Author: Filippo Armani

Translation and Compilation: Saoirse, Foresight News

_ (Content has been edited for brevity; for a quick overview, please refer directly to the key points and summaries at the end of each section)_

In Latin America, cryptocurrency has evolved into a practical financial tool used for everyday savings, transfers, and consumption. In a region plagued by issues such as inflation, currency volatility, and limited traditional banking services, millions choose cryptocurrency out of practical necessity rather than for speculative purposes. This report focuses on its core application scenario—payments—analyzing the four main pillars of infrastructure: exchanges, stablecoins, deposit and withdrawal channels, and payment applications, showcasing the underlying architecture that supports remittances, payroll, savings, and other real-world scenarios.

Although the report is not exhaustive, it aims to provide a shared, transparent, data-driven perspective on cryptocurrency usage in Latin America. As noted in Lemon Cash's “2024 Cryptocurrency Industry Status Report,” the region is large, rapidly developing, and still under-researched, with significant differences in usage patterns across countries—Brazil is dominated by institutional capital flows and retail speculation, Mexico focuses on remittance-driven activities, while Venezuela and Argentina heavily rely on stablecoins to hedge against inflation. Therefore, the report emphasizes common practical use cases rather than viewing Latin America as a single market.

Key Points

- Exchanges remain the core financial infrastructure: Supporting retail adoption, institutional activity, and cross-border value transfer in Latin America, annual fund flows surged from $3 billion in 2021 to $27 billion in 2024, with Ethereum dominating high-value settlements, Tron supporting low-cost USDT payments, and Solana and Polygon driving retail capital flow growth.

- Stablecoins are the backbone of the on-chain economy in Latin America: By July 2025, USDT and USDC accounted for over 90% of tracked exchange trading volume. At the same time, local stablecoins pegged to the Brazilian real (BRL) (with trading volume up 660% year-on-year) and the Mexican peso (MXN) (with trading volume up 1100 times) are gradually emerging as domestic payment tools.

- Deposit and withdrawal channels are faster and more accessible: In addition to exchanges, protocols like PayDece and ZKP2P, along with infrastructure providers like Capa, processed nearly $60 million in transaction volume, enabling permissionless multi-link connections between cryptocurrency and the local economy.

- Payment applications are evolving into crypto-native digital banks: Platforms like Picnic, Exa, and BlindPay integrate stablecoin balances, savings, and real-world consumption functions within a single interface. Cryptocurrency is widely used by bank customers and the unbanked to meet practical financial needs, especially favored by younger, mobile-first user groups.

Introduction

Latin America is one of the most active regions for cryptocurrency adoption globally, shaped by economic volatility, financial exclusion, and everyday needs. Faced with long-term inflation, continuous currency devaluation, and limited traditional banking services, millions in the region use cryptocurrency not for speculation or entertainment, but for survival, stability, and efficiency.

As of June 2024, the total cryptocurrency inflow in Latin America reached $415 billion, with Brazil, Mexico, Venezuela, and Argentina ranking among the top 20 globally for grassroots cryptocurrency adoption (Chainalysis, 2024). In markets like Argentina and Colombia, stablecoins have replaced Bitcoin as the most popular crypto asset, with exchange data showing that trading activity often spikes around payday as users convert their salaries into digital dollars to preserve value (Bitso, 2024).

In this ecosystem:

- Both stablecoins pegged to the US dollar and local currencies have become vital financial lifelines in Latin America, helping people secure savings, send remittances, and maintain purchasing power. In 2024, over 70% of cryptocurrency purchases in Argentina were stablecoins (Lemon, 2024).

- Exchanges like Lemon, Bitso, and Ripio are key infrastructures for accessing cryptocurrency and liquidity. Centralized platforms dominate usage in the region, with 68.7% of cryptocurrency trading volume in Latin America conducted through centralized exchanges, comparable to North America (Chainalysis, 2024).

- Deposit and withdrawal channels like ZKP2P, PayDece, and Capa play a crucial role in connecting cryptocurrency with the local economy, especially in countries with limited traditional financial services.

- Payment applications like Picnic, Exa, and BlindPay make cryptocurrency more user-friendly, integrating wallet, remittance, exchange, and even yield functions within mobile-native interfaces designed for local users.

These pillars collectively build a parallel financial system that is often more stable, accessible, and practical than traditional alternatives.

Exchanges

As of mid-2024, centralized exchanges remain the primary entry point for cryptocurrency in Latin America, accounting for 68.7% of total activity in the region, slightly below North America but far exceeding other emerging markets (Chainalysis, 2024). This reflects users' preference for trusted, regulated platforms with direct fiat access. These exchanges have expanded from basic trading services to include payments, savings tools, and cross-border transfers, becoming key deposit channels in the crypto economy.

The market is highly concentrated. Lemon's 2024 report shows that Binance controls 54% of trading volume in Latin American centralized exchanges, maintaining a dominant position. Among regional competitors like Bitso, Foxbit, and Mercado Bitcoin, Lemon leads with a 15% market share, highlighting the role of local applications in meeting needs that global platforms may overlook (Lemon, 2024).

Use cases are also evolving. At the retail level, exchange functionalities are becoming increasingly complex: Bitso's professional trading interface, Bitso Alpha, saw trading volume in 2024 comparable to Bitso Classic, despite having fewer users, indicating the significant influence of active professional traders (Bitso, 2024). At the institutional level, Brazil leads the region: from Q4 2023 to Q1 2024, transactions over $1 million grew by 48.4% (Chainalysis, 2024), driven by interest from traditional financial institutions, ETF demand, and regulatory initiatives like the Drex pilot. Major banks like Itaú and BTG Pactual have launched cryptocurrency investment services, blurring the lines between exchanges and banks. Small and medium-sized enterprises are also using exchanges for cross-border settlements and currency hedging; for example, in Brazil, companies use cryptocurrency to pay Asian suppliers to avoid bank fees, while Bitcoin and stablecoins are widely accepted in Asia (Frontera, 2024).

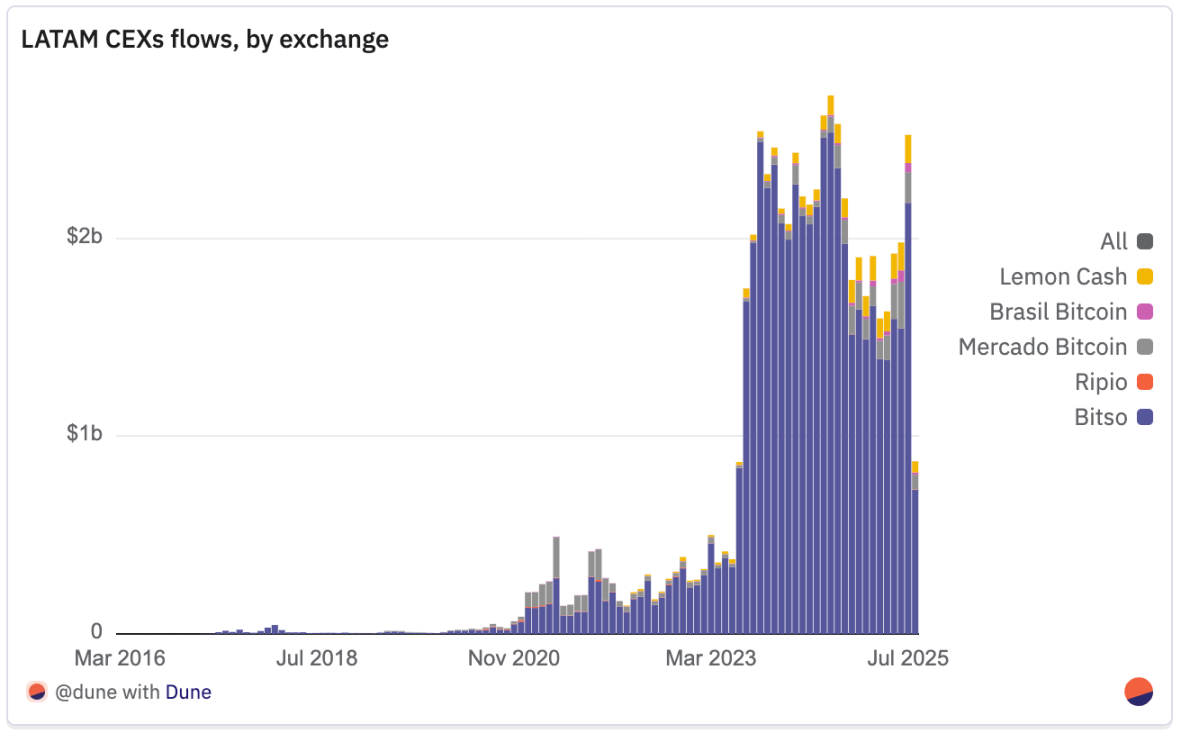

On-chain Flow Analysis of Latin American Exchanges

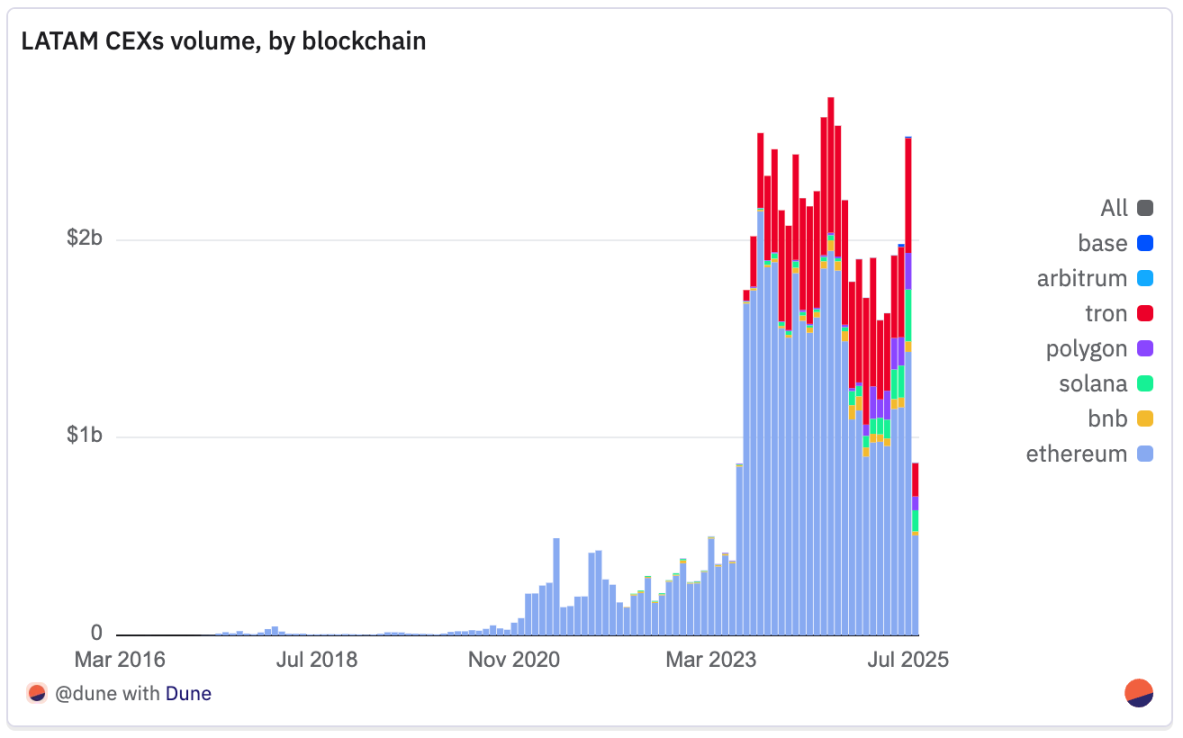

Flow analysis tracks the transfer of assets between hot wallets on exchanges, reflecting actual adoption, liquidity demand, and the role of deposits and withdrawals between cryptocurrency and the broader economy. Due to data availability limitations, the analysis does not include native Bitcoin chain data, so total exchange trading volume may be underestimated, and Bitcoin's role is only reflected through wrapped forms on other networks (e.g., BTCB).

From early 2021 to mid-2025, the fund flows of centralized exchanges in Latin America show a clear trajectory of growth, maturation, and consolidation, with total tracked transfers increasing from $3 billion in 2021 to $27 billion in 2024.

In 2021, the scale of activity was relatively small by global standards: Bitso processed less than $2 billion, Mercado Bitcoin around $1.2 billion, and smaller platforms like Brasil Bitcoin and Ripio only tens of millions of dollars. The market remained fragmented among OTC desks, informal brokers, and a few formal exchanges. In 2022, the market began to diversify, with new entrants like Lemon Cash recording $90 million in transfers in their first year.

2023 marked a true turning point, with trading volume increasing more than threefold year-on-year. Bitso's volume grew from $2.5 billion to $13.6 billion, while Lemon Cash nearly tripled to $260 million, as exchanges gradually integrated into payment ecosystems, remittance channels, and corporate capital flows. Inflation and currency devaluation in Argentina and Brazil drove demand for stablecoins, making exchanges key channels for dollar deposits and withdrawals.

Liquidity peaked in 2024, with Bitso reaching $25.2 billion, Mercado Bitcoin increasing to $915 million, and Lemon Cash hitting $870 million. Importantly, this growth did not rely on a sustained bull market but reflected a shift towards real applications such as cross-border trade, remittance settlements, and currency hedging.

A slowdown occurred in early 2025, with January dipping to a recent low, but activity steadily rebounded. By July, monthly trading volume reached its highest level since September 2024. Bitso's volume from January to July was $11 billion, lower than 2024 levels but still several times that of any year prior to 2023; Mercado Bitcoin reached $990 million, and Lemon Cash processed $890 million in just over half a year, likely approaching historical records.

Supporting all this flow is a clear technological pattern: Ethereum remains the backbone of exchange activity in Latin America. From January 2021 to July 2025, transfers based on Ethereum totaled over $45.5 billion, accounting for about three-quarters of all recorded flows, reflecting its position as the primary settlement layer for high-value transfers, stablecoins, and tokenized assets. Tron ranks second with $12.5 billion, primarily due to its role as a low-cost transfer channel for USDT, widely used for remittances and cross-border payments. Solana ranks third with a total flow of $1.45 billion, slightly above Polygon's $1.17 billion. In 2025, Polygon's share steadily increased, expanding its role in payment-related activities, accounting for 7.2% of monthly trading volume in July, slightly above Solana's 7.1%. Binance Smart Chain follows closely with $963 million. Base ($23.6 million) and Arbitrum ($11.2 million) are smaller but rapidly growing: Base has processed $22 million in 2025 to date, compared to just $1 million for all of 2024; Arbitrum has matched its total for all of 2024 by July.

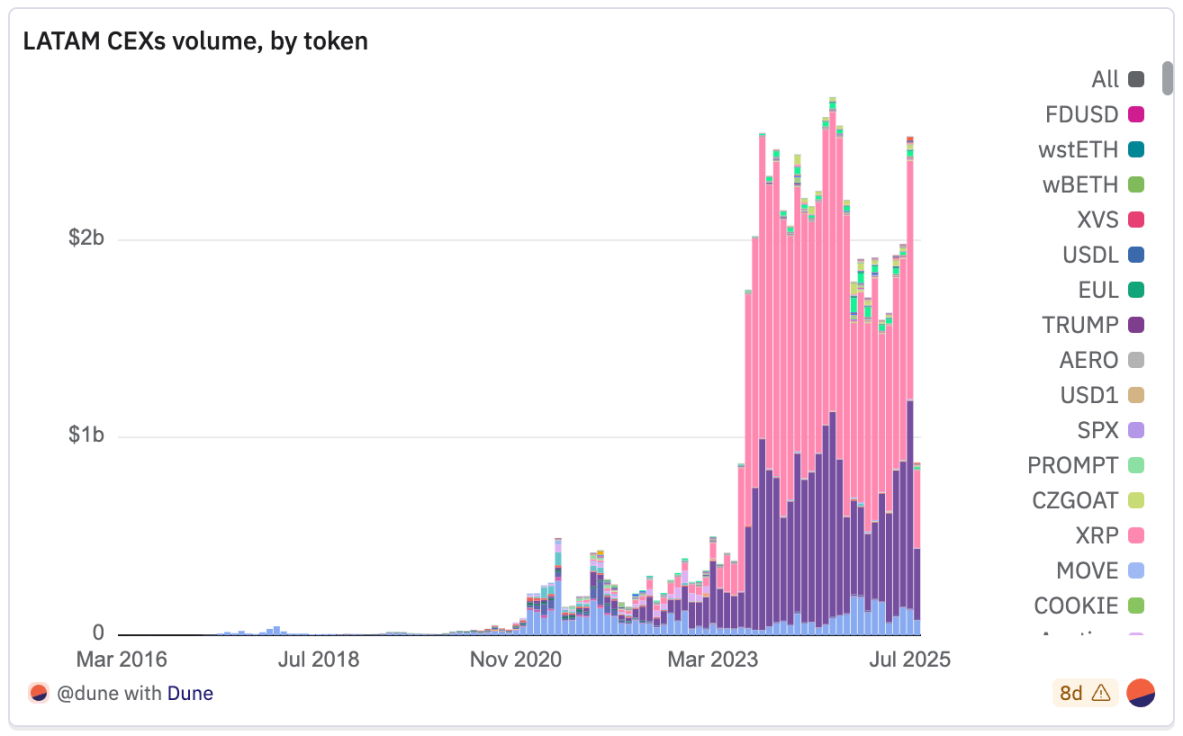

The situation at the token level is clearer. As mentioned, stablecoins dominate the market: by July 2025, USDT and USDC together accounted for nearly 90% of all transfer volumes. From January 2021 to July 2025, USDT processed $32.4 billion, almost double that of USDC ($18.36 billion), reflecting USDT's core position on the Tron network. ETH is the third-largest asset, transferring $4.74 billion. As of July 2025, SOL ranks fourth, accounting for about 1% of determined liquidity, with $660 million transferred since 2021.

