Original Title: Stablecoins and the Future of Payments

Original Source: Grayscale Research

Original Translation: AIMan@, Jinse Finance

Key Points of the Article:

● Stablecoins are digital tokens pegged to the US dollar and issued on the blockchain. Through this structure, tokenized digital dollars can benefit from blockchain functionalities, including borderless payments, near-instant settlement, potentially lower transaction costs, and high transparency.

● Stablecoins are ubiquitous in the cryptocurrency trading space but are now also being used for traditional payments. Currently, the circulation of stablecoins is approximately $250 billion, and stablecoin issuers are now major holders of US Treasury securities. The blockchain processes over 100 million stablecoin transactions monthly.

● While traditional payment systems are generally very efficient, certain elements can be cheaper, faster, and/or offer more features. Based on its comparative advantages, Grayscale Research expects stablecoins to make the most progress in the following areas: (1) cross-border payments; (2) domestic payments in credit card-dominated markets like the US; and (3) value transfer between AI agents.

● Stablecoins are a core use case of public blockchains, and the rising adoption of stablecoins may benefit nearly all aspects of the cryptocurrency asset class to some extent.

● In specific blockchains, Ethereum seems poised to benefit from the rising adoption of stablecoins, as it already has the largest number of stablecoins and processes the most stablecoin transactions. This trend should extend to Ethereum's Layer 1 blockchain and its Layer 2 ecosystem. Other beneficiaries may include certain high-performance Layer 1 blockchains, related decentralized finance (DeFi) applications, and traditional financial service companies adopting stablecoin infrastructure.

● Grayscale Research believes that the passage of the "GENIUS Act" establishes a comprehensive regulatory framework for US stablecoins, marking a milestone for the cryptocurrency industry. The act aims to facilitate the integration of stablecoins into the US financial system while establishing safeguards to support financial stability, protect consumers, and curb illegal activities.

Improvements in the efficiency of payment systems benefit everyone, but fundamental changes are difficult to achieve. Payment systems are essentially a network of numerous participants, so reform efforts may face significant coordination challenges. Even seemingly obvious improvements—such as universal information transmission standards and overlapping business hours between global banks—are difficult to implement. Over the past five years, the G20 has been explicitly committed to improving cross-border payments—especially frustrating for users—but progress has been slow.

Stablecoins are an emerging innovation in the digital payments space based on blockchain technology. Like most crypto applications, the adoption of stablecoins is a bottom-up phenomenon: a diverse range of users around the world benefit from using stablecoins for transactions and/or storing value. The "GENIUS Act" was signed into law by President Trump on Friday, July 18, providing a comprehensive regulatory framework for payment stablecoins in the US. This legislation, along with similar efforts in other countries, will enable stablecoins to integrate more deeply into the traditional financial system while establishing appropriate safeguards for financial stability, consumer protection, and preventing illegal activities.

Grayscale Research believes that stablecoins can disrupt certain aspects of the global payments industry by providing lower costs, faster settlement times, and higher transparency. We expect stablecoins to make the most progress in the following areas: (1) cross-border payments; (2) domestic payments in credit card-dominated markets like the US; and (3) value transfer between AI agents. Stablecoins also represent a way to hold digital value and may partially eliminate the intermediary role of commercial bank deposits. In the crypto ecosystem, the biggest beneficiaries may be stablecoin issuers and their distribution partners (who earn net interest margin NIM), as well as blockchains in the Ethereum ecosystem, certain other high-performance Layer 1s, and related decentralized finance (DeFi) applications, such as oracle services and decentralized exchanges (DEX).

Digital Dollars on the Blockchain

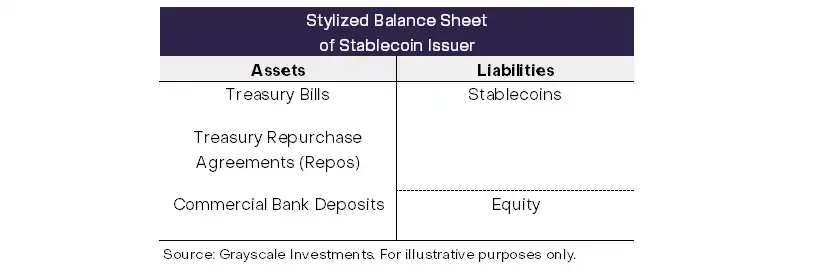

Stablecoins are digital tokens pegged to the US dollar and issued on the blockchain. There are many types of stablecoins (as described below), but mainstream users may only encounter one specific type: fully collateralized, fiat-backed stablecoins. These instruments are very similar to government-only money market funds: they are tokens that maintain a stable dollar value, fully backed by Treasury securities or similar collateral (Chart 1). The reason stablecoins can maintain their peg to the dollar is that stablecoin issuers are always ready to redeem stablecoins at face value or issue more stablecoins in exchange for cash. This is a very simple structure and is not particularly interesting as an innovation. However, when tokenized digital dollars are deployed on public blockchains, they gain blockchain functionalities, including borderless payments, near-instant settlement, potential low costs, and high transparency.

Chart 1: Regulated US Payment Stablecoins Will Have a Simple Structure

Today, stablecoins are ubiquitous in cryptocurrency trading. For example, stablecoins account for 70%-80% of the trading volume of crypto tokens traded on centralized exchanges (CEX). Therefore, the growth in cryptocurrency trading volume is likely to lead to an increase in stablecoin balances and transaction volumes. Stablecoins are also the primary tool for users to access DeFi applications (such as decentralized lending protocols). However, stablecoins are now also being used for traditional digital payments, especially in emerging market economies. This use case is unrelated to speculative cryptocurrency trading and may support sustainable growth of blockchain applications.

