widespread adoption of cryptocurrency but also a key catalyst for the next phase of growth in the industry.

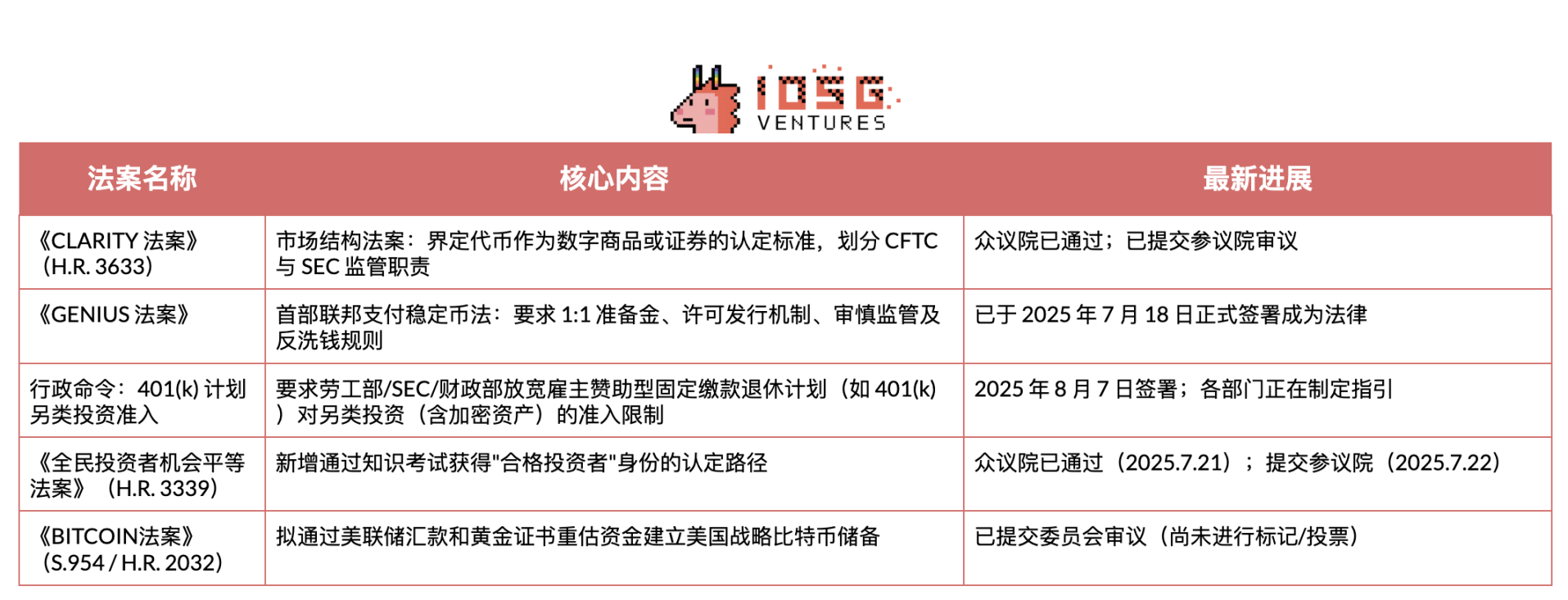

For investors, the current focus should be on the following developments: The "GENIUS Act" has officially come into effect, establishing a foundational regulatory framework for payment stablecoins; the House of Representatives has passed the "CLARITY Act," which will clearly define the standards for tokens under the jurisdiction of the Commodity Futures Trading Commission (CFTC) or the Securities and Exchange Commission (SEC); executive orders are pushing regulators to open investment channels for cryptocurrencies in 401(k) plans; and the House has passed a reform plan for accredited investor exams, which is expected to expand access for participants in private crypto trading.

CLARITY Act

The CLARITY Act establishes the core standard for whether a blockchain system is certified by the SEC as a "mature system," clearly delineating whether digital assets should be classified as "digital commodities" (CFTC jurisdiction) or securities (SEC jurisdiction). If a system is certified as mature, its native tokens can be traded as digital commodities under CFTC regulation; other on-chain assets will retain their original attributes.

What is a "Mature System"?

The Act specifies seven criteria for determining "maturity":

- System Value: Market value driven by actual adoption/use, with a fundamentally complete value mechanism.