Notably, the composition has changed over time: during 2021-2022 and most of 2023, ETH's share of trading volume often matched or even exceeded that of stablecoins, with a more diverse list of top tokens, including the BEP-20 version of Bitcoin (BTCB) and MATIC, which performed well due to Polygon's role. However, since the end of 2023, the share of stablecoins (especially USDT and USDC) has significantly expanded. This evolution may reflect a broad change in the use cases behind exchange liquidity: shifting from speculative trading of volatile assets to practical applications such as payments, remittances, merchant settlements, and dollar savings deposits and withdrawals.

The changes in blockchain and token composition indicate that the Latin American exchange ecosystem is maturing. Ethereum remains the settlement backbone, Tron dominates low-cost stablecoin transfers, and Polygon steadily increases its share by carving out a niche in payment-focused capital flows. These trends collectively suggest that exchanges are increasingly being used as channels for payments and value transfers rather than purely speculative trading venues.

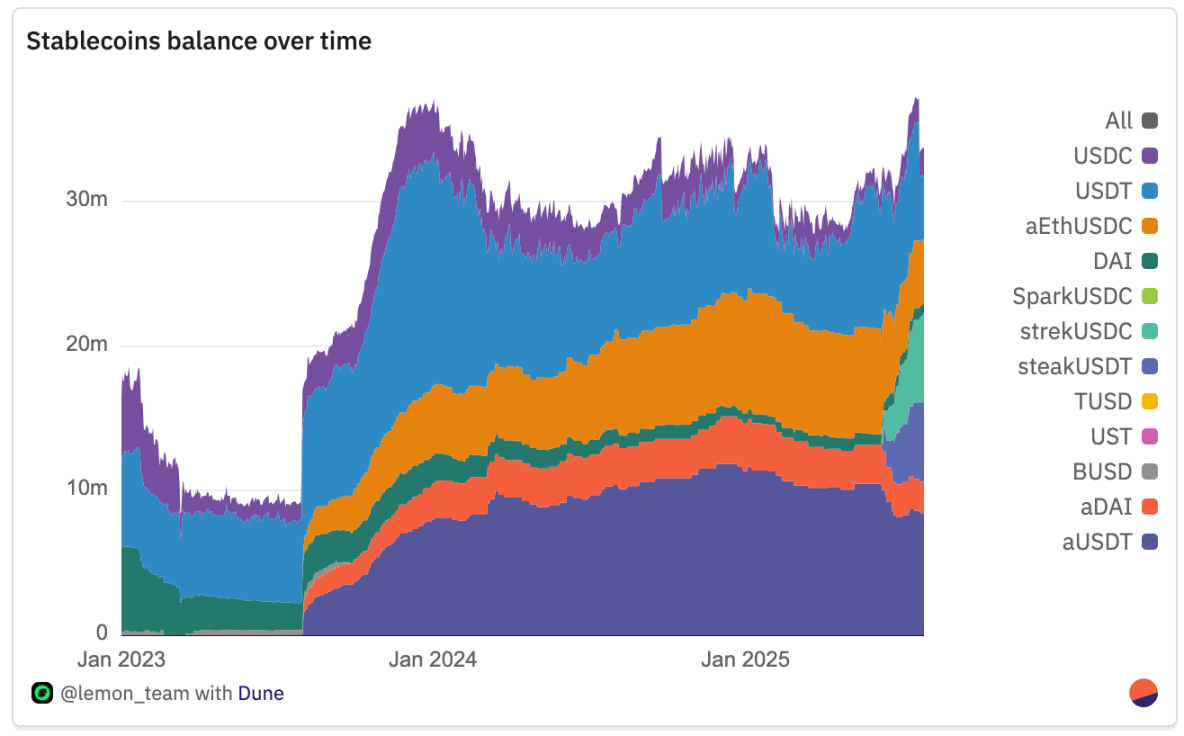

Lemon Cash is a typical example of this evolution. Reserve proof data shows that by mid-2025, the exchange held approximately $100 million in assets, with stablecoins making up the majority.

Over the past year, stablecoin balances have generally remained in the range of $20 million to $30 million, highlighting their role as a retail-friendly dollar channel.

Its network activity exhibits multi-chain characteristics: withdrawals are most active on Tron, Binance Smart Chain, and Ethereum, while deposits are strongest on Binance Smart Chain, Tron, and Stellar, with newer layer-2 networks like Polygon and Base growing from a smaller base. This reflects how exchanges in the region adapt to the fees, speeds, and accessibility of different networks, although settlement volumes at the regional level remain dominated by Ethereum.

Overall, the chain and token data reinforce structural trends: Latin American exchanges, driven by Ethereum and stablecoins, have achieved significant growth, with occasional speculative surges temporarily altering trading volume rankings. This pragmatic adoption, combined with cultural vibrancy, may define exchange activity in the region in the coming years.

Summary of Key Points

Exchanges have evolved into financial infrastructure. From 2021 to 2024, tracked exchange liquidity increased from $3 billion to $27 billion, with annual trading volume growing ninefold, shifting from fragmented OTC activities to large integrated platforms serving retail and institutional users.

- Bitso's liquidity grew from $1.96 billion in 2021 to $25.2 billion in 2024 (an increase of 1185%), accounting for the majority of all tracked liquidity in Latin American exchanges. From January to July 2025, its processing volume reached $11.2 billion, 44% of last year's total.

- Lemon's trading volume nearly doubled in 2023, reaching $87 million in 2024; as of July 2025, it has processed $84 million.

- From January 2021 to July 2025, Ethereum dominated approximately 75% of liquidity in Latin American exchanges (totaling $45.4 billion), processing high-value stablecoin and token transfers. Tron follows closely with $12.5 billion, dominating low-cost USDT remittance transfers.

- Solana ranks third overall at $1.5 billion, but by July 2025, Polygon surpassed it, accounting for 8% of monthly liquidity.

Stablecoins

Stablecoins are the financial cornerstone of cryptocurrency adoption in Latin America, serving purposes far beyond speculation. In the region, stablecoins act as savings tools, payment channels, remittance channels, and inflation hedges, becoming the most practical and widely used form of cryptocurrency. Latin America now leads globally in real-world stablecoin applications: according to Fireblocks' “2025 Stablecoin Status,” 71% of respondents use stablecoins for cross-border payments, and 100% of respondents have either enabled, are piloting, or plan to launch stablecoin strategies. Equally important, 92% of respondents reported that their wallet and API infrastructure supports stablecoins, highlighting demand and technological maturity. For millions in the region, stablecoins have become equivalent to digital dollars, accessible inflation hedges, and means to bypass capital controls (Frontera, 2024). In many cases, they are the only practical way for citizens to hold dollarized savings.

In countries like Argentina, Brazil, and Colombia, stablecoins have replaced Bitcoin as the preferred asset for everyday use, thanks to their price stability and direct peg to dollar-denominated value (Fireblocks “2025 Stablecoin Status”). This trend aligns with the exchange data from the previous section, where over 90% of exchange transfer volumes involve USDC and USDT. In 2024, on the Bitso platform in Argentina, these two stablecoins accounted for 72% of all cryptocurrency purchases, while Bitcoin only accounted for 8% (Bitso, 2024). A similar situation exists in Colombia, where stablecoins account for 48% of purchases, driven by restrictions on dollar bank accounts and ongoing currency volatility. The shift in Brazil is even more pronounced: stablecoin trading volume on local exchanges grew by 207.7% year-on-year, surpassing all other crypto assets (Chainalysis, October 2024). Besides transfers, stablecoins accounted for 39% of regional purchases in 2024, up from 30% the previous year (Bitso, 2024).

Local Stablecoins

While dollar-pegged assets still dominate stablecoin usage in Latin America to hedge against inflation, local currency-pegged stablecoins have seen rapid growth over the past two years. These tokens, pegged to local currencies such as the Brazilian real (BRL) or the Mexican peso (MXN), are increasingly used for domestic payments, on-chain commerce, and integration with local financial systems. By eliminating the frequent need for dollar-to-local currency exchanges, they reduce costs for merchants and users while speeding up local business settlements. For businesses, they connect directly with payment systems like Brazil's PIX, enabling instant, bankless transfers that comply with accounting and tax requirements. In high-inflation economies, they also serve as bridge assets, allowing users to transact in stable local currency while retaining the option to hedge into dollars or other value storage tools when needed.

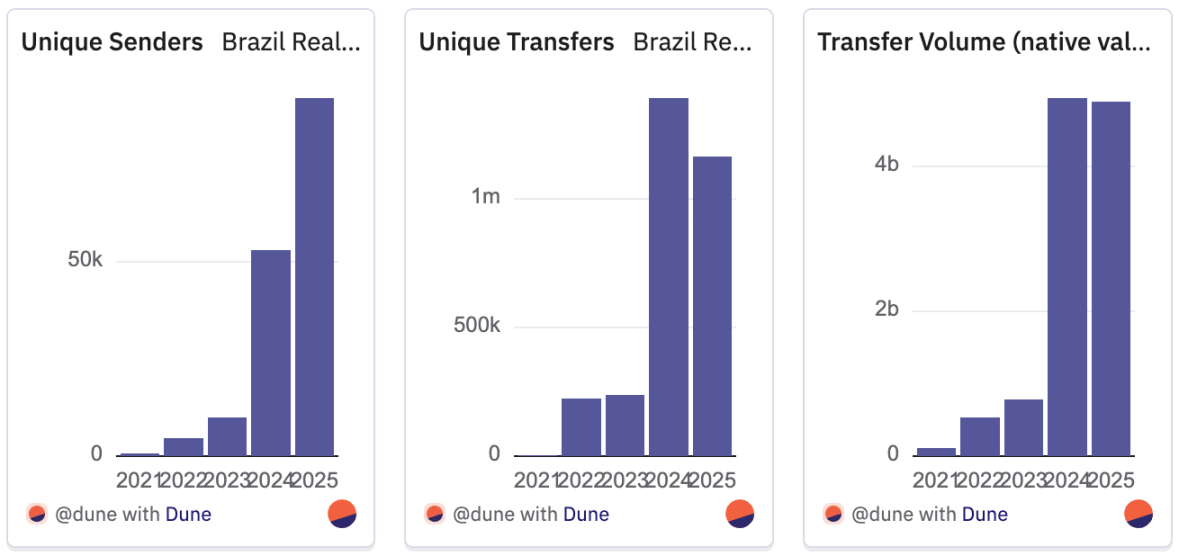

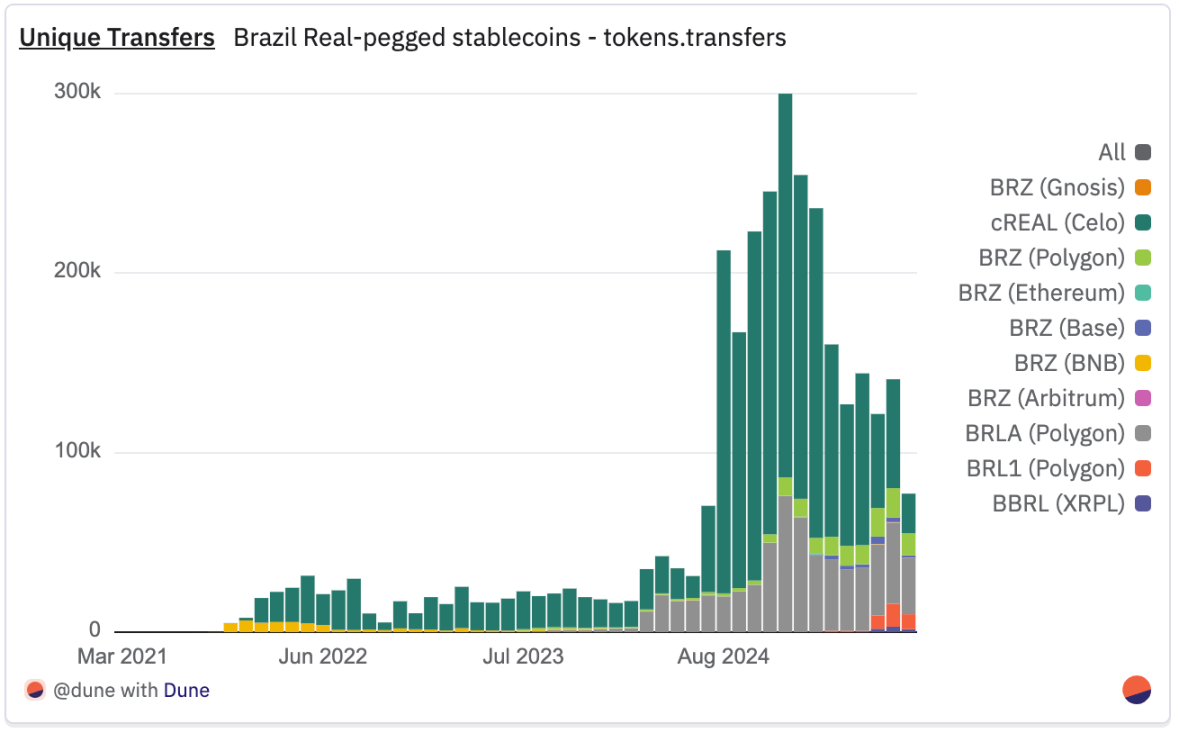

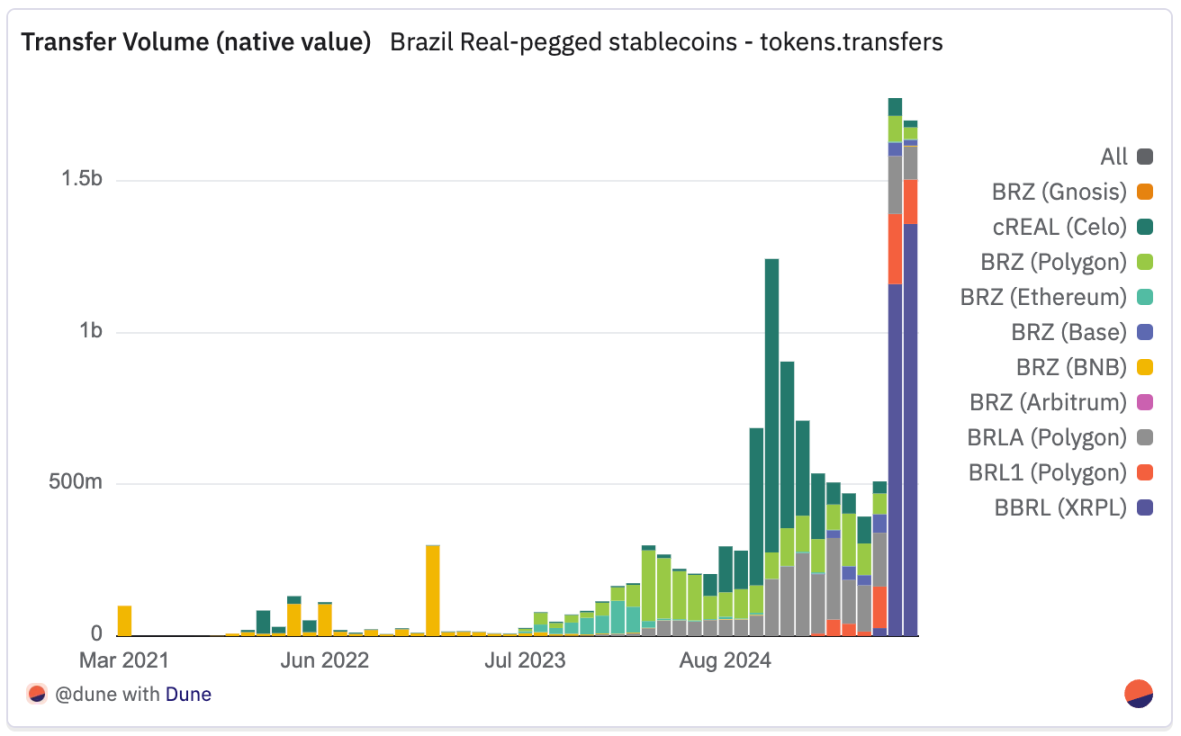

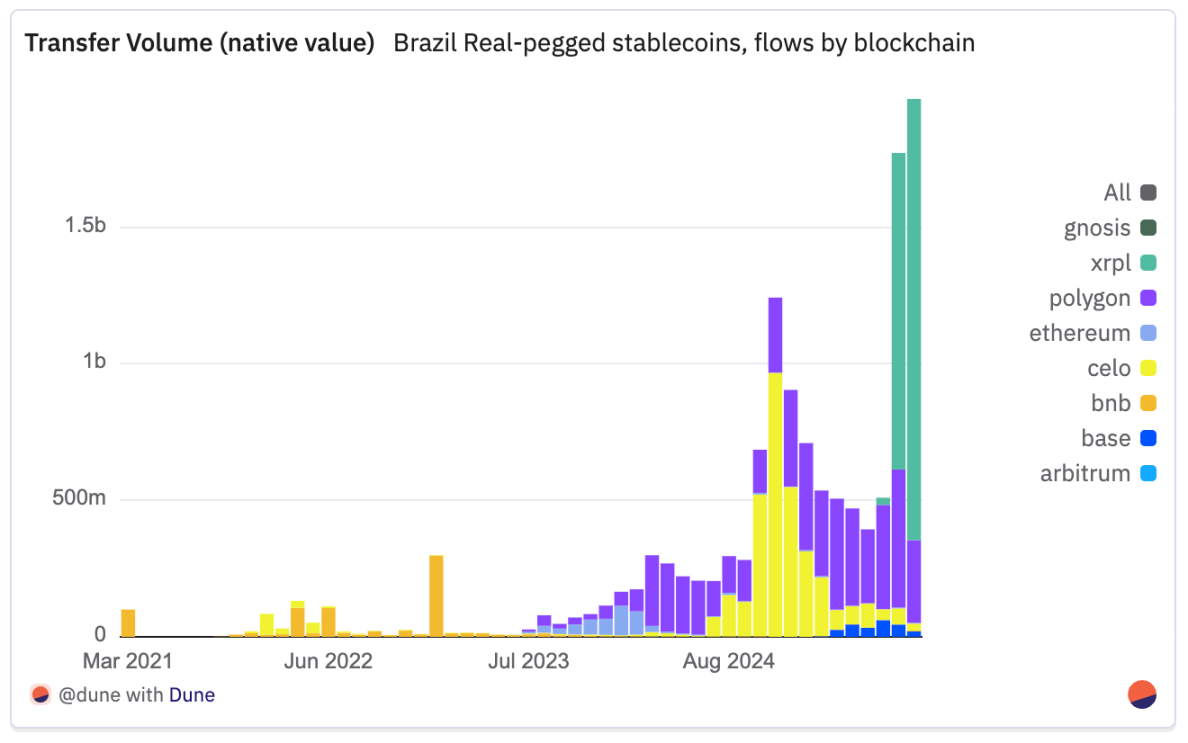

Brazil is the best case for this trend, with significant year-on-year growth in stablecoins pegged to the real. From just over 5,000 transfers in 2021, the number increased to over 1.4 million by 2024, maintaining over 1.2 million in 2025 to date, representing a more than 230-fold increase over four years. The number of independent senders has followed a similar trajectory, growing from fewer than 800 in 2021 to over 90,000 in 2025, an 11-fold increase since 2023 alone. The native transfer volume increased from about 110 million reais (approximately $2.09 million at the time of writing) in 2021 to nearly 5 billion reais (approximately $900 million) by July 2025, almost matching the total for all of 2024. Including data from August, 2025 has already surpassed 2024. What began as a marginal experiment has rapidly evolved into a core pillar of Brazil's on-chain economy, with transactions, users, and transfer values all experiencing several-fold growth within just a few years.

