1. Overview of Stablecoins

Stablecoins are a type of cryptocurrency whose price is typically pegged to a stable asset, such as the US dollar, euro, gold, or even certain commodities. The emergence of stablecoins primarily aims to address the issue of high volatility in cryptocurrencies. One of the earliest stablecoins is Tether (USDT), which was created in 2014 and promises that for every USDT issued, one dollar is held in a bank as collateral to ensure that the price of USDT remains anchored to the dollar. Over time, more types of stablecoins have emerged, such as asset-backed, over-collateralized crypto assets, and algorithmic stablecoins.

Stablecoins hold significant importance in the crypto market. They can serve as a hedge for users; when the market is too volatile, users can convert their crypto assets into stablecoins to avoid risk. Additionally, they are core assets in DeFi, as many lending, trading, and mining products are based on stablecoins. Furthermore, they help enhance the liquidity and trustworthiness of the crypto market, as both users and project parties prefer to use price-stable assets for settlement and storage. Moreover, stablecoins are gradually becoming a bridge connecting traditional finance and the crypto world, allowing fiat currencies to be tokenized, enabling fast transfers globally, and saving on cross-border fees; they can circulate like cash but with faster speeds and lower costs.

With the rapid development of the crypto market, stablecoins have gradually become core assets in scenarios such as DeFi, exchanges, and on-chain payments. This article will provide a comprehensive analysis of stablecoins, considering their market development status, types and mechanisms, application scenarios, policy compliance, challenges, and prospects.

2. Types and Mechanisms of Stablecoins

2.1 Asset-Backed Stablecoins

Asset-backed stablecoins (Fiat-collateralized Stablecoins) are a type of cryptocurrency supported by actual fiat currency reserves (such as US dollars, euros, etc.), typically pegged at a 1:1 ratio to a specific fiat currency. This type of stablecoin is one of the earliest and most mainstream forms, where the issuer deposits an equivalent amount of fiat currency or related assets into a bank or centralized custodian account to support the circulating supply of stablecoins in the market. Users can exchange stablecoins for the corresponding fiat currency at a 1:1 ratio at any time. Its advantages include price stability and ease of use, making it widely applicable in trading, payments, and DeFi scenarios. However, it also requires users to trust that the centralized issuer genuinely has sufficient reserves, making transparency and audit reports crucial for this type of stablecoin. Typical examples include USDT, USDC, and FDUSD.

2.1.1 USDT

Currently, the market capitalization of USDT is approximately $153.2 billion (https://www.coingecko.com/en/global-charts), making it the highest-valued stablecoin. USDT is issued by Tether, with each USDT backed by equivalent asset reserves to ensure its value stability. The main types of reserve assets include US Treasury bonds, Bitcoin, gold, cash, and cash equivalents. [Am1] To reassure users, Tether provides daily circulation data and quarterly reserve status, which can be viewed on its official Transparency page (https://tether.to/en/transparency/?tab=usdt). Tether reserves are audited by the independent accounting firm BDO, providing detailed composition and total amount of its reserve assets, and are regularly published to enhance transparency.

According to the latest data from Tether's official website, in the first quarter of 2025, the circulating supply of USDT increased by approximately $7 billion, and the number of user wallets grew by about 46 million. As of March 31, 2025, Tether's total reserve assets amounted to $149.2 billion, exceeding its total liabilities of $143.6 billion, showing an excess reserve of approximately $5.59 billion.

Figure 1. The last Reserves Report (March 31, 2025) of Tether. Source: https://tether.to/en/transparency/?tab=usdt

Currently, USDT supports over a dozen mainstream blockchains, including Ethereum (ERC-20), Tron (TRC-20), BNB Chain (BEP-20), Solana, and Ton. Initially, USDT was primarily issued on the Ethereum chain (ERC-20), but as transaction fees rose, more users shifted to the lower-cost Tron chain (TRC-20). Currently, over half of USDT circulates on Tron, reflecting users' demand for high-frequency, small-amount, low-fee cross-border usage. This also indicates Tether's flexibility in on-chain deployment strategies, allowing for quick adjustments based on market feedback.

Moreover, USDT holds an irreplaceable position in practical use cases. In almost all major centralized exchanges globally (such as Binance, Coinbase, OKX, etc.), USDT is the default trading unit. In the DeFi space, it also has a wide range of applications, serving as a primary trading pair on many decentralized trading platforms (such as Curve, Uniswap). Additionally, in emerging market countries (such as Argentina, Turkey, etc.) and in cross-border payments and OTC trading, USDT is widely accepted due to its strong liquidity and ease of exchange.

Although USDT is the largest and most widely used stablecoin globally, its path to compliance has not been smooth. Tether was fined $41 million by the U.S. Commodity Futures Trading Commission (CFTC) for insufficient information disclosure. To date, USDT has not obtained the electronic money issuer license required by the EU's MiCA and has not applied for a federal regulatory stablecoin license in the U.S. As regulatory frameworks tighten globally, USDT still needs to continuously improve its compliance transparency; otherwise, it may face risks of restricted circulation in certain regions.

With the implementation of the EU's MiCA and the U.S. GENIUS Act, stablecoins will gradually enter an era of strong regulation. If USDT wishes to maintain its leading position in the global stablecoin market, it must not only sustain its market circulation advantage but also enhance its regulatory compliance and information disclosure standards. Otherwise, even if it currently holds the highest market capitalization share, it may lose its first-mover advantage in a new round of compliance reshuffling.

2.1.2 USDC (USD Coin)

USDC (USD Coin) is issued by Circle, aiming to combine the stability of the US dollar with the flexibility of blockchain, providing a digital dollar that can be traded quickly, securely, and at low cost globally. USDC is currently the second-largest stablecoin by market capitalization, with a market cap of approximately $61.18 billion, second only to USDT.

USDC is 100% backed by highly liquid cash and its equivalent assets (such as short-term U.S. Treasury bonds, cash, and repurchase agreements), allowing users to exchange it for US dollars at a 1:1 ratio at any time. Its reserve funds mainly consist of the Circle Reserve Fund (USDXX) and cash. USDXX is a government money market fund registered with the U.S. Securities and Exchange Commission (SEC), primarily composed of cash, short-term U.S. Treasury bonds, and overnight repurchase agreements. The cash reserves are held in several top-tier banks globally, known for their strong capital, high liquidity, and strict regulation (such as BNY Mellon).

In terms of transparency and auditing, Circle provides users with real-time data on reserve assets and circulation, with reserve assets reported daily by BlackRock as an independent third party, publicly accessible. Additionally, a monthly audit report issued by the independent accounting firm Deloitte ensures the transparency and security of USDC's reserve assets, enhancing user trust.

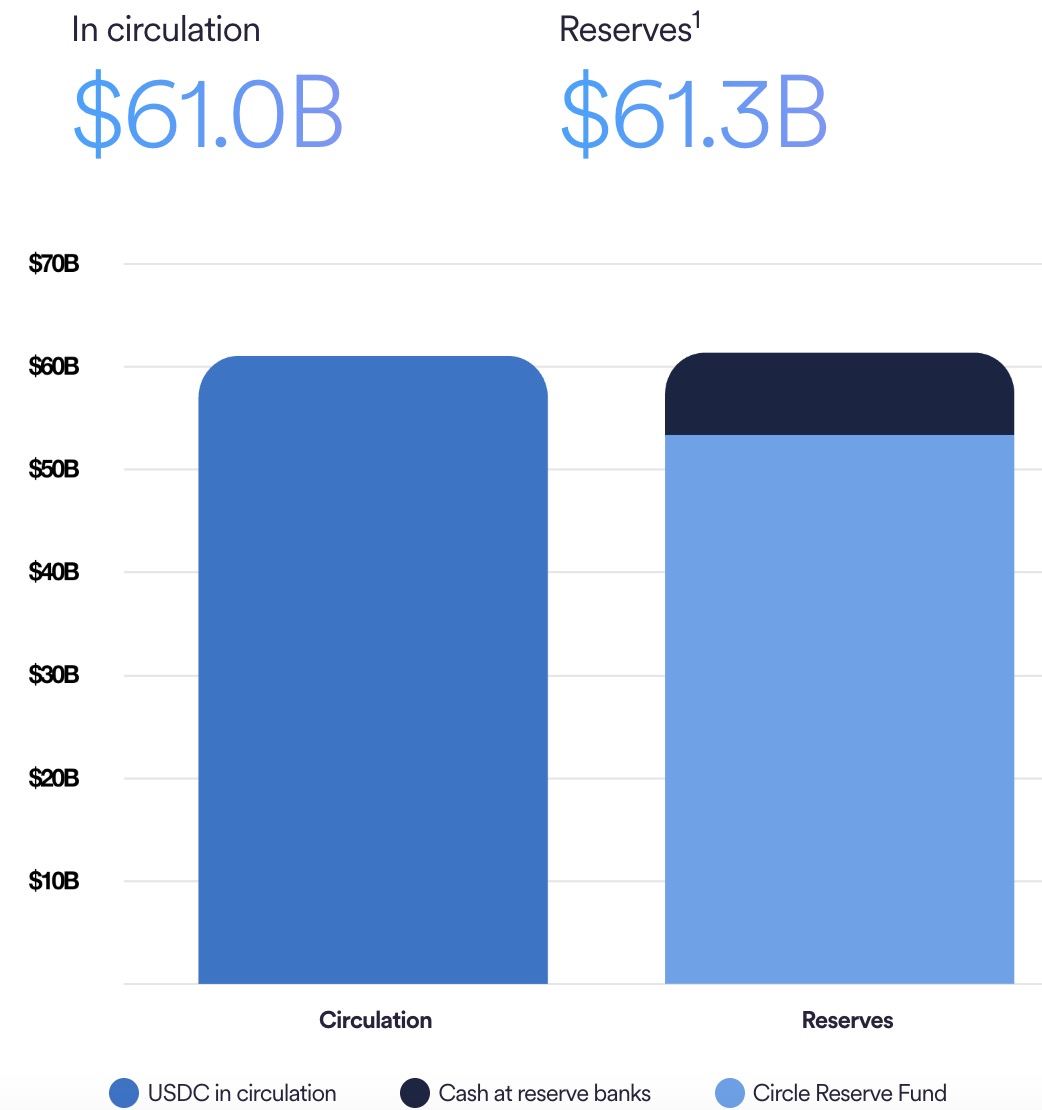

According to data released by Circle, as of June 2025, the total issuance of USDC is $61 billion, with total reserve funds amounting to $61.3 billion. It has been natively issued on over 15 public chains globally and listed on more than 100 exchanges, allowing users to transfer, save, pay, and engage in DeFi transactions at very low costs in over 180 countries worldwide.

Figure 2. USDC Reserves composition. Source: https://www.circle.com/transparency

USDC currently supports native issuance on over 15 mainstream blockchains, including Ethereum, Solana, Avalanche, Base, Polygon, and Arbitrum. Circle adopts native issuance rather than bridging, effectively reducing cross-chain asset risks. By deeply collaborating with multiple L2 ecosystems (such as Base and OP Stack), it strengthens its underlying position in Web3, making it one of the stablecoins with the highest integration between DeFi and CeFi.

In terms of compliance, USDC has consistently made compliance a core strategy, actively promoting license applications and regulatory connections globally. It is one of the few stablecoins that have proactively applied for an EMT (Electronic Money Token) license under the EU's MiCA framework and is recognized as a stablecoin issuer in multiple U.S. states. Circle also holds a BitLicense issued by the New York State Department of Financial Services (NYDFS) and a money transfer license in California, demonstrating its strong regulatory adaptability. This makes USDC the most compliance-friendly stablecoin currently, making it more appealing to institutional, corporate users, and government departments.

In terms of global application, USDC is not just an on-chain stablecoin; it is rapidly evolving into a payment bridge between Web2 and Web3. Circle has established partnerships with payment giants such as Visa, Mastercard, Stripe, and Worldpay to promote the use of USDC in real-world payments, merchant settlements, and cross-border remittances. For example, Visa has piloted the use of USDC for cross-border settlements in several countries, bypassing traditional banking systems and significantly reducing costs and time delays. This gives USDC the potential to serve as a real financial bridge that surpasses traditional stablecoins.

2.1.3 FDUSD

FDUSD (First Digital USD) is issued by Hong Kong's First Digital Labs through its subsidiary FD121 Limited and is an asset-backed stablecoin. It adopts a 1:1 reserve mechanism, meaning that for every FDUSD issued, the issuer must deposit an equivalent amount of U.S. dollars or cash equivalents (such as short-term government bonds, money market instruments) into a regulated custodial account, ensuring that each FDUSD is backed by $1 in assets. The reserve assets are managed and held by the regulated custodian First Digital Trust Limited and are subject to third-party audits to ensure that the on-chain circulation matches the off-chain reserve assets.