- Functional Completeness: Trading, services, consensus mechanisms, and node/validator operations are all in real-time operation.

- Openness and Interoperability: The system is open-source, with no unilateral exclusivity restrictions on core activities.

- Programmatic System: Rules are enforced by transparent code (no discretionary operations).

- System Governance: No single entity/group can unilaterally modify on-chain rules or control ≥20% of voting rights.

- Fairness: No special privileges (repairs/maintenance/security operations only allowed through decentralized processes).

- Distributed Ownership: Total holdings by issuers/affiliated parties/related individuals <20%.

The table below summarizes the core differences in actual regulation between digital commodities (CFTC jurisdiction) and securities (SEC jurisdiction). The CLARITY Act framework essentially continues the existing regulatory division but provides a clear path for assets to transition from SEC jurisdiction to CFTC—once the underlying chain meets the above maturity standards, the relevant digital commodities can be transferred to the CFTC regulatory system.

With the establishment of a legal framework, the key issue is the specific impact of the CLARITY Act on various crypto sectors.

Staking Services

Under the CLARITY Act framework, pure on-chain staking—i.e., operating validators/sequencers and distributing native rewards—does not require registration with the SEC. This "safe harbor" covers the operation of validators/nodes and the distribution of protocol rewards to end users.

However, this exemption does not cover financing activities through the minting or sale of new staking derivative tokens. Projects still need to obtain mature blockchain certification in a timely manner and always bear anti-fraud and information disclosure obligations.

Reflecting on the MetaMask/Lido/Rocket Pool incident: the non-custodial ministerial-style (i.e., executing established protocol rules without autonomous decision-making) reward distribution model aligns more closely with the safe harbor standards of the CLARITY Act. In contrast, models like Kraken's pooled, custodial, and yield-promising approach will still be regarded as securities issuance and will face the same regulatory issues if not rectified and restarted.

Regarding liquid staking tokens (LST): a 1:1 certificate that only reflects the user's staked assets and protocol rewards falls under the ministerial-style end-user distribution category. However, if it involves strategic choices (such as re-staking/AVS distribution), layered points/additional yields, or issuing asset management tokens/shares that aggregate and redistribute yields—such models are considered managed investment claims and will remain under SEC jurisdiction unless they meet exemption criteria.

Decentralized Exchanges (DEX)

DEXs providing pure on-chain spot trading of native blockchain tokens (such as BTC, ETH, governance, or utility tokens) are exempt from exchange registration. Operating core smart contracts, order book logic, matching engines, or AMM factories for DEXs are not considered "exchange" activities as defined by the Securities Exchange Act—therefore, there is no need to register as an exchange or broker for spot trading of exempt tokens.

However, platforms involving derivatives (futures, options, perpetual contracts), security tokens (on-chain stocks), or real asset tokens (such as gold) remain fully under SEC or CFTC regulation.

Paying protocol fees to liquidity providers (LPs) or other users contributing work/assets falls under the end-user distribution category, applicable to the DeFi exemption channel of the CLARITY Act. It should be noted that this Act does not change the standards for determining securities. If governance tokens (like UNI) distribute cash or yields to holders solely based on holding behavior, it will constitute profits interest, which is likely to be classified as securities based on the Howey Test (expectation of profits derived from the efforts of others). In such cases, yield distribution and secondary trading of tokens will fall under SEC regulation.

Decentralized Stablecoins

The collateralized debt position (CDP) model (locking collateral to mint tokens pegged to the dollar) falls under SEC jurisdiction during the launch phase: tokens exchanged for value are considered investment contracts until the protocol obtains mature blockchain certification. Early teams can still raise funds under the initial issuance exemption provisions of the CLARITY Act—up to $50 million within a rolling 12-month period—but must fulfill specific information disclosure obligations and a four-year full-cycle anti-fraud responsibility. Once governance is fully on-chain and no single entity controls ≥20% of voting rights or collateral, the protocol can apply for mature certification; thereafter, governance tokens and minting/burning mechanisms will transition to CFTC digital commodity regulation, no longer subject to SEC securities rules.

The delta-neutral model is different: due to its reliance on crypto collateral and derivative risk exposure and yield distribution mechanisms, it does not fall under the CLARITY Act's spot commodity exemption even if the underlying chain matures; it also does not comply with the "licensed payment stablecoin" framework of the GENIUS Act.