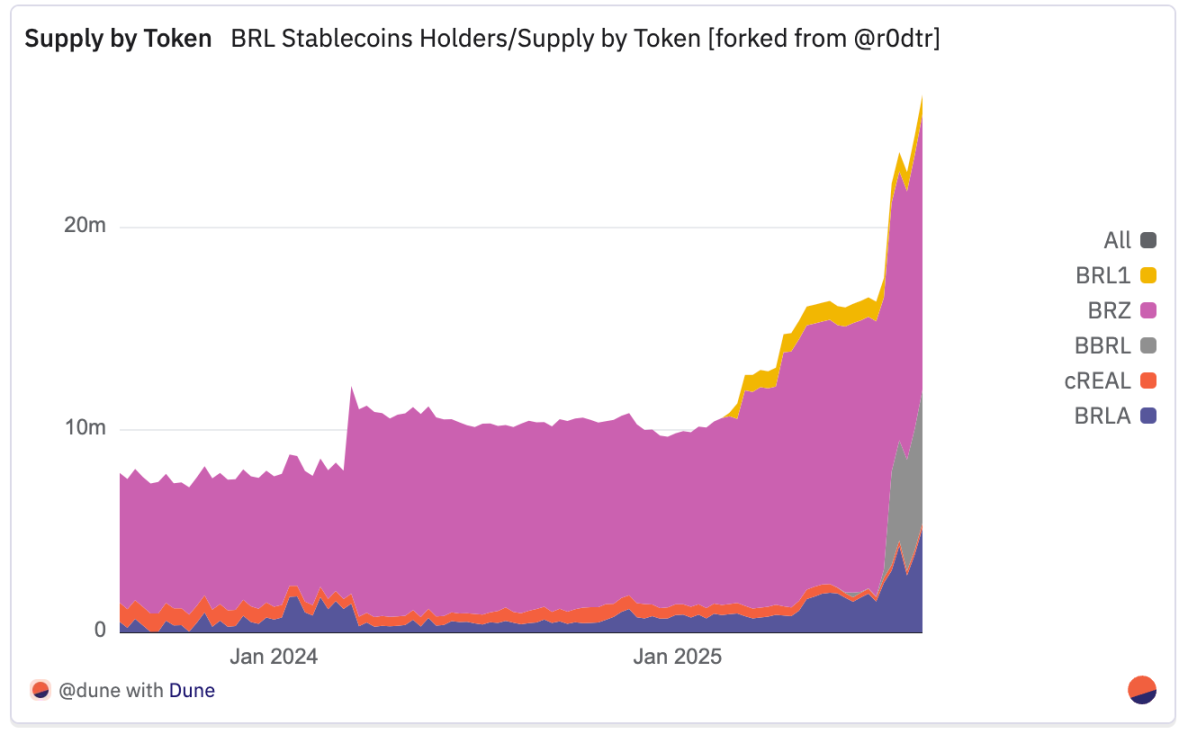

As of June 2025, five different real-pegged stablecoins are actively traded, reducing concentration and indicating a maturing ecosystem. The BRZ issued by Transfero is a blockchain financial solution company providing infrastructure for Latin American banks, fintechs, and payment providers; cREAL, issued on the Celo blockchain, adopts a mobile-first DeFi integration approach; BRLA, launched by BRLA Digital/Avenia, focuses on compliant fiat-crypto bridges; BRL1, launched by an alliance of Mercado Bitcoin, Bitso, and Foxbit, aims to establish industry standards; and BBRL, launched by Braza Group, targets regional commerce and payments.

Despite significant growth, real-pegged stablecoins are still in the early stages, with a circulation of about $23 million.

Moreover, the ecological landscape is evolving rapidly, as highlighted in Iporanga Ventures' latest “Real Stablecoin Report,” where there is currently no clear market leader, but in-depth project data reveals leaders in different fields:

BRLA: Leading in the number of independent senders, showing the broadest retail coverage.

cREAL: Dominating in the number of transfers, reflecting its early appeal in the retail and small payment sectors.

In terms of native transfer volume, BRZ was a clear leader until mid-2024, while cREAL surged to the top in the second half of that year. At the beginning of 2025, Celo's trading volume leadership receded, while BRLA steadily grew. Then, in July 2025, BBRL achieved a significant breakthrough with its launch on XRPL, accounting for about 65% of all native transfer volumes—despite having relatively few active senders, this surge was closely related to its launch on that network.

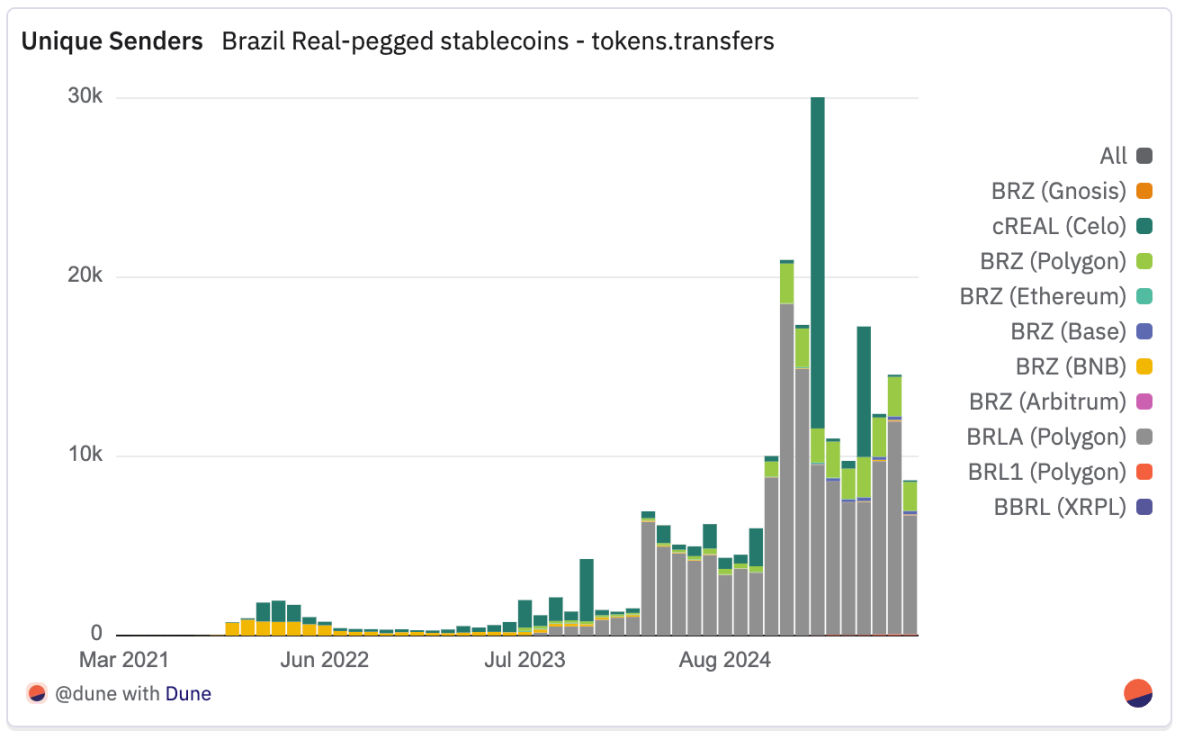

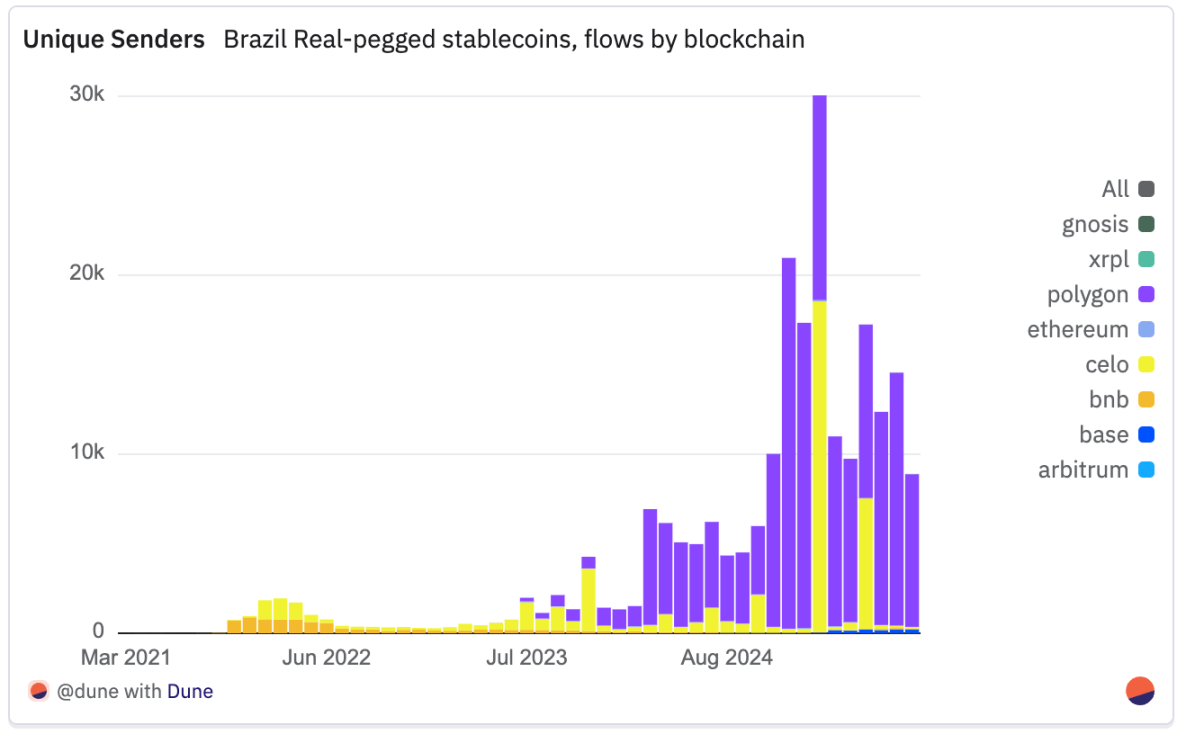

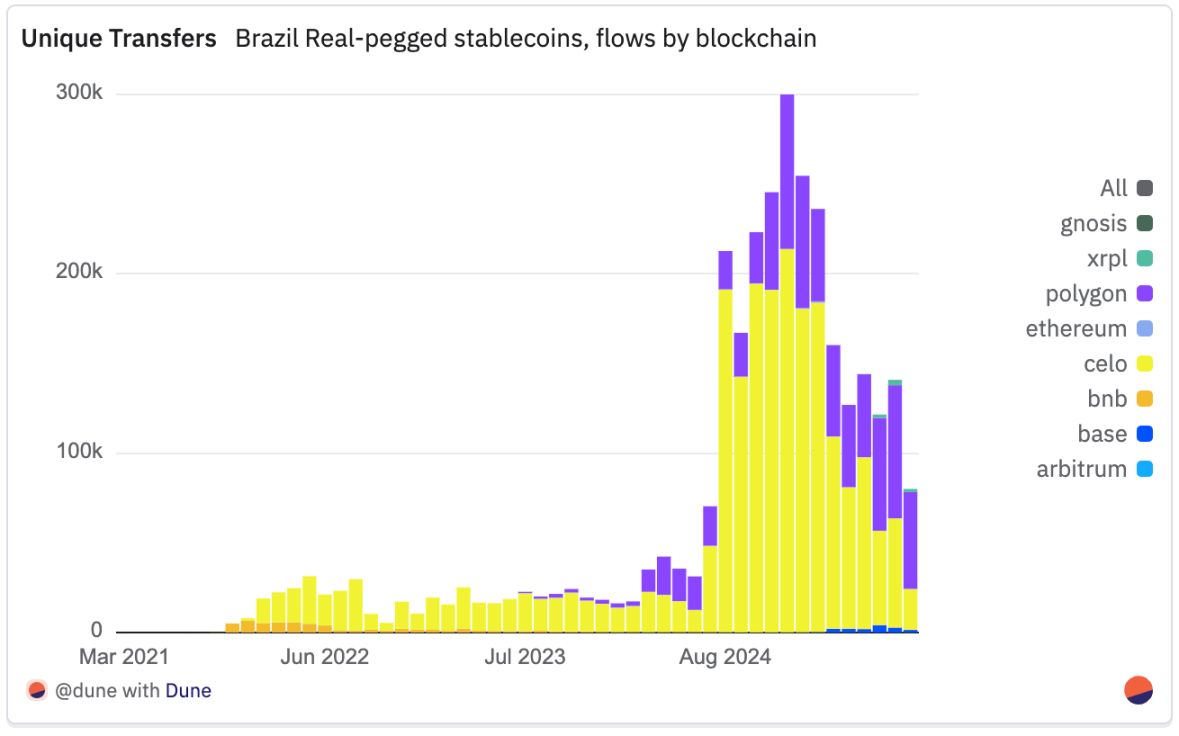

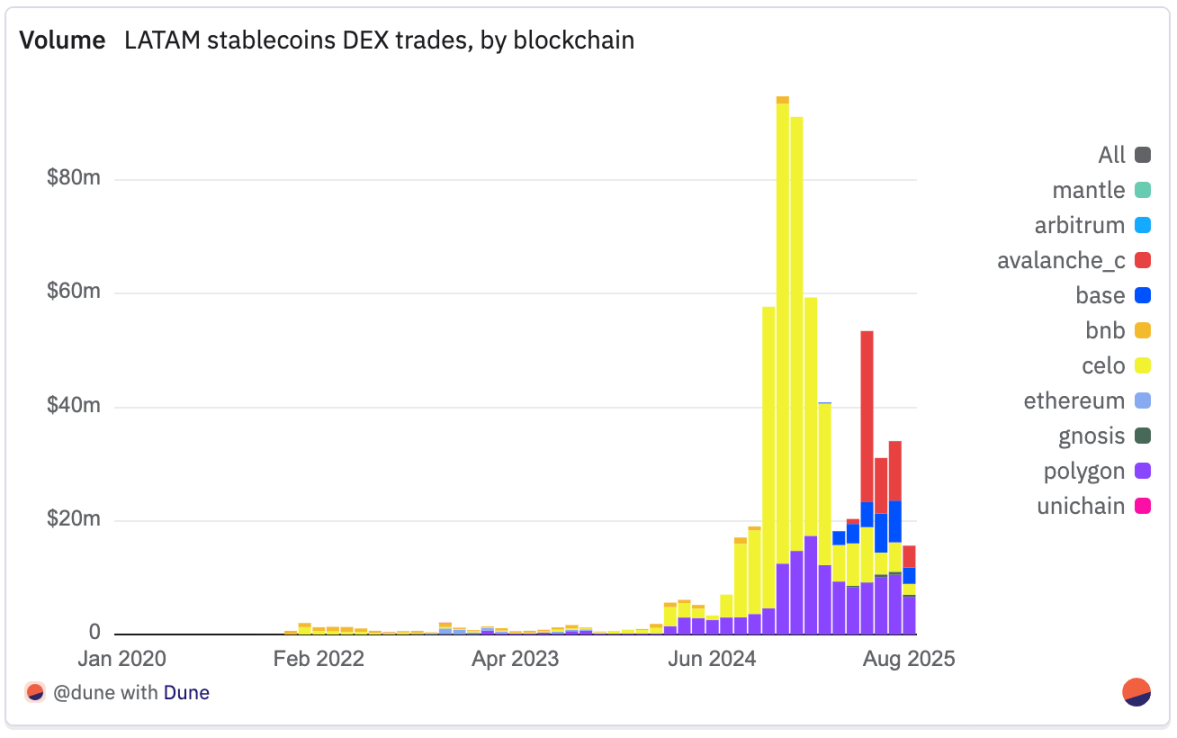

Unlike dollar-pegged stablecoins (whose supply and transfers are mainly concentrated on the Ethereum mainnet), real-pegged stablecoins are primarily active on Layer 2 and other alternative chains. Polygon is the main channel, leading in both native transaction volume and active users; by July 2025, there were about 74,000 transfers on Polygon involving 14,000 independent users, with monthly transaction volume reaching a record of 500 million reais.

Celo ranks second, maintaining a historical lead in the number of transfers, with cREAL's early appeal in the retail and small payment sectors driving transfer counts to a peak of 213,000 in December 2024. In 2025, despite a decrease in independent senders, Celo's trading volume remained substantial, reflecting significant repeat transaction flows from merchants, aggregators, and vaults.

XRPL is a notable newcomer, experiencing a surge with the launch of BBRL in July 2025: transfer counts increased from hundreds in May to about 3,000 in July, with native transaction volume soaring to approximately 1.16 billion reais, marking the formation of an emerging high-value channel.

Base showed steady growth in 2025, peaking in June; meanwhile, Binance Smart Chain remains small in scale after a significant drop in transfer counts and senders in 2022. The Ethereum mainnet has limited utility, used only occasionally for large, low-frequency transfers, although BRZ briefly dominated activity on that network from late 2023 to early 2024.

