Written by: kevin

Translated by: Luffy, Foresight News

Despite the cryptocurrency community's long-standing enthusiasm for tokenized assets and on-chain assets as a means to enhance accessibility, the most significant progress has actually come from the integration of cryptocurrencies with traditional securities. This trend is perfectly reflected in the recent surge of interest in "corporate crypto asset treasuries" in the public market.

Michael Saylor's Strategy was the first to implement this strategy, transforming his company into one with a market capitalization exceeding $100 billion, even outpacing Nvidia. We elaborated on this blueprint in our article about Strategy. The core logic of these financial strategies is that publicly traded stocks can obtain cost-effective unsecured leverage, which ordinary traders cannot access.

Recently, attention has expanded beyond Bitcoin to areas such as Ethereum-based treasury strategies, with increasing focus on Sharplink Gaming (SBET, led by Joseph Lubin) and BitMine (BMNR, led by Thomas Lee). But is the Ethereum treasury really reasonable? As we argued in our analysis of MicroStrategy, companies are essentially trying to arbitrage the long-term compound annual growth rate (CAGR) of the underlying asset against their own cost of capital. In previous articles, we outlined the logic of Ethereum's long-term CAGR: it is a scarce, programmable reserve asset that plays a foundational role in securing on-chain economic safety as more assets migrate to blockchain networks. In this article, we will explain why Ethereum treasuries have a bullish trend and provide operational advice for companies adopting this financial strategy.

Acquiring Liquidity: The Cornerstone of Treasury Companies

One of the main reasons tokens and protocols seek to create these treasury companies is to provide a pathway for tokens to access traditional financial liquidity, especially in the context of declining liquidity for altcoins in the cryptocurrency market. Typically, these treasury strategies acquire liquidity to purchase more assets in three ways. Importantly, this liquidity/debt is unsecured, meaning it is non-redeemable:

- Convertible Bonds: Raising funds by issuing debt convertible into equity, with proceeds used to purchase more Bitcoin;

- Preferred Stock: Raising funds by issuing preferred stock that pays fixed annual dividends to investors;

- At-the-Market Issuance (ATM): Directly selling new shares in the public market to raise flexible real-time funds for purchasing Bitcoin.

Why Ethereum Convertible Bonds Are Superior to Bitcoin Convertible Bonds

In our previous article about Strategy, we pointed out that convertible bonds offer two main advantages for institutional investors:

- Downside protection with upside exposure: Convertible bonds allow institutions to gain exposure to the underlying asset (such as Bitcoin or Ethereum) while protecting their principal investment through the inherent protective features of the bonds;

- Volatility-driven arbitrage opportunities: Hedge funds often purchase convertible bonds not only to gain exposure but also to execute gamma trading strategies, profiting from the volatility of the underlying asset and its securities.

Gamma traders (hedge funds) have now become major participants in the convertible bond market.