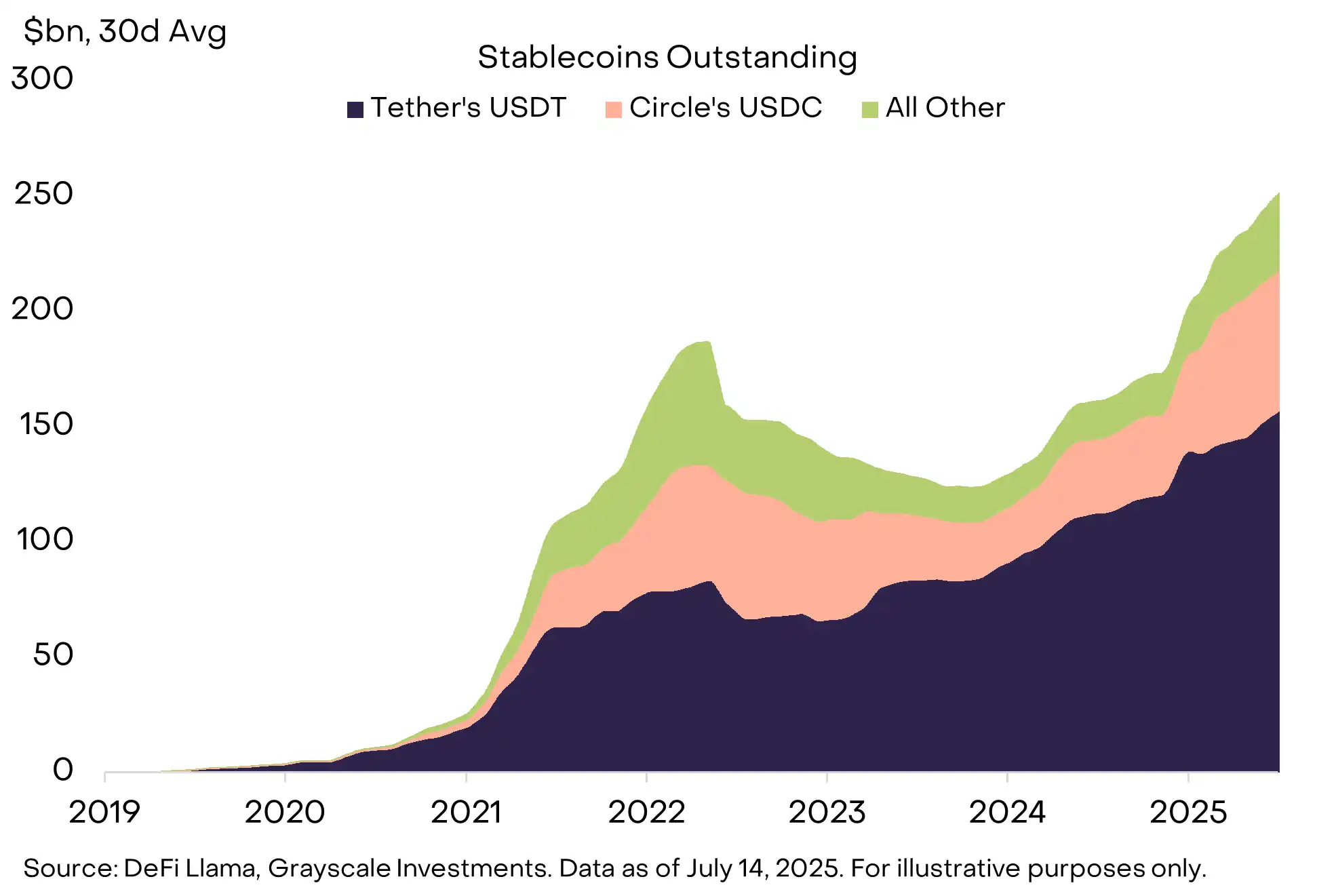

Although issuers have created stablecoins for various currencies, the $250 billion in circulation is almost entirely made up of US dollar stablecoins. Two issuers dominate the US dollar stablecoin market: Tether, the issuer of the USDT stablecoin, and Circle, the issuer of the USDC stablecoin (see Chart 2). Tether is registered overseas, and its USDT accounts for about 60% of the total "market cap" of stablecoins. Circle is registered in the US, and its USDC accounts for about 25% of the total market cap of stablecoins. Tether's reserve assets are currently the largest holders of US Treasury securities: if it were a country, it would be the 18th largest foreign holder of US Treasuries, just behind Saudi Arabia and ahead of South Korea.

