Cover image source: "The Great Era"

From Wall Street investment banks to tech companies in the Bay Area, and to financial giants and payment platforms in Asia, an increasing number of enterprises are eyeing the same business—stablecoin issuance.

Under the scale effect, the marginal issuance cost for stablecoin issuers is zero, and to them, it seems like a risk-free arbitrage game. In the current global interest rate environment, the interest rate spread is incredibly tempting; stablecoin issuers only need to deposit users' dollars into short-term U.S. Treasury bonds to earn a stable income of 4-5% annually, raking in billions of dollars effortlessly.

Tether and Circle have long proven that this path is viable, and as stablecoin regulations gradually take shape in different regions, the compliance pathways have become clearer. More and more companies are eager to try, with FinTech giants like PayPal and Stripe quickly entering the fray. Not to mention that stablecoins naturally possess the ability to integrate with payment, cross-border settlement, and even Web3 scenarios, offering immense imaginative potential.

Stablecoins have become a battleground for global financial companies.

But therein lies the problem; many people only see the "seemingly risk-free" arbitrage logic of stablecoins, overlooking that this is a capital-intensive, high-barrier business.

If a company wants to legally and compliantly issue a stablecoin, how much will it actually cost?

This article will break down the real costs behind a stablecoin, telling you whether this seemingly easy arbitrage business is worth pursuing.

The Costs Behind Stablecoin Issuance

In many people's minds, issuing a stablecoin is merely about creating an on-chain asset, which seems to have a low technical barrier.

However, launching a stablecoin with a compliant identity aimed at global users involves a far more complex organizational structure and system requirements than one might imagine. It not only involves financial licenses and audits but also includes significant capital investments in areas such as fund custody, reserve management, system security, and ongoing operations.

From a cost and complexity perspective, the overall construction requirements are comparable to those of a medium-sized bank or a compliant trading platform.

The first hurdle faced by stablecoin issuers is the construction of a compliance system.

They often need to simultaneously address regulatory requirements from multiple jurisdictions, obtaining key licenses such as the U.S. MSB, New York BitLicense, EU MiCA, and Singapore VASP. Behind these licenses are detailed financial disclosures, anti-money laundering mechanisms, and ongoing monitoring and compliance reporting obligations.

In comparison to medium-sized banks with cross-border payment capabilities, stablecoin issuers often face annual compliance and legal expenses reaching tens of millions of dollars just to meet the most basic qualifications for cross-border operations.

In addition to licenses, building a KYC/AML system is also a hard requirement. Project teams typically need to engage mature service providers, compliance consultants, and outsourced teams to continuously operate a full set of mechanisms for customer due diligence, on-chain reviews, and address blacklist management.

In today's tightening regulatory environment, it is nearly impossible to gain access to major markets without establishing robust KYC and transaction review capabilities.

Market analysis indicates that HashKey's total costs for applying for a Hong Kong VASP license can reach between 20 million to 50 million HKD, and they must have at least two regulatory officers (ROs) and collaborate with the "Big Three" accounting firms, with costs several times higher than in traditional industries.

Beyond compliance, reserve management is also a key cost in stablecoin issuance, covering both fund custody and liquidity arrangements.

On the surface, the asset-liability structure of stablecoins does not seem complex; users deposit dollars, and the issuer purchases an equivalent amount of short-term U.S. Treasury bonds.

However, once the reserve scale exceeds 1 billion or even 10 billion dollars, the operational costs behind it will rise rapidly. Just for fund custody, annual fees could reach tens of millions of dollars; while Treasury bond trading, clearing processes, and liquidity management not only incur additional costs but also heavily rely on the collaboration of professional teams and financial institutions.

More critically, to ensure an "instant redemption" user experience, issuers must prepare sufficient off-chain liquidity positions to handle large redemption requests during extreme market conditions.

This configuration logic is very close to the risk preparation mechanisms of traditional money market funds or clearing banks, far from the simplicity of "smart contract locking."

To support this structure, issuers must also establish highly stable and auditable technical systems that cover key financial processes both on-chain and off-chain. This typically includes smart contract deployment, multi-chain minting, cross-chain bridge configuration, wallet whitelisting mechanisms, clearing systems, node operations, security risk control systems, and API integrations.

These systems not only need to support large-scale transaction processing and fund flow monitoring but also must be scalable to adapt to regulatory changes and business expansion.

Unlike the "lightweight deployment" of typical DeFi projects, the underlying systems of stablecoins essentially serve as a "public settlement layer," with technical and operational costs often reaching millions of dollars annually.

Compliance, reserves, and systems are the three foundational projects of stablecoin issuance, collectively determining whether the project can achieve long-term sustainable development.

Essentially, stablecoins are not merely a technical tool product but a financial infrastructure that combines trust, compliance architecture, and payment capabilities.

Only those enterprises that truly possess cross-border financial licenses, institutional-level clearing systems, on-chain and off-chain technical capabilities, and controllable distribution channels are likely to operate stablecoins as a platform-level capability.