Lending Business

Lending falls under the credit category rather than spot trading, thus not applicable to the spot commodity exemption provisions of the CLARITY Act. Unless invoking exemption regulations (D regulations/S regulations), pooled interest-bearing deposit certificates are regarded as securities under regulation.

Yield Aggregators

Immutable and non-custodial aggregator contracts (with no single entity able to unilaterally modify) do not need to register as trading platforms or intermediaries.

However, any governance tokens or treasury share certificates that grant holders future yield rights constitute investment contracts upon issuance. Additionally, complex custodial strategies may trigger multiple registration requirements: if rebalancing or control is off-chain or held by centralized operators, the project will lose DeFi exemption eligibility and re-trigger compliance obligations for brokers/dealers or exchanges.

ETF Staking Business

The CLARITY Act provides support at a fundamental principle level: this Act explicitly states for the first time that staking rewards belong to "end-user distribution" (not securities) and allows networks certified as "mature" to transfer their native tokens to CFTC regulation. This eliminates the core securities law barrier to transferring protocol yields within funds.

However, ETFs must still comply with fund regulatory rules. There are two major hard constraints: first, the Investment Company Act liquidity rules (22 e-4 rules) stipulate that "illiquid assets" cannot exceed 15% of net asset value; if an asset cannot be liquidated at near book value within seven calendar days, it is classified as an illiquid asset. Native staking positions with unbinding/exit queue mechanisms typically fall into this category.

Second, if the product is a registered open-end ETF, it must adhere to the diversification requirements of the 1940 Investment Company Act: the well-known 75/5/10 rule means that staking risk exposure and validator relationships cannot be concentrated in a single "issuer" or operator. In practice, this requires employing a multi-validator split strategy and precise scale control to ensure that no single counterparty exceeds the 5%/10% threshold in at least 75% of assets (some crypto ETPs circumvent this restriction through non-'40 Act structures, but most staking ETFs are still registered under the '40 Act and use Cayman subsidiary structures).

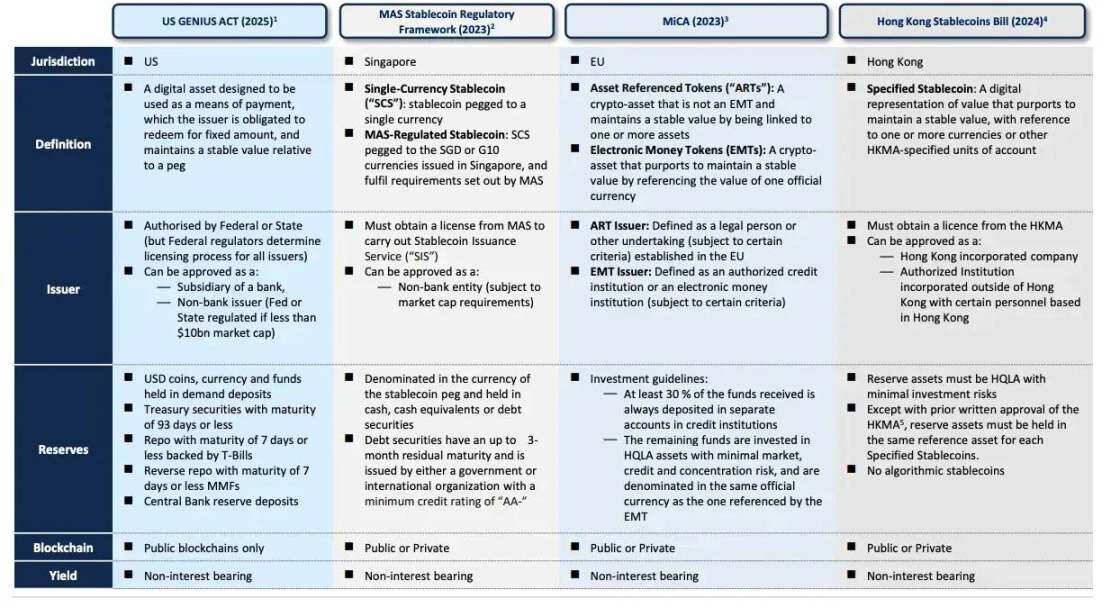

GENIUS Act

In July 2025, the United States officially enacted the GENIUS Act—this is the first federal law to comprehensively regulate stablecoins.