Chart 2: The Largest Stablecoins are USDT and USDC

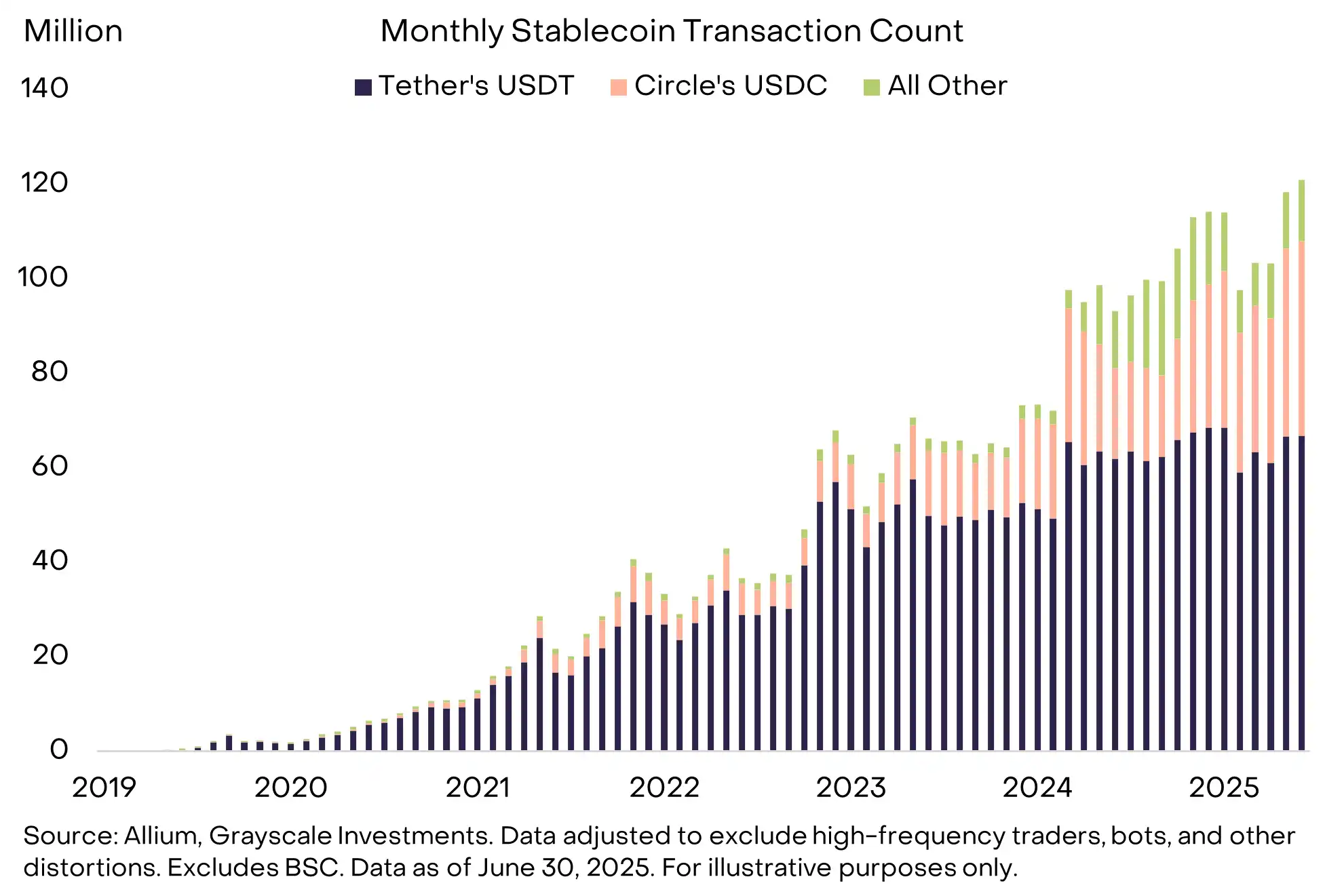

There is currently no perfect metric for measuring stablecoin transaction volume, but a coalition of crypto data experts has partnered with Visa to create a widely used benchmark aimed at eliminating certain types of biases (such as high-frequency traders and bots). According to these estimates, users conducted over 120 million stablecoin transactions in June 2025 (Chart 3). The total value transferred was approximately $800 billion, annualized to nearly $10 trillion. In comparison, the Visa network processed about $130 trillion in payments in 2024. It is important to clarify that these transactions involve both crypto trading and payment use cases, and on-chain data alone cannot distinguish between them. Currently, the vast majority of stablecoin transactions may still be related to crypto trading (possibly up to 90%), rather than payments for goods and services.

Chart 3: Over 100 Million Stablecoin Transactions Monthly

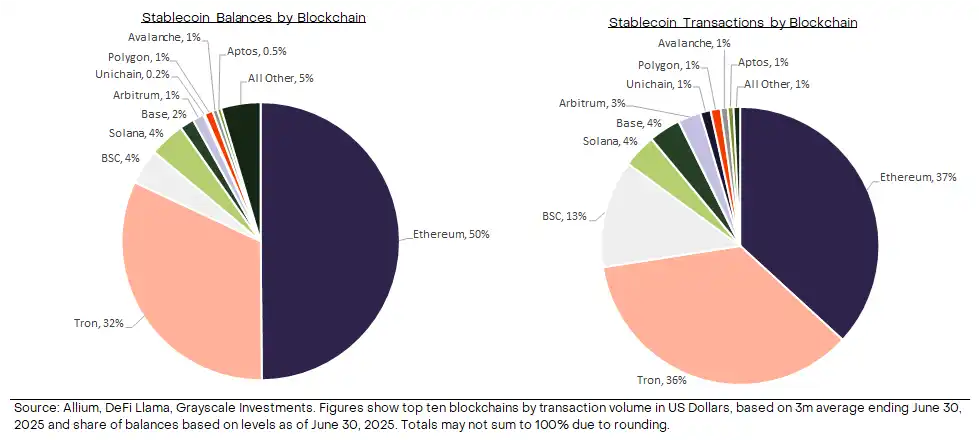

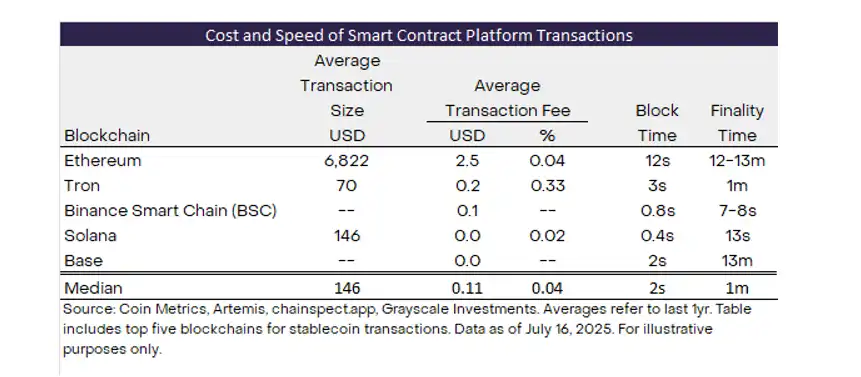

Most smart contract platform blockchains use stablecoins, but the current leaders in this category are Ethereum and Tron (Chart 4). About half of the stablecoin balances are on Ethereum, including USDT and USDC; nearly all stablecoin balances on Tron consist of USDT. So far this year, Ethereum and Tron have processed approximately $1.7 trillion in stablecoin transactions; the majority of transactions on Tron use Tether's USDT stablecoin (>99%), while the majority of transactions on Ethereum use Circle's USDC stablecoin (about 65%).

Chart 4: Ethereum and Tron are the Leading Stablecoin Blockchains Today

The Slow Lane of Traditional Payments

The modern global economy relies on effective payment systems, and the existing infrastructure operates well enough to maintain smooth functioning. At the same time, there are still areas for improvement. The most obvious example is cross-border payments—this is also why the G20 has explicitly focused on this issue—but certain domestic payment networks also suffer from inefficiencies. Additionally, the growth of AI agent trading will place new demands on the payment infrastructure of economies. Stablecoins can help improve efficiency in the global payments space and may reduce costs for consumers and businesses.