For this reason, before deciding whether to enter this field, companies must first assess whether they have the ability to build a complete stablecoin system, including: Can they obtain ongoing recognition from multiple regulatory bodies? Do they have their own or trusted custodial fund systems? Can they directly control wallet, trading platform, and other channel resources to truly facilitate circulation?

This is not a light-hearted entrepreneurial opportunity but a hard battle that demands high capital, systems, and long-term capabilities.

So, What Happens After Issuing a Stablecoin?

Completing the issuance of a stablecoin is just the beginning.

Regulatory permissions, technical systems, custody structures—these are merely prerequisites for entry. The real challenge is how to make it circulate.

The core competitiveness of stablecoins lies in "whether anyone uses it." Only when stablecoins are supported by trading platforms, integrated into wallets, connected to payment gateways and merchants, and ultimately used by users can they be considered truly circulated. Along this path, there are also high distribution costs awaiting them.

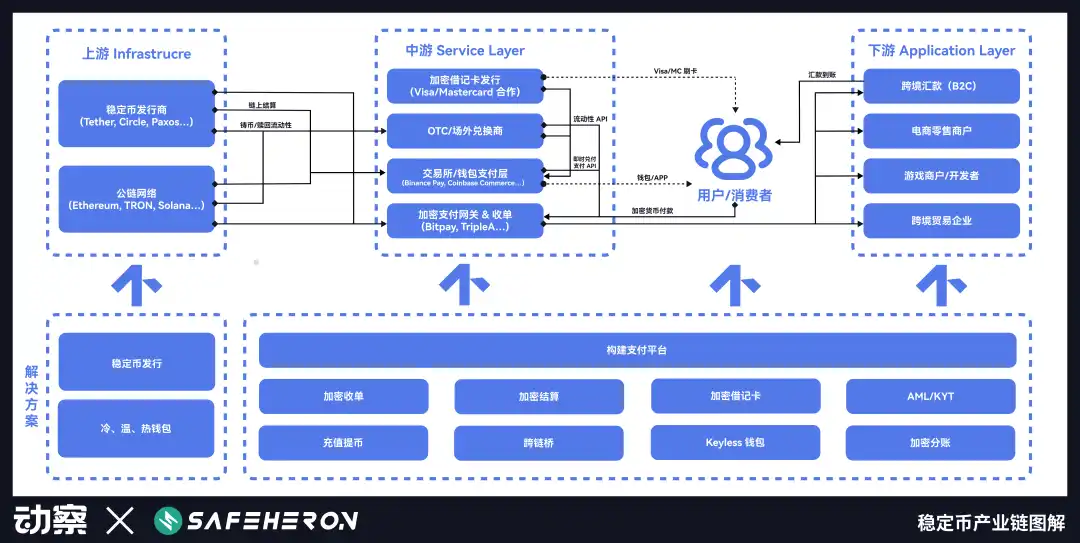

In the stablecoin industry chain diagram released by Beating in collaboration with digital asset self-custody service provider Safeheron, it is clear that stablecoin issuance is just the starting point of the entire chain, and to enable stablecoins to circulate, attention must be directed towards the mid-to-lower reaches.

Taking USDT, USDC, and PYUSD as examples, we can clearly see three distinctly different circulation strategies:

- USDT initially relied on gray market scenarios to build an unreplicable network effect, quickly occupying a market standard position due to its first-mover advantage;

- USDC primarily expanded through channel partnerships within a compliant framework, relying on platforms like Coinbase;

- Even with PayPal backing, PYUSD still needs to rely on incentive mechanisms to drive TVL and has always struggled to penetrate real usage scenarios.

Their paths differ, yet they all reveal the same fact—competition in stablecoins lies not in issuance but in circulation. The key to success or failure is whether they have the capability to build a distribution network.

1. The Unreplicable First-Mover Structure of USDT

The birth of USDT stemmed from the real dilemmas faced by crypto trading platforms at that time.

In 2014, the Hong Kong-based cryptocurrency trading platform Bitfinex rapidly expanded globally, but traders wanted to trade in dollars while the platform lacked stable dollar deposit channels.

The cross-border banking system was hostile to cryptocurrencies, making it difficult for funds to flow between Hong Kong, Taiwan, and mainland China, with accounts frequently being shut down, leaving traders at risk of losing access to their funds at any moment.

Against this backdrop, Tether was born. It initially operated on the Omni protocol based on Bitcoin, with a simple and direct logic: users wire dollars to Tether's bank account, and Tether then issues an equivalent amount of USDT on-chain.

This mechanism bypassed traditional banking clearing systems, allowing "dollars" to circulate across borders 24/7 for the first time.

Bitfinex was Tether's first important distribution node, and more importantly, both were operated by the same group of people. This deep binding structure allowed USDT to quickly gain liquidity and use cases in its early days. Tether provided Bitfinex with a compliance-ambiguous but efficient dollar channel. They conspired together, with information symmetry and aligned interests.

From a technical perspective, Tether is not complex, but it solved the pain points of crypto traders regarding fund inflows and outflows, which became key to occupying users' minds early on.