First Digital Labs is a subsidiary of the First Digital Group in Hong Kong, focusing on the research and issuance of stablecoins. It is responsible for the contract deployment, cross-chain issuance, and ecosystem expansion of FDUSD, while closely collaborating with the custodian First Digital Trust Limited to ensure that the issuance process is compliant and secure. The institution has registered as a Virtual Asset Service Provider (VASP) in Lithuania and is actively applying to be included in the proposed stablecoin regulatory framework by the Hong Kong Monetary Authority (HKMA). Additionally, FDUSD employs an asset isolation protection mechanism, meaning that user funds and the company's own assets are completely separated, ensuring that even in the event of company bankruptcy, user assets remain unaffected.

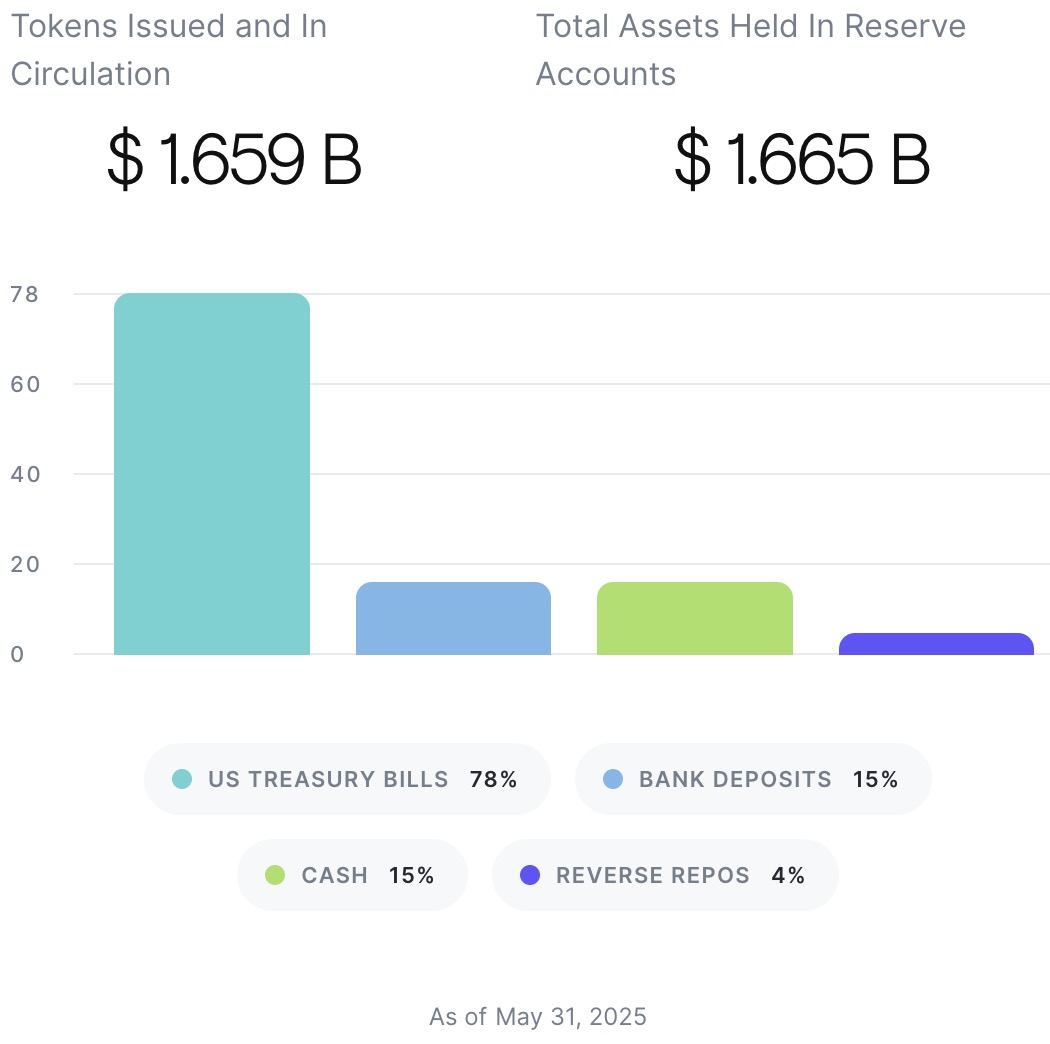

FDUSD currently has a market capitalization of $1.54 billion and is deployed on mainstream public chains such as Ethereum, Solana, Sui, and BNB Chain. According to the latest data updated on May 31, 2025, on the First Digital Labs official website, the total amount of FDUSD tokens issued and in circulation is $1.659 billion, while the total assets in the reserve account amount to $1.665 billion, with reserve assets slightly exceeding the total circulating tokens, ensuring 1:1 reserve support. The reserve assets consist of 78% U.S. Treasury Bills, 15% cash, 4% reverse repos, and 15% bank deposits.

Figure 3. FDUSD Data. Source: https://firstdigitallabs.com/transparency

In terms of collaborative promotion, FDUSD has a close partnership with Binance. At the beginning of 2023, due to regulatory pressure on Paxos, the issuer of BUSD (Binance's own stablecoin), Binance ceased support and promotion of BUSD and urgently sought a compliant, secure, and sustainable next-generation stablecoin alternative. Due to its solid compliance structure, stable asset reserves, public audit mechanisms, and regulatory expectations from the Hong Kong market, FDUSD became a key focus of support for Binance. Although there is no equity or financial relationship between Binance and FDUSD, Binance provides extensive access at the exchange level for FDUSD, including trading pairs with mainstream cryptocurrencies, zero-fee support, cross-chain deposit and withdrawal functions, and deep integration into Binance's financial and earning products, enhancing FDUSD's liquidity and market usage. Compared to other stablecoins, FDUSD enjoys stronger support and more promotional resources within the Binance ecosystem, making it a priority for promotion following BUSD.

Although FDUSD has not yet obtained a formal stablecoin issuance license from Hong Kong or other major jurisdictions, First Digital Labs is actively applying and maintaining communication with governments and regulatory bodies, which clarifies FDUSD's compliance path and enhances its market recognition, giving it the potential to become a mainstream compliant stablecoin.

2.1.4 USD1

USD1 is a stablecoin issued by World Liberty Financial (WLFI) that is pegged 1:1 to the U.S. dollar, aimed at providing users with a stable, secure, and auditable digital dollar option. Each USD1 is backed by equivalent U.S. dollar assets, including short-term U.S. Treasury bonds, bank deposits, and cash equivalents. Its reserves are held by the institutional-grade custodian BitGo and are verified in real-time on-chain through Chainlink's Proof-of-Reserves (PoR) mechanism, enhancing transparency and user trust. Additionally, WLFI states that it will conduct a third-party accounting audit quarterly, but has not yet disclosed the specific auditing firm or the content of the audit report.

USD1 is one of the few stablecoins that supports Chainlink PoR. PoR is an oracle-based on-chain reserve verification system that synchronizes the balances of U.S. dollars, Treasury bonds, and other reserve assets held by BitGo in real-time to the blockchain for public access. This provides unprecedented asset transparency for users, auditors, and third-party developers. However, while WLFI claims it will conduct regular audits in the future, it has not provided any specific names of auditing firms or detailed reports to date, which still requires further information disclosure to enhance credibility.

One significant reason for the widespread attention on USD1 is its political background. Its issuer, WLFI, is currently controlled by the Trump family, with Trump being referred to as a crypto advocate in this project. His sons Eric Trump and Donald Trump Jr. serve as Web3 ambassadors, while his youngest son Barron Trump is also dubbed a DeFi pioneer. Although WLFI claims that its governance mechanism has community characteristics, in reality, core decision-making power involving the Trump family is not open to ordinary token holders, and there are significant controversies regarding decentralized governance. This strong political color has led USD1 to be commonly referred to as a Trump-affiliated political stablecoin, creating a unique label in the market.

USD1 has been deployed on Ethereum and BNB Chain and plans to expand to more mainstream chains. Users can purchase it through centralized exchanges that support this stablecoin (such as Binance) using U.S. dollars or other stablecoins (like USDT, USDC), or obtain it through OTC or DEX trading methods. Additionally, large users or institutions that support off-chain bank transfers can perform real-time minting or redemption through BitGo-controlled platforms, with the process requiring strict KYC certification.

Regarding compliance, USD1 has not publicly obtained relevant licenses from the EU's MiCA or U.S. financial regulatory agencies. Its strict KYC mechanism and custodial arrangements indicate its intention to comply with the requirements of major jurisdictions, but due to the lack of publicly available third-party audit reports and regulatory approval documents, the market remains cautious about its compliance. Compared to stablecoins that have actively applied for and hold compliance licenses (such as USDC and FDUSD), USD1 still has room for improvement in transparency and regulatory cooperation.

USD1 officially launched in March 2025, leveraging its strong political background and market expectations to gain support from multiple mainstream exchanges within a few months, quickly surpassing the cold start phase. As of now, its market capitalization has exceeded $2.1 billion, placing it among the top ten stablecoins by market cap. This performance reflects the market's high attention to its political endorsement and reserve model, while also highlighting the unique appeal of political capital combined with financial instruments in the current crypto market.

In the future, if USD1 can improve audit transparency and clarify regulatory permissions, it will be more favorable for it to obtain legal circulation qualifications in major global markets, enhancing the confidence of users and institutional investors.

2.2 Over-Collateralized Crypto Asset Stablecoins

Over-collateralized crypto asset stablecoins ensure the value of the stablecoin by collateralizing more cryptocurrency than the amount issued. For example, if a user wants to obtain $100 worth of stablecoins, they need to lock up $150 or more worth of crypto assets (such as ETH, BTC, etc.) in a smart contract. This over-collateralization method can mitigate the risks associated with the high volatility of cryptocurrency prices, ensuring that the stablecoin always has sufficient assets to support its value. If the value of the collateralized assets drops significantly, the system will trigger a forced liquidation mechanism to ensure the stablecoin's redemption capability.

This mechanism does not require the intervention of centralized institutions, thus providing a higher degree of decentralization and security. However, because it requires collateralizing more assets than the amount of stablecoins issued, capital efficiency is relatively low, and compared to centralized stablecoins, the user threshold for use is relatively higher.

2.2.1 DAI (USDS)

DAI is a decentralized stablecoin launched by MakerDAO, pegged 1:1 to the U.S. dollar, and employs an over-collateralization mechanism to ensure stability. Users can deposit supported crypto assets such as ETH, WBTC, and stETH into the Maker protocol's vault to generate the corresponding amount of DAI. Additionally, users can directly purchase DAI through exchanges for payments, savings, trading, and other purposes. To cope with market fluctuations, the system requires users to over-collateralize, typically with collateralization rates between 110% and 200%; if the value of the collateralized assets falls below the minimum requirement, the system will automatically liquidate part of the collateral to ensure DAI's stable peg.

The Maker protocol has also introduced a Dai Savings Rate (DSR) mechanism, allowing users to earn interest by depositing DAI. The DSR has no minimum threshold and allows for flexible deposits and withdrawals. This mechanism is also one of the important tools for stabilizing the price of DAI: MKR holders can adjust the DSR through governance voting; when the price of DAI exceeds $1, the interest rate can be lowered to reduce demand, and conversely, the interest rate can be raised to attract users to hold DAI, thus balancing market supply and demand. Currently, DAI's market capitalization has exceeded $3.5 billion, making it one of the most important stablecoins in the DeFi ecosystem.

In September 2024, MakerDAO announced a rebranding, upgrading to Sky Protocol and launching a new stablecoin, USDS, along with a governance token, SKY. USDS is positioned as an upgraded version of DAI, also a decentralized over-collateralized stablecoin pegged to the U.S. dollar. It supports a diverse range of collateral assets, including ETH, USDC, USDT, and RWA (real-world assets). Users can voluntarily convert DAI to USDS at a 1:1 ratio or directly exchange USDC, USDT, ETH, or SKY for USDS through the Sky.money platform. Additionally, the existing MKR token can be exchanged for SKY at a ratio of 1:24,000. It is important to emphasize that DAI and MKR will continue to circulate, and users can choose whether to migrate as needed.