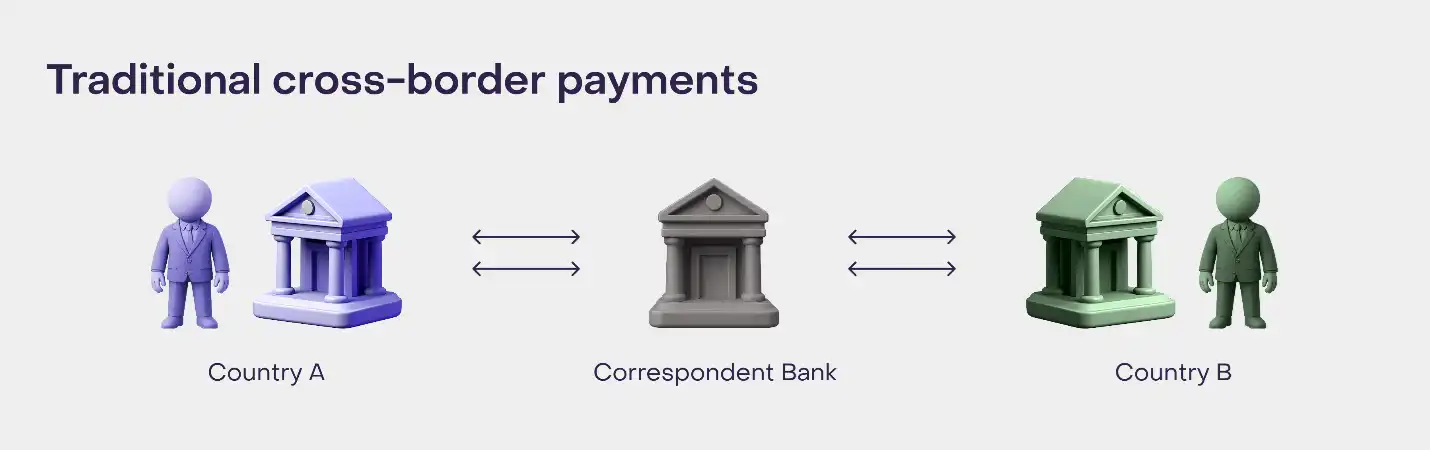

Cross-border payments involve financial institutions (and their regulators) from multiple countries, making them generally more complex than domestic payments. Due to this complexity, cross-border payments often incur higher costs, slower settlement speeds, and are often opaque to users. The most common type of cross-border payment involves correspondent banks, which open accounts for partner banks in various domestic markets and are responsible for settling transactions between them (Chart 5). In some cases, multiple correspondent banks connect financial institutions in distant markets.

Chart 5: Cross-Border Payments Involve Multiple Intermediaries

Source: Grayscale Investments. For reference only.

Each additional intermediary in the process adds potential costs and delays. The Financial Stability Board (FSB) reports aggregated data on cross-border payment costs in its annual report. Excluding remittances, the average cost of personal-to-business cross-border payments in 2024 is 2%, while the average cost of personal-to-person cross-border payments is about 2.5%. For remittances, the average cost is about 5%. For many cross-border payments, speed is not an issue: according to the FSB's annual report, about 70% of retail payments can be completed within one business day of the payment initiation. However, there are also some payment channels with average processing times exceeding two days, potentially lasting up to 10 days. In these cases, stablecoins can offer lower costs and faster settlement times.

We believe that there is room for improvement in domestic payment systems in the US and other countries, which are currently dominated by credit card networks. The concentration of credit card networks may allow providers to maintain profits, while regulators and elected officials often explore ways to reduce costs. Stablecoins can increase competition in these markets and help lower costs for users.

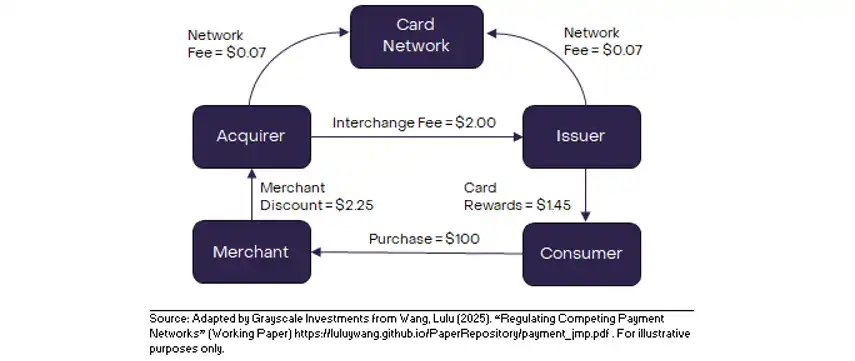

The diagram below shows the typical structure of credit card payments in the US and the flow of associated fees. When a consumer spends $100, the merchant typically receives $97.75 and pays the remaining $2.25 (the so-called merchant discount) to the issuing bank (the financial institution processing the transaction on behalf of the merchant). A portion of this amount ($1.45) is returned to the consumer in the form of credit card rewards. The remaining portion ($0.80) is earned as revenue by the banks and credit card companies that make up the credit card network. While many consumers appreciate the credit card rewards that this system provides, merchants may be motivated to seek alternative forms of digital payment. Additionally, policymakers may be concerned that this system benefits cardholders (who receive rewards) while cash users (who still pay the same final retail price in most cases) are disadvantaged.

Chart 6: Credit Card Payments Involve Various Fees

Finally, traditional payment systems are less suitable for AI agents—autonomous software capable of acting independently and executing complex instructions. As non-human actors, AI agents cannot legally own or operate bank accounts. In contrast, blockchain allows AI agents to autonomously control wallets and allocate financial resources. Blockchain also supports near-instant microtransactions, while traditional systems require days for settlement and incur high costs. Therefore, stablecoin payments on the blockchain can both enhance the functionality of AI agents and significantly expand their scope. While this is a new use case for global payment systems, some analysts expect it to grow rapidly in the coming years, potentially making AI agent payments a primary use case for stablecoins.