The Act limits issuance eligibility to regulated entities and establishes core rules for prudent operation, conduct standards, anti-money laundering, and bankruptcy disposal. Its core entry threshold is: "No entity other than licensed payment stablecoin issuers may issue payment stablecoins in the United States."

According to the Act, issuers must hold 100% reserve assets, limited to the following three categories:

- U.S. dollars or Federal Reserve bank deposits

- Short-term U.S. Treasury bills with a maturity of 93 days or less

- Treasury-backed overnight repurchase agreements

Under Section (7)(A) "Restrictions on Payment Stablecoin Activities," licensed issuers may only engage in the following activities:

- Issuing payment stablecoins

- Redeeming payment stablecoins

- Managing related reserve assets (including legally buying, selling, holding reserve assets, or providing custodial services)

- Legally providing stablecoin, reserve asset, or private key custodial services

- Conducting directly supportive activities related to the above

This strict list has clear regulatory intent: to ensure redemption safety by isolating stablecoin activities from high-risk activities. The Act specifically states that "payment stablecoin reserve assets may not be pledged, re-pledged, or reused." This means that banks, even when using their own issued tokens to value assets, cannot count them as reserve collateral for loan activities.

With the GENIUS Act clarifying issuance eligibility and reserve rules, multiple industries are beginning to transition from pilot programs to large-scale applications:

- Banking: Although facing competition from tokenized cash deposits, banks leverage their regulatory structure advantages to become natural issuers. The most likely path is through bank subsidiaries or strictly regulated bank-tech company collaborations, starting with enterprise use cases, whitelist counterparties, and conservative liquidity management policies to replace potential deposit outflows with stablecoin revenues.

- Retail: Large merchants view stablecoins as tools to reduce card fees and shorten settlement cycles. Early implementations will rely on licensed issuers and closed-loop redemption systems, promoting through settlement discounts rather than interest payments, and directly integrating with ERP and payment systems to enhance capital turnover efficiency.

- Card Organizations: Visa and Mastercard are incorporating stablecoins into new settlement channels while retaining their authorization, anti-fraud, and dispute resolution infrastructure. This move enables weekend and near-real-time settlements without requiring front-end modifications from merchants, pushing the profit model towards tokenization, compliance, and dispute management services.

- Fintech: Payment processors and wallet platforms are launching stablecoin accounts, cross-border payment, and on-chain settlement products based on bank-grade KYC, sanctions screening, and tax reporting. Competitive advantages will focus on hiding the complexity of chain technology, providing reliable fiat channels, and meeting operational control systems for corporate procurement and auditing requirements.

As the U.S. regulatory framework is established, similar frameworks are emerging globally (such as Hong Kong's "Stablecoin Regulation"), and more stablecoin regulations are expected to follow.

▲ TBAC Presentation, Digital Money

Other Policy Trends

New Retirement Plan Investment Policy

The executive order "Expanding Access to Alternative Assets for 401(k) Investors," signed in August 2025, aims to broaden the investment options for employer-sponsored retirement plans, allowing retirement savers to allocate digital assets and other alternative assets through actively managed investment tools.

As an executive function, the Department of Labor must reassess the Employee Retirement Income Security Act (ERISA) guidelines within six months. ERISA-compliant safeguards are expected to be introduced: reaffirming the prudential standards of neutrality and case-by-case analysis, and providing a safe harbor verification checklist.

The independent SEC, while not directly bound by the executive order, can promote access through rule-making: clarifying standards for qualified custodians, improving disclosure/marketing regulations for crypto funds, and approving retirement plan-friendly investment tools.

Currently, most core 401(k) menus do not include crypto assets, primarily accessed through self-directed brokerage windows—participants can purchase spot Bitcoin ETFs (some plans include Ethereum ETFs), and a few providers offer limited "crypto asset windows." In the short term, compliance pathways will be limited to regulated ERISA-compliant products: spot BTC/ETH ETFs and professionally managed funds with regulated crypto allocations. Due to the 401(k) committee's adherence to ERISA's "prudent investor" principle, it is challenging to justify single volatile tokens, self-custody, or staking/DeFi yields as suitable for ordinary savers. Most tokens and yield strategies lack standardized net asset valuation, stable liquidity, and clear custodial audit trails, and their legal status is unclear, which may trigger SEC/Labor Department scrutiny and collective lawsuit risks if included in plans.