In addition to the raw data, Iporanga Ventures' report indicates that adoption is driven by practical high-value use cases. B2B payments lead, with businesses paying overseas suppliers or employees and settling locally via PIX; inbound capital flows see dollars exchanged for real stablecoins for domestic payments. They are becoming key infrastructure in Brazil's tokenized asset ecosystem, enabling on-chain settlements without bank custody. In the gig economy and among SMEs, stablecoins support payments, hedging, and capital protection, with merchant integrations like CloudWalk's BRLC and Mercado Pago's dollar stablecoin expanding mainstream applications.

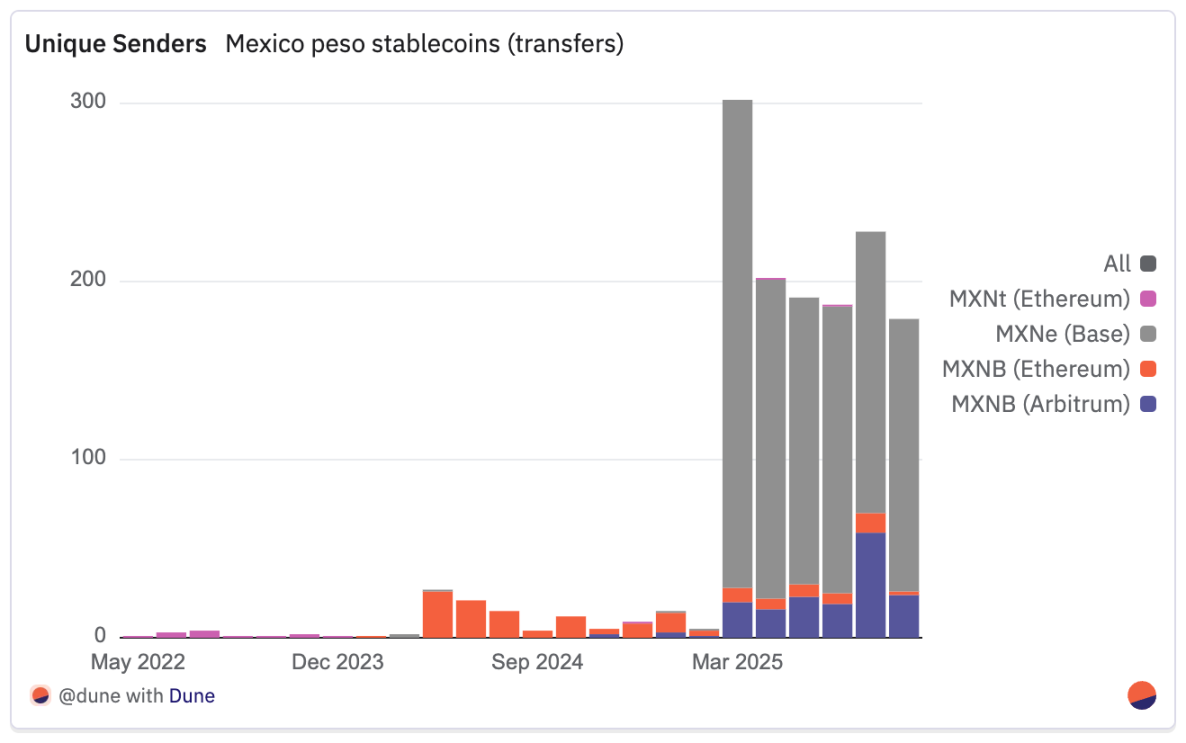

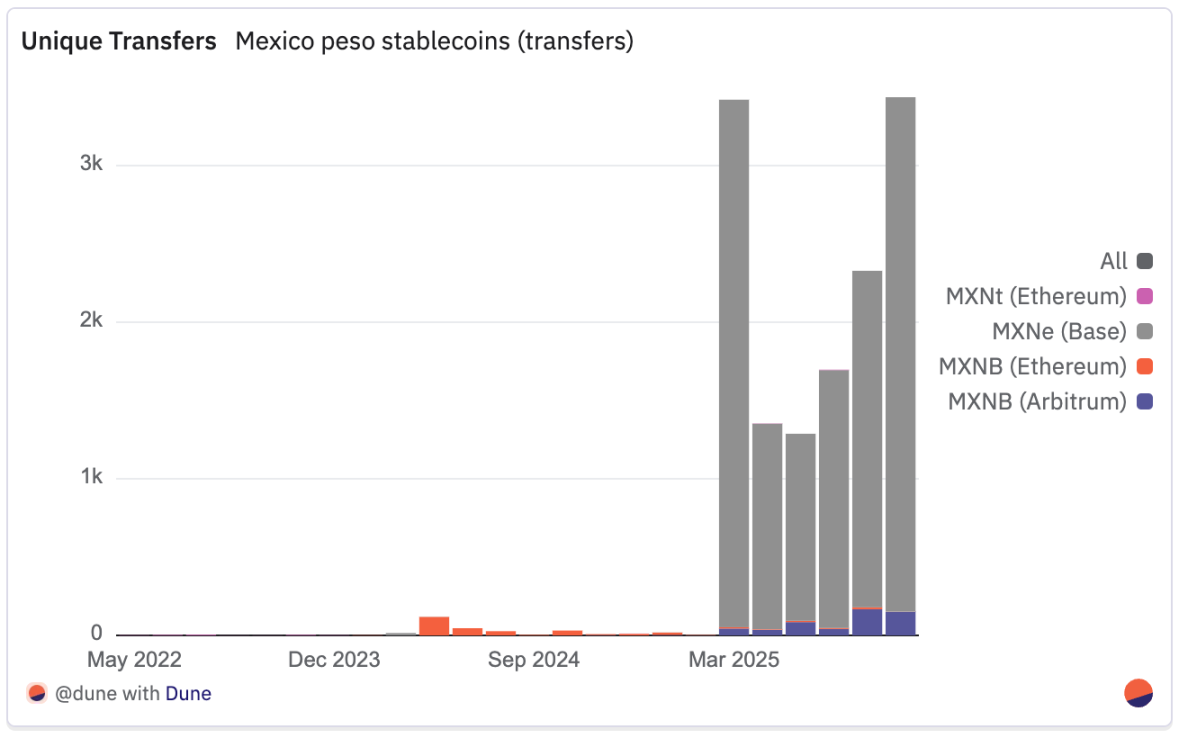

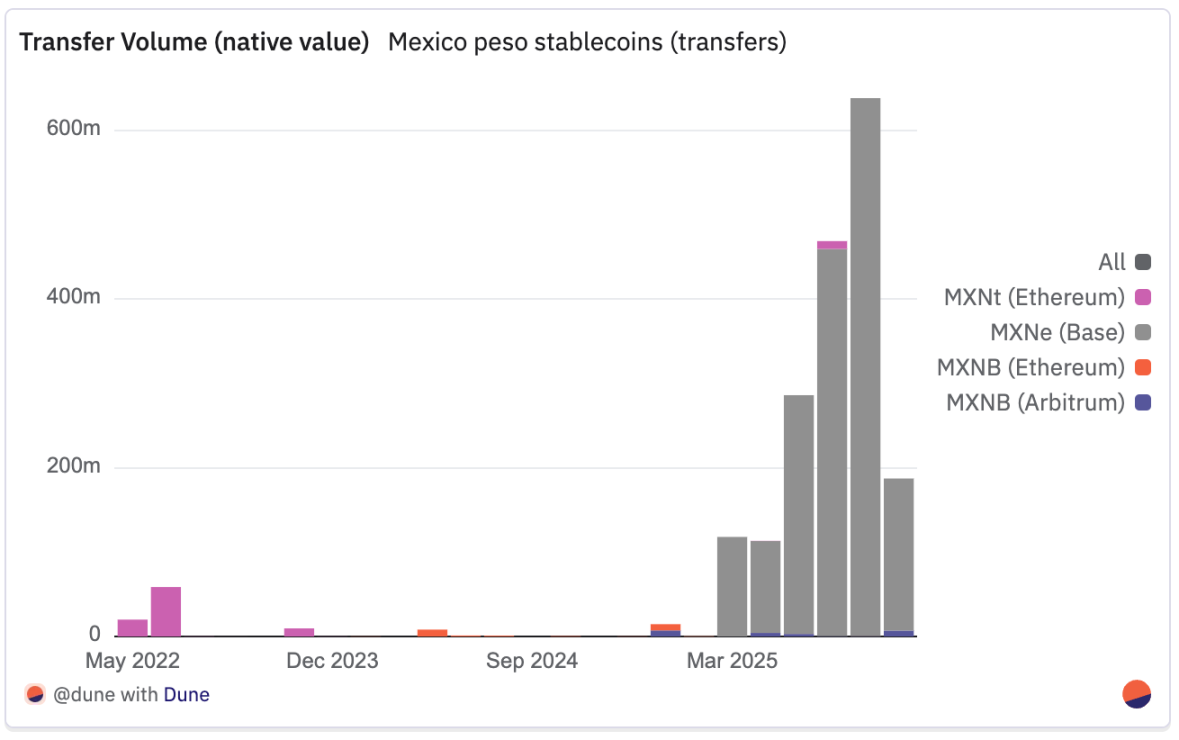

While Brazil has the most diverse and mature local currency stablecoin ecosystem, Mexico's peso-pegged market is forming around two main projects—MXNB from Juno/Bitso and MXNe from Brale, each taking different paths. Notably, MXNB has evolved from sporadic issuance at the end of 2024 to a more stable and widespread application model in 2025.

The growth of MXNB in 2025 marks a clear shift towards everyday use. In July 2025, MXNB saw 179 transfers involving 70 independent senders, a significant increase from 46 transfers and 21 senders a year earlier (a year-on-year increase of 339% and 290%, respectively).

Although the trading volume peaked at 14.5 million Mexican pesos (approximately $750,000 at the time of writing) in January 2025 with relatively few transactions, the 480,000 Mexican pesos (about $25,000) in July came from more small payments. The average transaction size dropped from about 28,700 Mexican pesos in July 2024 to 3,600 Mexican pesos. This shift coincided with a decisive migration to Arbitrum: approximately 99% of transfers were conducted on Ethereum in 2024, while since the second quarter of 2025, about 94% of transfers have shifted to Arbitrum, making the low-cost Layer 2 the default choice.

MXNe from Brale, on the other hand, has taken the opposite path, becoming the largest trading volume peso stablecoin while operating solely on Base.

Activity peaked in March 2025 with 3,367 transfers involving 274 senders, but even as transaction counts decreased, trading volume continued to rise—reaching a record of approximately 637.7 million Mexican pesos in July 2025, from 2,148 transfers and 158 senders. This brought the average transaction size close to 297,000 Mexican pesos, indicating high-value transactions and potential institutional usage.

The contrast is stark: MXNB now dominates small retail payments, while MXNe seems focused on large settlements. Compared to Brazil's more diverse real stablecoin landscape, the Mexican market remains concentrated around these two issuers and fewer chains, although this has not hindered liquidity growth. Since mid-2025, peso trading pairs have rapidly entered the top ranks of decentralized exchange trading volumes, marking a maturation of market structure.

Decentralized Exchange Liquidity and Trading Patterns

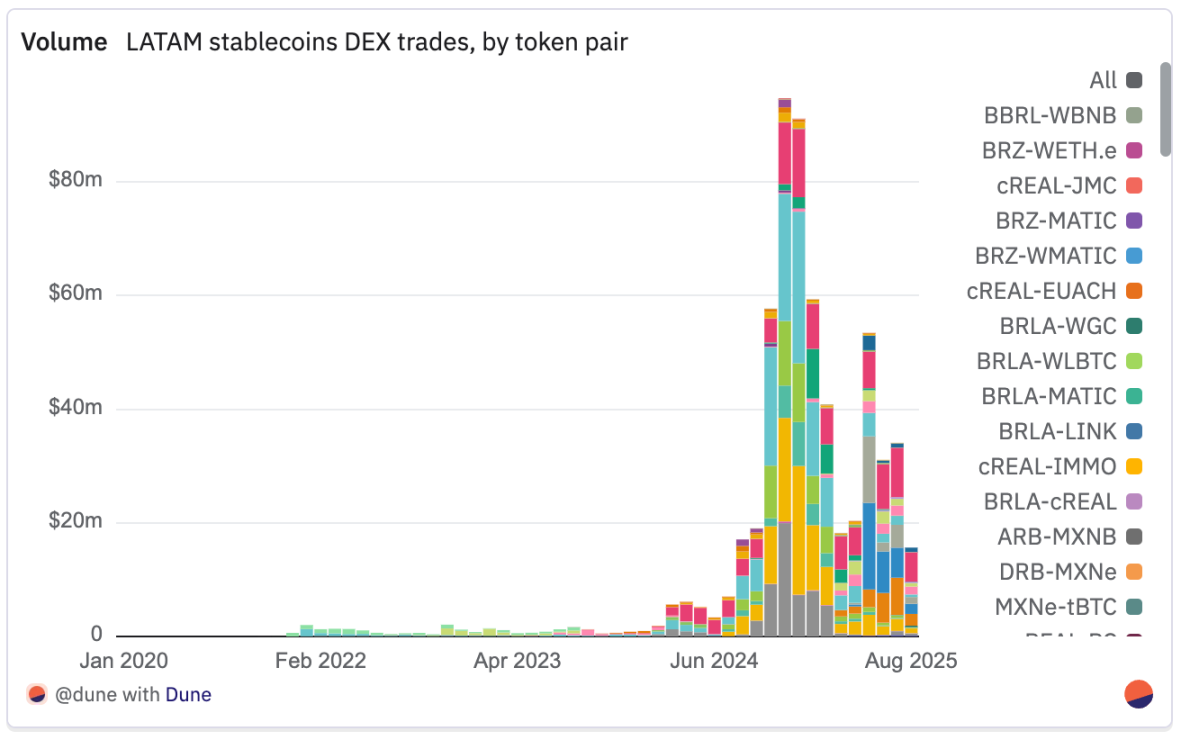

The rise of real and peso-pegged stablecoins in Latin America extends beyond payments to meaningful liquidity in decentralized exchanges (DEX), establishing on-chain forex channels between local currencies and global stablecoins.

Among assets related to the real, cREAL is the main trading hub. Its largest trading pair, CELO–cREAL, has processed approximately $126 million in trading volume, supported by the deep liquidity of the Celo native decentralized exchange ecosystem. cREAL also anchors major cross-stablecoin markets—cREAL–USDT ($87.7 million), cREAL–cUSD ($59.1 million), and non-dollar trading pairs like cEUR–cREAL ($48.6 million) and cKES–cREAL ($24.9 million), highlighting its dual role as a channel for real deposits and a base currency for multi-currency exchanges. However, after peaking at $80 million in November 2024 (accounting for 85% of the tracked stablecoin total that month), cREAL's monthly decentralized exchange trading volume has steadily declined, dropping to $5 million in July 2025, returning to levels seen in July 2024.

BRLA is becoming the main dollar channel, with BRLA–USDC ($97.5 million) and BRLA–USDT ($21.3 million) as its primary trading pairs. Since March 2025, BRLA–USDC has consistently ranked as the top dollar-denominated decentralized exchange trading pair in the dataset, briefly surpassed only by the MXNB trading pair in May 2025. Although BRLA has never reached the peak trading volume of cREAL, in July 2025, BRLA trading pairs moved $9 million, nearly double the trading volume of cREAL that month, and three times BRLA's own trading volume in July 2024.

BRZ remains stable and widely integrated, with liquidity distributed across trading pairs like BRZ–USDC ($15.1 million), BRZ–USDT ($14.7 million), and BRZ–BUSD (approximately $9.1 million). It has the broadest range of trading pairs among real stablecoins, and although its trading volume is lower than that of cREAL or BRLA, it has been steadily growing, from $26,000 in July 2024 to $3 million in July 2025, peaking at $4.77 million in April.

As for peso-pegged stablecoins, MXNB's largest trading pairs—MXNB–WAVAX ($29.7 million) and MXNB–USDC ($18.6 million)—surged during the high-value trading and liquidity inflow period in May 2025. Since then, peso trading pairs have remained strong, with three Mexican peso trading pairs still ranking among the top volumes in local stablecoin decentralized exchanges, indicating that this growth is not coincidental.

MXNe operates solely on Base, primarily focusing on the MXNe–USDC (approximately $18.3 million) trading pair. Its decentralized exchange activity has steadily grown from $1.13 million in March to $6.6 million in July 2025, consistent with Base's push to integrate local stablecoins with deep dollar liquidity pools. Interestingly, although MXNe leads in transfer volume over MXNB, MXNB has higher decentralized exchange trading volume, indicating that MXNe focuses on high-value transfers and dollar integration, while MXNB concentrates on active on-chain trading.

The decentralized exchange trading volumes of BRL1 and BBRL remain limited, with minimal cross-currency stablecoin activity, and only three trading pairs show significant activity, the largest of which (BRLA–BRZ) peaked at approximately $400,000 in April 2025.