Same Goods, Different Tracks

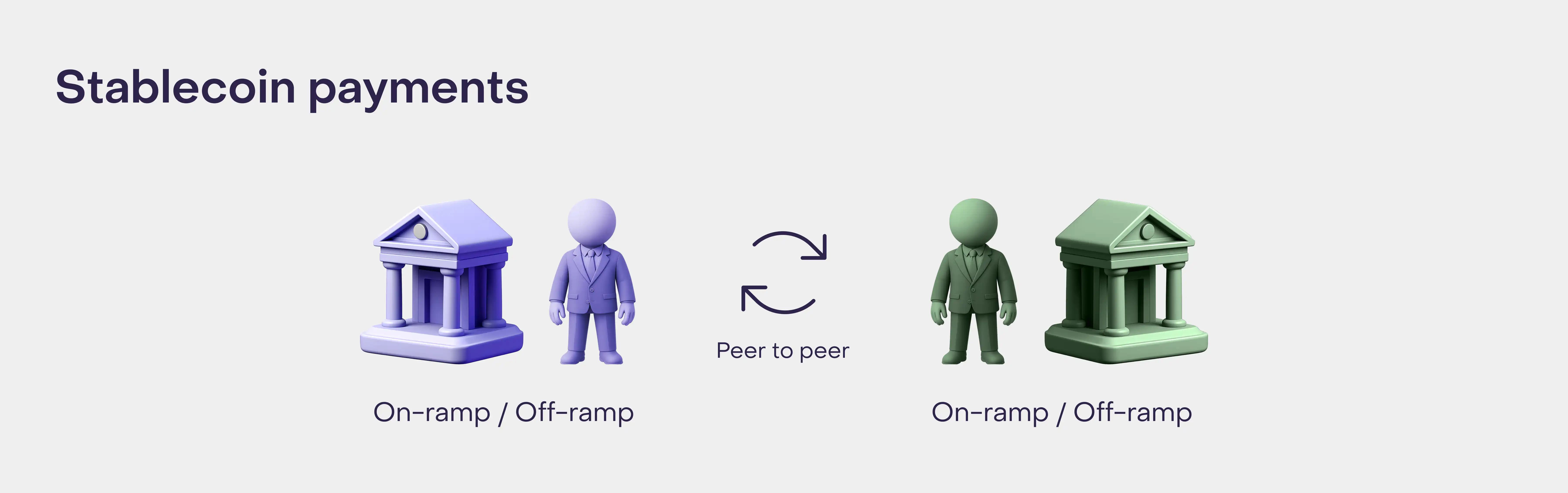

Stablecoins on public blockchains provide a fundamentally different architecture for digital payments. In payment industry terms, stablecoins are an innovation in the "back end" (the underlying infrastructure layer), while many recent innovations have focused on the "front end" (the user interface layer). Transfers of stablecoins on the blockchain are entirely peer-to-peer, requiring no intermediaries to process transactions (Chart 7). However, users may need to "onboard" funds to the blockchain through financial institutions before they can "offboard" funds for use. If stablecoin payments can offer (1) lower end-to-end total costs, (2) faster speeds, and/or (3) lower payment failure risks, users will choose them.

Chart 7: Stablecoin Payments are Peer-to-Peer

Source: Grayscale Investments. For reference only.

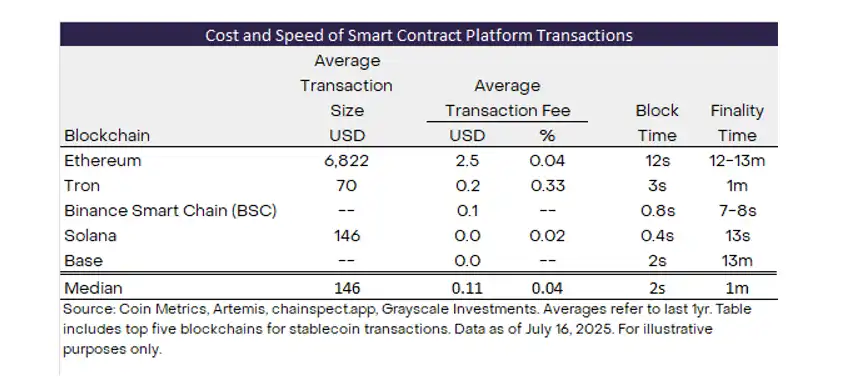

Smart contract platform blockchains process transactions relatively quickly and at lower costs (Chart 8). The transaction costs on blockchains do not increase in a 1:1 ratio with transaction value, so the percentage of fees for high-value transactions is often lower. For users who do not need to deposit or withdraw funds, stablecoins on public blockchains are already an efficient way to transfer digital value globally. If the adoption rate of stablecoins continues to grow, and more merchants accept stablecoin payments for goods and services, the demand for bank payment channels may decline, allowing more users to enjoy the benefits of stablecoin transactions on the blockchain.

Chart 8: Smart Contract Blockchains Provide Fast and Cheap Transactions

However, in practice, most merchants have not yet accepted stablecoin payments, and users need to withdraw funds to use them. Therefore, when transacting with stablecoins, users need to consider the total end-to-end costs, including deposit/withdrawal costs. While this is technically a simple process, financial institutions often charge deposit/withdrawal fees to cover compliance costs: intermediaries are responsible for implementing anti-money laundering (AML) and counter-terrorism financing (CFT) policies and procedures, as well as any applicable sanctions-related restrictions and other capital controls. Intermediaries may also need to bear costs associated with payment fraud and other administrative expenses. For all these reasons, the end-to-end costs of stablecoin transactions are not always cost-competitive with traditional payment methods.

Many large crypto financial institutions, such as Coinbase (the largest exchange in the US) and Mercado Bitcoin (the largest exchange in Latin America), offer zero-fee deposit and withdrawal services for stablecoins and other assets. For zero-fee deposit and withdrawal transactions, stablecoin transactions can be significantly cheaper than traditional payment methods. In other cases, the deposit/withdrawal fees per transaction are about 1%, in which case the cost/benefit will depend on the specific situation. In some other cases, these fees may exceed 5%, making stablecoins less cost-effective than traditional alternatives. Over time, lower average deposit/withdrawal costs may be a factor supporting the continued adoption of stablecoins.

Grayscale Research expects stablecoins to penetrate traditional payment sectors, but they are unlikely to be competitive across all market segments (especially in the short term, as some related blockchain infrastructure is still under development). Stablecoins already hold a dominant position in cryptocurrency trading and may further enhance it. In terms of payment use cases, we expect stablecoins to be most competitive in the following three areas:

Digital payments that are relatively slow, costly, and/or involve many financial intermediaries—most notably cross-border payments.