While USDS maintains decentralization, it further enhances its mechanism design and user incentives. Users can deposit USDS into the Sky Savings Rate (SSR) module to receive sUSDS savings certificates, which will automatically grow as the protocol sets interest rates, supporting redemption at any time. Users can also earn STRs (Sky Token Rewards) points, which can be redeemed for rights or used for governance participation. The entire operation is executed automatically by smart contracts, with assets managed independently by users, ensuring both security and transparency.

As of now, USDS has surpassed a market capitalization of $7.15 billion, making it the third-largest stablecoin globally, following USDT and USDC. Its rapid development not only reflects market trust in the Maker/Sky ecosystem but also demonstrates a new balance found by decentralized stablecoins between compliance and mechanism innovation.

Although USDS is an upgraded version of a decentralized stablecoin with advanced mechanisms and transparent operations, it also carries some risks. For instance, it relies on crypto assets as collateral, and in the event of severe market fluctuations (such as a sharp drop in ETH), it may trigger large-scale liquidations, affecting stability. Additionally, some collateral assets are real-world assets (RWA), which involve off-chain compliance and execution issues, potentially leading to legal risks. Overall, the innovation of USDS is commendable, but users still need to be aware of the uncertainties that may arise during its operation.

In terms of compliance, both DAI and USDS are decentralized, over-collateralized stablecoins that emphasize censorship resistance and self-management, but they still face certain challenges in compliance under current mainstream regulatory frameworks. DAI, launched by MakerDAO, is entirely generated based on on-chain mechanisms, without a centralized issuer, and has not obtained financial licenses or provided external audits, making it difficult to meet the requirements for identity verification, reserve compliance, and redemption mechanisms set by regulations such as the EU's MiCA and Singapore's SCS. Although USDS is a new generation stablecoin introduced after MakerDAO rebranded to Sky Protocol, incorporating some assets with stronger compliance (such as USDC and RWA) to enhance credibility, it still has not been included in any regulatory licensing system. Both are widely used in DeFi scenarios but lack significant compliance.

2.3 Algorithmic Stablecoins

Algorithmic stablecoins differ from asset-backed or over-collateralized stablecoins in that they typically do not rely on fiat currency or crypto assets as reserves. Instead, they maintain a 1:1 peg to the U.S. dollar or other fiat currencies through smart contracts that control supply and demand.

2.3.1 Terra USD (UST)

TerraUSD (UST) is an algorithmic stablecoin launched by the Terra project, designed to maintain a 1:1 peg to the U.S. dollar through a mechanism linked to its sister token, LUNA. The core of UST's price stability lies in its exchange relationship with LUNA. When the price of UST exceeds $1, users can mint UST by burning LUNA, increasing the supply of UST in the market and thereby lowering its price. Conversely, when the price of UST falls below $1, users can burn UST to mint LUNA, reducing the supply of UST in the market and raising its price. This mechanism relies on the arbitrage actions of market participants to maintain UST's price stability.

In 2022, when the price of UST fell below $1, the system's algorithm allowed users to exchange discounted UST for LUNA at a price of $1, leading to a large amount of UST being burned while new LUNA was minted. As more LUNA was released into the market, the price of LUNA rapidly declined, and LUNA was the only support for UST's value. When the price of LUNA plummeted, market confidence in UST further declined, leading to more people selling UST and LUNA, creating a panic. This death spiral ultimately caused the price of UST to drop to a few cents, and the price of LUNA nearly reached zero, resulting in the collapse of the entire Terra ecosystem.

The collapse of UST and LUNA had a direct and profound negative impact on the algorithmic stablecoin sector, causing the entire Web3 market to question the mechanisms of algorithmic stablecoins. Algorithmic stablecoins incentivize users to mint or burn tokens through price differentials to maintain their peg, but once market confidence is shaken, the arbitrage mechanism struggles to function, significantly increasing the risk of de-pegging. Additionally, algorithmic stablecoins do not hold sufficient or high-quality collateral assets, making it impossible to provide stable value support during large-scale redemptions. To date, while algorithmic stablecoins have not completely disappeared, their market capitalization has significantly shrunk, and multiple countries regard them as high-risk assets. Coupled with regulatory pressures, algorithmic stablecoins may struggle to survive without making changes.

2.3.2 FRAX

Frax was initially a partially collateralized, partially algorithmically adjusted stablecoin that used a portion of assets (such as USDC) as collateral, while the other portion was automatically adjusted by the system's algorithm to maintain price stability. When the price of the stablecoin deviates from the target price, the algorithm incentivizes users to actively mint or burn FRAX through an arbitrage mechanism, adjusting supply and demand to maintain price stability. For example, when the price of FRAX is $1.02, exceeding $1, the system encourages users to mint more FRAX to increase supply: users can use $1 worth of collateral (such as USDC + FXS) to mint 1 FRAX and then sell it on the market for $1.02, earning a $0.02 profit. This increases the quantity of FRAX in the market, causing the price to revert to around $1. Conversely, when the price is below $1 (e.g., $0.98), users are encouraged to burn FRAX: they can buy FRAX on the market for $0.98 and then redeem the collateral assets as set by the system, totaling $1, thus earning the price difference. This leads to the burning of FRAX, reducing its quantity in the market and naturally raising the price. This mechanism resembles "market self-regulation," allowing FRAX to maintain a value close to $1 through supply and demand changes.

Although algorithmic stablecoins are relatively decentralized, the entire market lost confidence in them after the collapse of Terra/UST. While Frax is not a 100% algorithmic stablecoin, its partially collateralized + algorithmically adjusted model is still viewed as high-risk. Additionally, various countries have begun tightening regulations on stablecoins, particularly emphasizing that stablecoins must have clear, real, and transparent reserve assets.

To adapt to changes and retain users, Frax made significant improvements in its latest V3 version. Frax V3 abandoned the original partial algorithmic mechanism and fully transitioned to a model that is 100% backed by external assets. Each FRAX stablecoin is now supported by equivalent assets, no longer relying on the market value of the governance token FXS. Users can deposit specific assets, such as USDC, sDAI, short-term U.S. Treasury bonds, overnight reverse repurchase agreements (ON RRP), or FDIC-insured dollar deposits into the protocol's vault to mint FRAX at a 1:1 ratio. This "full collateralization" model significantly enhances stability and compliance. Frax V3 also introduces a dynamic collateralization ratio mechanism. The protocol ensures that the overall collateralization ratio (CR) remains above 100% through AMO (Algorithmic Market Operations) and on-chain governance measures, and it will be adjusted upward as necessary to enhance the system's risk resistance.

In the context of tightening global regulations and a crisis of trust in algorithmic stablecoins, Frax has shifted to a new model supported by 100% real assets, such as USDC, sDAI, and short-term U.S. Treasury bonds in its V3 version. This transformation helps it align more closely with regulatory requirements from the EU's MiCA and Singapore's MAS. However, as of now, Frax has not obtained any stablecoin issuance licenses from major countries, nor has it conducted regular third-party audits. Its asset custody is still managed internally by the protocol, lacking an authoritative independent custody mechanism. Therefore, while Frax is actively moving towards compliance, it still has a distance to cover from a regulatory perspective. In the future, if it hopes to develop long-term in markets like Europe and the U.S., it will need to make more efforts in audit disclosure, license applications, and risk isolation.

2.4 Yield-Generating Stablecoins

Yield-generating stablecoins are a type of stablecoin that can automatically generate returns during the holding period. They not only peg to the value of fiat currencies like the U.S. dollar but also utilize protocol income or on-chain hedging to generate returns, distributing the interest income from underlying assets back to the holders.

The main feature of these stablecoins is that users can automatically earn returns just by holding them, without needing to participate in mining or staking. They are typically backed by interest-generating assets, such as U.S. Treasury bonds, on-chain lending, or staked tokens, and the interest generated is distributed to holders through a certain mechanism. They function like ordinary stablecoins pegged to the U.S. dollar while also acting as a type of interest account, allowing users' funds to remain stable while gradually growing. Yield-generating stablecoins can meet the needs of users seeking low-risk options, providing a certain level of interest while maintaining stability.

2.4.1 Ethena USDe

USDe is a synthetic dollar stablecoin launched by Ethena, using crypto assets as support and employing on-chain custody and centralized liquidity yield. It combines synthetic asset collateralization with smart hedging strategies to achieve a 1:1 peg to the U.S. dollar while generating returns.

USDe uses over-collateralization of crypto assets, where users deposit crypto assets like stETH and ETH into the Ethena protocol. To hedge against the price decline of these assets, Ethena establishes corresponding short positions on centralized exchanges, such as shorting ETH perpetual contracts, thereby creating a portfolio that is insensitive to market fluctuations. This strategy is known as "delta-neutral hedging," aiming to avoid significant fluctuations in the value of the asset portfolio and keep the dollar value of the collateral relatively stable. The essence of this mechanism is not to directly control the price of USDe but to stabilize the value of the underlying assets, providing assurance for the 1:1 minting of USDe.

However, this does not directly determine whether USDe equals $1. To address this, the Ethena protocol has designed a core arbitrage mechanism based on a delta-neutral strategy to adjust market supply and demand and stabilize the pegged price. When the price of USDe in the secondary market is below $1 (for example, dropping to $0.98), arbitrageurs can buy USDe at a lower price from the market and then go to the Ethena protocol to redeem these USDe for an equivalent amount of underlying crypto assets (such as ETH or stETH) at a 1:1 price. Since the internal pricing at redemption remains at $1, arbitrageurs earn a 2% risk-free profit through the operation of "buying at 0.98 and redeeming at 1.00." This arbitrage operation increases market demand for USDe, thereby driving up its price and gradually pushing it back to $1.

Conversely, when the market price of USDe exceeds $1 (for example, rising to $1.02), users can collateralize crypto assets (such as ETH) in the protocol to generate new USDe at a 1:1 ratio and then sell it in the market for profit. For instance, a user can generate 1 USDe by collateralizing $1 worth of ETH and sell it for $1.02, earning a 2% profit. This leads to an increase in the supply of USDe in the market, alleviating the supply-demand imbalance and causing the price to gradually fall back to around $1. This mechanism guides the price of USDe to fluctuate around $1 through market forces, ensuring stability.

In this process, the Ethena protocol obtains protocol cash flow through two main channels: one is funding fee income, and the other is staking income. In the perpetual futures market, a funding rate mechanism is set up to keep the contract price aligned with the spot price. When the market is bullish (with high long sentiment), long positions pay funding fees to short positions. When the market is bearish (with many short positions), short positions pay funding fees to longs. If the current market is bullish (generally long), Ethena's short positions can steadily earn funding fee income. Additionally, some assets that inherently generate yield, such as stETH (staked ETH, which generates ETH staking rewards), also allow Ethena to earn this portion of staking income. Therefore, the entire protocol has cash flow, and USDe is indeed a yield-generating stablecoin supported by income-generating assets.

However, the yield is not automatically distributed to every holder of USDe; only when users stake USDe as sUSDe do they receive protocol dividends. In other words, USDe is a yield-generating stablecoin, but its yield is distributed through sUSDe, and holding USDe itself does not directly entitle users to interest. Users can redeem sUSDe back to USDe at any time, exiting the interest-bearing state.

Furthermore, Ethena employs an off-chain custody mechanism, where all assets supporting USDe are always stored in an institutional-grade exchange's external custody system. Assets only briefly flow to the exchange during funding fee settlements or actual profit and loss events, thereby reducing risk exposure to centralized exchanges.

According to data from Ethena's official website, USDe is currently deployed on 24 public chains, with a user count of 713,000 and a market capitalization of $5.89 billion, making it the fourth-largest stablecoin by market cap, following USDT, USDC, and USDS (DAI).

2.4.2 USDY

USDY (US Dollar Yield Token) is a yield-bearing stablecoin issued by Ondo Finance, which officially defines it as a tokenized note. It is backed by short-term U.S. Treasury bonds and bank demand deposits, held and secured by a trust institution (such as Ankura Trust), ensuring that each USDY is backed by an equivalent amount of U.S. dollar assets. The current market capitalization of USDY is $580 million.

There are two versions of USDY. One is the accumulating USDY, where the token's face value rises daily with earnings, reflecting asset appreciation. The other is rUSDY, which maintains a constant price of $1, with interest returns distributed by increasing the number of tokens. For example, if a user purchases 100 rUSDY at $1 each, when the underlying asset's yield causes the price of USDY to rise to $1.01, the price of rUSDY remains at $1, but the holder's wallet will automatically increase to 101 rUSDY. This entire process is executed automatically daily based on yield conditions. The two versions can be exchanged for each other, allowing users to choose based on their preferences.