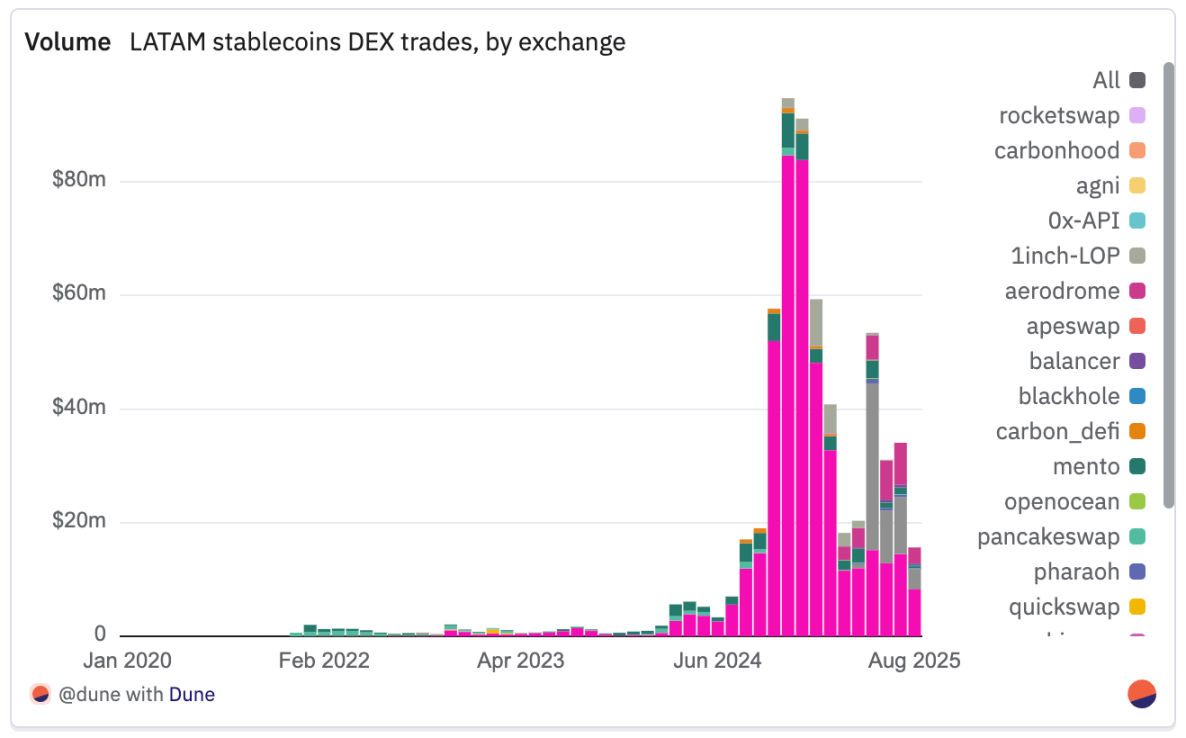

Transaction volumes are concentrated on a few platforms, each associated with specific local stablecoin ecosystems. Uniswap remains the clear liquidity giant, with a total trading volume of $426 million, playing a central role in the real and peso-pegged stablecoin markets on Ethereum and Layer 2. Chain-native decentralized exchanges hold decisive shares of their respective stablecoins: Trader Joe ($52.8 million) and PancakeSwap ($13.3 million) capture most of the BRZ liquidity on Avalanche and Binance Smart Chain, while Mento ($50.8 million) serves as the dedicated platform for cREAL trading within the Celo ecosystem. The 1inch Limit Order Protocol operates differently, functioning more like an aggregator settlement layer rather than a liquidity host, often appearing in large one-off exchanges rather than maintaining deep liquidity pools.

One of the most significant developments in 2025 is the rise of Aerodrome, with a cumulative trading volume of $25.8 million—almost entirely driven by MXNe–USDC trades since the second quarter. As a native stablecoin anchor on the Base chain, its position is similar to that of Mento in the Celo ecosystem. Smaller but noteworthy platforms like Carbon DeFi ($4.8 million), Pharaoh ($1.95 million), and Balancer (approximately $1.8 million) cater to decentralized or niche cross-asset liquidity pools. Overall, the absolute value of local stablecoin liquidity is expanding, increasingly anchored to chain-native decentralized exchange infrastructure, with Aerodrome's rapid rise in 2025 being the most evident example.

Liquidity patterns remain closely tied to the parent chains and dominant decentralized exchanges of each stablecoin. Celo leads with a total trading volume of $363 million, almost entirely driven by cREAL–cUSD/USDC trades on Mento, consistently ranking first in dollar-denominated trading volume from July 2024 to February 2025. Polygon follows closely with $136 million, providing diversified real-pegged liquidity—particularly BRLA and BRZ—distributed across Uniswap and QuickSwap, reflecting its dual role in stablecoin transfers and decentralized finance/payment integration. Avalanche ranks third with approximately $54.8 million, driven by a surge in MXNB–WAVAX trades on Trader Joe (the largest decentralized exchange on that chain) in May 2025, while Uniswap, Pharaoh, and the 1inch Limit Order Protocol also contributed liquidity to the real and Mexican peso markets. Base follows with about $26.2 million, almost entirely driven by MXNe–USDC trades on Aerodrome, aligning with Base's initiatives to promote local stablecoins in 2025.

The broader conclusion is clear: local stablecoin decentralized exchange liquidity is ecosystem-anchored, with each major chain pairing its flagship assets with a few dominant platforms. The breakthrough growth cases in 2025—MXNB trading on Trader Joe on Avalanche and MXNe trading on Aerodrome on Base—indicate that when local stablecoins hold strategic importance, blockchain adoption and exchange dominance can mutually reinforce each other.

Beyond Brazil and Mexico, several other Latin American countries are also experimenting with local currency stablecoins, although most are still in early growth or limited pilot stages. In Argentina, extreme currency volatility has hindered the lasting appeal of tokens pegged to the Argentine peso, such as Transfero's ARZ and Num Finance's nARS. Colombia has seen multiple stablecoins emerge, including nCOP (Num Finance), cCOP (Celo/Mento), COPM (Minteo), and COPW (Bancolombia), aimed at serving remittances and domestic payments, but adoption rates remain limited. Chile's CLPD on Base and Peru's nPEN (Num Finance) and sPEN (Anclap on Stellar) are similarly niche, with usage primarily limited to pilot projects and specific payment channels. Although these projects indicate growing regional interest, their trading volumes remain limited, highlighting the decisive role of local conditions—especially currency stability and regulatory clarity—in driving adoption rates.

Key Takeaways

Stablecoins are the backbone of the Latin American chain economy. Stablecoins pegged to the dollar and local currencies have replaced volatile assets as the core of cryptocurrency usage, achieving sustained double and triple-digit growth.

- In July 2025, USDT and USDC accounted for over 90% of all exchange transfer volumes, up from about 60% in 2022.

- Brazil leads in the number of active local stablecoins and overall activity. As of July 2025, real stablecoins have processed $906 million, nearly matching the total for all of 2024 ($910 million), with an annualized projection of around $1.5 billion.

- In Mexico, peso-pegged stablecoins (MXNB + MXNe) reached approximately $34 million in July 2025, up from just 1 million Mexican pesos (about $53,000) in July 2024, a year-on-year increase of about 638 times.

- Major blockchain channels for local stablecoins: Polygon (BRLA, BRZ), Celo (cREAL), Base (MXNe), and Arbitrum (MXNB).

Deposit and Withdrawal Channels

Deposit and withdrawal channels (including centralized and peer-to-peer models) are key connecting links between the Latin American crypto economy and traditional finance. In countries like Argentina, Brazil, and Mexico, users often convert their salaries into stablecoins on payday, using cryptocurrencies not for speculation but as a buffer against volatility.

In Brazil, the government-supported Pix system plays a crucial role as a fiat-to-crypto deposit channel, providing instant low-cost settlements. In Argentina, despite the continuous development of formal platforms, informal currency exchange networks known as "cuevas" remain the primary withdrawal channels due to capital controls and economic uncertainty.

Behavioral data from Bitso (2024) shows that cryptocurrency usage spikes on specific days and times of the week, aligning with payroll cycles. This behavioral pattern reinforces the view of cryptocurrencies as practical financial tools for preserving value in turbulent environments.

Emerging players like PayDece, zkP2P, and Takenos are innovating at the infrastructure level, building non-custodial, mobile-first solutions aimed at serving underbanked populations and enhancing financial sovereignty. Their emergence marks a shift towards more decentralized, censorship-resistant channels.

For the region's growing population of freelancers and remote workers, crypto withdrawal channels are becoming an essential part of the ecosystem, helping them receive international payments in cryptocurrency (especially stablecoins), bypassing unstable local currencies and limited traditional banking services (Frontera, 2024).

ZKP2P

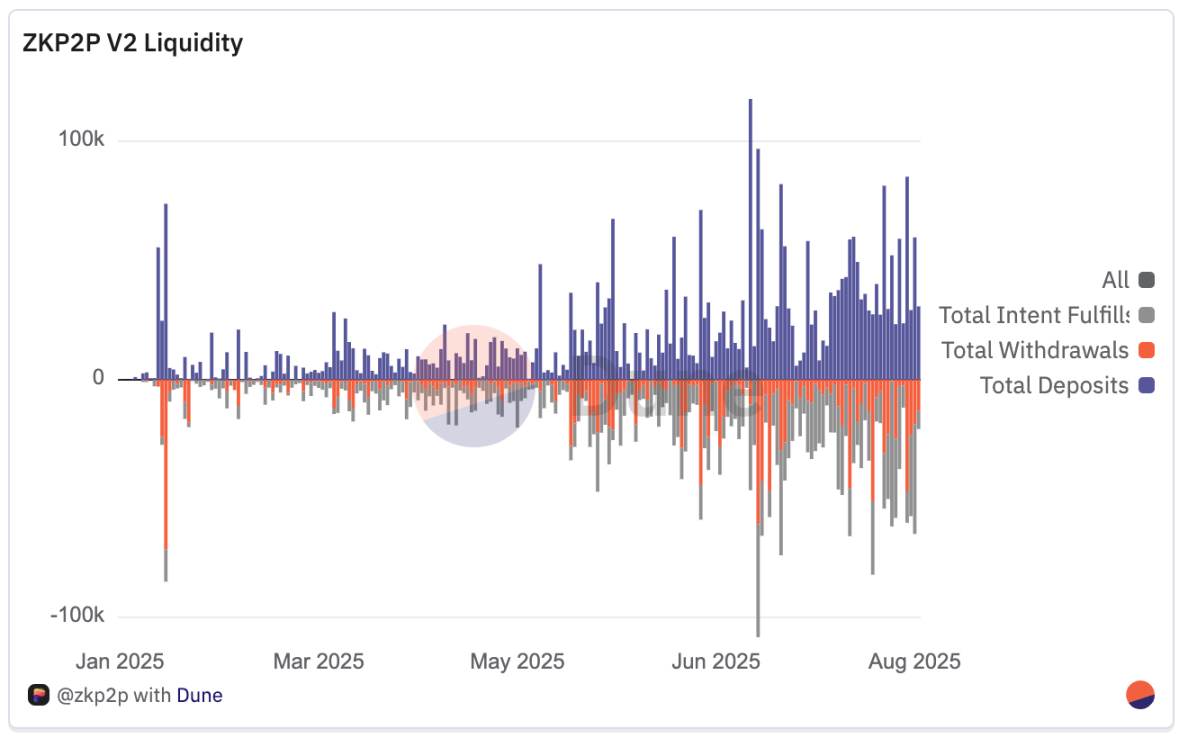

ZKP2P is a decentralized, trust-minimized peer-to-peer deposit and withdrawal protocol that uses advanced cryptographic proofs like zkEmail and zkTLS to enable direct exchanges between fiat and cryptocurrencies without intermediaries, fees, or additional verification. Launched at the end of 2023 and upgraded to V2 in 2024, it currently supports multi-chain exchanges (Ethereum, Solana, Base, Polygon) and various tokens, from USDC and ETH to popular local tokens and even meme coins.

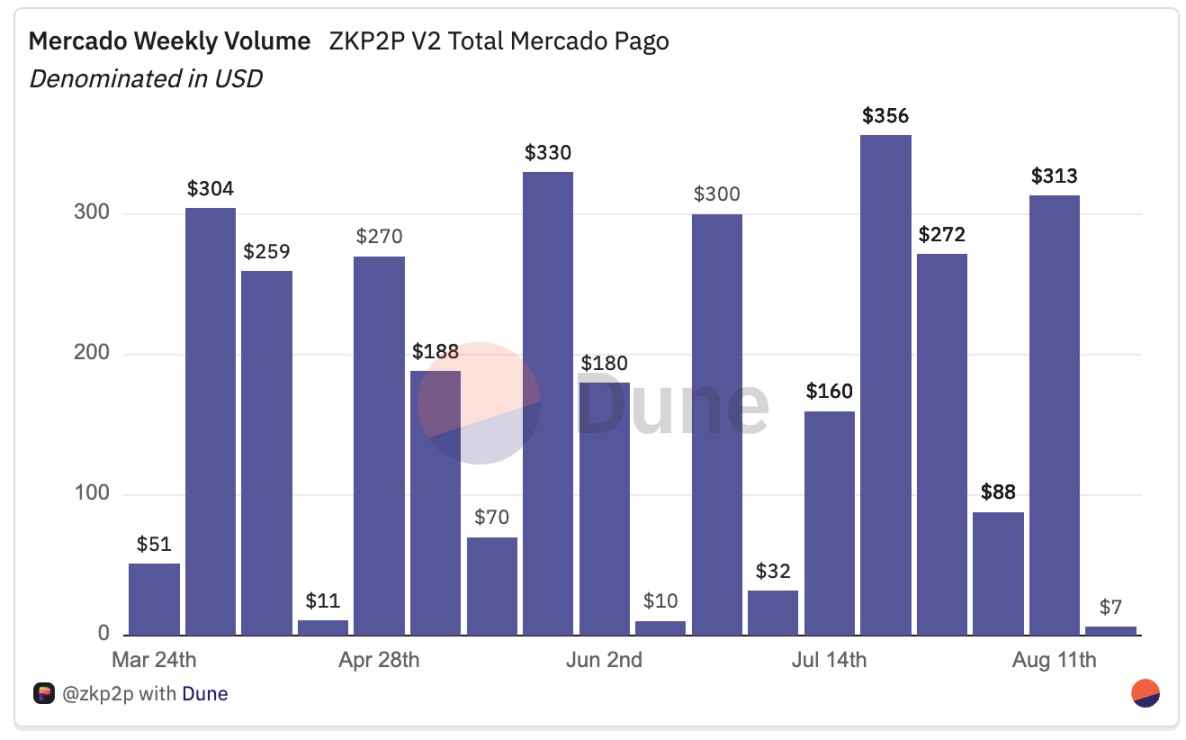

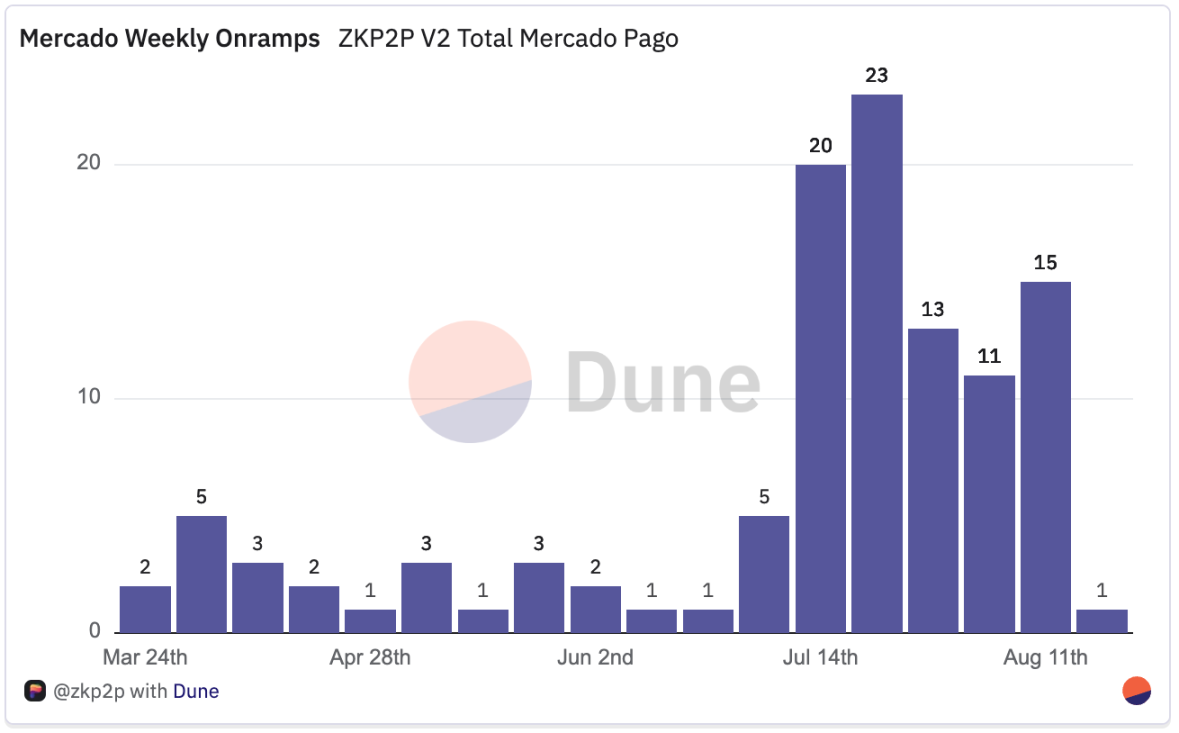

In Argentina, ZKP2P integrates with Mercado Pago, allowing for near-instant exchanges between Argentine pesos (ARS) and USDC.

Since its launch, the Argentina-focused channel has processed over 100 deposit transactions, totaling more than $3,000 USDC, with an average transaction size of $30, a minimum of just $1, and a maximum of $356.

By peer-to-peer standards, settlement speeds are relatively fast, with a median settlement time of about 30 minutes over the past week.