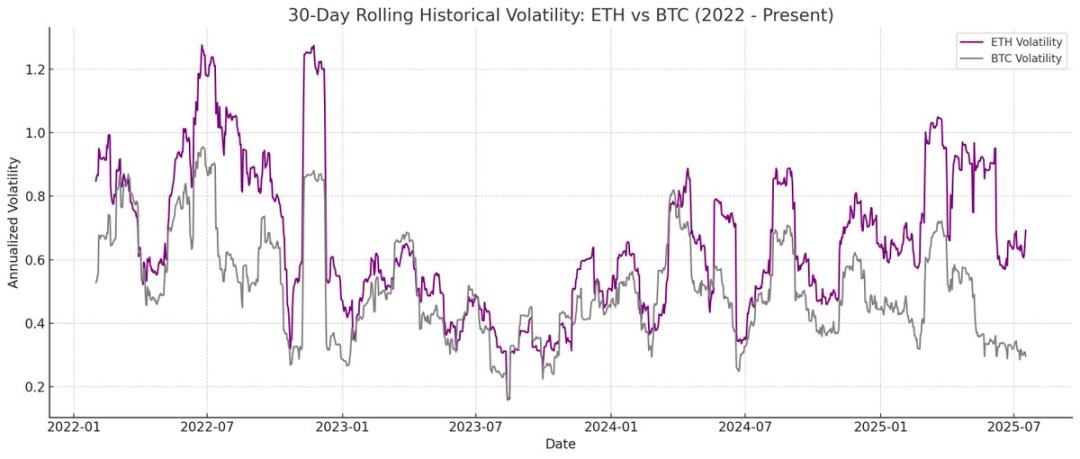

With this in mind, Ethereum's higher historical volatility and implied volatility compared to Bitcoin become key differentiators. Ethereum treasury companies reflect this higher volatility naturally in their capital structure by issuing Ethereum convertible bonds (CBs). This makes Ethereum-backed convertible bonds particularly attractive to arbitrageurs and hedge funds. The key is that this volatility also allows Ethereum treasuries to obtain more favorable financing conditions by selling convertible bonds at higher valuations.

Figure 1: Comparison of Historical Volatility of Ethereum and Bitcoin Source: Artemis

For holders of convertible bonds, higher volatility increases the opportunity to profit through gamma trading strategies. In short, the higher the volatility of the underlying asset, the more profitable gamma trading becomes, giving Ethereum treasury convertible bonds a clear advantage over Bitcoin treasury convertible bonds.

