Original | Odaily Planet Daily (@OdailyChina)

Author | Ethan (@ethanzhangweb3)_

On August 19, the stablecoin protocol Cap announced its launch on the Ethereum mainnet. Users can deposit USDC into the reserve pool, mint cUSD, and start accumulating protocol points called caps. This also marks a key step for the project after completing a $11 million funding round in April, officially moving from concept to implementation.

Cap's funding lineup is quite impressive. As a globally renowned asset management company, Franklin Templeton has been actively positioning itself between on-chain assets and traditional finance in recent years, and this investment is seen as an endorsement of the "mechanism-driven" stablecoin model. The involvement of investment institutions like Triton Capital adds further credibility to Cap at the capital level.

On the day of the launch, Bankless co-founder David Hoffman posted on X, pointing out that Cap's uniqueness lies in its combination of unsecured lending and EigenLayer re-staking. He wrote: "Borrowers can access credit lines, but the risk is borne by the re-stakers, which provides cUSD holders with unprecedented protection."

Mechanism: Dual Token and Five Roles

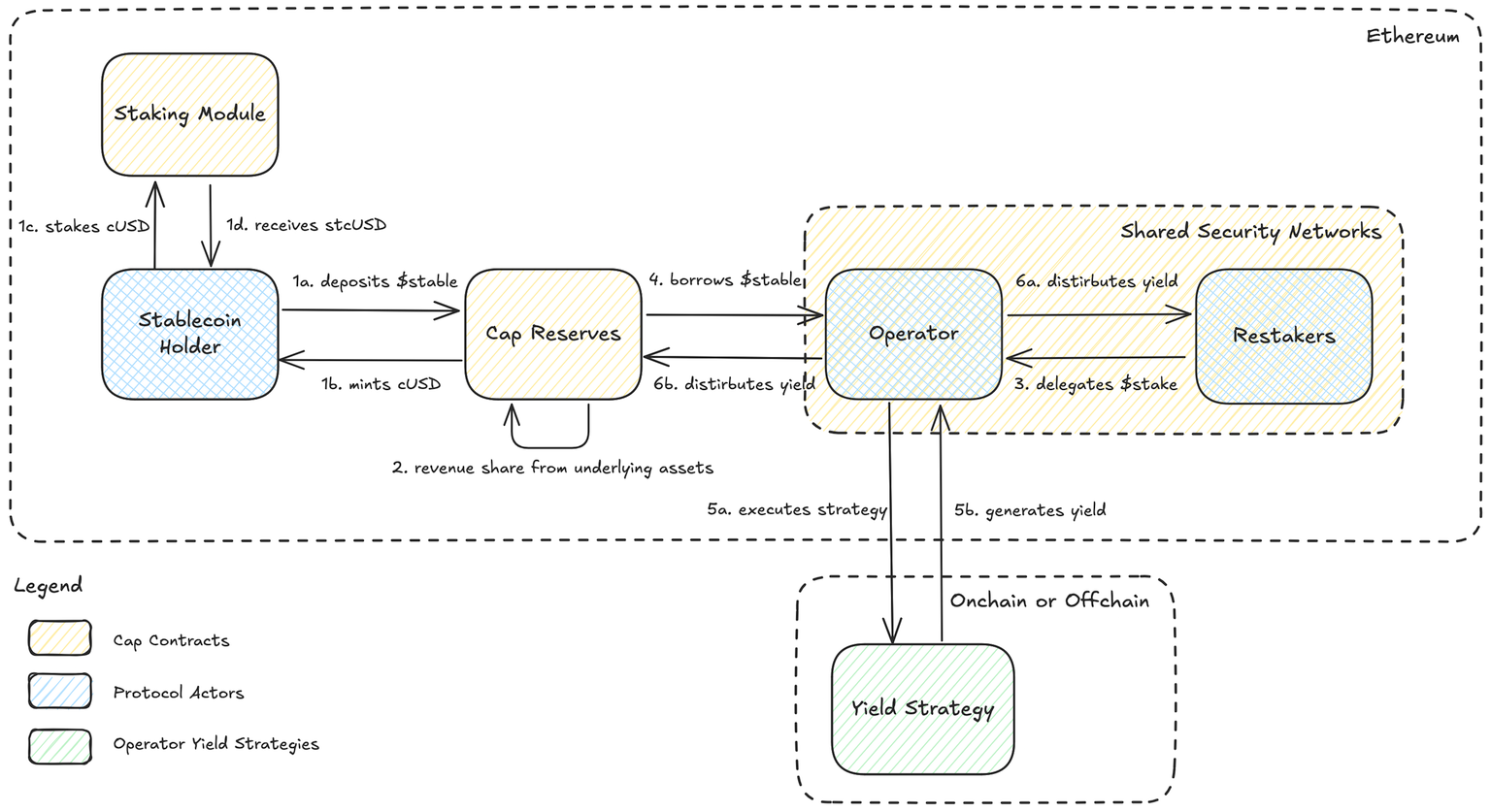

Cap's overall design resembles a structured financial system, where the core is not just the issuance of stablecoins but also the restructuring and redistribution of returns and risks through mechanistic rules. The protocol includes five core participants: cUSD holders, stcUSD holders, operators, re-stakers, and liquidators. Funds flow out of the reserve pool, with operators executing strategies, and through revenue distribution and liquidation mechanisms, they cycle back to users.

Cap employs a dual-token structure: cUSD is the reserve-backed base stablecoin, supporting USDC deposits for minting and proportional redemptions, serving as a unified settlement layer in the system, helping users switch freely between various reserve assets; stcUSD is the yield-bearing stablecoin, where users must first hold cUSD and stake it to receive stcUSD, thereby obtaining automatic compound yield distribution from the protocol.

Operators are the key nodes for generating revenue. To lend funds, operators must first obtain guarantees from re-stakers, who provide credit support with locked assets and charge a fixed risk premium. If operators successfully repay the loan and pay interest, the protocol distributes the revenue proportionally: the base interest rate goes to stcUSD holders, the premium portion is paid to re-stakers, and the remaining profit belongs to the operators. This logic ensures that incentives among different participants remain aligned.