USDY is primarily open to non-U.S. individual and institutional investors. After completing KYC, users can purchase USDY via bank wire or using stablecoins (such as USDC, USDT), and the system will start accruing interest. Ondo mints transferable tokens within 40-50 days, during which users will receive temporary receipts, so the actual USDY tokens are typically issued to users' wallets after 40-50 days. Once users' subscription funds enter the system, Ondo Finance will uniformly use these funds to purchase low-risk, high-quality U.S. dollar assets such as short-term Treasury bonds and bank demand deposits, while setting a certain proportion of excess reserves to ensure the adequate collateralization and redemption safety of USDY. Based on the daily interest income generated from these underlying assets, the USDY in users' hands will gradually appreciate (or automatically increase in quantity in the form of rUSDY), achieving a stable peg to the U.S. dollar while automatically earning returns. Throughout this process, users do not need to stake or manually operate; the yield is automatically generated and distributed.

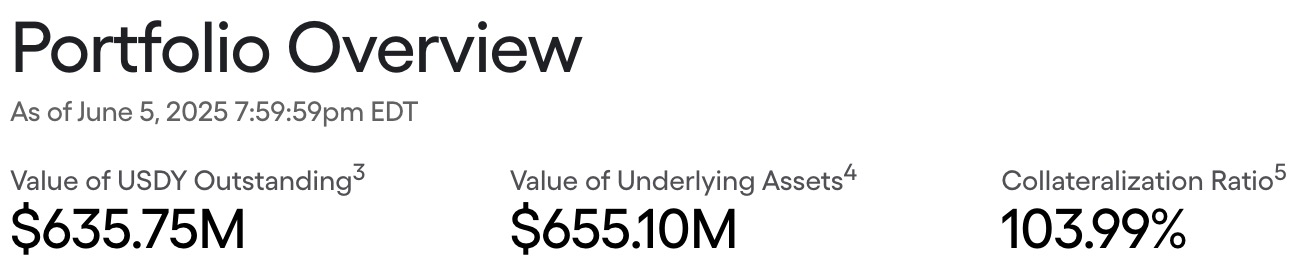

USDY ensures asset transparency and reserve security through various means. Ondo Finance regularly discloses the assets held behind USDY, including short-term Treasury bonds and demand deposits from regulated banks, and manages them through a trusted custody institution. Every week, the official team releases a transparency report detailing USDY's total supply, the proportion of various underlying assets, cash reserves, and yield rates. According to the latest information updated on June 5 from the official website, the USDY system has issued $636 million in stablecoins, backed by real assets valued at $655 million, with a collateralization rate of 103.99%, reflecting high capital safety and sufficient asset backing.

Figure 4. USDY portfolio overview. Source: https://ondo.finance/usdy

2.5 RWA-Supported Stablecoins

RWA (Real World Assets) supported stablecoins refer to stablecoins issued with real assets (such as cash, government bonds, commercial paper, etc.) as reserve backing. These stablecoins typically emphasize asset transparency, compliance, and auditing mechanisms.

2.5.1 USD0

USD0 is an RWA-supported stablecoin launched by Usual Protocol, where all minted USD0 is fully backed by real assets, meaning the reserve amount is greater than or equal to the circulating amount, ensuring a 1:1 peg.

The collateral assets supported by Usual are primarily U.S. Treasury bonds (T-Bills), but it does not directly hold these real-world assets. Instead, it collaborates with professional RWA platforms to achieve access. For example, platforms like Hashnote, Ondo, and Backed hold real short-term Treasury bonds and tokenize them. Usual collaborates with these platforms to bring their issued on-chain T-Bills assets into the protocol as collateral backing for the USD0 stablecoin. To simplify the user experience, Usual packages T-Bills assets from different platforms into a universal collateral asset—USYC. When using it, users do not need to worry about which institution the specific assets come from; they only need to interact with USYC.

There are two ways for users to participate. The first is for users holding tokenized RWA. These users typically obtain tokenized T-Bills through third-party platforms (such as Hashnote) and can collateralize these eligible assets to the protocol via Usual's daoCollateral contract, which will automatically mint USD0 stablecoin at a 1:1 ratio. Upon redemption, users can also use this contract to exchange USD0 back for the original collateral assets. The second way is for users who do not have RWA assets but wish to obtain USD0. These users can choose an indirect participation method: they only need to deposit USDC, and the Usual protocol will call upon USYC assets that have been pre-collateralized by other providers (Collateral Providers) in the system to mint an equivalent amount of USD0 for the user. Meanwhile, the USDC paid by the user will be transferred to the Collateral Provider as their liquidity income source, and the provider will also receive USUAL token incentives.

Through the above mechanisms, users can smoothly participate in Usual's stablecoin system, whether or not they own tokenized RWA. The design of USYC helps the protocol integrate various sources of real-world assets behind the scenes, providing users with a simple, secure, and efficient experience while ensuring stability and compliance.

At the same time, Usual has also launched a derivative product of USD0 called USD0++, which is essentially a yield-bearing USD0. Users can deposit their USD0 into Usual's yield pool, receiving an equivalent amount of USD0++, representing the principal (USD0) they deposited and the interest continuously accumulating in the pool. The protocol uses these deposited USD0 to collateralize and mint more USYC or execute other low-risk RWA strategies, with the generated yield proportionally distributed to USD0++ holders, causing USD0++ to continuously appreciate. When users redeem, they can exchange USD0++ for a larger quantity of USD0, thus obtaining returns. The incentives for USD0++ are released linearly, with a maximum release period of 4 years. If users exit midway or withdraw assets, the unvested incentives will be partially deducted or become unrecoverable. Usual encourages long-term participation in this way, enhancing the protocol's capital stability and liquidity security.

USD0 currently has a market capitalization of approximately $619 million. According to official data from Usual, the collateral assets for USD0 are about $620 million (mainly USYC), with a collateralization rate of 100.81%, indicating sufficient capital reserves.

Figure 5. USD0 reverse data. Source: https://usual.money/

In terms of compliance, Usual does not directly custody real-world assets (such as government bonds) but obtains tokenized versions of these assets (like T-bills tokens) through compliant RWA platforms, which are mostly already in line with relevant financial and securities regulatory standards. The tokenized T-bills issued by these platforms are conducted within a legal framework, providing Usual with a foundation for compliant asset sources. At the same time, the Usual protocol itself is decentralized, with all processes of collateralization, minting, and redemption completed through on-chain smart contracts, without custody of user assets or involvement of centralized clearing agents, thus achieving bankruptcy isolation and security transparency. The overall design avoids the reliance on traditional stablecoins on bank custody, reducing compliance risks, but attention must still be paid to potential regulatory policy changes that partner platforms may face in the future.

2.6 Native Stablecoins of Public Chains/Exchanges

An increasing number of public chains and exchanges are choosing to launch their own native stablecoins. This type of stablecoin is issued by the public chain team or its core ecosystem, specifically designed for the ecosystem of that chain, deeply integrated into core modules such as trading, lending, and governance, aiming to reduce reliance on external stablecoins like USDT and USDC, and enhance the stability and autonomy of the on-chain financial system.

2.5.1 BUSD (Binance USD)

BUSD was initially issued in collaboration between Binance and Paxos Trust Company and is an asset-backed stablecoin. Each BUSD is backed by a real reserve asset of $1, which includes bank deposits or short-term U.S. Treasury bonds, held by the regulated financial institution Paxos in the U.S., and is subject to regular third-party audits to ensure that the number of BUSD on-chain corresponds exactly to the off-chain dollar reserves.

BUSD adopts an off-chain custody and on-chain issuance model, with reserve assets stored in the traditional financial system (such as bank accounts and money market instruments), while the on-chain BUSD (ERC-20 token) is minted and distributed by Paxos, which users can exchange for dollars. Through the Paxos website, users can submit redemption requests to convert BUSD back to off-chain dollars.

In February 2023, the New York Department of Financial Services (NYDFS) required Paxos to stop issuing BUSD, primarily due to a review of its regulatory compliance. Although there were no explicit allegations of wrongdoing against Paxos, regulatory concerns about its compliance risks were raised. Consequently, the official announcement was made to cease the minting of new coins, while existing BUSD could still be redeemed for dollars and continued to be protected by custody. Subsequently, Binance gradually halted new lending activities related to BUSD, canceled trading pairs, and closed withdrawal channels, gradually converting users' BUSD balances into new coins like FDUSD. Currently, it is no longer possible to mint new BUSD through any official or legal channels. Over time, the circulation of BUSD will gradually decrease, ultimately exiting the market. As of now, the market capitalization of BUSD is approximately $310 million.

The BUSD incident highlights the importance of compliance regulation for stablecoins, as compliant stablecoins are more secure for long-term operation. At the same time, this incident reflects the regulatory risks faced by centralized stablecoins and the strong demand for transparency; third-party audits and asset disclosures are key to gaining user trust.

In addition to BUSD, major public chains have also begun exploring and planning their own native stablecoins in recent years to enrich their ecosystems and enhance user experience. For example, Berachain has issued the collateralized stablecoin Honey, which achieves price anchoring through its multi-asset collateral mechanism; Base plans to launch USDb, aiming to create a native stablecoin pegged to the dollar to support a wider range of DeFi applications; Layer 2 solutions like Arbitrum and Optimism are also actively exploring the launch of their own stablecoins to address cross-chain and scalability needs. These stablecoins typically adopt over-collateralization or asset reserve models, balancing security and liquidity, thereby promoting ecosystem prosperity and efficient capital circulation.

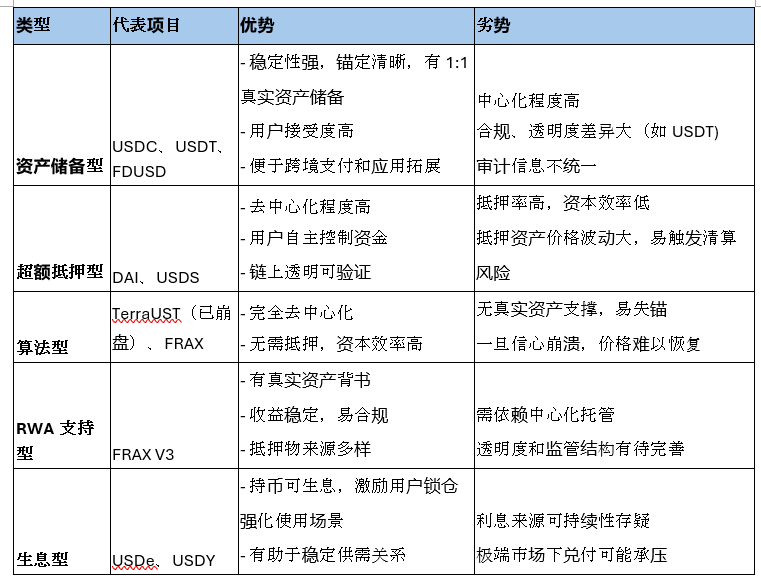

2.7 Comparison of Advantages and Disadvantages of Different Types of Stablecoins

The types of stablecoins mentioned above include: asset-backed, crypto-collateralized, algorithmic, RWA-supported, and yield-bearing stablecoins. Each type of stablecoin has its own strengths and weaknesses in terms of stability, security, degree of decentralization, and compliance.

Fiat-backed stablecoins (such as USDC, USDT, FDUSD) are currently the most widely used and have the most regulatory support. These stablecoins are typically backed by 1:1 dollar or short-term Treasury bonds, held by centralized institutions. This gives them excellent performance in price stability and user acceptance, but they also face issues of centralization and varying transparency, with some projects (like USDT) being questioned due to insufficient information disclosure.

Crypto-collateralized stablecoins (such as DAI, USDS) use on-chain crypto assets like ETH and stETH as collateral to generate stablecoins through over-collateralization. This mechanism has a high degree of decentralization and self-custody of funds, but due to the volatility of the underlying assets, it may trigger liquidation risks. Additionally, low collateral efficiency limits its large-scale use.

Algorithmic stablecoins (such as the now-collapsed TerraUST) attempted to maintain their peg through system algorithms adjusting supply and demand but are prone to collapse when market confidence is low, leading to their gradual elimination in recent years. Some projects (like the original FRAX) adopted partial algorithmic mechanisms but have now transitioned to 100% collateralization to meet stricter regulatory requirements.

RWA-supported stablecoins (such as USD1, Frax V3, sDAI) combine blockchain and traditional financial assets, using real assets like short-term Treasury bonds and money market funds as collateral. These stablecoins have clear advantages in security and compliance and are increasingly favored by policies, but they also face issues of centralized custody and audit dependency.