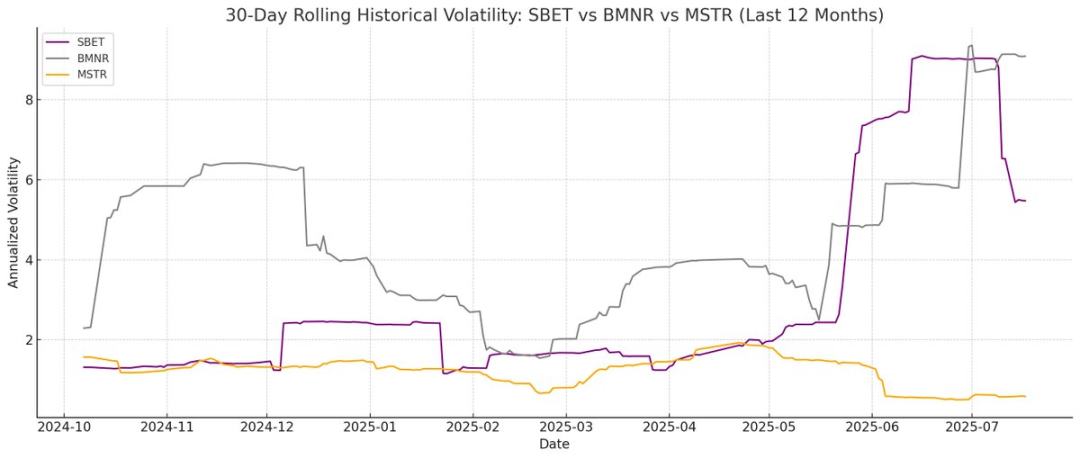

Figure 2: Comparison of Historical Volatility of BMNR and MSTR Source: Artemis

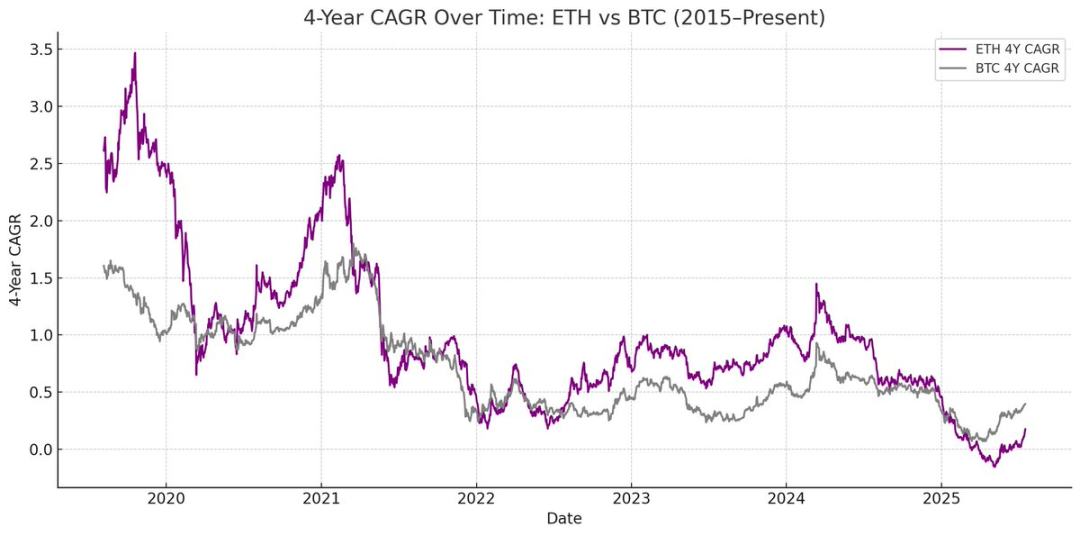

However, there is an important caveat: if Ethereum cannot maintain its long-term CAGR, the appreciation of the underlying asset may not be sufficient to support conversion before maturity. In this case, Ethereum treasury companies would face the risk of having to repay the bonds in full. In contrast, the likelihood of such downside risk occurring with Bitcoin is lower, as historically, most convertible bonds under this strategy have converted into equity.

Figure 3: Four-Year Compound Annual Growth Rate: Ethereum vs. Bitcoin. Source: Artemis

Why Ethereum's Preferred Stock Issuance Can Provide Differentiated Value

Unlike convertible bonds, preferred stock issuance is designed for fixed-income asset classes. Although some convertible preferred stocks offer mixed upside potential, yield remains the primary consideration for many institutional investors. The pricing of these instruments is based on the underwriting credit risk, i.e., whether the treasury company can reliably pay interest.

The key advantage of the Strategy approach lies in using at-the-market issuance (ATM) to fund these payments. Since this typically only accounts for 1%-3% of the total market capitalization, the dilution effect and risk introduced are minimal. However, this model still relies on the market liquidity and volatility of Bitcoin and the securities underlying the Strategy.

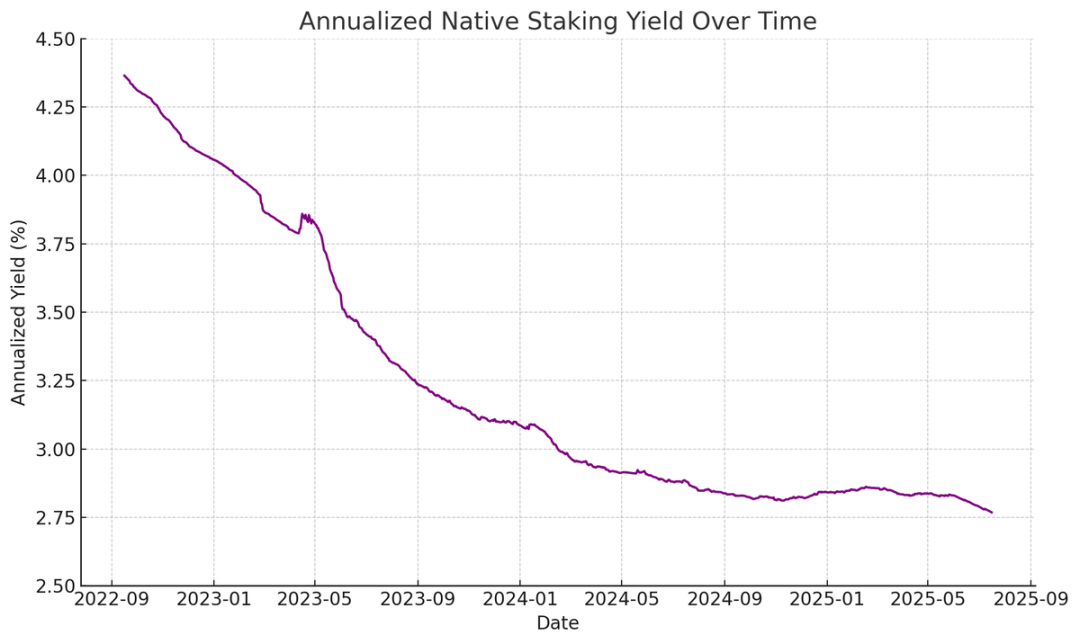

Ethereum adds another layer of value: native yield generated through staking, re-staking, and lending. This built-in yield provides greater certainty for paying preferred stock dividends and theoretically should lead to higher credit ratings. Unlike Bitcoin, which relies solely on price appreciation, Ethereum's return characteristics combine CAGR with native yield from the protocol layer.