On the risk side, Cap sets clear boundaries through its liquidation mechanism. If an operator defaults or the health of the loan position falls below a threshold, liquidators will buy the collateral assets of the re-stakers at a discounted price through a Dutch auction and exchange them for reserve stablecoins to compensate stcUSD holders. This means that user principal has a clear on-chain recourse mechanism, with risks borne by re-stakers, achieving structural equivalence of responsibility.

Mechanism Case Study (Source: Official Documentation)

To better understand how this mechanism achieves the distribution of returns and risks, let's consider a minimal scenario:

Alice deposits $100 of USDC on the Ethereum mainnet, and the system automatically mints 100 cUSD. She then stakes these cUSD for stcUSD, thus becoming a yield participant and starting to earn automatic compound interest according to the protocol rules.

Meanwhile, an operator identifies a potential strategy opportunity with an annual yield exceeding 8%. To obtain a loan, they need to find a re-staker willing to guarantee their risk. After due diligence, the re-staker provides the guarantee and charges a preset risk premium. Once the guarantee is secured, the operator can borrow funds from the reserve pool to execute their strategy.

If the strategy is successful, the protocol distributes the revenue according to fixed rules: for example, if the operator earns a 15% return, 8% will be automatically allocated to stcUSD users, 2% paid to re-stakers, and the remaining 5% is the operator's net profit. Users do not need to perform any manual operations; the revenue accumulates automatically through the contract's compounding mechanism.

This is the "Happy Path" designed by Cap—funds flow from users, generate revenue through on-chain strategies, and complete automatic distribution among different roles, with users as the upstream holders receiving priority rights to earnings.

However, reality is not always a Happy Path. If an operator defaults or the position falls below the risk threshold, the protocol will trigger the liquidation mechanism, and liquidators will auction the re-stakers' collateral assets at a discount, recovering stablecoin reserves to compensate stcUSD users' principal. This mechanism ensures that user risks are always at the priority level of protocol protection, avoiding the structural risk of "strategy failure, user pays."