Yield-bearing stablecoins (such as USDe, USDY) embed yield functions into the stablecoin mechanism, allowing users to automatically earn interest by depositing into the protocol. These stablecoins not only meet basic pegging requirements but also incentivize users to hold and lock up their assets, increasing stability and usage rates. However, if their sources of interest (such as protocol earnings, RWA returns, etc.) are not sustainable, they may face redemption pressure and risks, especially in extreme market conditions that could affect their ability to redeem.

In summary, the future development trend of stablecoins is moving towards greater transparency, compliance, and security. Asset-backed and RWA-type stablecoins may gain a larger market share under policy promotion, while crypto-collateralized stablecoins will continue to play their value in decentralized ecosystems. Each type has its own application scenarios and risks, and users and developers need to make reasonable choices based on their needs.

3. Core Application Scenarios of Stablecoins

As an important component of the cryptocurrency market, stablecoins are price-stable and widely used in various scenarios such as payments, cross-border settlements, DeFi, trading, value storage, and hedging.

3.1 Medium of Exchange

The three main functions of money include a medium of exchange, a measure of value, and a store of value. The medium of exchange refers to a widely accepted medium used for the exchange of goods or assets. Stablecoins can serve as a medium of exchange for on-chain trading matching and settlement, especially in centralized exchanges (CEX) and decentralized exchanges (DEX), for pricing and settlement. Stablecoins act as digital dollars on-chain, widely accepted in the crypto market as an intermediary for exchanging assets and a universal tool for on-chain value transfer. Due to their price pegged to the dollar and low volatility, users frequently use them in cryptocurrency trading. For example, most trading pairs on exchanges like Binance, OKX, and Coinbase are priced in USDT or USDC, with stablecoins typically appearing on the right side of trading pairs.

Figure 6. Stablecoins as a medium of exchange. Source: https://www.binance.com/en/trade/BTC_USDT?type=spot

In DEXs like Uniswap, Curve, and Balancer, stablecoins also play a crucial role as important components of liquidity pairs, primarily serving as intermediaries for trading various assets. Users can more intuitively assess the prices and values of other crypto assets through stablecoins, avoiding trading losses caused by market volatility. Additionally, many DEX asset exchanges are not matched through order books but are completed through liquidity pools, with each pool consisting of two assets, referred to as a liquidity pair, such as ETH/USDT, BTC/USDC, etc. Liquidity providers (LPs) deposit these two assets in pairs into the pool for others to trade. This helps users buy and sell crypto assets more smoothly, enhancing the overall trading experience. Stablecoins can also circulate quickly between different protocols, becoming the most commonly used and important medium for on-chain value transfer.

3.2 Multiple Roles of Stablecoins in DeFi

Stablecoins play a core role in the DeFi ecosystem, widely used in lending, trading, liquidity provision, and re-staking scenarios.

In lending scenarios, stablecoins can serve as both borrowing assets and collateral assets. For example, in mainstream lending protocols like Aave and Compound, users can collateralize crypto assets to borrow a stablecoin equivalent to a certain percentage of the collateral value to meet liquidity needs. For instance, if a user holds 10 ETH but does not want to sell it, they can choose to collateralize their ETH in a lending protocol like Aave to borrow stablecoins like USDC or DAI equivalent to 60%-75% of the collateral value. Stablecoins are stable in price and have good liquidity, allowing users to invest elsewhere, participate in other projects, or purchase goods. This way, users retain long-term ownership of ETH while obtaining flexible stablecoins for use. If market fluctuations cause the value of the collateralized assets to drop below a certain threshold, the protocol will automatically liquidate the collateral to prevent bad debts.

At the same time, for users with lower risk tolerance, stablecoins can also be used as collateral to borrow other tokens. For example, a user with 10,000 USDC can collateralize it in a lending protocol to borrow tokens like ETH to participate in liquidity mining, leverage operations, or simply earn deposit interest. This method carries relatively lower risk, as stablecoins have low price volatility and easy redemption, making them suitable for conservative investors.

According to CoinLaw data statistics (https://coinlaw.io/stablecoin-statistics/), the total locked value (TVL) of the entire DeFi system reached $120 billion in 2024, with stablecoins contributing 40%, highlighting the important position of stablecoins in lending, trading, and liquidity pools., the total locked value (TVL) of the entire DeFi system reached $120 billion in 2024, with stablecoins contributing 40%, highlighting the important position of stablecoins in lending, trading, and liquidity pools.)

In addition, stablecoins also play a key role in liquidity staking (LRT) and restaking protocols. Represented by EigenLayer, these protocols view stablecoins as low-risk, highly liquid underlying assets. On one hand, stablecoins are often used to establish risk buffer pools to help users cope with staking losses or slashing events; on the other hand, many protocols use stablecoins as a means of profit distribution to avoid the uncertainties brought by the volatility of platform tokens. Some protocols also support using stablecoins alongside other assets as composite collateral, improving capital utilization efficiency. For institutional users with lower risk tolerance, the participation of stablecoins also enhances their trust and willingness to engage in the restaking ecosystem.

Overall, stablecoins have become an indispensable value anchor and liquidity engine in the DeFi system, not only enhancing the security and capital efficiency of protocols but also providing users with a more robust way to participate.

3.3 Payments and Settlements

Stablecoins are gradually being used for payments and cross-border settlements worldwide. Their greatest advantages are fast transfers, low fees, and global acceptance, making them a substitute for the slow and costly transfer processes in traditional banking systems. For example, using stablecoins for cross-border remittances incurs fees that are less than half of those charged by traditional banks, and funds can arrive within minutes. According to CoinLaw data, in 2024, the adoption rate of stablecoins globally increased by 22%, particularly favored by users in emerging markets, as they effectively combat local currency inflation. Additionally, 50% of cross-border digital transactions utilized stablecoins, highlighting their important position in global payments. In terms of remittances, using stablecoins can save an average of about 4.5% in fees compared to traditional banking channels, significantly reducing the cost of cross-border transfers.

On the retail side, consumer usage of stablecoins is also rapidly growing. By 2024, over 25,000 merchants globally accepted stablecoin payments, with approximately 15% of e-commerce transactions using stablecoins. When using stablecoins for payments in physical stores or online, users enjoy a pleasant experience of real-time checkout and low costs, avoiding intermediary clearing methods.

Figure 7. Stablecoins gain traction in retail e-commerce transactions in 2024. Source: https://coinlaw.io/stablecoin-statistics/

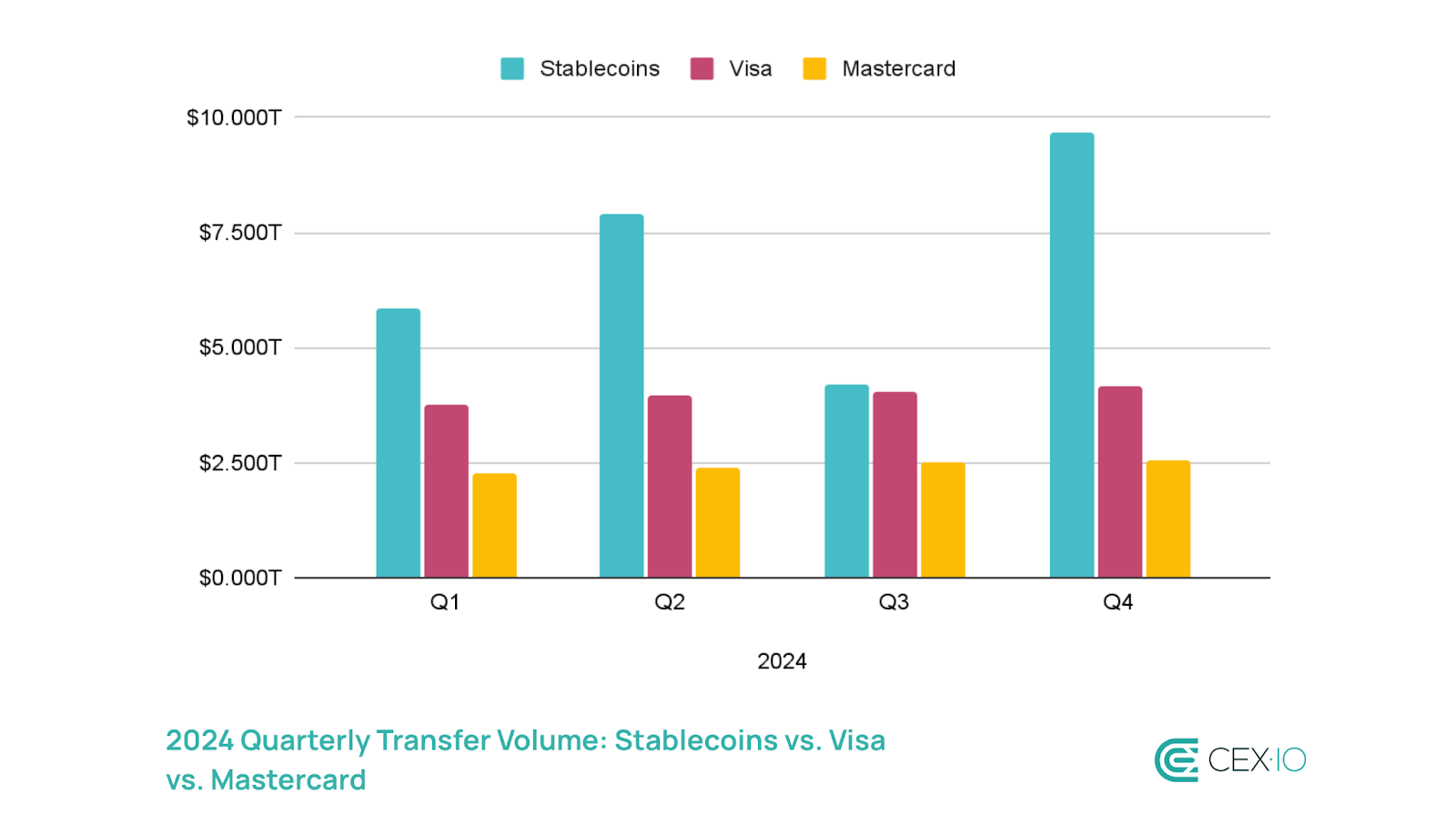

Moreover, in commercial payment scenarios, stablecoins are gradually becoming the preferred choice for corporate salaries and supplier settlements. According to Rise Works' 2024 Annual Report, 65% of salaries in corporate payments within the crypto sector are paid in stablecoins like USDT and USDC. Major payment companies like Visa and Stripe have also integrated stablecoins (such as USDC) into their settlement networks. According to data from CEX.IO, the total transaction volume of stablecoins in 2024 reached between $27 trillion and $35 trillion, surpassing Visa and Mastercard. The application of stablecoins in 2024 has expanded into the tokenized asset field, supporting over $250 billion in on-chain securities transactions, showcasing their new role in financial asset issuance and settlement.

Figure 8. 2024 Quarterly Transfer Volume: Stablecoins vs. Visa vs. Mastercard. Source: https://blog.cex.io/ecosystem/stablecoin-landscape-34864

It is evident that stablecoins are changing traditional payment systems, playing an increasingly significant role, especially in international payments, corporate settlements, and the digital economy.

3.4 Store of Value and Hedging Asset

Due to their peg to the dollar and stable value, stablecoins are becoming an important store of value and hedging asset for users worldwide.

A store of value refers to an asset that can maintain its value over the long term and is not easily depreciated, suitable for preservation for future use, such as gold or the dollar, which are typical store of value tools. For many users living in high-inflation countries, stablecoins are equivalent to digital dollars, providing a convenient and secure means of preserving value. In countries like Argentina, Nigeria, and Venezuela, where local currencies continue to depreciate, many residents find it difficult to easily obtain dollar accounts or physical cash. However, stablecoins can be held, transferred, and stored with just a crypto wallet, bypassing banks and foreign exchange restrictions, without relying on any intermediaries; users only need to remember their private keys to control their wealth.

Stablecoins also serve as a hedging asset. During periods of economic turmoil, local currency depreciation, or war conflicts, users can hedge risks and avoid wealth shrinkage by converting their assets into USDT or USDC. For example, in 2023, Argentina's annual inflation rate reached about 140%, while USDT, pegged to the dollar, maintained a stable 1:1 ratio, making it very popular locally. In war-torn or financially controlled countries like Ukraine and Lebanon, stablecoins have also become an important tool for users to safeguard their assets by circumventing the banking system. Additionally, an increasing number of users in Latin America and Africa are choosing to convert their wages or savings into stablecoins for long-term holding. Cross-border e-commerce and freelancers often use stablecoins for payments to avoid exchange rate losses; crypto investors also convert their assets into stablecoins after cashing out during bull markets to hedge risks and wait for the next opportunity.