Network effects or lack of competition allowing intermediaries to maintain high profits in digital payments. This also includes cross-border payments, but we believe it also encompasses card-centric domestic payment systems like those in the US.

Public blockchain infrastructure providing unique advantages for digital payments, such as programmable payments and the ability to create new accounts with bank permission. These features are crucial for AI agent payments.

Market Opportunities

Accurately estimating the potential market size (TAM) for stablecoins is not easy, but data from existing payment systems can give us a rough idea of its possible scale. Chart 9 presents our rough estimates based on various sources. The global payment industry processes 20-30 trillion transactions annually, with a total value of $1,000-2,000 trillion (i.e., $1-2 quadrillion). The industry's revenue is about $2 trillion, roughly divided into net interest margin (NIM) and transaction fees.

Chart 9: The Global Payment Industry Processes 20-30 Trillion Transactions Annually

In contrast, the stablecoin industry remains small. Currently, the total volume of stablecoin transactions is about 100 million per month (approximately 0.05% of traditional payments), with a total value of about $800 billion per month (approximately 0.5%-1.0% of traditional payments).

Based on a 4%-5% cash interest rate in the US and $250 billion in non-interest-bearing stablecoins, stablecoin issuers may earn about $10 billion to $12 billion in total interest income annually. Most stablecoins do not pay interest, so total interest and net interest income (NIM) may be comparable (although stablecoin issuers have other operating expenses). We estimate that the blockchains processing stablecoin transactions may earn only about $500 million annually from such activities (excluding fees from other transactions). Therefore, the total revenue of the stablecoin industry is only about 0.5% of the revenue of the traditional payment industry.

The rising adoption rate of stablecoins should support net interest margins (NIM) and transaction revenues. According to the "GENIUS Act," US-regulated payment stablecoins cannot pay interest directly. Therefore, stablecoin issuers may be able to temporarily maintain healthy net interest margins (NIM). However, competitive pressures may eventually lead to some interest income being shared with distribution partners (such as Circle's partnership with Coinbase) and ultimately shared with users. Thus, the growth rate of net interest income may be slower than the supply of stablecoins. The net interest income earned by stablecoin issuers primarily comes at the expense of commercial banks, as the digital dollars issued by commercial banks are currently used for public trading.

In contrast, we believe that the growth of transaction revenues should roughly align with the growth of transaction volumes. For example, if stablecoins account for 20% of the transaction volume processed by traditional payment channels, then the annual transaction volume would reach about 500 billion transactions. At a weighted average fee of $0.10 (see Chart 8), 500 billion transactions would equate to $50 billion in transaction fees annually—approximately 100 times the revenue currently earned by smart contract platform blockchains from stablecoin activities.

Ethereum hosts the largest number of stablecoins and processes the most stablecoin transactions. It also encompasses USDC, USDT, and some smaller stablecoins. Therefore, the Ethereum ecosystem is likely to benefit from the proliferation of stablecoins. This includes Ethereum Layer 1 (which may be better suited for high-value transactions and those requiring the highest security) and Ethereum Layer 2 (which offers low-cost and high-speed transactions). Currently, the largest Ethereum Layer 2 stablecoin networks are Base, Arbitrum, and OP.

However, stablecoin activity is unlikely to be limited to the Ethereum ecosystem. We believe that other high-performance blockchains may also see an increase in stablecoin activity, including Solana, Avalanche, Sui, and many others. These blockchains are favored by many users for their low costs, high transaction throughput, and/or excellent end-user experience. Especially in consumer-facing applications, these alternative Layer 1 blockchains may have advantages over Ethereum Layer 1 or Ethereum Rollup. Tron is closely associated with Tether's USDT stablecoin, so its competitive position may depend on whether Tether takes steps to qualify USDT as a regulated payment stablecoin under the new GENIUS Act framework or whether Tron can effectively diversify into other stablecoins.

Applications that constitute the core infrastructure of DeFi should also benefit from the adoption of stablecoins. There may be many specific examples, but we focus on leading oracle and messaging service Chainlink, as well as the leading Ethereum decentralized exchange Uniswap. Specialized service providers focused on stablecoins, such as Paxos, Ethena, and M0, are also expected to further popularize stablecoins.

Fintech Companies Taking Action

Traditional fintech companies and increasingly traditional financial service firms have not missed the opportunity presented by stablecoins. Earlier this year, leading payment company Stripe finalized an $1.1 billion deal to acquire stablecoin infrastructure provider Bridge, marking its largest acquisition to date. Bridge enables businesses to issue, use, and transfer stablecoins globally through its API. Today, Bridge's clients range from startups to multinational corporations, such as SpaceX, which uses stablecoins for fund management, and ScaleAI, which uses stablecoins to pay its global contractors.

Stripe has also recently acquired crypto wallet and deposit/withdrawal service provider Privy. Stripe's vision is to make stablecoins an "extension layer" above the fiat currency system, thereby reducing the traditional financial friction faced by businesses and AI applications.

In addition to Stripe, other leading fintech companies involved in stablecoin development include PayPal (which launched its own stablecoin PYUSD in 2023, currently the tenth largest stablecoin by market cap) [30], Fiserv (which recently launched the FIUSD stablecoin), Robinhood, and Revolut (which is actively exploring the launch of stablecoins). Stablecoins have also been directly integrated into the platforms of several fintech companies, including Robinhood (to support weekend settlements), MoneyGram, Visa, and Mastercard.

Beneficiaries of stablecoin adoption may include existing companies that issue their own stablecoins and can leverage distribution advantages, or companies that integrate third-party resources to improve product services. We believe that key winners may include infrastructure providers like Stripe and Paxos, as well as low-cost deposit/withdrawal service providers like Coinbase and Mercado Bitcoin.

Ensuring System Security

The GENIUS Act provides a comprehensive regulatory framework for stablecoins in the US, expected to support the adoption of stablecoins while maintaining financial stability, protecting consumer rights, and preventing the financial system from being used for illegal activities. However, it is important to emphasize that most stablecoins have proven effective in maintaining their peg to the US dollar before a robust regulatory framework is established. Additionally, global regulators have provided detailed compliance guidelines for stablecoin issuers and related service providers, and these agencies regularly collaborate with law enforcement.

