Original | Odaily Planet Daily (@OdailyChina)

Author | Ethan (@ethanzhangweb3)_

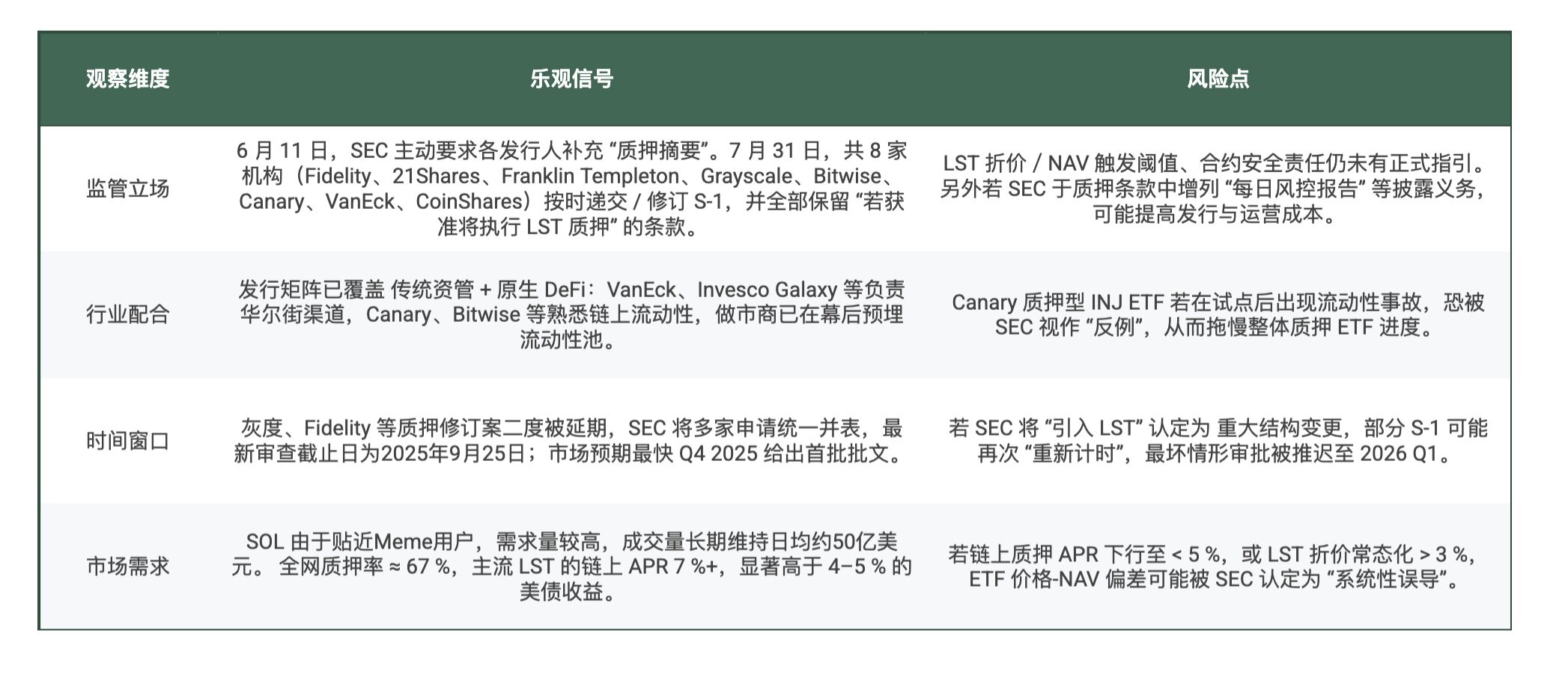

On May 20 this year, the SEC first pressed the pause button, requiring 21 Shares, Bitwise, VanEck, and Canary Capital to wait on their spot Solana ETF—stating that “more time is needed to assess legal and policy issues.”

Less than a month later, the winds changed. On June 11, several insiders revealed that the SEC had verbally notified all potential issuers that “revised S-1 must be submitted within a week, and comments will be provided within 30 days,” specifically requesting additional descriptions of “physical redemption” and “staking”—clearly implying that “staking is negotiable”;

Soon, major asset managers collectively responded: Franklin Templeton, Galaxy, Grayscale, VanEck, Fidelity and six other institutions submitted updated S-1s on June 13-14; for the first time, the SEC's documentation included the term “Staked ETP,” with staking becoming one of the chapter titles.