Returns and Risks: The Other Side of the Mechanism

From the above case, it can be seen that the "automatic compounding" yield path provided by Cap's stcUSD is driven by a complete set of on-chain mechanisms, allowing users to receive yield distribution with minimal operation. Compared to the traditional DeFi model, where users manually migrate and desperately chase APY, this model is clearly more user-friendly.

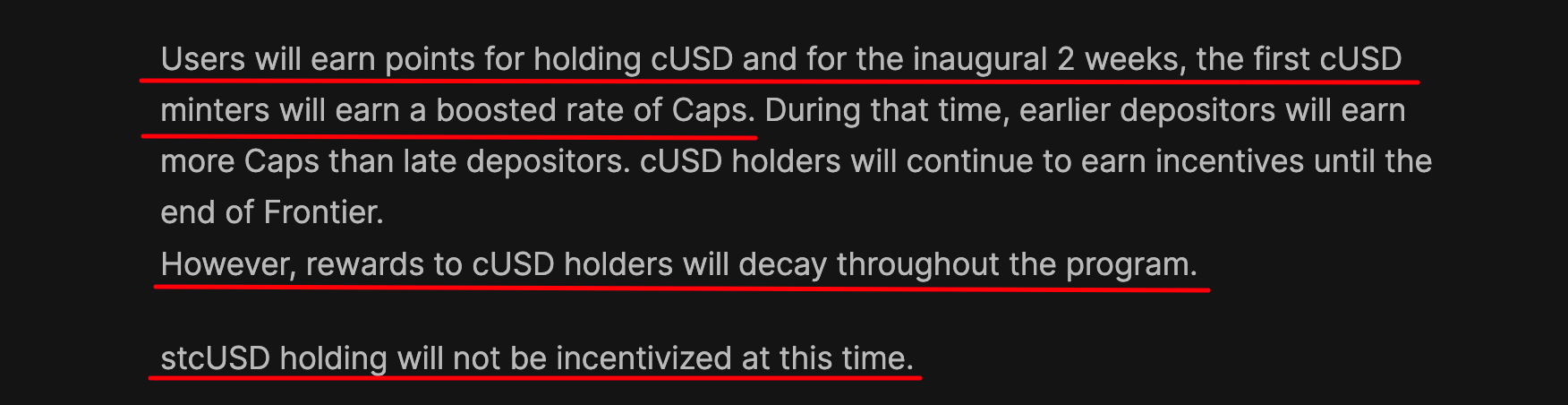

However, Cap's current yield narrative is not among the most attractive. According to existing rules, cUSD holders can earn point rewards, and after staking cUSD for stcUSD, they can switch to obtaining on-chain yields. However, both cannot be enjoyed simultaneously: points and yields must be chosen one or the other. (See more in “Cap Frontier Plan”)_

As of the time of publication, the official website shows that Cap's TVL is $15.44 million, with stcUSD APY around 23.07% (which has peaked at 130%). As funds continue to flow in, the yield shows a fluctuating upward trend, but whether it can be maintained ultimately depends on the efficiency of strategy execution and the overall robustness of the system.

Cap's core feature is that it does not rely on centralized decision-making by the team but allows returns and risks to flow dynamically among different participants through mechanisms. For users, this design not only brings a more sustainable yield path but also strengthens the verifiability of risk protection—this remains a minority in the current DeFi yield products.

Risk Logic

Cap's logic in risk management is significantly different from traditional yield-bearing stablecoins.

In common models, once a strategy fails, the losses are often directly borne by users, and may even be hidden by the project in undisclosed financial structures. Cap's design shifts this portion of risk to re-stakers: if an operator defaults or the position falls below a safe threshold, the collateral assets of the re-stakers will be liquidated, prioritizing compensation to stcUSD holders. Structurally, stcUSD resembles "priority creditors," meaning that even with automated yields, risks are not easily passed on to users.

Of course, this does not mean that Cap is completely without risks. Smart contracts themselves remain a core risk point; any undiscovered vulnerabilities could lead to systemic issues. External components that the protocol relies on, such as EigenLayer, oracles, and cross-chain bridges, could also become potential conduits for risk transmission. Additionally, if reserve assets and re-staked assets experience price fluctuations or compliance issues, it could trigger a chain reaction.