A wealth of data also validates this trend. According to Chainalysis' 2024 Annual Report (https://www.chainalysis.com/blog/subsaharan-africa-crypto-adoption-2024/), stablecoin trading volume on non-U.S. platforms accounts for over 60% of global trading volume, primarily concentrated in emerging markets., stablecoin trading volume on non-U.S. platforms accounts for over 60% of global trading volume, primarily concentrated in emerging markets.) The latest report released by Chainalysis in 2025 (https://www.chainalysis.com/blog/stablecoin-innovation-in-2025-ep-159/) indicates that in Sub-Saharan Africa, over 30% of on-chain transactions involve stablecoins, with a large portion used for remittances, savings, and daily payments; stablecoins (especially USDT and USDC) have become key means for users in these regions to cope with local currency depreciation and achieve digital savings. indicates that in Sub-Saharan Africa, over 30% of on-chain transactions involve stablecoins, with a large portion used for remittances, savings, and daily payments; stablecoins (especially USDT and USDC) have become key means for users in these regions to cope with local currency depreciation and achieve digital savings.)

These data and scenarios indicate that stablecoins are not only financial innovation tools but are also becoming widely applicable digital savings and hedging solutions in the real world.

4. Market Status and Development Trends

4.1 Total Market Capitalization and Change Trends

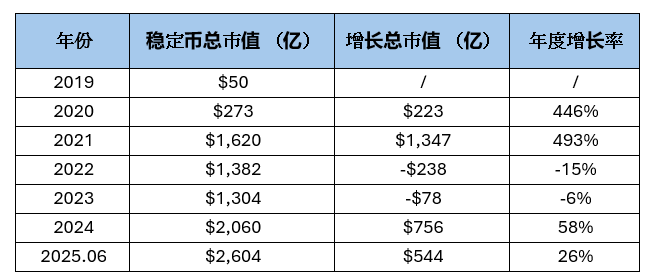

The table below shows the changes in the total market capitalization of stablecoins in recent years, clearly reflecting the market growth trajectory of stablecoins. As of June 13, 2025, the total market capitalization of global stablecoins has reached $260.4 billion, an increase of $54.4 billion compared to the entire year of 2024, with an annual growth rate of 26%. Compared to the starting point of only $5 billion in 2019, the market size of stablecoins has achieved explosive growth of over 5100% (51 times) in less than six years.

From a trend perspective, the market capitalization of stablecoins exhibited exponential growth in 2020 and 2021, increasing by 446% and 493%, respectively, benefiting from the DeFi boom, the rise of on-chain assets, and the surge in demand for stable dollar assets during the COVID-19 pandemic. In 2022 and 2023, the market experienced a brief decline, decreasing by 15% and 6%, respectively, mainly due to the negative impacts of the Terra collapse, tightening macro interest rate environments, and the FTX collapse. Starting in 2024, the market has resumed a growth trend, with an annual increase of 58%, and the first half of 2025 continues this upward trend, reflecting the rising demand for stablecoins in emerging fields such as the Web3 ecosystem and RWA (real-world assets).

Changes in stablecoin market capitalization. Data Source: https://defillama.com/stablecoins

This market capitalization trend not only reflects the increasing market recognition of stablecoins in crypto finance but also indirectly indicates the continuous rise in the usage of stablecoins in scenarios such as DeFi, payments, RWA, cross-border settlements, Web3 gaming, and the metaverse. Currently, over 70% of DeFi transactions, 65% of Web3 gaming payments, and more than half of on-chain cross-border payments are already using stablecoins as the primary medium.

In the future, as stablecoin regulatory policies gradually clarify (such as MiCA and the GENIUS Act), the ecosystem of compliant stablecoins accelerates (such as USDC and PYUSD), and sovereign countries explore mechanisms for the coexistence of central bank digital currencies (CBDCs) and stablecoins, the stablecoin market is expected to welcome a new growth inflection point.

4.2 Competitive Landscape and Market Structure

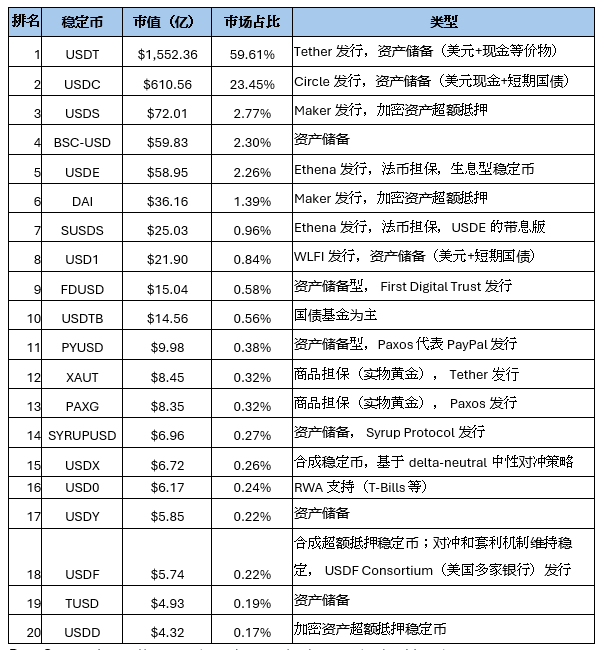

As mentioned above, the total market capitalization of stablecoins globally has reached $260.4 billion, showing a growth trend. The table below lists the top 20 stablecoins by market capitalization on Coingecko (data as of June 13). Let's take a look at the current overall competitive landscape and market structure of the stablecoin market.

Data Source: https://www.coingecko.com/en/categories/stablecoins

Overall Competitive Landscape

As of June 2025, the total market capitalization of stablecoins has exceeded $260 billion, with Tether's USDT and Circle's USDC accounting for over 83% of the market share. USDT dominates the market with a market cap of $155.2 billion, representing nearly 60%, far surpassing other competitors. USDC follows closely with a market cap exceeding $61 billion, accounting for about 23%. Together, they form a duopoly in the stablecoin market, firmly holding a dominant position.

In terms of overall market share, the second tier includes USDS, BSC-USD, USDE, DAI, etc., with their market caps mostly ranging between $3.5 billion and $7 billion, and market shares between 1% and 3%. These stablecoins are vying for market share through differentiated positioning. For example, MakerDAO's DAI, as a representative of decentralized crypto-collateralized assets, although its market share is only about 1.4%, still holds a place in the DeFi ecosystem, and the USDS launched by Maker ranks third in market cap, with DAI being convertible to USDS. This tier also includes some innovative stablecoins, such as USDE launched by Ethena Finance, which combines stablecoins with yield generation, and has a market cap exceeding $5.5 billion, attracting widespread market attention. Currently, this tier has not yet formed a stable leader and remains in a constantly changing competitive state.

The tail market is even more fragmented and competitive. Stablecoin projects ranked below the top 10 generally have market caps below $1.5 billion, with market shares mostly below 0.5%. Most of these projects are new attempts in vertically segmented fields, such as commodity-backed stablecoins like XAUT and PAXG, new stablecoins supported by RWA (real-world assets) (like USD0 and USDTB), or synthetic stablecoins (like USDX and USDF) that maintain stability through hedging strategies. Although their market shares are limited, they bring innovative vitality to the market and represent potential future development directions.

Overall, the current stablecoin market presents a structure of head monopoly and mid-tail competition. Most users still prefer the longest-standing, largest, and most liquid mainstream stablecoins, but new types of products are gradually emerging to meet diverse needs. The future landscape may still undergo structural adjustments with technological breakthroughs, regulatory changes, and innovations in yield design.

Market Structure and Type Distribution

Currently, asset-backed stablecoins are the absolute mainstream in the stablecoin market, accounting for over 90% of the market share. Representatives of this type include USDT, USDC, etc., which typically achieve value anchoring and ensure capital liquidity by holding cash in USD or short-term U.S. Treasury bonds. The advantages of asset-backed stablecoins lie in their price stability, low entry barriers, and high market acceptance, making them the preferred choice for exchanges, DeFi protocols, and even centralized financial (CeFi) services. For example, USDT is widely used as a base asset for trading pairs on exchanges due to its large circulation and support for multiple chains.

In contrast, the market share of crypto asset over-collateralized stablecoins represented by DAI and USDD is still less than 2%. These stablecoins do not rely on the traditional financial system but are issued through collateralization with crypto assets (like ETH), possessing stronger decentralization attributes and resistance to censorship. Although they play an important role in the DeFi ecosystem, their higher volatility and complex mechanisms mean they are currently mainly used by crypto-native users and have not yet become mainstream choices.

It is worth noting that new types of stablecoins are rapidly developing, especially those that combine yield mechanisms and RWA real assets, which are gaining increasing attention. For example, "yield-bearing stablecoins" like USDE and SUSDS provide passive income to users by holding interest-generating assets, meeting the higher demand for capital efficiency from institutions and high-net-worth users. Stablecoins like USD0 and USDTB, supported by real-world assets (RWA), attempt to bring traditional financial assets (like government bonds) on-chain, following a compliance route that makes it easier to gain acceptance in regulatory-friendly ecosystems.

Additionally, there are some commodity-backed (like gold-backed XAUT and PAXG) and synthetic stablecoins (like USDX and USDF) that occupy a small portion of the market. Although these products are smaller in scale, they provide users with inflation hedging and diversified investment options, reflecting the diversity of stablecoin design ideas.

At the same time, traditional financial institutions and Web2 giants are also accelerating their layouts. For example, PayPal's PYUSD, with a market cap of nearly $1 billion, marks the transition of stablecoins from crypto-native assets to mainstream payment tools. It is evident that stablecoins are gradually shifting from basic payment mediums to multifunctional roles such as value storage, yield generation, and asset mapping, playing an increasingly critical role in the integration of Web3 and traditional finance.