On June 16, CoinShares joined the fray, becoming the eighth applicant; on June 24, Grayscale noted a 2.5% management fee in the new S-1, betting on “high fees + strong brand” to be the first to pass.

Entering July, the pace of the SOL ETF clearly accelerated:

- July 7—CoinDesk reported: the SEC set a “hard deadline at the end of July” to aim for approval of the first batch of spot SOL ETFs before October 10;

- July 8—Fidelity's application was delayed by 35 days, “awaiting additional materials”;

- July 28—Grayscale's application was postponed again, with a new final deadline set for October 10;

- July 29—Cboe BZX submitted two 19b-4 applications at once: ①Canary Staked INJ ETF; ②Invesco × Galaxy spot Solana ETF, clearly indicating “spot + staking” as a double assurance;

- July 31— ①Jito Labs + Bitwise + Multicoin + VanEck + Solana Institute submitted an open letter to the SEC's special working group on crypto assets, officially endorsing “Staked ETP”; ②21 Shares simultaneously submitted a revised S-1 that included staking terms at the last minute (see SEC archived documents).

Thus, within two months, there was a back-and-forth of “two delays + three rounds of revisions + four new applications”—bringing us to the core issue we will discuss today: Is it feasible to include Liquid Staking Tokens (LST) in an ETF?

Why: Why are LSTs eager to enter ETFs?

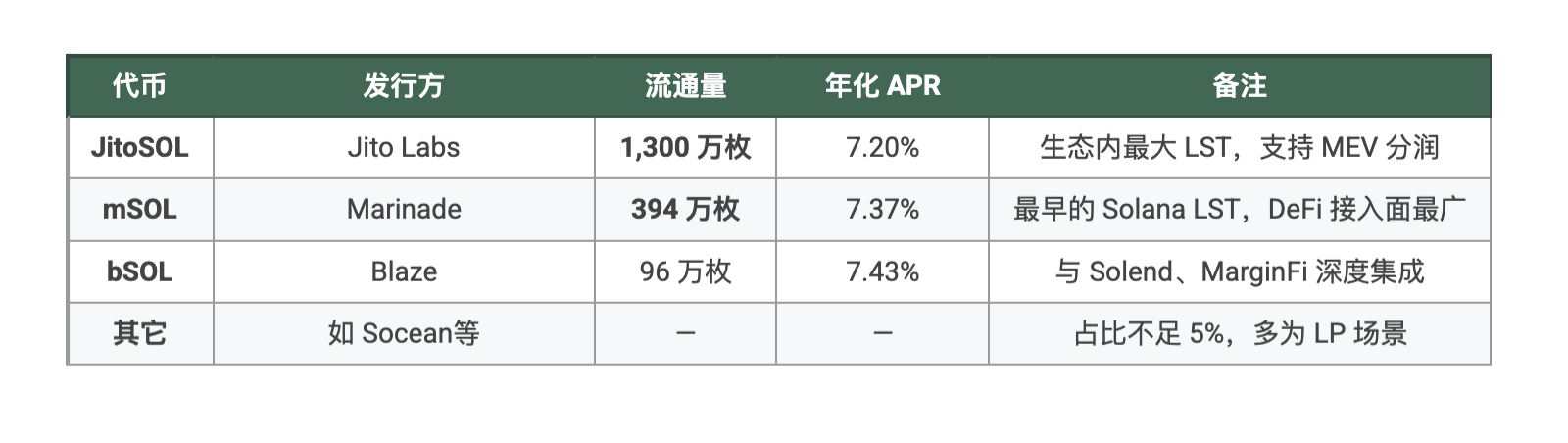

LST List and Current Status

Note: APR data from LST issuers' official websites as of August 1, this data may change in real-time, subject to actual presentation.

Threefold Benefits

Passive Funds = Long-term Lockup

The larger the ETF, the more it can turn LSTs into a “fund pool that unintentionally reduces positions but continues to earn returns.” For Jito and Marinade, this equates to a direct addition of “billions” in long-term staking volume, allowing the protocol to stabilize its commission and naturally boost TVL.