Cap has designed multiple mitigation mechanisms, including whitelisted asset restrictions, dynamic interest rate adjustments, and off-chain guarantee agreements, but the effectiveness of these measures still needs to be tested over time and in practice.

Summary

In summary, Cap's yield model can be described as "more transparent and more structured": the sources of yield are on-chain verifiable, and the risk exposure is written into the contract logic, so users no longer rely on verbal promises from the team. However, from another perspective, the more complex the protocol, the more potential vulnerabilities it may have, which is something that no participant can overlook.

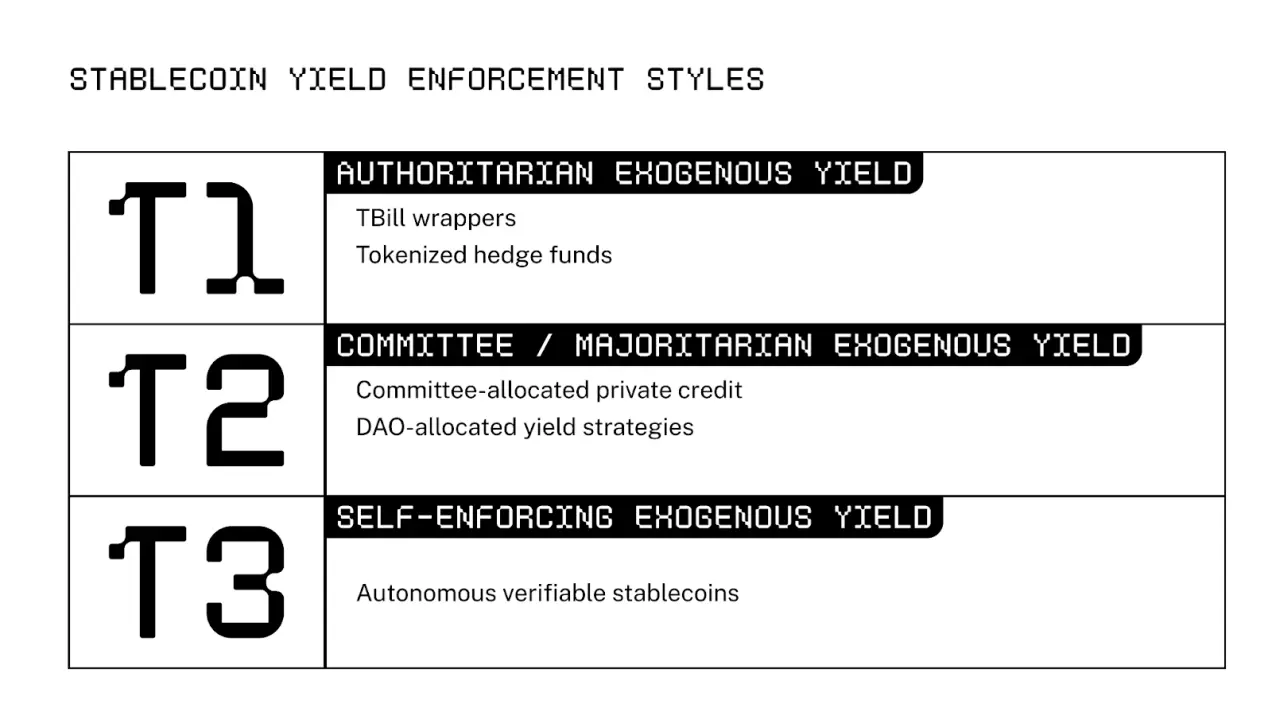

Comparison of Yield-Bearing Stablecoin Architectures: Three Design Paths

Referring to the classification method of the Stanford Blockchain Club, yield-bearing stablecoins can be divided into three types based on their yield distribution mechanisms: centralized strategy management (T1), DAO governance-based allocation (T2), and on-chain self-coordination models (T3).

The core differences among the three paths lie in two dimensions: how strategies are determined and who bears the risks.