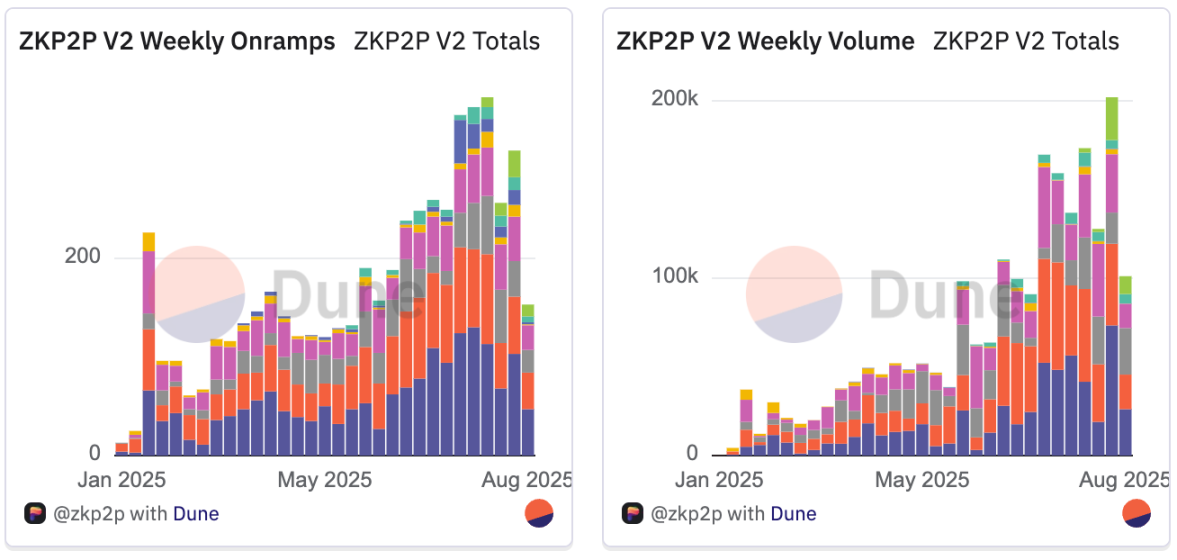

Globally, ZKP2P has broader appeal, completing 4,861 deposits in V2, processing over $1.9 million (a total of $2.08 million for V1 and V2 combined).

The liquidity of all payment channels currently stands at $114,000, with major channels including Revolut (total trading volume of $470,000), Wise ($390,000), Cash App ($327,000), and Venmo ($559,000). The global average deposit and withdrawal transaction size is $385, more than 12 times the Latin American average, highlighting the growth potential as the region's scale aligns with global patterns.

Although still in the early stages in Latin America, ZKP2P is steadily gaining traction, especially in low-value, high-frequency use cases. Upcoming integrations with local channels like Brazil's PIX may expand its role as a permissionless bridge between local currencies and cryptocurrencies. A notable case is the integration of Daimo Pay × ZKP2P × World Account, which converts Worldcoin's WLD to USDC, cross-chain to Base, and lists on ZKP2P, completing settlement directly in the World App in about 15 minutes. This model offers faster, cheaper settlements, demonstrating how cross-chain, non-custodial withdrawal channels can transform cryptocurrencies from speculative assets into consumable income.

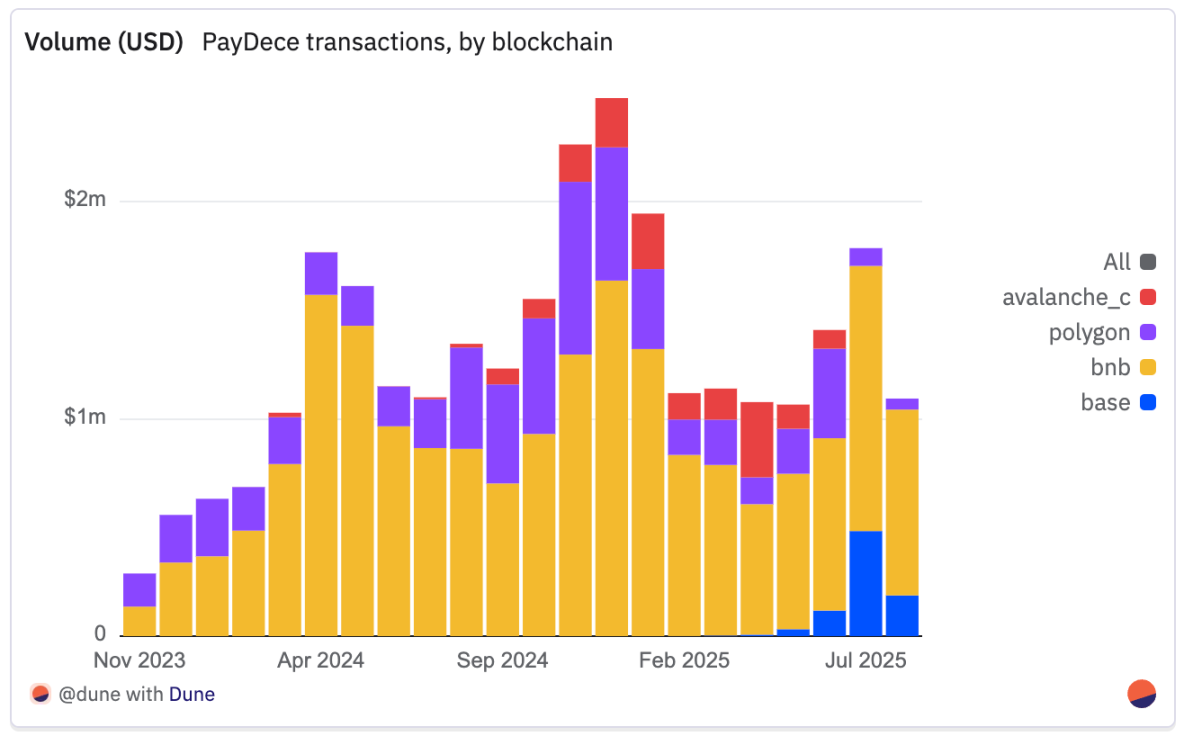

PayDece

PayDece is a peer-to-peer cryptocurrency deposit platform built on the core principles of Web3 (decentralization, privacy, and self-custody). It enables secure, anonymous transactions through smart contracts without the need for centralized intermediaries or mandatory identity verification (KYC).

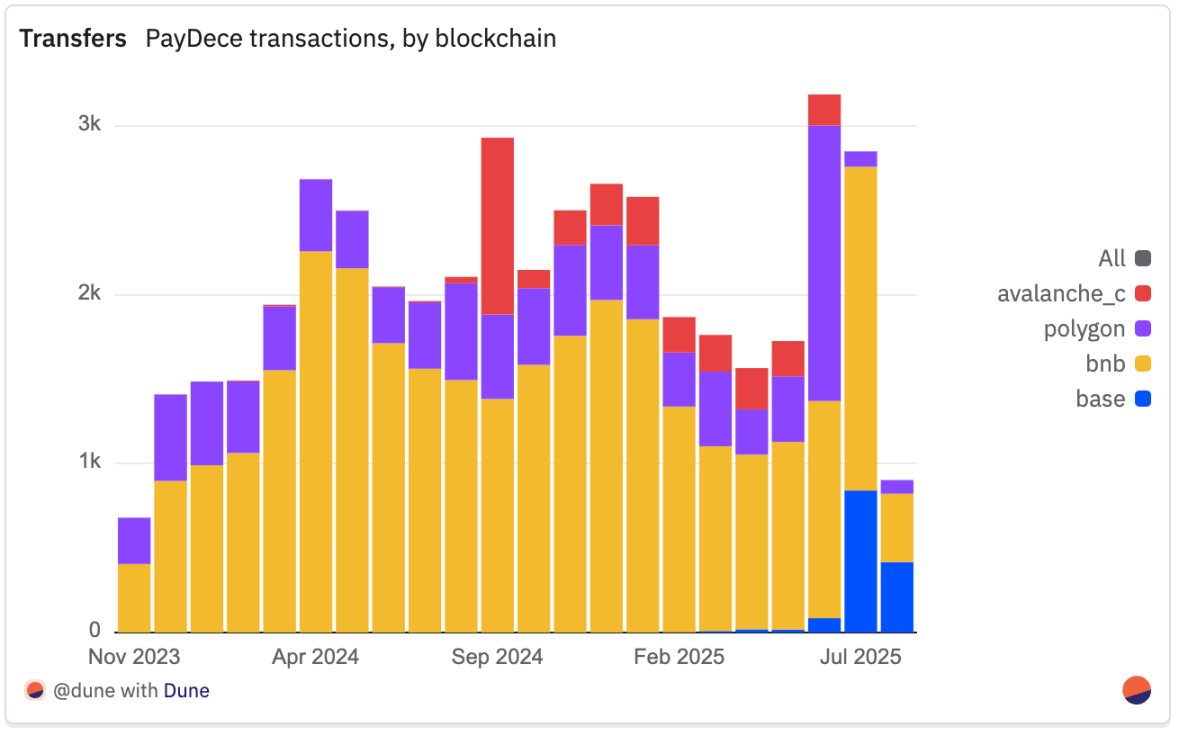

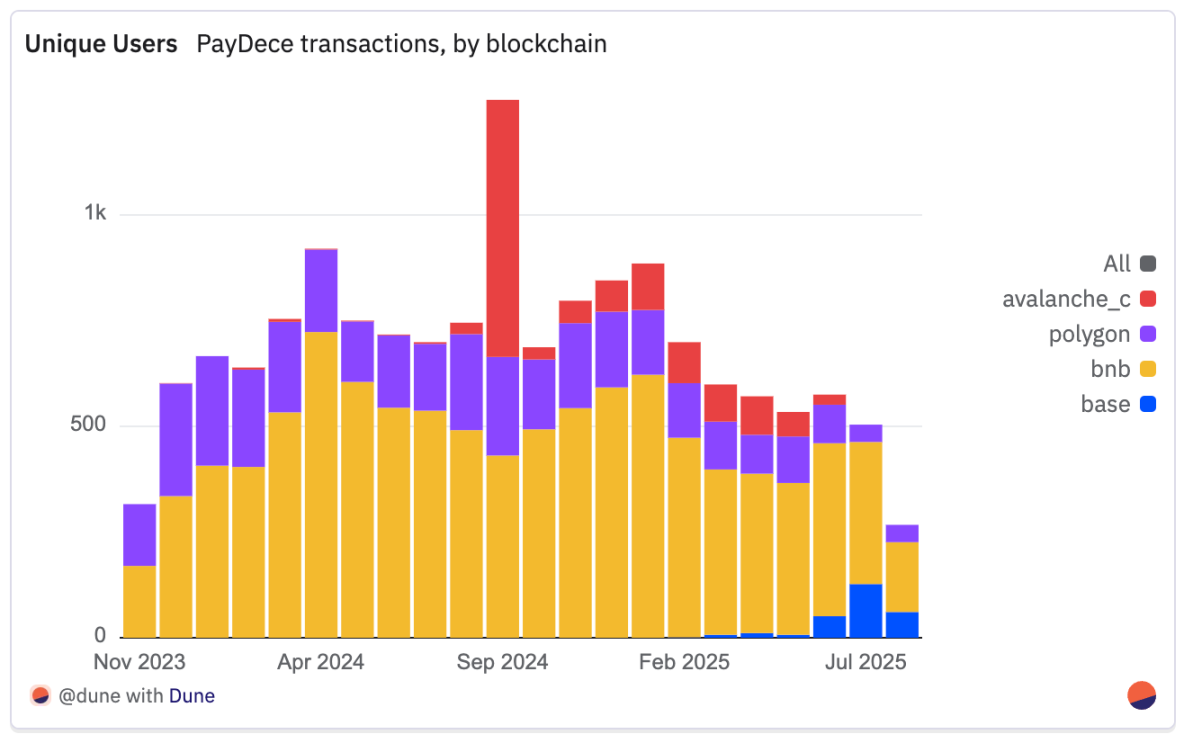

Across all supported chains, PayDece has processed over 44,000 transfers involving approximately 15,000 independent users. Activity is primarily concentrated on stablecoins—USDT ($19.17 million) and USDC ($7.74 million), with Binance Smart Chain leading blockchain usage at $19.5 million, followed by Polygon ($6.3 million), Avalanche ($1.68 million), and Base ($830,000).

Since the end of 2023, PayDece's activity has shown strong early growth, with monthly trading volume increasing from less than $300,000 in November 2023 to $1.79 million in July 2025, having previously surpassed $2.4 million at the end of 2024. The number of transfers and users has grown in tandem, with significant peaks in April 2024, November-December, and June-July 2025. Trading volumes remain well above early adoption levels, indicating a stable repeat user base and ongoing transaction flow.

With a privacy-first design, multi-chain support, and growing on-chain liquidity, PayDece is becoming a major decentralized alternative for Latin American users seeking censorship-resistant, self-custody deposit and withdrawal solutions.

Capa

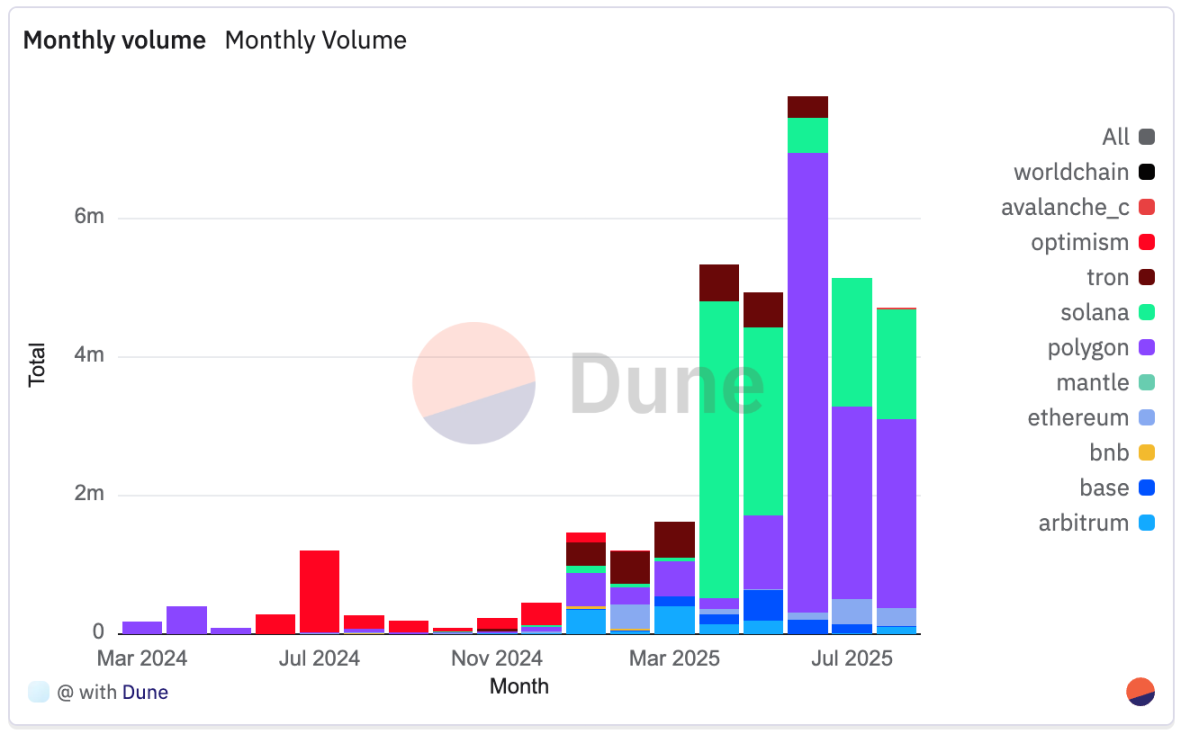

Capa is a financial infrastructure provider focused on simplifying cryptocurrency access and utility in Latin America. Its API allows fintech companies, enterprises, and payment applications to embed stablecoin channels for fiat-crypto exchanges and directly support cross-border transactions within their services. By emphasizing liquidity, compliance, and network diversity, Capa addresses the fragmentation of payment systems in Latin America and the high costs of cross-border transfers.

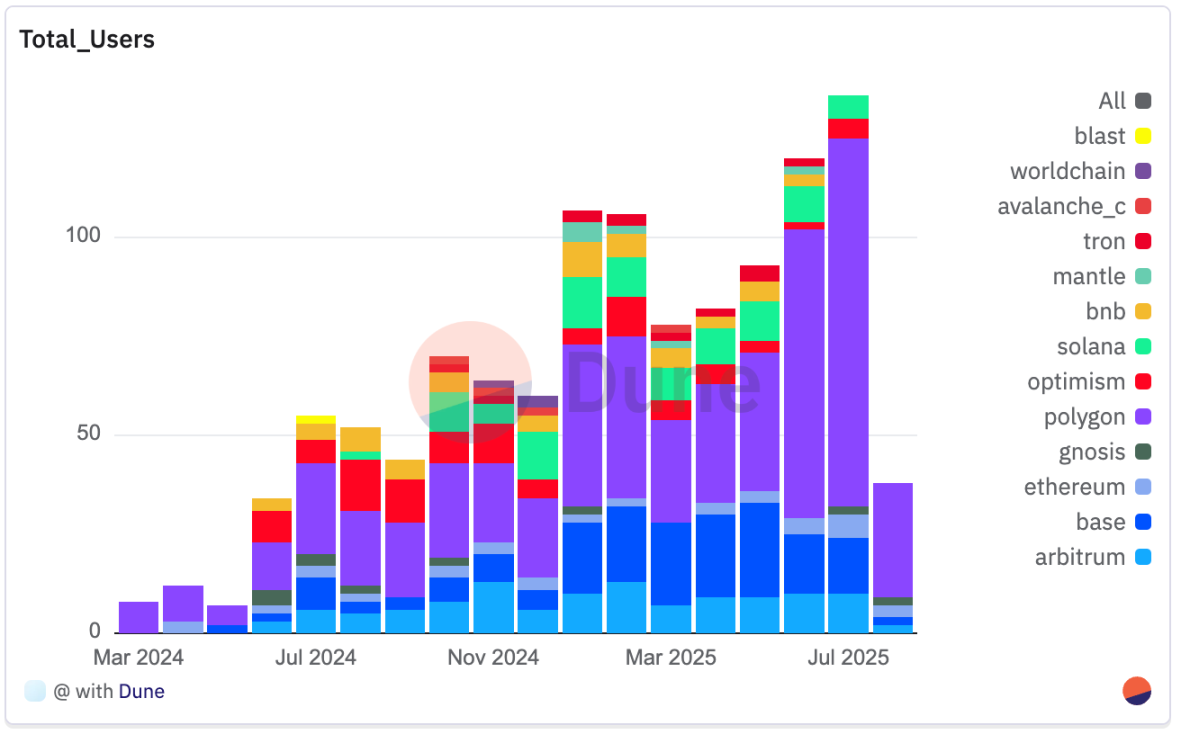

Since its launch, Capa has processed a total trading volume of $29.9 million across 5,501 transactions. The platform operates across multiple blockchains, with Polygon leading at $14.1 million, followed by Solana ($6.95 million), Tron ($2.73 million), Optimism ($2.52 million), Arbitrum ($1.26 million), Base ($1.11 million), and Ethereum ($1.06 million), with a small amount of funds flowing on Binance Smart Chain as well.