Figure 4: Annualized Native Staking Yield of Ethereum Source: Artemis

I believe a compelling innovation of Ethereum preferred stock is its potential to become a non-directional investment tool, allowing institutional investors to participate in network security without taking on directional risk related to Ethereum's price. As we emphasized in our Ethereum report, maintaining at least 67% honest validators is crucial for ensuring Ethereum's security. As more assets migrate on-chain, it becomes increasingly important for institutions to actively support Ethereum's decentralization and security.

However, many institutions may not wish to take a direct long position in Ethereum. Ethereum treasury companies can act as intermediaries, absorbing directional risk while providing institutions with fixed-income-like returns. The preferred stocks issued by SBET and BMNR are specifically designed as on-chain fixed-income staking products for this purpose. They can bundle trading priority rights, protocol-level incentives, and other advantages to make them more attractive to investors seeking stable returns without taking on full market risk.

Why At-the-Market Issuance (ATM) Is More Beneficial for Ethereum Treasuries

For crypto treasury companies, a widely used valuation metric is mNAV (market capitalization to net asset value ratio). Conceptually, mNAV functions similarly to the price-to-earnings (P/E) ratio: it reflects the market's pricing of future growth per share of assets.

Ethereum treasuries should inherently enjoy a higher mNAV premium due to Ethereum's native yield mechanism. These activities can generate recurring "income" or increase the per-share value of Ethereum without incremental capital. In contrast, Bitcoin treasury companies must rely on synthetic yield strategies (such as issuing convertible bonds or preferred stock). Without these institutional products, it becomes difficult to justify the yield when the market premium of a Bitcoin treasury approaches its net asset value.

Most importantly, mNAV is reflexive: a higher mNAV enables treasury companies to raise funds more effectively through at-the-market issuance. They issue shares at a premium and use the proceeds to purchase more underlying assets, thereby increasing the per-share asset value and reinforcing this cycle. The higher the mNAV, the more value can be captured, making at-the-market issuance particularly effective for Ethereum treasury companies.

The ability to access capital is another key factor. Companies with deeper liquidity and stronger financing capabilities naturally enjoy higher mNAVs, while companies with limited market access often trade at a discount. Therefore, mNAV typically reflects a liquidity premium — the market's confidence in a company's ability to effectively access more liquidity.

How to Filter Treasury Companies from First Principles

A useful mental model is to view at-the-market issuance as a way to raise capital from retail investors, while convertible bonds and preferred stock are typically designed for institutional investors. Therefore, the key to a successful at-the-market issuance strategy is to build a strong retail base, which often depends on having a credible and charismatic leader, as well as ongoing transparency around the strategy to instill confidence in retail investors about the long-term vision. In contrast, successfully issuing convertible bonds and preferred stock requires strong institutional sales channels and relationships with capital markets. Based on this logic, I believe SBET is a stronger retail-driven company, primarily due to Joe Lubin's leadership and the team's consistent transparency regarding their accumulation of Ethereum per share. Meanwhile, BMNR, under Tom Lee's leadership, appears more capable of leveraging institutional liquidity due to its close ties to traditional finance.

Why Ethereum Treasuries Are Important for the Ecosystem and Competitive Landscape