First Type: Centralized Strategy, Efficiency and Risk Coexist.

Representative Projects: Ethena (USDe), Ondo, Agora, Resolv.

These stablecoins have their yield strategies decided and executed centrally by the project team. User funds flow into a unified pool, which the team allocates for use. For example, USDe generates yield by shorting ETH perpetual contracts and constructing hedging models to capture interest rate spreads.

For users, this model has lower transparency, and the yield mechanism heavily relies on the team's capabilities. If the strategy fails or the team is negligent, users have almost no recourse. To some extent, this resembles giving the project a "unsecured debt", where trust is a prerequisite, and risks are uncontrollable.

Second Type: Governance Coordination, Stable but Slow.

Representative Projects: MakerDAO (DSR), Sky, Maple Finance.

These stablecoins delegate strategy allocation to governance organizations. Funds can dynamically switch between multiple external strategies, with decisions made by governance token holders or their authorized representatives.

Advantages lie in structural stability and risk diversification, but governance games often lead to slow strategy updates, with issues like vote bribery and misaligned incentives persisting over time. Additionally, since users are at the end of the protocol, they still face the dilemma of being unable to recover losses if a strategy fails.

Third Type: Mechanism-Driven, Automatically Coordinating Risk and Returns.

Representative Project: Cap (stcUSD).

Cap solidifies the logic of risk and return distribution through smart contracts and achieves automatic operation via on-chain incentive mechanisms. The team no longer decides the flow of funds but forms a self-consistent closed loop through a "re-staking + lending + liquidation" triangular structure:

- Operators identify strategic opportunities and can borrow funds after being guaranteed by re-stakers;

- When operations are successful, returns are automatically distributed proportionally among stcUSD users, re-stakers, and operators;

- In the event of default, the liquidation mechanism is triggered, and re-staked assets will prioritize compensation to stcUSD users.

Compared to the first two types, Cap's stcUSD is more like a "priority creditor" design at the protocol level. The flow of funds is verifiable, risk responsibilities are quantifiable, and governance participation is minimized. This model emphasizes that: returns can be competitive, but risks must be clearly defined.

Summary: Differentiation in Yield Paths and Risk Attribution

In summary, the core differences among the three models boil down to three points: methods of yield distribution, decision-making power for strategies, and risk attribution.

Interactive Tutorial: How to Participate in the Cap Protocol?

Having understood the mechanisms and risk structures built by Cap, let's take a look at the real user experience—minting cUSD, staking it for stcUSD, and earning on-chain yields. The entire process has a low interaction threshold.

Here is an example of a minimal path operation: using the cUSD Swap process as an example, the stcUSD method is similarly applicable. (Tip: Currently supports the ETH mainnet, be sure to confirm that your wallet network has switched)