Equal Opportunity for All Investors Act

This Act proposes to establish a new "qualified investor" designation path through an SEC knowledge exam. The House passed the draft on July 21, 2025, and the Senate received it for review on July 22.

Early U.S. token presales, crypto venture capital, and most private rounds rely on D regulations, currently limited to qualified investors. The knowledge exam path will break through wealth/income threshold restrictions, allowing knowledgeable but not necessarily wealthy investors to legally participate in private crypto financing.

Opponents argue that expanding access to opaque, low-liquidity private markets may exacerbate investment risks. The fate of the bill in the Senate will depend on the rigor of the exam and whether sufficient safeguards are in place. Even if passed, the SEC will need one year to design the exam and an additional 180 days to implement it through FINRA, meaning it will not take effect immediately.

The BITCOIN Act

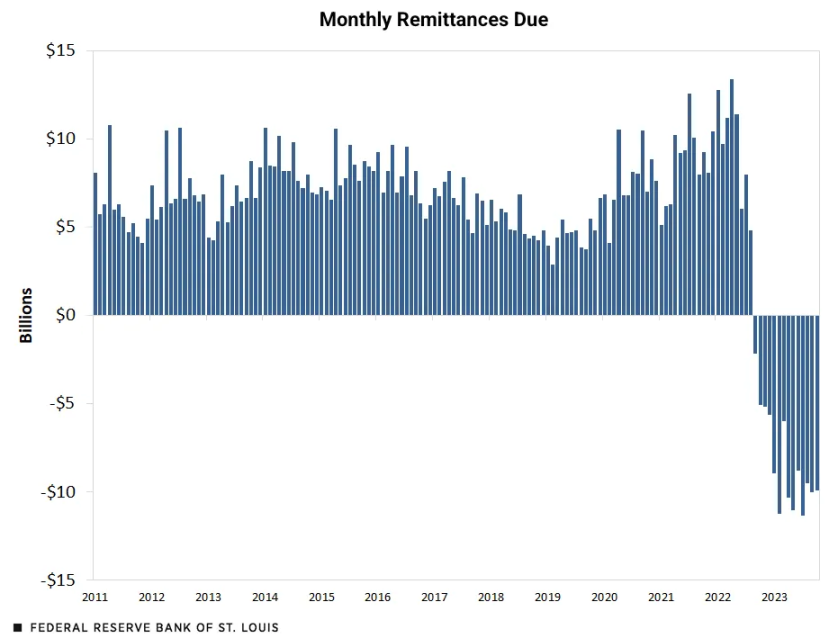

Senator Cynthia Lummis submitted the BITCOIN Act (S.954) on March 11, 2025, proposing to establish a U.S. strategic Bitcoin reserve. The Act requires the Treasury to purchase 200,000 BTC annually (for five years, totaling 1 million BTC) and sets a 20-year lock-up period (during which sales, exchanges, or pledges are prohibited). After 20 years, gradual sales may be suggested to reduce federal debt (limited to 10% of holdings every two years). The Act also stipulates that confiscated BTC must be transferred to the strategic reserve after judicial proceedings conclude.

Funding does not rely on new taxes or national debt but is sourced through: (1) the first $6 billion of annual remittances from the Federal Reserve to the Treasury during the 2025-2029 fiscal years prioritized for purchasing Bitcoin; (2) revaluing the Federal Reserve's gold certificates from $42.22 per ounce to market price (approximately $3,000 per ounce), with the appreciation portion prioritized for Bitcoin investment.