Liquidity Depth Leap

ETFs will continuously trade in the secondary market, while the LST corresponding to fund shares requires daily subscriptions and redemptions for market making—market makers will simultaneously establish depth for LST/SOL and LST/USDC, providing LST with thicker support than DeFi pools.

Brand Credit Spillover

Entering the SEC compliance framework means “being endorsed by Wall Street.” Once public documents like 10-K and N-CSR start to mention JitoSOL / mSOL, the due diligence costs for ordinary institutions will plummet, upgrading LST from “niche DeFi certificates” to “accountable financial assets.”

Impact Geometry? Three Main Lines of Analysis

For Solana: Dual Enhancement of Security and Valuation

- Staking Rate Increase—Based on 2025 H1 data estimates, if the first batch of spot SOL ETFs raises a total of $5 billion, with 80% allocated to LST, approximately 24 million staked SOL will be added on-chain at once (calculated at 167 USD/SOL), raising the staking rate from 66% to nearly 71%, with the network's Nakamoto coefficient also rising.

- Valuation Anchor “Yield”—Staking APR ≈ 7% becomes a segment of the DeFi risk-free yield curve. Buyers can simplify discounting using “current SOL price / 7%” rather than purely a Beta parabolic curve, which is more favorable for sector valuation.

For Other ETFs:

Conclusion: If the SOL LST ETF passes first, the ETH camp will be forced to detail the “native staking” terms more thoroughly, while the BTC ETF will have to continue relying on lowering fees to maintain attractiveness.

For ETF Buyers:

- One Ticket, Three Gains—Spot Beta + over 7% annualized + secondary market liquidity; for accounts with heavy compliance constraints like Family Offices / pensions, this is the first “buyable high-yield PoS” ticket.

- Tax & Settlement Friendly—Staking income is often taxed as capital gains rather than operating income within the 40 Act/33 Act structure, which is more favorable than personal on-chain staking.

- Fee Rate Game—Currently disclosed fee rates range from Grayscale's 2.5% to an expected 0.9% (speculated to be VanEck's framework), whoever offers more yield will attract more orders. The BTC ETF has already been pushed to 0.19-0.25%, and the fee war is bound to spread.

Call to Action: Will it pass? What are the risks?

Based on the above data, the probability of passing is estimated at 60-70%. At the same time, I believe that to pass smoothly, issuers should at least supplement three types of response plans in the S-1:

Plan One: Discount Circuit Breaker Threshold

It is recommended to set an upper limit on the deviation of the LST market price from the reference NAV (example: ± 5%); once the threshold is reached, pause primary market subscriptions/redemptions and initiate a “price adjustment” or cash creation backup process to ensure that fund shares align with the underlying asset value.

Plan Two: NAV Calculation and Calibration

At least two independent data sources should be introduced: one on-chain oracle (like Chainlink) + one compliant custodian/market maker quote (like Coinbase Prime, Cumberland, etc.); it is recommended to update every 10 seconds and disclose redundancy and failover plans to facilitate regulatory assessment of price distortion risks.

Plan Three: Contract Risk Coverage

At the smart contract level, in addition to annual third-party audits, consider purchasing policies from Lloyd’s of London, Nexus Mutual or similar levels to cover extreme scenarios like hacking attacks and staking penalties; and clearly outline claims processes, coverage limits and triggering conditions in the prospectus, allowing investors and regulators to have a quantitative expectation of potential losses.

(Note: The above measures are a “reference framework” proposed by the author based on public cases and industry practices; specific thresholds and technical routes still need further communication and determination between the issuer and the SEC.)

Conclusion

From being “blacklisted” in May to “stimulated” in July, the SEC completed a posture reversal in just 70 days: it is no longer entangled in “whether it can go up,” but has begun discussing “how to go up”—“In the footnotes of crypto ETF 2.0, staking and LST are mentioned for the first time.” On the other side of the table, crypto players have told Wall Street with “an open letter + a revised S-1”: “Maximizing capital efficiency, we understand it better than you.” The next step is to see if regulators are willing to let this “high-yield, low-operation” staking game truly enter pensions and 401(k)s.

If it is really approved, it will not only be a victory for Solana but also a milestone for the PoS narrative moving from on-chain to exchanges, from geeks to institutions.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。