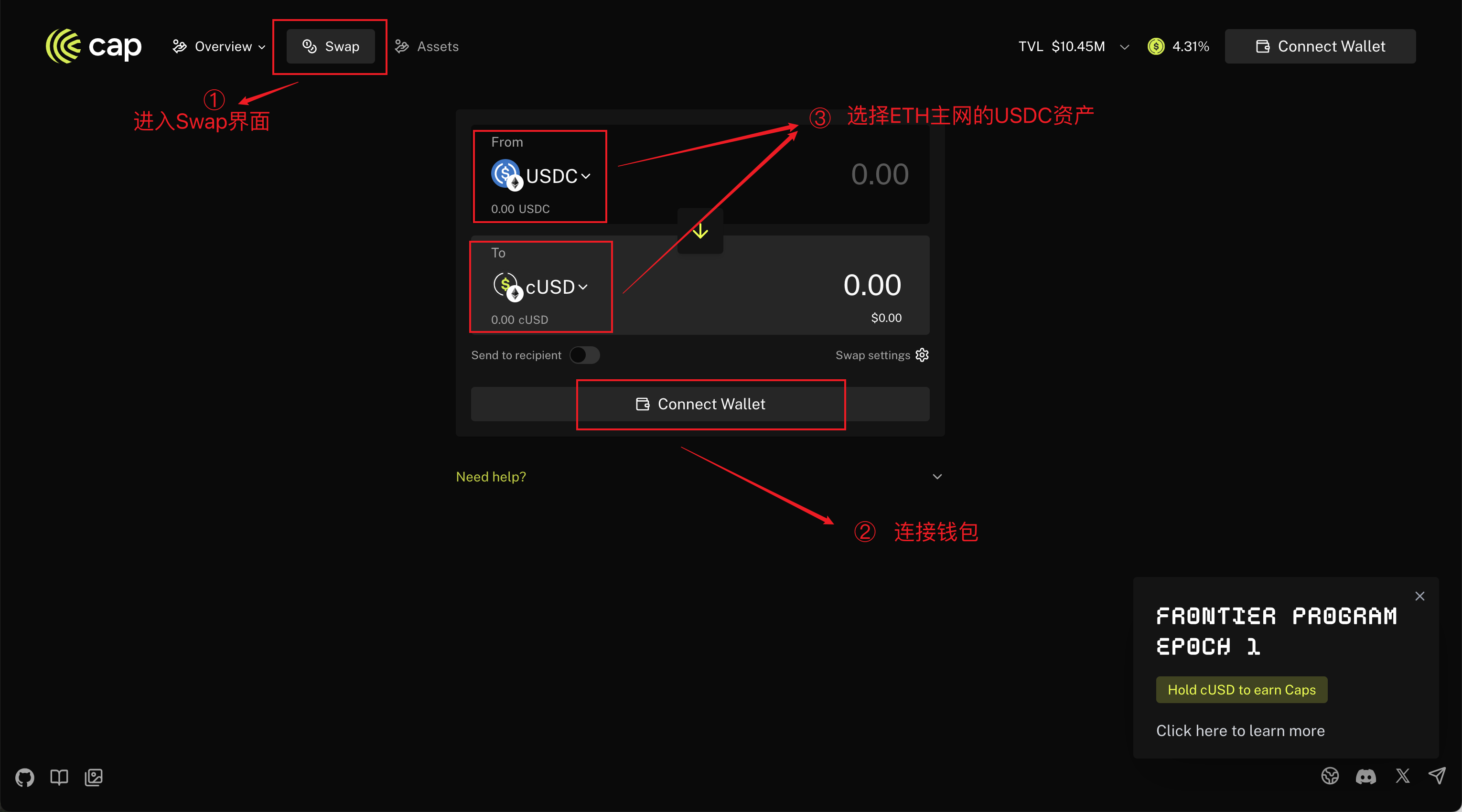

STEP 1: Open the Cap Official Website;

STEP 2: Click "LAUNCH APP," enter the "SWAP" interface, and connect your wallet; select USDC on the ETH mainnet to exchange for cUSD; then click "Swap" and wait for the wallet plugin to sign;