4.3 On-Chain Data Analysis

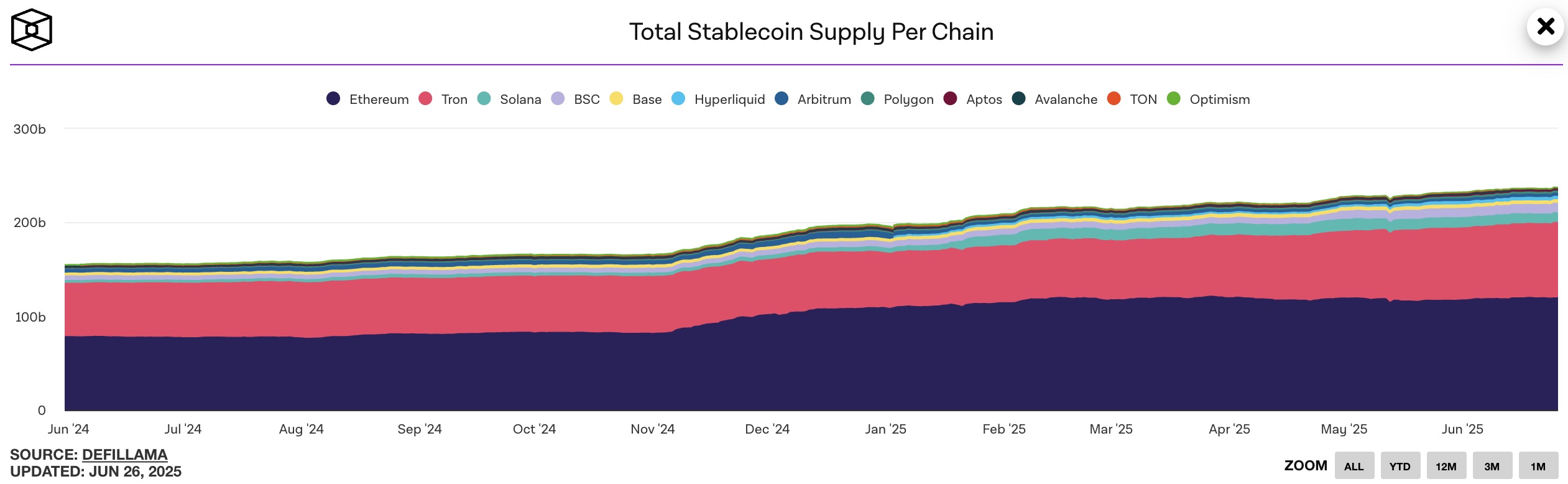

Comparison of Stablecoin Supply Across Different Public Chains

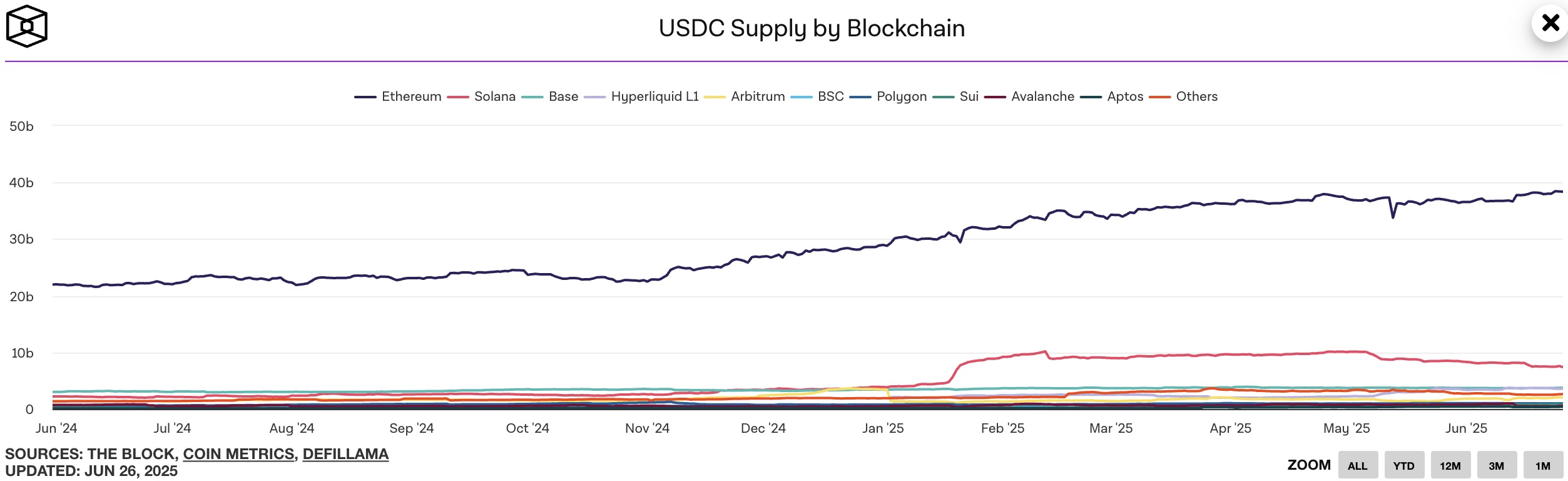

The following chart shows the supply of stablecoins across various public chains as reported by The Block. It is evident that the distribution of stablecoins across different chains presents a clear differentiation pattern. Ethereum remains the main chain for stablecoin issuance, firmly holding a dominant market position. Tron follows closely, with the total supply of stablecoins continuing to grow, showing a trend of approaching or even surpassing Ethereum.

Figure 9. Total Stablecoin Supply Per Chain. Source: https://www.theblock.co/data/stablecoins/usd-pegged/total-stablecoin-supply-per-chain

Specifically, the total supply of stablecoins on the Ethereum chain has grown from $78.8 billion in June 2024 to $120.2 billion in June 2025, with an annual growth rate of 52.5%. Meanwhile, the supply of stablecoins on the Tron chain has increased from $56.9 billion during the same period to $80.5 billion, with a growth rate of 41.5%, demonstrating strong growth momentum. Notably, Solana's stablecoin supply has surged from $3 billion a year ago to the current $10.3 billion, with an impressive annual growth rate of 243%.

This growth trend reflects a clear market signal: users' preference for low-fee, high-performance public chains is increasing. Against the backdrop of generally high fees on the Ethereum network, chains like Tron and Solana are gradually attracting a large number of stablecoin users and related DeFi activities due to their low costs and fast transactions. This not only changes the on-chain distribution pattern of stablecoins but also boosts the activity and growth potential of emerging public chain ecosystems.

As stablecoins begin to be deployed across multiple chains such as BNB, Avalanche, Polygon, Arbitrum, and Base, the entire stablecoin market is transitioning from a single mainnet to a multi-chain parallel structure. Cross-chain deployment provides broader development space for DeFi protocols, payment scenarios, and bridging applications.

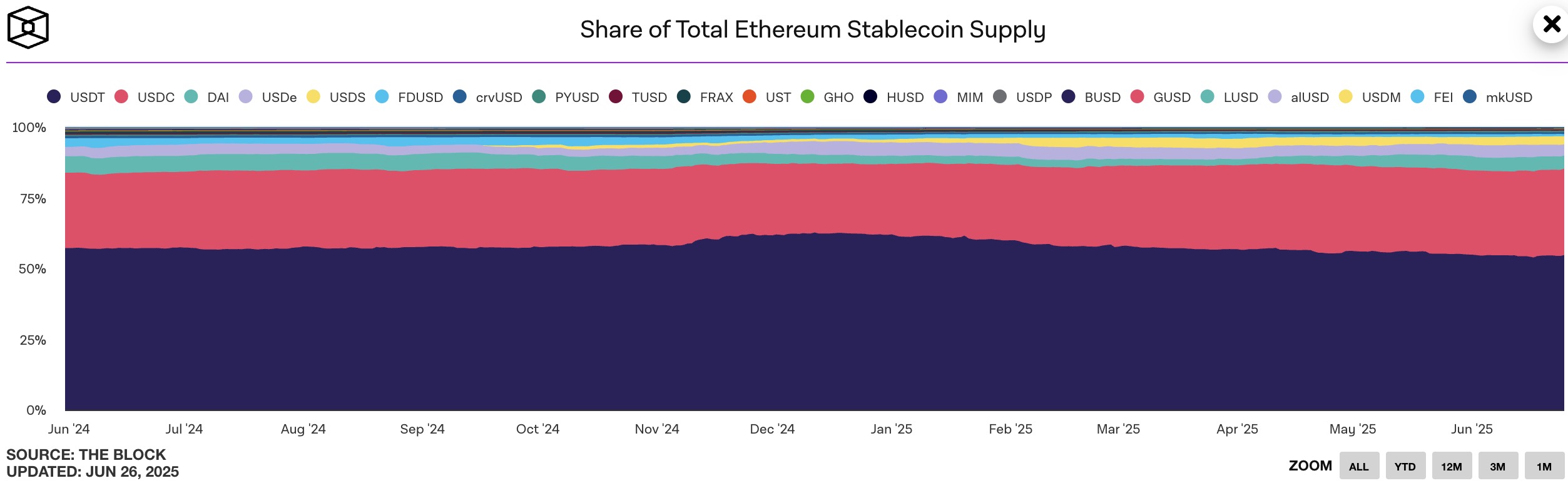

Proportion of Stablecoins on the Ethereum Chain

As the largest DeFi public chain, Ethereum is also the ecosystem where stablecoins are most widely used. From the perspective of stablecoin supply proportions, the current structure of stablecoins on Ethereum shows a clear concentration trend. USDT (Tether) remains the largest stablecoin on Ethereum, with a supply exceeding 50% of the total stablecoin supply on Ethereum. Despite transparency and regulatory controversies, USDT is still the preferred base stablecoin for many users and platforms due to its early issuance and wide range of trading pairs.

Following USDT, USDC accounts for about 25%-30% of the supply on Ethereum. Although it is not as much as USDT, its transparent reserves, public audits, and strong compliance make it more favored in institutional, payment, and compliance scenarios. With the implementation of the U.S. GENIUS Act and the EU MiCA Act, USDC's compliance advantages may further enhance its market share.

In addition to these two mainstream centralized stablecoins, there is also a group of new or decentralized stablecoins on Ethereum. DAI is the oldest decentralized stablecoin, generated through over-collateralization of crypto assets. USDe (Ethena) is a yield-bearing stablecoin that generates returns through hedging mechanisms and is growing rapidly. USDS, launched by MakerDAO's upgraded Sky Protocol, is also experiencing rapid growth. Although these stablecoins currently have relatively low market shares, they represent new attempts and directions, attracting increasing attention.

Overall, the stablecoin ecosystem on Ethereum presents a scenario where USDT dominates, USDC and decentralized stablecoins grow steadily, and new stablecoins gradually rise. This also reflects that users, when using stablecoins, make different trade-offs between compliance, liquidity, decentralization, and yield.

Figure 10. Share of total Ethereum stablecoins supply. Source: https://www.theblock.co/data/stablecoins/usd-pegged/share-of-total-stablecoin-supply

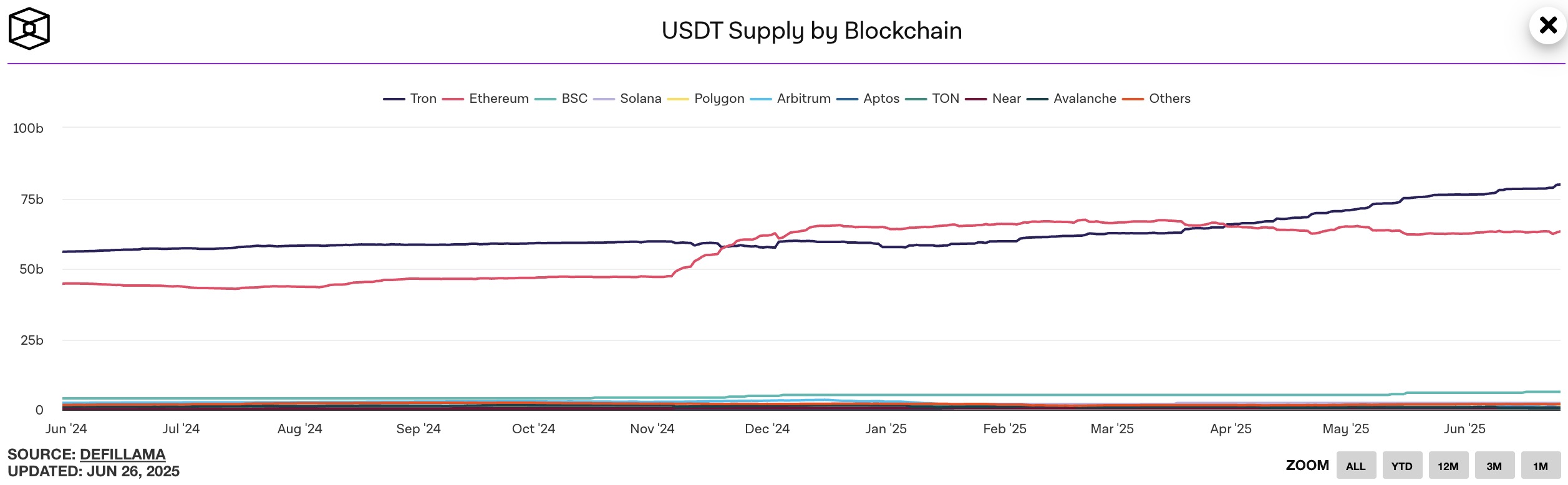

Distribution of USDT and USDC Across Different Chains

According to on-chain stablecoin distribution data provided by The Block, Tron and Ethereum are currently the main issuance and circulation chains for USDT. From the second half of 2024 to the present, the supply of USDT on Tron has remained stable between $56 billion and $59 billion, mostly higher than that on Ethereum. In early 2025, Ethereum briefly surpassed Tron, but since April, Tron has regained its lead. As of now, the supply of USDT on Tron has reached $79.8 billion, while Ethereum's supply is $63.2 billion.

Figure 11. USDT supply by blockchain. Source: https://www.theblock.co/data/stablecoins/usd-pegged/usdt-supply-by-blockchain-daily

This trend reflects the core competitiveness of the two chains. Ethereum has the most mature DeFi ecosystem and high interoperability, attracting a large number of high-value transactions and institutional users. In contrast, Tron has become the ideal choice for small payments, cross-border transfers, and high-frequency trading due to its low fees and high transaction speeds. In addition to Ethereum and Tron, USDT is also deployed across multiple chains such as BNB, Polygon, Avalanche, and Solana, enhancing its accessibility and flexibility among different global user groups.

Compared to USDT, USDC, as the second-largest stablecoin by market capitalization, is more concentrated on Ethereum. Over the past year, the supply of USDC on Ethereum has grown from $21.9 billion to $38.3 billion, with an annual growth rate of 74.8%, showing strong upward momentum. Circle's compliance efforts and the transparent reserve structure of USDC make it the preferred stablecoin for scenarios such as DeFi and RWA.