▲ https://www.stlouisfed.org/

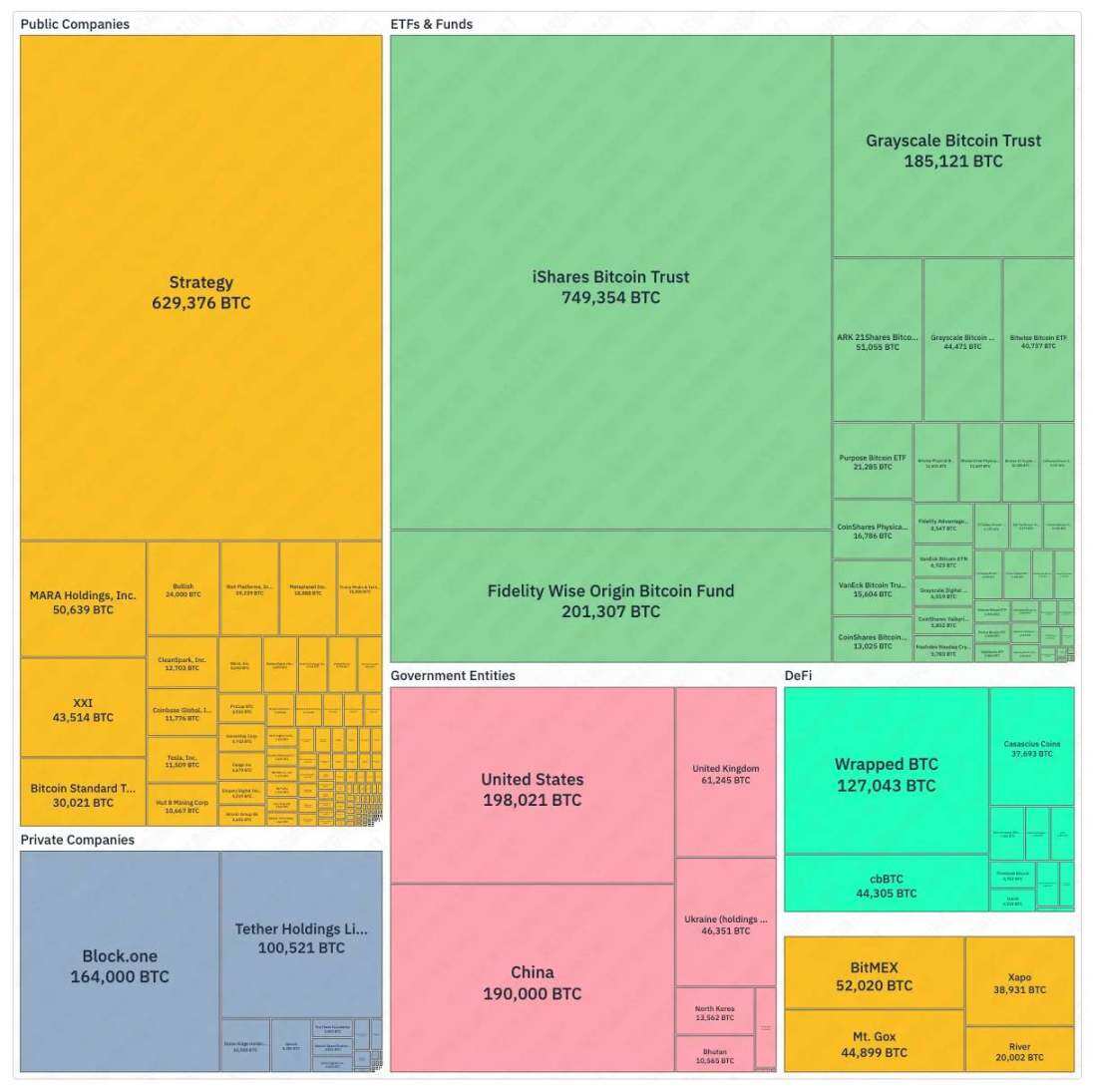

If fully implemented, the U.S. would accumulate 1 million BTC (approximately 4.8% of the total cap of 21 million). In comparison, the current largest Bitcoin-holding public company, MicroStrategy, holds 629,000 BTC (about 3%), and this reserve size would surpass any single ETF holding, even significantly exceeding the total industry ETF holdings reported by bitcointreasuries.net (approximately 1.63 million BTC).

By elevating Bitcoin to the status of a strategic reserve asset, the U.S. would grant it unprecedented legitimacy. This official endorsement could change the stance of institutional investors who have been waiting on the sidelines due to regulatory uncertainty. If the U.S. takes the lead, it may trigger similar actions from other countries. All these effects would create strong price drivers for Bitcoin: sustained purchases over five years would create substantial demand, combined with supply shocks from the 20-year lock-up period, likely leading global capital to follow suit.