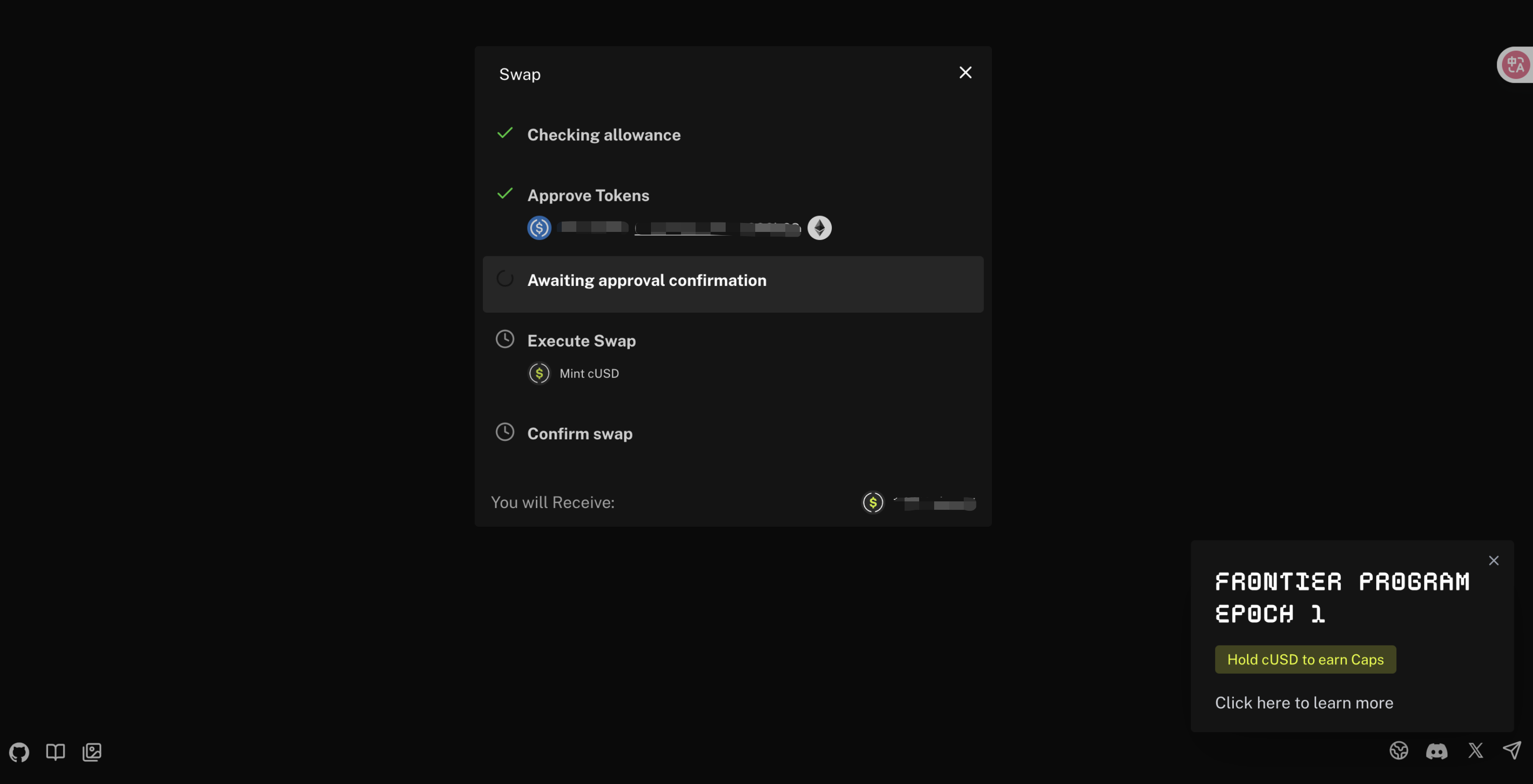

STEP 3: Wait for the exchange to complete (this page will show wallet plugin pop-ups like "Approve contract interaction," "Transfer exchange amount," etc.);