Capa's user base (over 900 independent addresses) is increasingly concentrated on low-cost, fast-settlement chains. As of July 2025, 68% of users transact via Polygon, followed by Base (10%), Arbitrum (7%), Ethereum (4%), and Solana (4%). This contrasts sharply with December 2024, when Solana accounted for 20% and Polygon only 33%.

In terms of transaction direction, Capa has completed 1,173 deposit transactions and 809 withdrawal transactions to date. In 2025, especially in recent months, both types of transactions have seen significant growth.

From July 2024 to July 2025, monthly retail (B2C) deposit amounts increased from an average of $200 to $1,300, while withdrawal amounts rose from $336 to $1,200, reflecting an increase in demand for stablecoin exchanges and withdrawals as the platform integrates with more regional partners.

The growth in monthly trading volume indicates that fintech companies and wallets relying on the Capa API for stablecoin payments and cross-border value transfers are increasingly adopting the service. It supports seamless settlements of USDC and USDT across different networks, reducing friction for B2C and B2B applications.

A recent case highlighting Capa's unique positioning is its role in supporting MXNe (a Mexican peso stablecoin launched on Base and listed on Coinbase Wallet). MXNe is built by Etherfuse, with Brale providing the infrastructure and Capa supplying liquidity, marking a step forward in accessible, locally-focused financial tools. Notably, Capa is currently the only platform offering 1:1 Mexican peso deposits and withdrawals with MXNe, connecting fiat currency with on-chain assets while fully complying with regulatory requirements.

By focusing on both deposits and withdrawals as well as real-time settlements, Capa is becoming a critical infrastructure layer for the Latin American crypto economy. Although less visible to users, it is essential in supporting compliant, efficient, and scalable cryptocurrency integration across the region.

Key Takeaways

Deposit and withdrawal channels are bridging the gap between on-chain economies and local economies. The combination of permissionless protocols and compliant infrastructure makes fiat-crypto conversions in Latin America faster, cheaper, and easier.

- ZKP2P has pioneered a non-custodial, cryptography-based deposit and withdrawal method, enabling near-instant exchanges between stablecoins and local currencies. While global usage is strong (over $1.87 million in V2), adoption in Latin America remains in its early stages (around $3,000), with significant growth potential as integrations like Brazil's PIX are rolled out. A median settlement time of about 41 minutes indicates that frictionless peer-to-peer fiat-crypto exchanges are becoming a viable reality.

- PayDece is emerging as a decentralized stablecoin reuse transfer platform, with a trading volume of $27.8 million and 15,000 users. Since the end of 2023, trading volume has grown sixfold, with monthly throughput stabilizing between $1 million and $2 million, indicating a growing demand for uncensored deposit channels in Latin America and a maturing user base.

- Capa has processed $29.9 million through its deposit and withdrawal and cross-border stablecoin settlement APIs. Its growth on Polygon and Solana highlights its role as a key driver for fintech and B2B applications to expand cross-border in a compliant environment.

Payment Applications

Cryptocurrency-driven payment applications and digital banks are among the most effective distribution channels in Latin America. Exchanges like Lemon, Belo, Buenbit, and Ripio offer physical and digital cards for everyday payments. Platforms like Picnic, BlindPay, and Exa position themselves as crypto-native digital banks by providing dollar-denominated balances, yield features, and stablecoin payments within a single application. Interestingly, the demand for cryptocurrency-driven financial tools continues to grow. According to Lemon's data, downloads of cryptocurrency applications in Latin America doubled year-on-year in the second quarter of 2024, reflecting a rekindled user interest. This resurgence indicates a shift from hype-driven onboarding to demand-driven usage rates (Lemon, 2024).

In Argentina, Lemon Cash's cryptocurrency card allows users to spend stablecoins while paying in pesos, connecting cryptocurrency with real-world utility. Users can even earn Bitcoin cashback, creating an incentive loop that merges saving and spending (Frontera, 2024).

These applications are increasingly being used by unbanked and underbanked populations to manage finances without needing a bank account. In many rural or remote areas, cryptocurrency applications serve as an alternative to traditional finance rather than a supplement.

Picnic

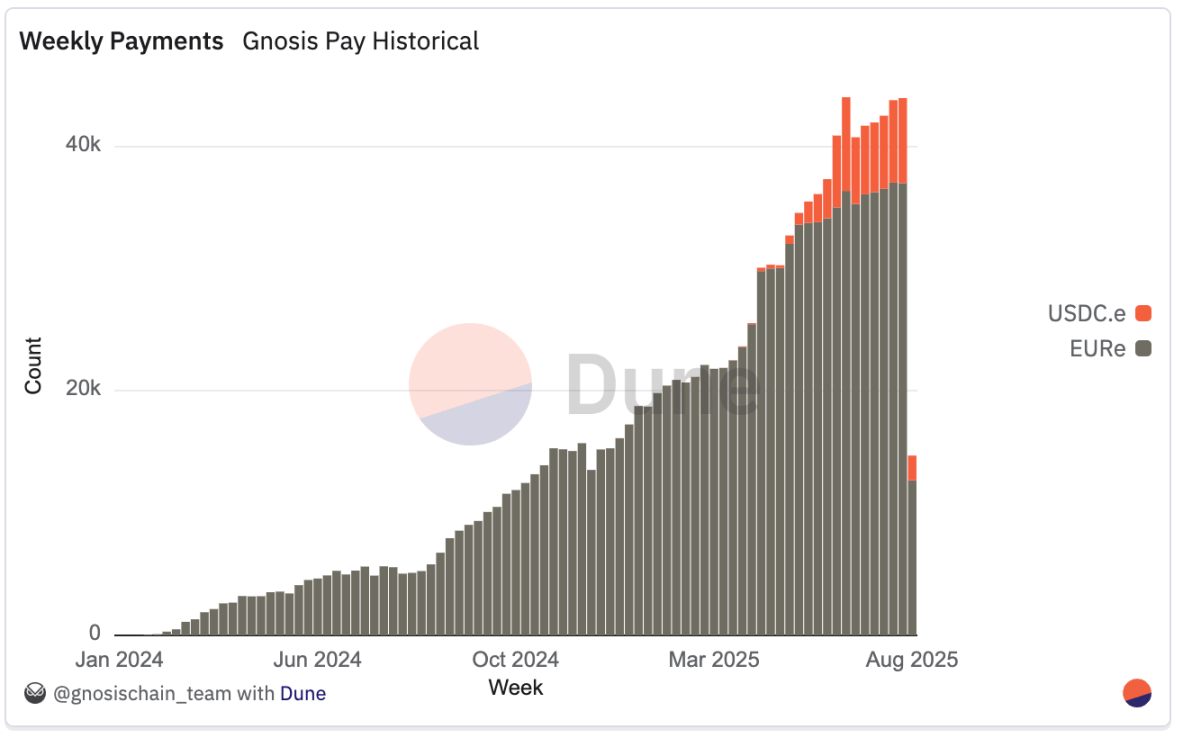

Picnic is a decentralized investment platform built on blockchain, aimed at simplifying access to digital assets. Its smart wallet is supported by Safe contracts and ERC-4337 account abstraction technology, allowing users to register with just an email while maintaining self-custody. In addition to investing in a curated portfolio of crypto assets, Picnic has launched Picnic Pay in collaboration with Gnosis Pay, introducing the first stablecoin card in Brazil, thus expanding into real-world payments.

- Users can top up their Gnosis Pay card through Brazil's instant payment system, Pix, with deposited reais automatically converted to dollars and settled on-chain.

- The card supports online and in-store purchases and integrates with Apple Wallet and Google Wallet.

- Picnic Pay connects directly with decentralized finance protocols, allowing funds from Aave or yield-generating real stablecoins to be used directly for consumption.

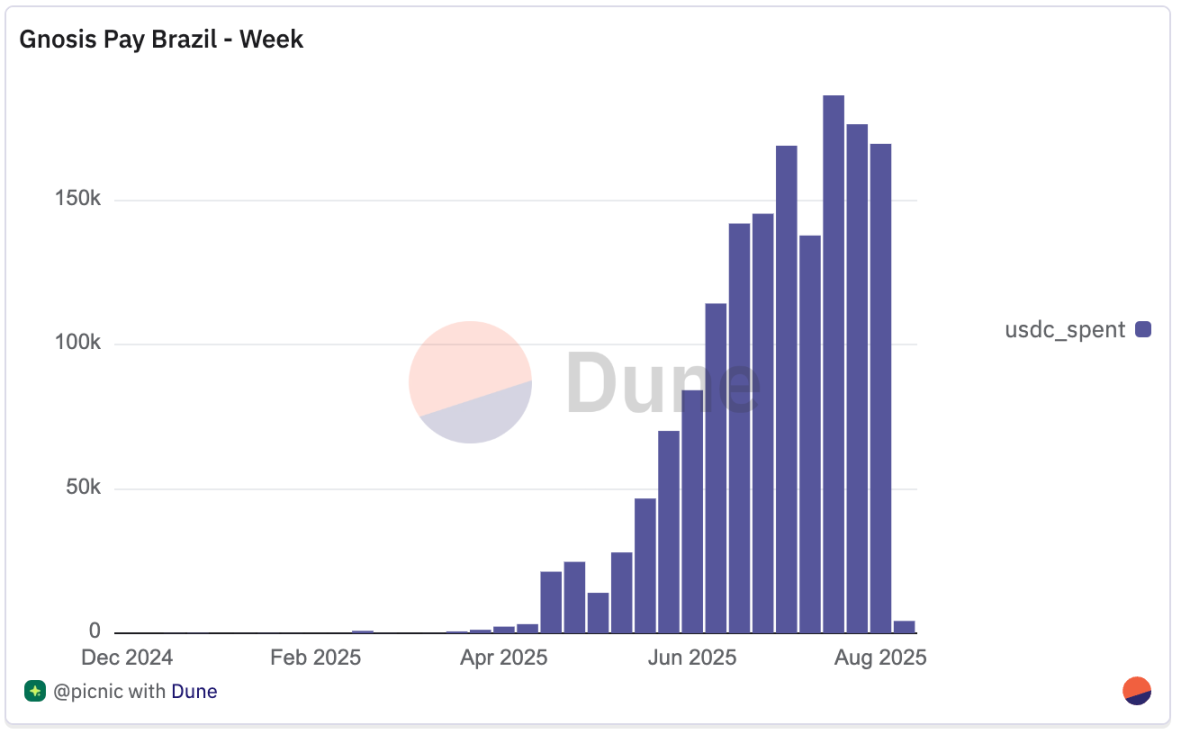

All USDC.e activity on Gnosis Pay in Brazil is attributed to Picnic, which currently accounts for about 7% of Gnosis Pay's total weekly trading volume but nearly 15% of total weekly payments, highlighting its higher payment frequency relative to the value of each payment.

Since its launch, Picnic has grown to over 350 daily active users, processing more than 45,000 payments weekly, with weekly trading volume exceeding $150,000.

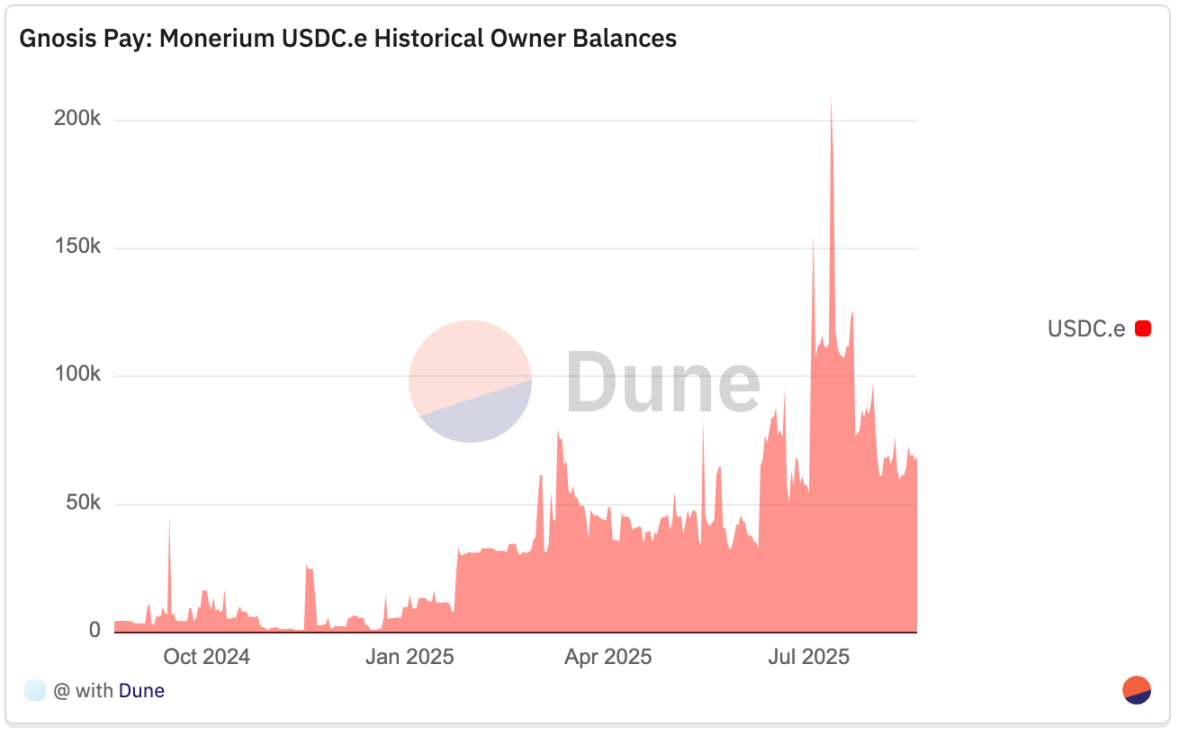

After its launch at the Rio de Janeiro Network Summit in April 2025, activity has remained strong, with daily transactions typically between 800 and 1,000, occasionally peaking above 1,100. By the end of July, user balances stood at $80,000, down from a peak of $200,000 on July 20, indicating that funds are actively circulated on the platform rather than lying idle, consistent with its role as a payment tool focused on consumption rather than long-term value storage.

Picnic has integrated with Avenia to offer BBRL yield products, expanding its savings suite beyond BRLA. Users can convert BRLA into yield-generating versions (such as stBRLA or yBRLA), earning approximately 12% annualized returns linked to Brazil's CDI rate. In addition to savings, Picnic connects users to major decentralized finance platforms like Aave and Morpho, enabling BTC lending in Brazil, thereby expanding the use of local stablecoins in terms of yield, trading, and credit access.

Through Picnic Pay and its decentralized finance yield integration, the platform sits at the intersection of asset management and consumer payments. By embedding stablecoin card functionality into its investment platform, it directly connects yield-generating and self-custodied assets with everyday consumption—an emerging model in Latin America where local payment channels like Pix serve as bridges for on-chain settlements.

Exa Application

Exactly Protocol is a decentralized, non-custodial interest rate market that offers variable and fixed lending rates determined by the utilization of multiple term pools.

The Exa application extends this model to mobile, allowing users to deposit assets such as USDC, ETH, wstETH, WBTC, and OP, which remain self-custodied while continuously earning variable interest before consumption. After completing KYC verification (Visa compliance requirement), users can access the Exa card, an on-chain payment card that supports two modes:

Instant Payment: The purchase amount is deducted directly from the interest-earning balance.

Installment Payment: The application borrows from Exactly's lending pool at a fixed rate at the time of purchase, with repayments fixed over a maximum of six installments.

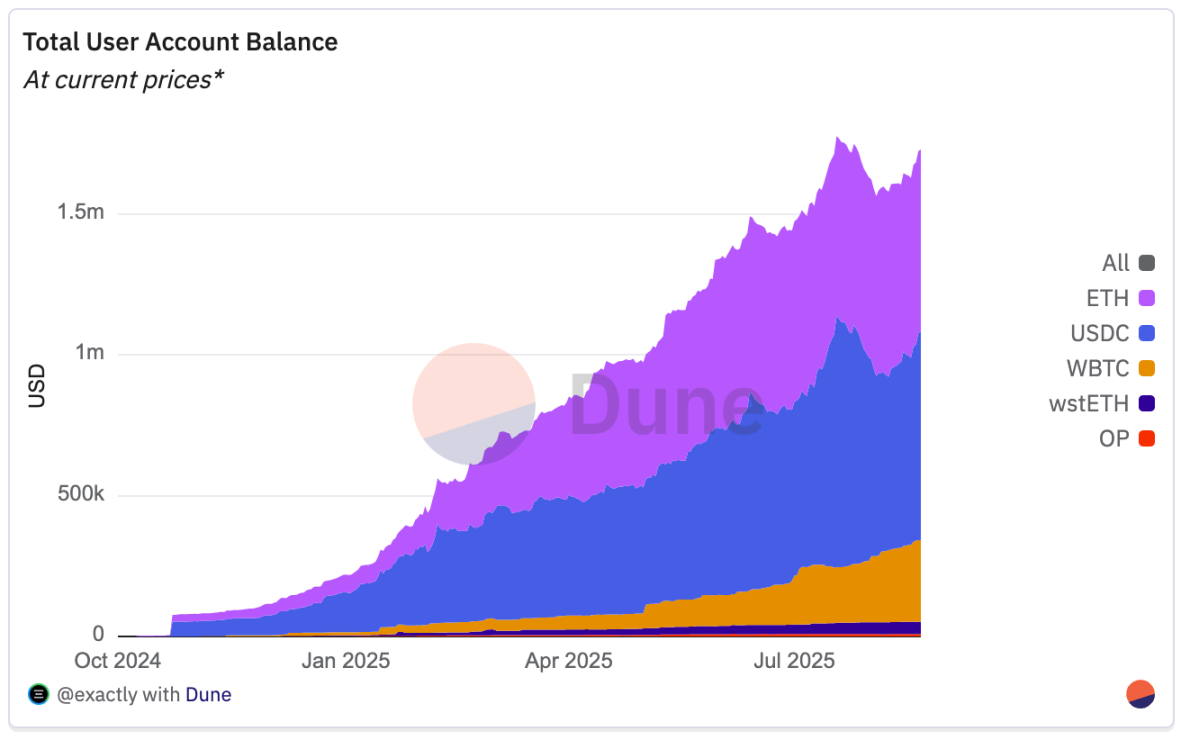

According to the latest data, the Exa application holds $1.62 million in user balances (with a total locked value of approximately $1.08 million), including about $650,000 in ETH and USDC, approximately half of which is WBTC, with smaller allocations for other tokens.