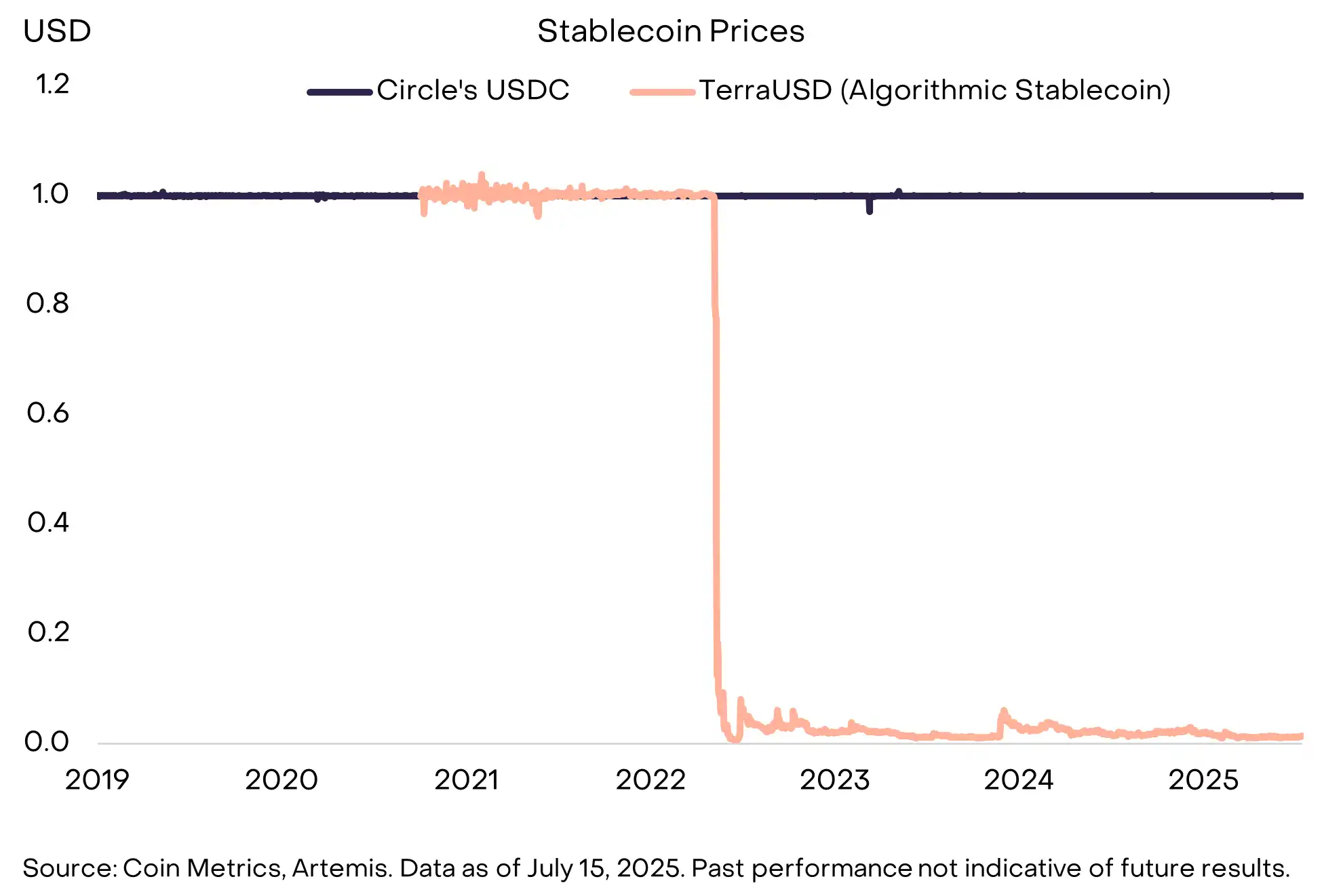

In 2022, the collapse of the Terra USD stablecoin, which saw its circulating supply grow to over $18 billion, was a significant blemish on the stablecoin industry. According to the GENIUS Act, such "algorithmic" stablecoins cannot be used as regulated payment stablecoins and will not be integrated into mainstream consumer finance applications. Stablecoins fully backed by fiat assets (such as government bonds and cash), like Circle's USDC, have consistently maintained their pegged exchange rate effectively (Chart 10). For example, since September 2018, USDC's price has fallen below $1.00 for less than 1% of the time and has only dropped more than 1% from $1.00 on one day. Similar to government money market funds and currency boards in foreign exchange, stable value instruments backed by safe and liquid collateral typically maintain their pegged exchange rates effectively. Furthermore, these narrow structures do not require the deposit insurance systems of commercial banks or central bank discount window lending systems to support risk-bearing.

Chart 10: Failed Stablecoins are Exceptions, Not the Norm

According to the GENIUS Act, institutions authorized to issue stablecoins must hold reserves equivalent to at least 100% of the issued stablecoins and hold them in clearly identifiable asset forms. Acceptable reserve assets include US dollar currency, demand deposits, short-term government bonds (maturity ≤ 93 days), repurchase and reverse repurchase agreements backed by government bonds, shares in government money market funds, and central bank reserve deposits.