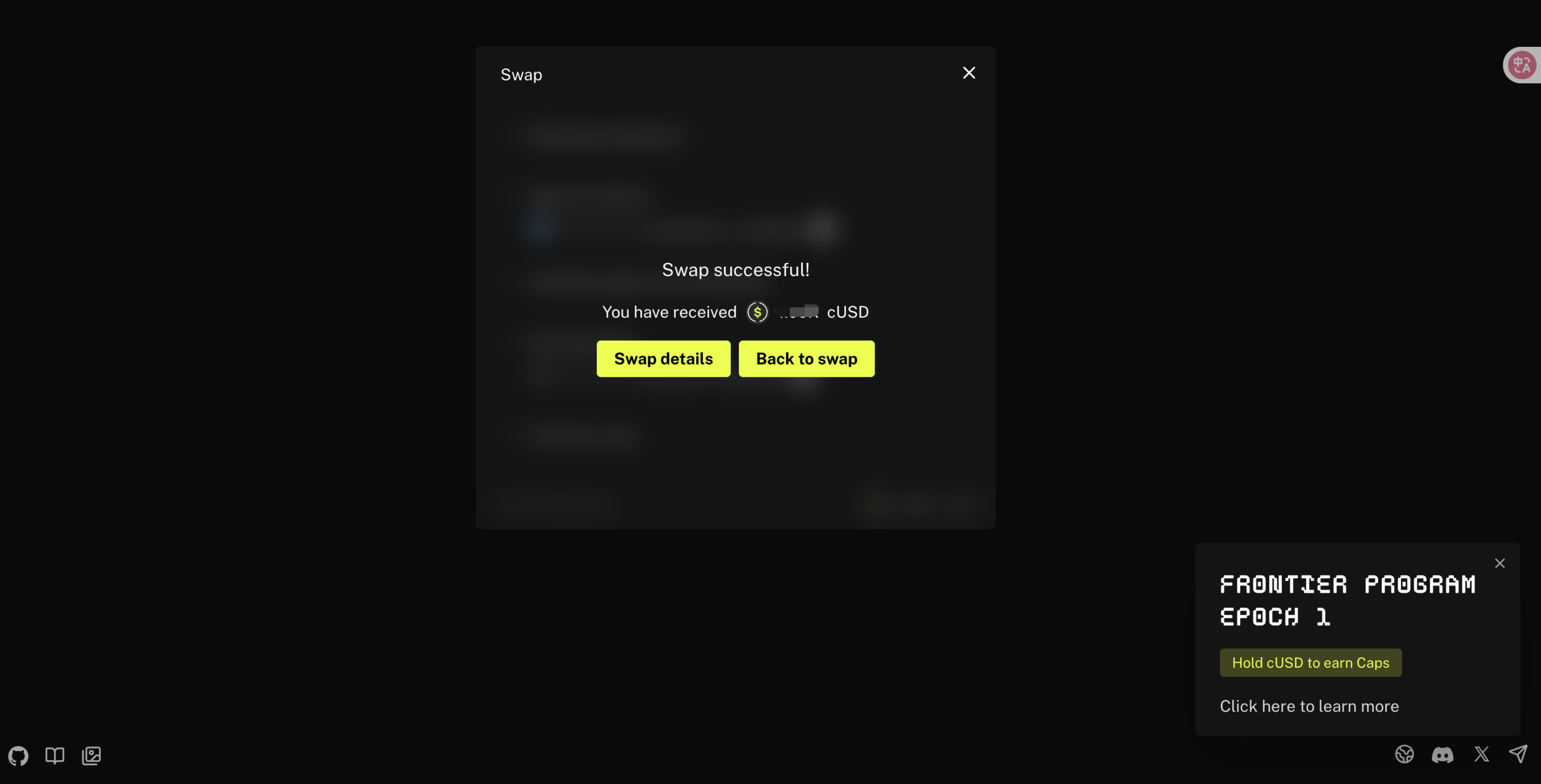

STEP 4: Complete the exchange of cUSD.

Conclusion

The launch of Cap is not just about adding a new stablecoin; it is a structural experiment regarding the distribution of returns and risks. Over the past few years, the stablecoin market has evolved from being dollar-pegged to emphasizing compliance and transparency, and now to exploring yield generation. Most attempts either limit returns to reserve interest or overly rely on team decisions, making it difficult to find an effective balance between scaling and risk control.

Cap's solution is to hand over the distribution of returns and risks to mechanisms. Returns are generated through the competition between operators and re-stakers, while risks are hedged through on-chain rules and liquidation systems, placing users in a logically safe zone. This design endows stcUSD with a certain "self-sustaining" capability and, to some extent, detaches it from subjective human judgment.

However, mechanisms do not mean no risk; they merely redistribute the positions of risk. The complexity of Cap means it still needs to undergo long-term market validation. Contract security, external dependencies, and the credit quality of re-stakers are all key factors determining whether this structure can continue to operate.

From this perspective, Cap resembles the experimental starting point of stablecoin 3.0. It is neither a simple payment medium nor just a redistribution of reserve interest, but rather aims to build a mechanism-driven stablecoin yield system. If this model can establish a foothold in practice, the definition of stablecoins may be rewritten: not only "stable," but also "yield-generating."

After all, what users ultimately care about may not be whether the mechanism is elegant, but rather: can this system provide me with real, sustainable on-chain yields?

Cap has already posed this question to the market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。