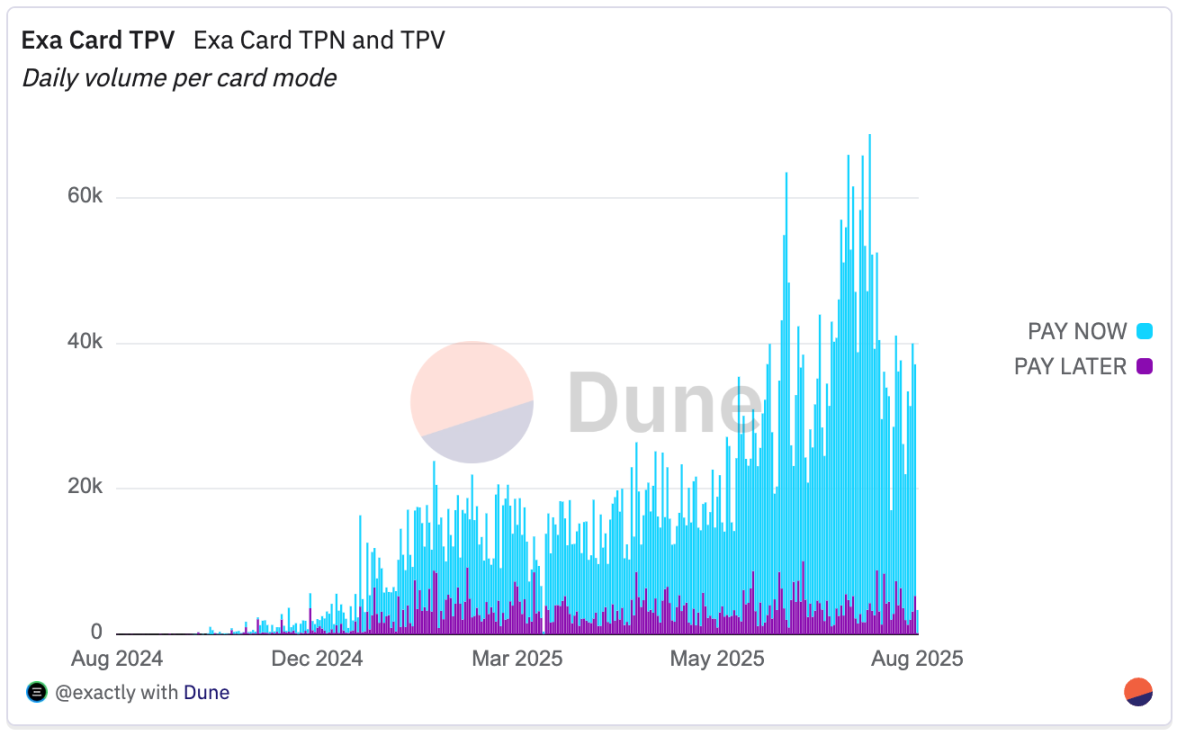

The total transaction volume for the Exa card has reached $5.04 million, with most coming from instant payment transactions, while installment payments (buy now, pay later) account for $793,000. Compared to card usage, lending still occupies a smaller share, with 69 loans issued to 30 borrowers totaling $47,400.

Overall, current usage is concentrated on card transactions, with a small proportion of loan volume. The combination of yield-generating deposits and fixed-rate lending payments creates a unique on-chain payment model, where the user's net cost or yield depends on the spread between deposit yields and lending rates.

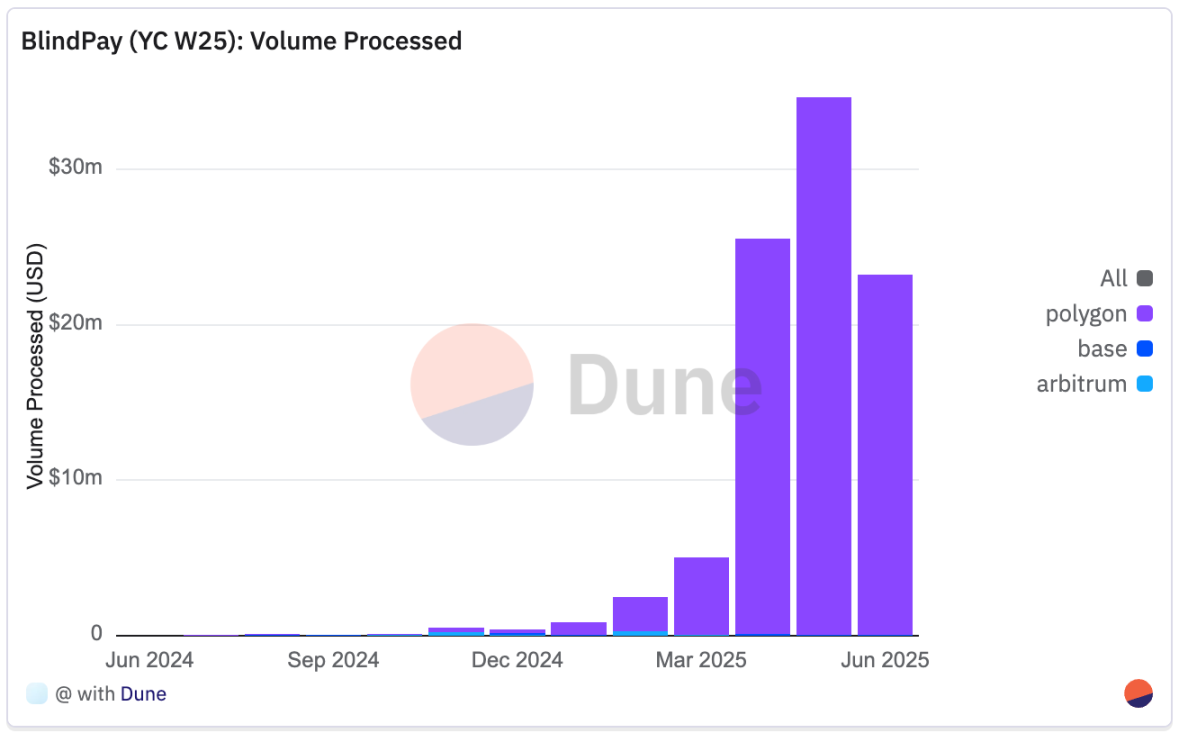

BlindPay

BlindPay provides API infrastructure for businesses to send and receive fiat and stablecoin payments globally. It manages compliance, regulatory requirements, and the complexities of integration with various payment channels, including Pix (Brazil), SPEI (Mexico), and PSE (Colombia) in Latin America, as well as ACH, Wire, RTP, and SWIFT in the United States. On the blockchain side, it supports Ethereum, Arbitrum, Base, Polygon, and Tron, facilitating settlement flows between cryptocurrencies and local fiat systems. BlindPay offers various features, including:

- Priority API Integration: Developer-friendly endpoints for embedding global payments into applications and platforms.

- Infrastructure Layer Compliance Handling: Built-in KYC/KYB, fraud detection, and regulatory alignment.

- Local and Cross-Border Payments: Support for regional instant payment systems and stablecoin transfers.

- Settlement Speed: Designed to settle significantly faster than traditional channels.

Since its launch, BlindPay has processed a total transaction volume of $93 million, covering all active regions, including the United States, Brazil, Mexico, Argentina, and Colombia, with most transaction volume concentrated in Latin American countries. Although this data only covers up to June, the team emphasizes that July and August brought an additional $70 million in transaction volume.

Polygon accounts for $91.86 million, approximately 99% of the total processed volume, followed by Arbitrum ($756,000) and Base ($426,000). Monthly transaction volume has grown from several million dollars in mid-2024 to sustained levels of several million dollars in 2025, reflecting increased API adoption and the expansion of more payment channels.

By combining stablecoin channels with local payment infrastructure, BlindPay addresses the operational gap between blockchain settlements and real-world payments, which is particularly important for Latin American businesses that need to connect multiple currencies, banking systems, and jurisdictions.

Key Takeaways

Payment applications are becoming crypto-native digital banks. Applications now integrate savings, yields, and everyday payments, covering both banked and unbanked users through mobile-first, stablecoin-driven financial services.

- Picnic processes over 45,000 payments weekly through Gnosis Pay, offering local stablecoin yield products with approximately 12% annualized returns.

- The Exa application has processed $5.04 million in card payments, with 85% associated with the "instant payment" model linked to interest-earning deposits.

- BlindPay's total processing volume is $93 million, with 99% on Polygon, integrating stablecoin channels with Pix (Brazil), SPEI (Mexico), and PSE (Colombia) for compliant, fast payments.

- Lemon Cash, Nubank, and Mercado Pago are embedding cryptocurrencies directly into the consumer banking system—for example, Lemon's stablecoin card (with BTC cashback) and Mercado Pago's own dollar stablecoin (Meli Dólar).

Projects Worth Noting That Are Not Captured by Dune

While this report focuses on projects with on-chain data on Dune, the breadth of the Latin American crypto ecosystem far exceeds our current coverage. The region has numerous mature and innovative platforms that we have yet to track through verifiable on-chain data.

- Abroad—— An open-source payment infrastructure that integrates USDC with real-time fiat networks to enable instant, low-cost cross-border and offline payments. Partners, including wallets, banks, and fintech companies, can embed Abroad, allowing users to make payments through local systems like Pix (Brazil) and PSE (Colombia). Recent partners include Beans and Decaf, focusing on the Latin American market and strict compliance.

- Amero—— A fintech platform building financial infrastructure that connects traditional payment channels in Latin America with the digital asset ecosystem. Its deposit and withdrawal channels support over 100 payment methods, including credit cards, bank transfers, and cash transactions at over 350,000 locations. Amero integrates with Circle's programmable wallet, supporting Ethereum, Avalanche, and Polygon, and will launch a prepaid Mastercard/Visa card in Mexico for USDC top-ups, global spending, and ATM withdrawals. Partnerships with Circle and MoneyGram support remittances and self-service withdrawals, targeting unbanked users, merchants, and freelancers.

- Argiefy—— A fintech application from Argentina designed to help users save money and make better financial decisions in a turbulent economy. It offers a currency converter, verified transactions, coupons, promotions, and community-shared daily shopping and travel deals. The platform also integrates cryptocurrency-to-fiat exchange services through partners like zkp2p, combining local transactions with digital asset liquidity access.

- Bando—— An on-chain consumption protocol that allows users to pay for real-world goods and services directly with cryptocurrencies and stablecoins, without the need for fiat conversion or traditional withdrawal channels. Operating in over 100 countries and 6,000+ businesses, it supports merchants like Amazon, Uber, and Airbnb, as well as prepaid cards, mobile top-ups, bill payments, and digital goods. Bando addresses financial barriers in Latin America through Web3, integrating with wallets like MiniPay, Binance Wallet, and Base App, leveraging decentralized finance liquidity and smart contracts to route transactions to verified fulfillers for seamless shopping, top-ups, and digital services.

- Buenbit—— A fintech platform founded in Argentina, operating in Latin America, including Mexico and Peru, offering a user-friendly app for cryptocurrency trading, daily yield savings, cryptocurrency-backed credit lines, and seamless payments using stablecoins or other assets via an international Mastercard. It supports over 40 cryptocurrencies, such as BTC, ETH, DAI, and USDT, across networks like Ethereum and Polygon, offering free deposits, instant transfers via Buentag, and secure non-custodial wallets for over 700,000 users seeking financial inclusion amid regional volatility.

- Coinsenda—— Provides wallet and exchange services for individuals and businesses to exchange 18 digital assets with local currencies, with an active OTC desk for USDT. 90% of activities occur on Tron, serving over 2,900 monthly active users with a monthly processing volume of approximately $546,000. USDT accounts for over 87% of recent transactions, benefiting from free Tron withdrawals and widespread adoption in payroll payments, with smaller remittance transaction volumes.

- El Dorado—— A peer-to-peer marketplace for buying and selling stablecoins using the most popular payment methods in Latin America. Through its app, users can send and receive USDT and other stablecoins, with 90% of activity coming from retail market recipients, supported by a liquidity network of 10,000 merchants. El Dorado is primarily active in Brazil, Colombia, Argentina, Peru, and Bolivia, with a monthly transfer volume of $18 million and 180,000 monthly active users, with Tron accounting for 60% market share.

- KAST—— A payment platform offering a seamless stablecoin experience, including global credit card spending. With over 500,000 total users (50,000-100,000 monthly active users) and a total transaction volume of approximately $500 million, it supports cross-chain payment and deposit/withdrawal services across Latin America, the EU, the US, and Asia. Tron leads usage with a 55% share, with Brazil showing the strongest growth, experiencing a 112% month-over-month increase in spending in the first half of 2025.

- Kripton—— A Latin American payment processor and retail crypto service provider that has applied the decentralized principles of Bitcoin to commerce since 2019. In April 2025, it adopted USDT on Tron as its primary digital dollar for secure and subsidized payments. Serving retail, merchants, and payment platforms, Kripton's network is deeply integrated into the region's stablecoin economy, with Tron accounting for 70% of usage.

- Muney App—— A fintech platform that simplifies the buying, transferring, and withdrawing of stablecoins in Latin America. Built on Polygon, it provides plug-and-play infrastructure for wallets and apps, connecting digital dollars with local cash through a decentralized network of verified merchants. Users can deposit and withdraw cash, make peer-to-peer payments, and access compliant withdrawal channels, focusing on remittances—including sending USD cash withdrawals to Venezuela from multiple countries.

- Mural Pay—— A fintech platform and API focused on stablecoin payments, providing businesses with instant global deposits, withdrawals, invoicing, virtual accounts, and compliance tools. Active in over 40 markets, it focuses on Latin America and Africa, supporting low-cost, real-time transactions in stablecoins and traditional currencies. A recent partnership with Taxbit has expanded its stablecoin invoicing and cross-border payment capabilities in the US, EU, and Latin America.

- Orionx—— A Chilean cryptocurrency exchange and financial infrastructure provider operating in Chile, Peru, Colombia, and Mexico. Founded in 2017, it offers fiat deposits starting from 10,000 Chilean pesos for buying and trading over 20 digital assets. In June 2025, Orionx secured a strategic Series A investment from Tether to expand stablecoin-driven remittance, receiving, treasury services, and payment solutions, particularly for USDT on the Tron network.

- Sphere—— A digital economy "operating system" designed for markets lacking financial services, focusing on providing fast, secure cross-border payment services. It targets individual users, merchants, and developers, integrating stablecoin-backed deposit and withdrawal channels, with the core goal of promoting financial inclusion. Currently, its operations cover Latin America and the US, holding a 45% market share in the Tron (TRON) ecosystem, with a quarterly growth rate of 68% in total transaction volume.

- Swapido—— A non-custodial platform based on the Lightning Network, focusing on instant exchanges of Bitcoin to Mexican pesos and bank transfers in Mexico. The platform is designed for remittances, payments, and everyday consumption scenarios, allowing global users to sell Bitcoin in seconds and have the exchanged pesos directly deposited into any local bank account in Mexico. Currently, it only supports Bitcoin transactions, with plans to add stablecoin functionality in 2025.

- Takenos—— An Argentine fintech application that combines digital wallet and Web3 banking features, designed for freelancers, gamers, influencers, and anyone needing to handle cross-border payments in Latin America. Users can receive income settled in USD, EUR, or other currencies globally, withdraw funds via cryptocurrency, local cash, or USD, and utilize features like instant payment links, debit/credit cards, and seamless global transfers.

- Ugly Cash—— A stablecoin-based financial service application offering high-yield accounts, instant fee-free cross-border transfers covering over 60 countries, and a Visa card with a 1% cashback rate. Users can hold and spend stablecoins, withdraw cash via ATMs, and use virtual accounts supporting bank transfers in USD, EUR, and Mexican pesos.

Leading fintech companies in Latin America, such as Nubank, Mercado Pago, PicPay, and RappiPay, have expanded from traditional banking and payment services into the crypto space, echoing the paths of global players like Revolut and PayPal. These platforms collectively serve hundreds of millions of users and now support in-app buying, selling, holding, and transferring of assets like Bitcoin, Ethereum, and stablecoins, often accompanied by yield or cashback benefits. Mercado Pago has integrated crypto features into its e-commerce system and launched the USD-pegged stablecoin "Meli Dólar" in 2024; PicPay has added trading features for Bitcoin, Ethereum, and USDP, planning to launch a stablecoin pegged to the Brazilian real and integrate with the Binance ecosystem; RappiPay has simultaneously launched cryptocurrency payment features within its wallet, debit card, and savings account systems. By embedding crypto services into mainstream fintech applications, these leading platforms provide compliant and low-barrier access channels for millions of users in a turbulent economic environment.

Conclusion

As presented throughout this report, the cryptocurrency narrative in Latin America revolves around building an alternative financial infrastructure that people will genuinely use. Across the region, the proliferation of on-chain applications is driven by real demand: protecting savings from inflation, facilitating cross-border fund transfers, settling with suppliers, disbursing salaries, and empowering everyday business activities.

Latin America is developing a parallel financial system—one that is multi-chain, stablecoin-centric, and deeply integrated with local payment networks. This system increasingly possesses all the functionalities of traditional banking, yet is often faster, cheaper, and more accessible.

Challenges remain: data gaps, regulatory differences, and the urgent need for deeper liquidity in local currency stablecoins. However, the trajectory of development is clear: starting from speculative trading, it is now evolving into a resilient, multi-layered ecosystem—where cryptocurrencies are not only investment vehicles but also the default choice for savings, transfers, and consumption.

If the past decade was about proving the theoretical viability of cryptocurrencies, the next decade will be about scaling their practical applications. The new chapter of the on-chain economy in Latin America will be co-authored by developers, analysts, and communities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。