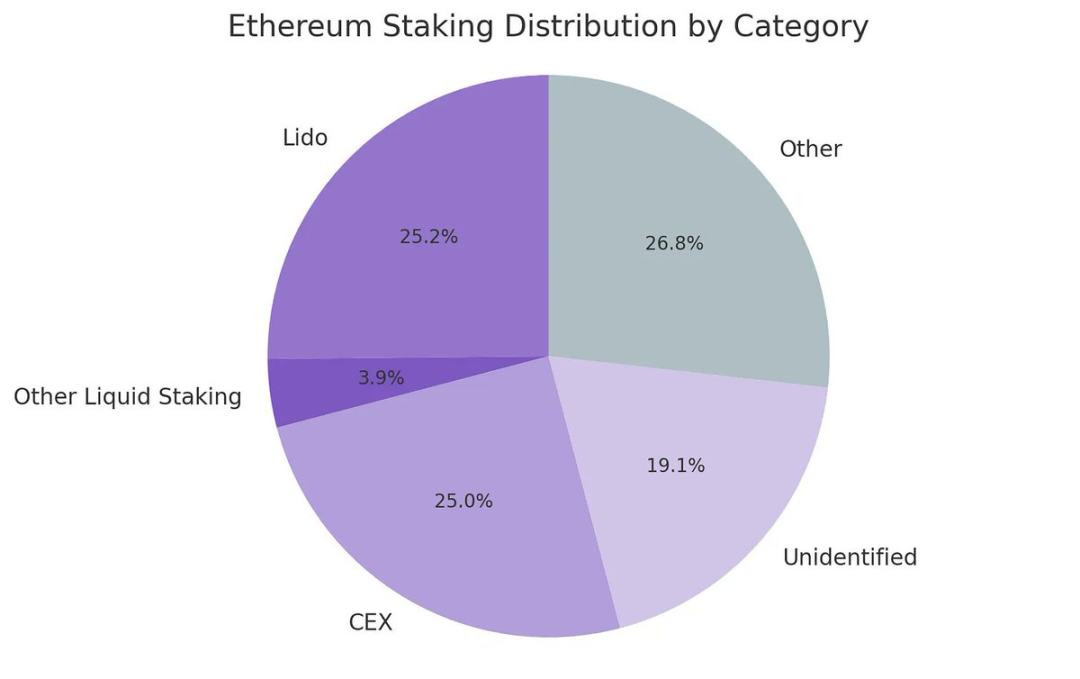

One of the biggest challenges facing Ethereum is the increasing centralization of validators and staked Ethereum, primarily reflected in liquid staking protocols like Lido and centralized exchanges like Coinbase. Ethereum treasury companies help balance this trend and promote validator decentralization. To support long-term resilience, these companies should diversify their Ethereum across multiple staking providers and, where possible, become validators themselves.

Figure 5: Staking Distribution by Category Source: Artemis

In this context, I believe the competitive landscape for Ethereum treasuries will differ significantly from that of Bitcoin treasury companies. In the Bitcoin ecosystem, the market has evolved into a winner-takes-all scenario, with Strategy holding more than ten times the amount of Bitcoin compared to the second-largest holder. Thanks to its first-mover advantage and strong narrative control, it also dominates the convertible bond and preferred stock markets.

In contrast, Ethereum treasury strategies are just getting started. No single entity has established dominance; instead, multiple Ethereum treasuries are being launched in parallel. This lack of first-mover advantage is not only healthier for the network but also fosters a more competitive and accelerated market environment. Given the relatively close Ethereum holdings of the main participants, I believe a dual oligopoly structure may emerge with SBET and BMNR advancing together.

Figure 6: Holdings of Ethereum Treasury Companies Source: strategicethreserve.xyz

Valuation: A Combination of Strategy and Lido

Broadly speaking, the Ethereum treasury model can be seen as a fusion of Strategy and Lido, tailored for traditional finance. Unlike Lido, Ethereum treasury companies have the potential to capture a larger share of asset appreciation because they hold the underlying assets, making this model far superior in terms of value accumulation.

From a rough valuation perspective: Lido currently manages about 30% of the total staked Ethereum, with an implied valuation exceeding $30 billion. We believe that within a market cycle (4 years), the total scale of SBET and BMNR could surpass Lido, thanks to the speed, depth, and reflexivity of traditional financial capital flows — as demonstrated by Strategy's growth strategy.

For reference: Bitcoin's market capitalization is $2.47 trillion, while Ethereum's market capitalization is $428 billion (equivalent to 17%-20% of Bitcoin). If the scale of SBET and BMNR reaches about 20% of Strategy's $120 billion valuation, this implies a long-term value of approximately $24 billion. Currently, their total valuation is slightly below $8 billion, indicating significant growth potential as Ethereum treasuries mature.

Conclusion

The integration of cryptocurrency with traditional finance through digital asset treasuries represents a significant transformation, with Ethereum treasuries now emerging as a powerful force. Ethereum's unique advantages provide Ethereum treasury companies with distinct growth potential. Their potential to promote validator decentralization and foster competition further distinguishes them from Bitcoin treasuries. Combining Strategy's capital efficiency with Ethereum's built-in yield will unlock tremendous value and drive the on-chain economy deeper into traditional finance. Rapid expansion and increasing institutional interest suggest that this will have a transformative impact on the cryptocurrency and capital markets in the coming years.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。