As capital market volatility intensified in 2015, the appeal of USDT rapidly magnified. A large number of users from non-dollar regions began seeking dollar alternatives to bypass capital controls, and Tether provided them with a "digital dollar" solution that required no account opening, no KYC, and could be used wherever there was internet access.

For many users, USDT was not just a tool but a means of hedging.

The ICO boom of 2017 was a critical moment for Tether to achieve product-market fit (PMF). After the Ethereum mainnet went live, ERC-20 projects surged, and trading platforms shifted to crypto asset trading pairs, making USDT the "dollar substitute" in the altcoin market. By using USDT, traders could freely navigate between platforms like Binance and Poloniex to complete trades without repeatedly moving funds in and out.

Interestingly, Tether has never actively spent money on promotion.

Unlike typical stablecoins that adopt subsidy strategies to expand market share in their early stages, Tether has never actively subsidized trading platforms or users for using its services.

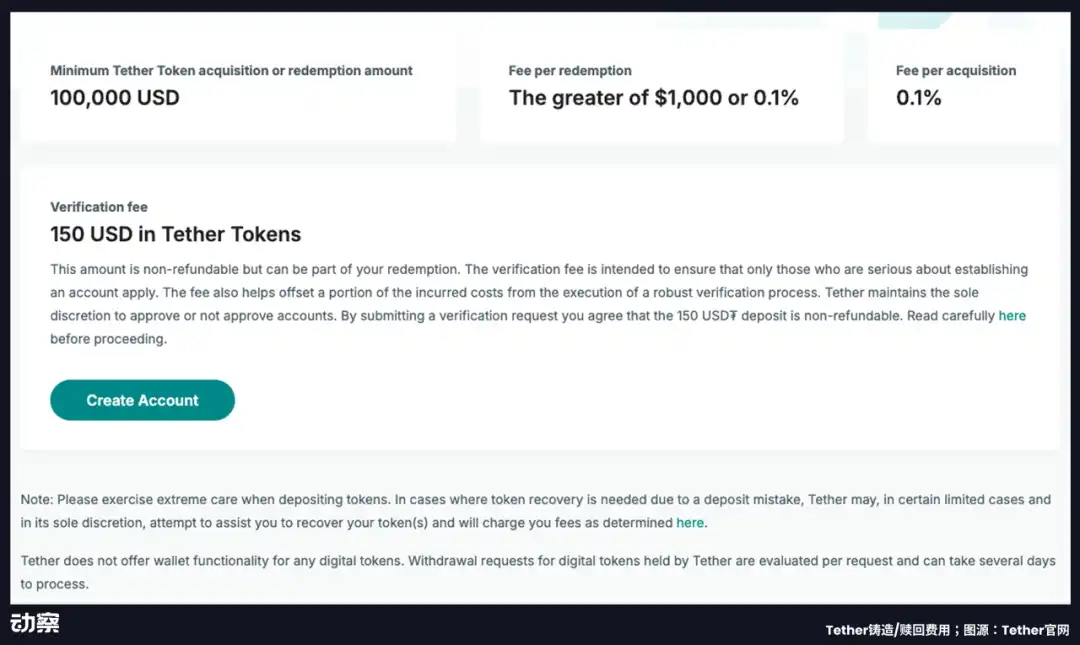

On the contrary, Tether charges a 0.1% fee for each minting and redemption, with a minimum redemption threshold of 100,000 dollars, plus an additional verification fee of 150 USDT.

For institutions wishing to directly access its system, this fee structure almost constitutes a "reverse promotion" strategy. Because it is not promoting a product but setting a standard. The cryptocurrency trading network has long been built around USDT, and any participant wishing to access this network must align with it.

After 2019, USDT has almost become synonymous with "on-chain dollars." Despite facing regulatory scrutiny, media skepticism, and reserve controversies, USDT's market share and circulation continue to rise.

By 2023, USDT has become the most widely used stablecoin in non-U.S. markets, especially in global southern countries. Particularly in high-inflation areas such as Argentina, Nigeria, Turkey, and Ukraine, USDT is used for wage settlements, international remittances, and even as a substitute for local currencies.

Tether's true moat has never been its code or asset transparency, but rather the trust pathways and distribution networks it established in the Chinese-speaking crypto trading community in its early years. This network started in Hong Kong, using Greater China as a springboard, and gradually extended to the entire non-Western world.

This "first-mover becomes the standard" advantage means that Tether no longer needs to prove who it is to users; instead, the market must adapt to the circulation system it has already established.

2. Why Circle Relies on Coinbase

Unlike Tether, which grew naturally in gray market scenarios, USDC was designed from the outset as a standardized and institutionalized financial product.

In 2018, Circle partnered with Coinbase to launch USDC, aiming to create a "on-chain dollar" system for institutions and mainstream users within a compliant and controllable framework. To ensure governance neutrality and technical collaboration, both parties held 50% shares and established a joint venture named Center, responsible for the governance, issuance, and operation of USDC.

However, this governance joint venture model does not solve the key issue—how can USDC truly circulate?

……

Read the full article on the Dongcha Beating public account

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。