▲ bitcointreasuries.net

However, the BITCOIN Act is currently only submitted to the Senate Banking Committee and has not yet been reviewed or voted on, lagging behind the already passed CLARITY Act in the House and the legislated GENIUS Act. In practical terms, this Act involves core issues of Federal Reserve independence and budget politics: mandating the purchase of 1 million BTC and locking it for 20 years, financed through Federal Reserve remittances and gold revaluation. The Act currently has mainly Republican support, but significant decisions at the balance sheet level typically require bipartisan consensus to pass in the Senate. More critically, directing future Federal Reserve remittances for Bitcoin purchases would reduce fiscal revenues that could be used to lower borrowing costs, potentially exacerbating budget deficit risks.

ETF

The clearest signal of a policy shift is the SEC's approval of spot crypto ETFs after years of delays. In January 2024, the agency historically approved multiple spot Bitcoin ETPs and immediately initiated trading, driving Bitcoin to a historic high in March 2024 and attracting mainstream capital. By July 2024, spot Ethereum ETFs were trading in the U.S., with major issuers launching funds that directly hold ETH.

The SEC has also shown an open attitude towards assets beyond Bitcoin and Ethereum: actively processing other crypto ETF applications and collaborating with exchanges to establish universal listing standards to simplify future approval processes. Positive progress is also seen in the staking sector—the SEC recently clarified that "protocol staking activities" do not constitute securities issuance under federal securities law.

Development of U.S. Prediction Markets

In early October 2024, a federal appeals court approved the launch of the prediction market platform Kalshi before the elections, significantly enhancing market participation. The CFTC subsequently continued to advance the rule-making for event contracts and held a roundtable in 2025, although no timetable was set, further guidance or final rules may be forthcoming.

Polymarket, through its subsidiary QCX LLC (now renamed Polymarket US), obtained CFTC-designated contract market status and announced the acquisition of the QCEX exchange, indicating that it would "soon" open access to the U.S. market. If integration and approval progress smoothly, and the CFTC ultimately adopts an open attitude towards political contracts, Polymarket may participate in the 2026 U.S. election prediction market. Reports indicate that the platform is also exploring issuing a dedicated stablecoin to capture treasury yields for platform reserves, but currently, user yields mainly come from market-making/liquidity rewards rather than returns from idle funds in real assets.

Conclusion

U.S. policy is a major lever shaping market structure and capital access, thereby having a decisive impact on Bitcoin prices. The SEC's approval of spot ETFs on January 10, 2024, opened mainstream capital channels, driving Bitcoin to a historic high in March 2024; while a friendly policy environment following Trump's victory in November 2024 further propelled prices to refresh historical peaks in July-August 2025. Future trends will depend on the normalization process of rules and infrastructure.

Baseline Scenario: Policies continue to be implemented. Regulatory agencies enforce the GENIUS Act, the Department of Labor formulates ERISA safeguards, and the SEC gradually approves ETFs/staking mechanisms. Access channels expand through brokerage windows and registered investment advisors (RIAs), and banks and card organizations expand stablecoin settlement applications.

Optimistic Scenario: The Senate advances market structure legislation, the first batch of "mature blockchain" certifications lands without significant objections, and the Department of Labor provides a safe harbor system. Banks issue licensed stablecoins on a large scale, and the ETF product menu continues to expand. This will accelerate pension/RIA allocations, enhance liquidity depth, and lead to a revaluation of compliant, truly decentralized assets.

Pessimistic Scenario: Legislative processes stagnate—all pending bills remain unadvanced. The SEC delays or rejects amendments to staking-related ETF applications. Banking regulators take a hard stance on the implementation of the GENIUS Act, delaying large-scale issuance; major custodians restrict brokerage window access.

Regardless of the scenario, the following hard indicators will become key observation signals: the number of licensed stablecoin issuers and settlement volumes, the status of the first batch of mature certifications and SEC objections, net inflows into ETFs, and the proportion of 401(k) plans that open brokerage windows, as well as the progress of bank/card organization settlement pilots transitioning to formal operations. These indicators will reveal whether the U.S. crypto market is evolving towards a regulated financial system or falling back into contraction.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。