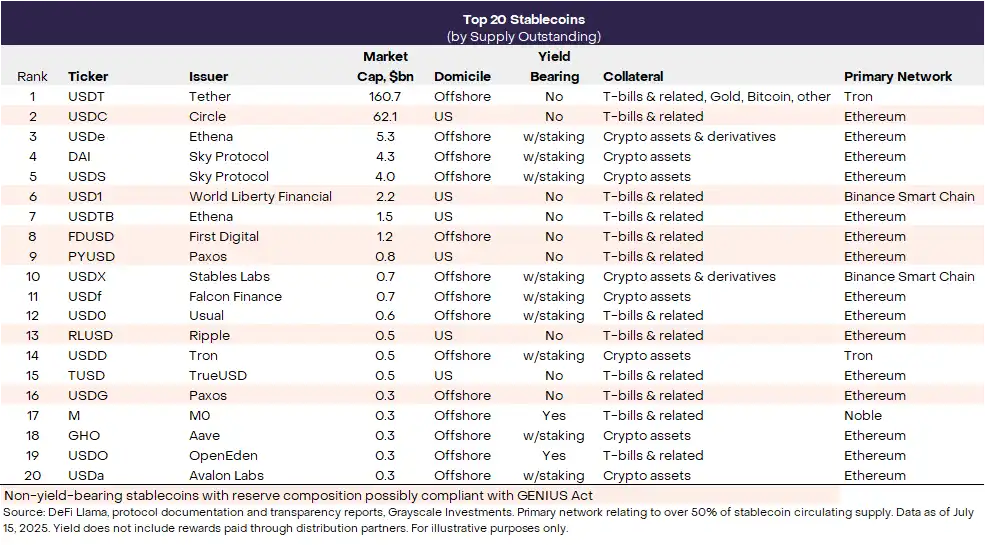

Under the GENIUS Act, stablecoins backed by other stablecoins (for example, stablecoins that include Circle USDC in their reserves) will not qualify as regulated payment stablecoins. Based on their current reserve composition, stablecoins backed by crypto assets (such as DAI) and/or stablecoins that include derivatives (such as USDe) will not qualify as US payment stablecoins (although they may take steps to gain qualification). This means that relatively few stablecoins appear to qualify as regulated US payment stablecoins based on their reserve composition (although issuers also need to register with regulators, maintain various compliance policies, and meet other requirements of the new law). Non-yielding stablecoins with potential compliant reserve structures include Circle's USDC, World Liberty's USD1, First Digital's FDUSD, PayPal's PYUSD, Ripple's RLUSD, and Paxos' USDG (Chart 11).

Chart 11: Top 20 Stablecoins

Additionally, the Financial Action Task Force (FATF), responsible for developing anti-money laundering and counter-terrorism financing policy rules, has issued guidelines on digital assets for about a decade. In practice, financial institutions engaged in digital asset operations must apply nearly all standard FATF policies, including Know Your Customer (KYC) policies and ongoing customer due diligence. This includes the Travel Rule, which requires service providers to record and transmit specific identity information about participants in crypto transactions. Stablecoin issuers must cooperate with law enforcement and freeze funds when requested. For example, in 2023, at the request of law enforcement, Tether froze $225 million worth of USDT; recently, Circle froze $58 million related to a memecoin.

The GENIUS Act also treats each authorized stablecoin issuer as a "financial institution" under the US Bank Secrecy Act (BSA), subjecting it to comprehensive anti-money laundering and sanctions rules. Issuing institutions must maintain risk-based anti-money laundering/counter-terrorism financing (AML/CFT) programs, designate compliance officers, monitor transactions, and submit Suspicious Activity Reports (SARs), retain records, verify customers according to KYC systems, and establish technical controls to block, freeze, or deny illegal transfers. The Treasury Department has been directed to develop targeted regulations, but the statutory responsibilities—customer due diligence, SAR reporting, and sanctions screening—are the same as those of banks.

Limitations on Stablecoin Adoption

Stablecoins are a popular innovation in the global payment infrastructure space, and we expect them to help reduce costs and bring new benefits to consumers. However, the adoption of stablecoins still faces limitations, partly because certain competitive payment innovations have proven effective. Additionally, the underlying blockchain infrastructure lacks some functionalities necessary for stablecoins to fully realize their potential.

Many major countries have seen the emergence of fintech platforms offering low-cost, near-instant retail payment services. These platforms include Alipay and WeChat Pay in China, UPI in India, and Pix in Brazil. Furthermore, some companies are working to connect these systems for more efficient cross-border payments. Other fintech companies focus on cross-border payments, including Revolut, Remitly, and Wise. When both parties have accounts on the platform, these services can provide cheap and fast cross-border payments. Ultimately, stablecoins may have to compete with tokenized deposits, which represent another structure for digital dollars on the blockchain. Tokenized deposits are a bank-centric framework that lacks some advantages of stablecoins (as digital bearer assets) but are favored by some regulators (and certainly by some banks).

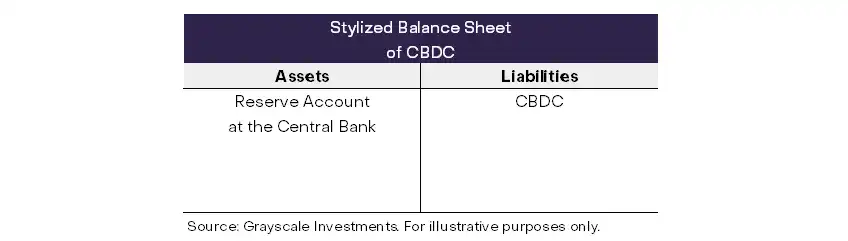

Ultimately, consumers may also have to choose between stablecoins and central bank digital currencies (CBDCs). The many possible types of CBDCs exceed the scope of this report. However, simply put, CBDCs are another type of digital token, but they are more directly pegged to fiat currency due to the claim on central bank money (see Chart 12). CBDCs may or may not circulate on public blockchains like Ethereum. Compared to stablecoins, the main advantage of CBDCs is that the digital token is more directly linked to the monetary system of the economy (rather than indirectly linked through safe collateral). However, some policymakers are concerned that CBDCs may lead to reduced privacy or introduce other risks. Last week, the US House also considered anti-CBDC legislation; the bill passed in the House by a vote of 219 to 210, with two Democrats voting in favor and Republicans holding the majority.

Chart 12: CBDCs Can Directly Access Central Bank Money

The biggest limitation on recent stablecoin applications may come from the underlying blockchain infrastructure itself. Over the past decade since Ethereum's launch, smart contract platforms have made significant progress, successfully processing millions of transactions daily. However, they still have some weaknesses in payments. For example, most blockchains do not default to privacy—every transaction is recorded on a public ledger—users may be reluctant to disclose their historical spending patterns with each payment. To fully realize the potential of stablecoins, blockchains may need systems that combine verifiable identity with privacy elements. Some researchers suggest using zero-knowledge proofs to embed this logic directly into the blockchain.

Like stablecoins, blockchain is an emerging technological innovation that is still developing. As blockchain technology matures with the support of a more robust regulatory framework, we believe it will bring numerous benefits to consumers and help enhance the efficiency of digital payments and other financial services.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。