Figure 12. USDC supply by blockchain. Source: https://www.theblock.co/data/stablecoins/usd-pegged/usdc-supply-by-blockchain

Currently, the second-largest supply of USDC on-chain is on Solana, followed by Base. Notably, the supply of USDC and USDT on Solana and Base is showing a continuous growth trend. Solana, with its high-performance architecture, extremely low fees, and rapidly growing ecosystem in recent years, such as the rise of DeFi protocols like Jupiter, Jito, and Pump.fun, has become an important public chain for the surge in on-chain trading volume. As the core of DeFi liquidity, stablecoins have also increased accordingly. Additionally, Circle's native support for Solana has further propelled the growth of USDC. Base, as the L2 network launched by Coinbase, has quickly gathered a large number of developers and users, especially in the second half of 2024, leveraging the MemeFi and Layer2 boom. Stablecoins, as important mediums for on-chain asset interactions, naturally become the first choice for asset inflows.

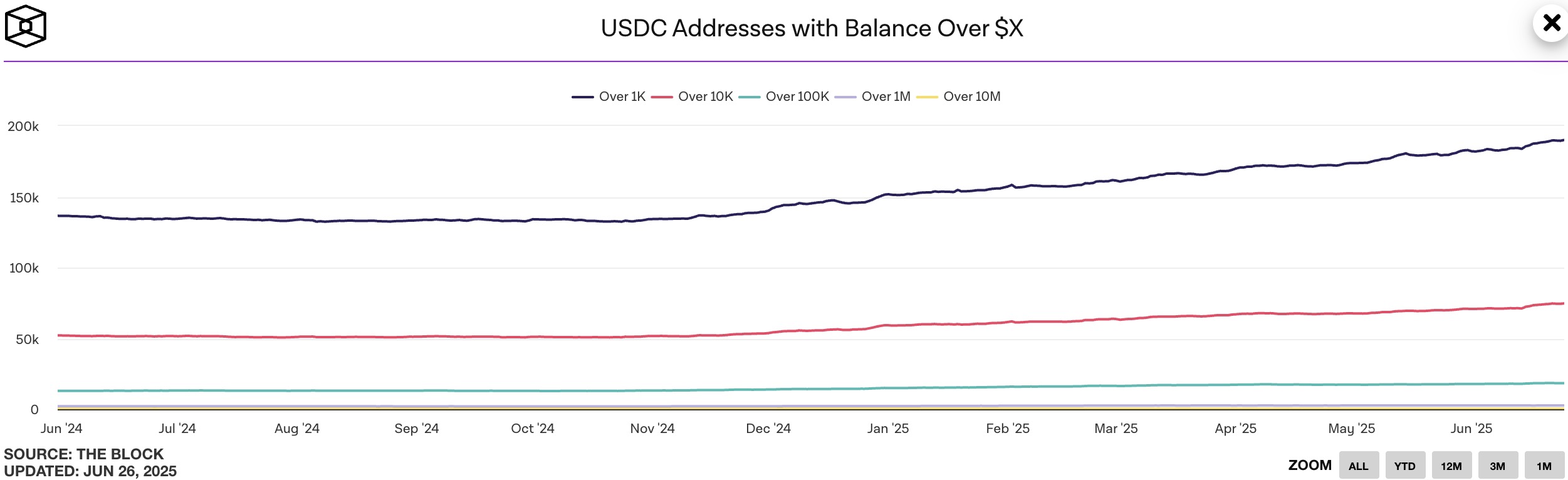

USDC Active Address Analysis

According to on-chain data from The Block, among the USDC holding addresses on Ethereum, the number of small and medium-sized holding addresses is the highest, primarily including addresses holding over $1k and $10k, and this number is continuously growing. This indicates that the user activity of USDC is steadily increasing, with this segment of users mainly using USDC for transfers, payments, storage, and DeFi trading scenarios. The number of large holding addresses over $10M is relatively small, around 379. Most of these large holders are exchange wallets, clearing pools, and DeFi protocol treasuries, used to support liquidity and settlement, reflecting that USDC is not only popular among retail investors but also favored by many institutions and protocols.

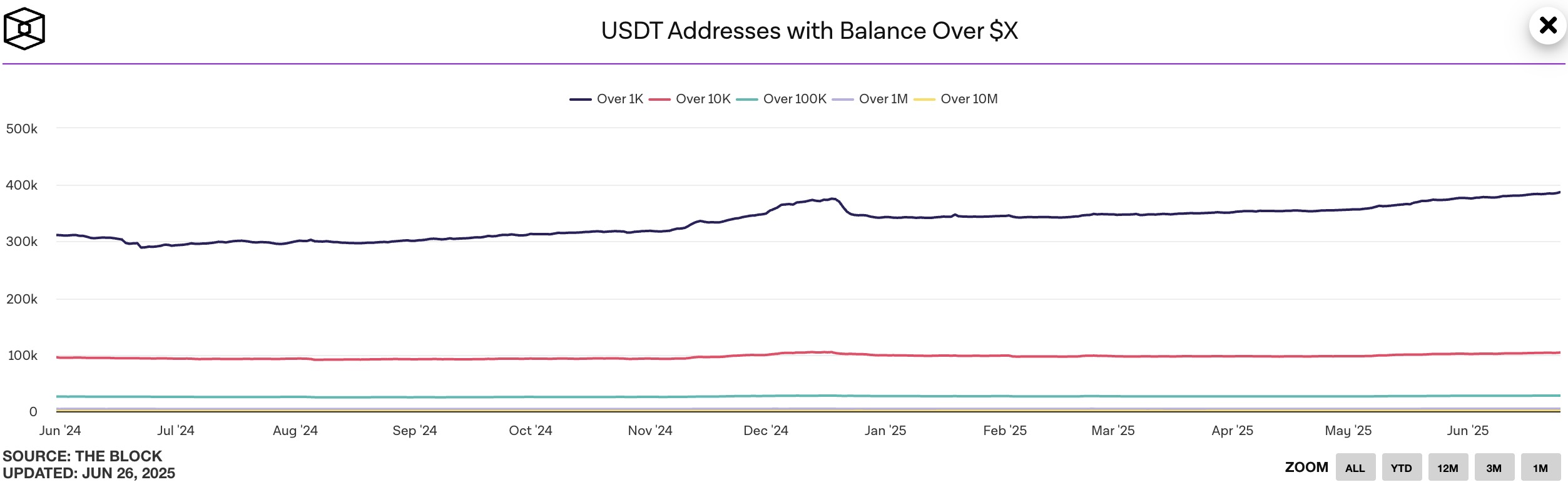

Figure 13. USDC addresses with balance over $X. Source: https://www.theblock.co/data/stablecoins/usd-pegged/usdc-addresses-with-balance-over-x

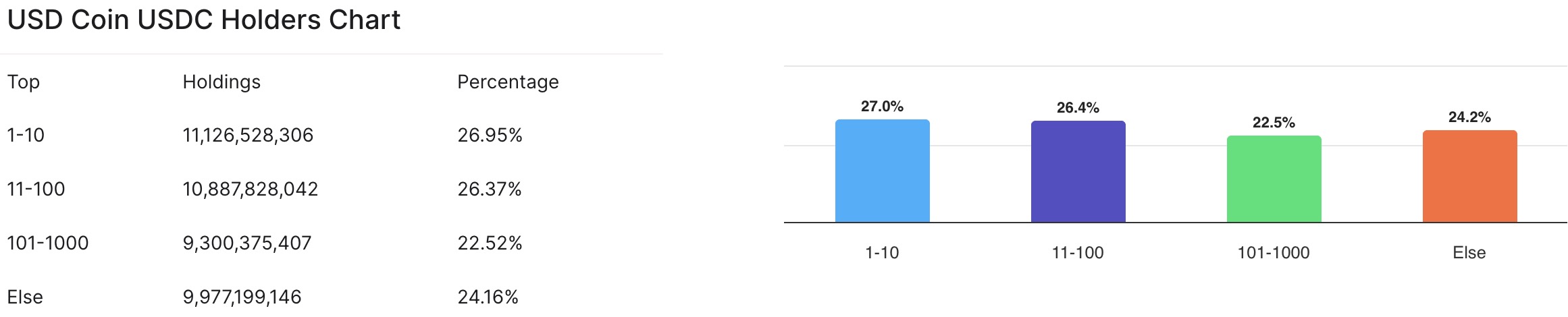

The rich list from CoinLore shows that the top 10 addresses of USDC hold about 26% of the supply, while the top 100 addresses hold 53%, indicating that USDC is not a highly decentralized crypto asset. These addresses often belong to centralized exchanges (such as Binance and Coinbase), custodial institutions, or on-chain protocol pools, which means that any liquidity issues on-chain (such as large withdrawals) could cause significant market fluctuations. Additionally, centralized control also comes with compliance risks and regulatory intervention capabilities. For example, Circle, the issuer of USDC, has repeatedly cooperated with regulators to freeze illegal addresses, which enhances compliance but also weakens resistance to censorship and the spirit of decentralization.

Figure 14. USD Coin USDC Rich List. Source: https://www.coinlore.com/coin/usd-coin/richlist?

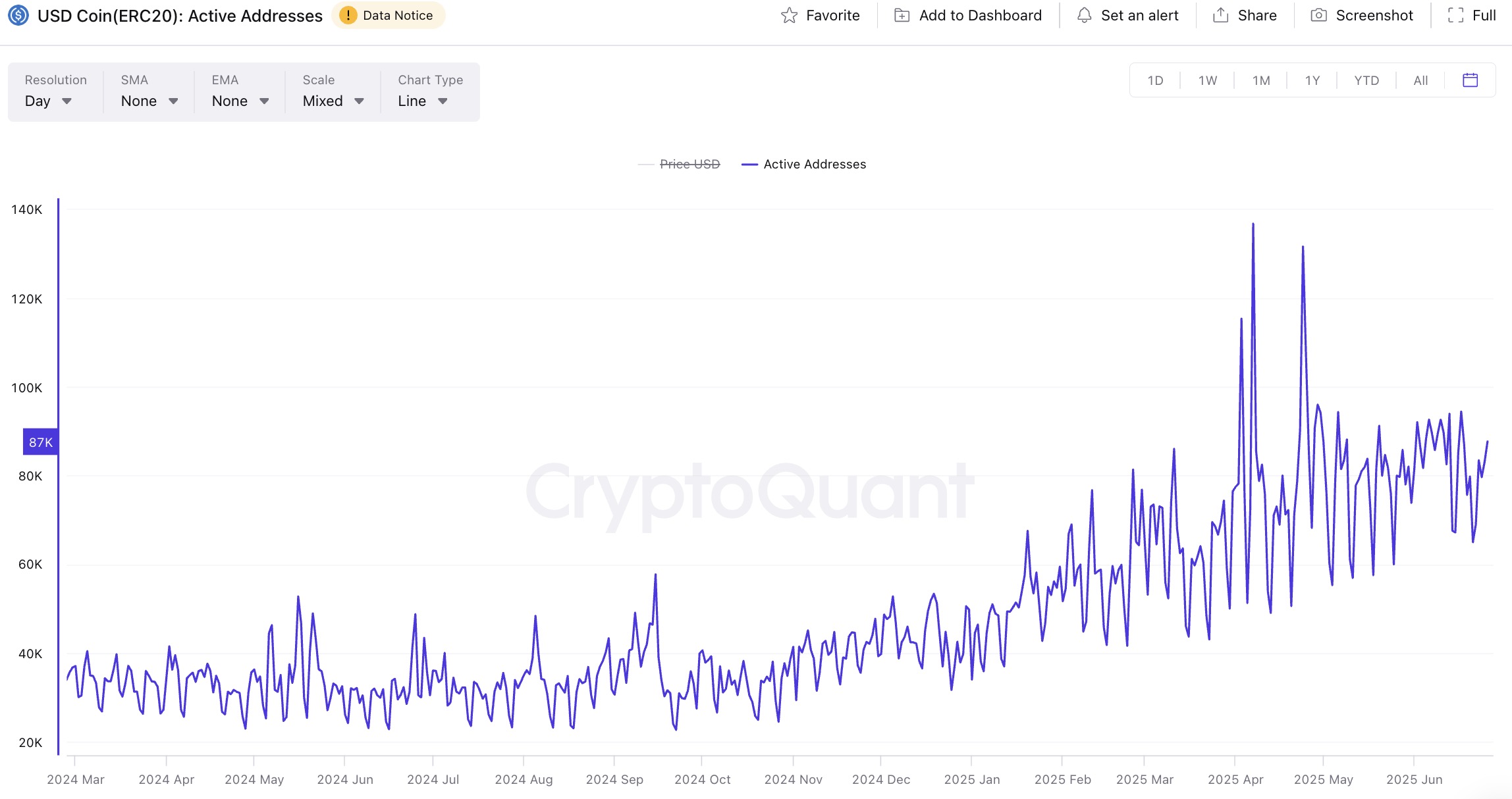

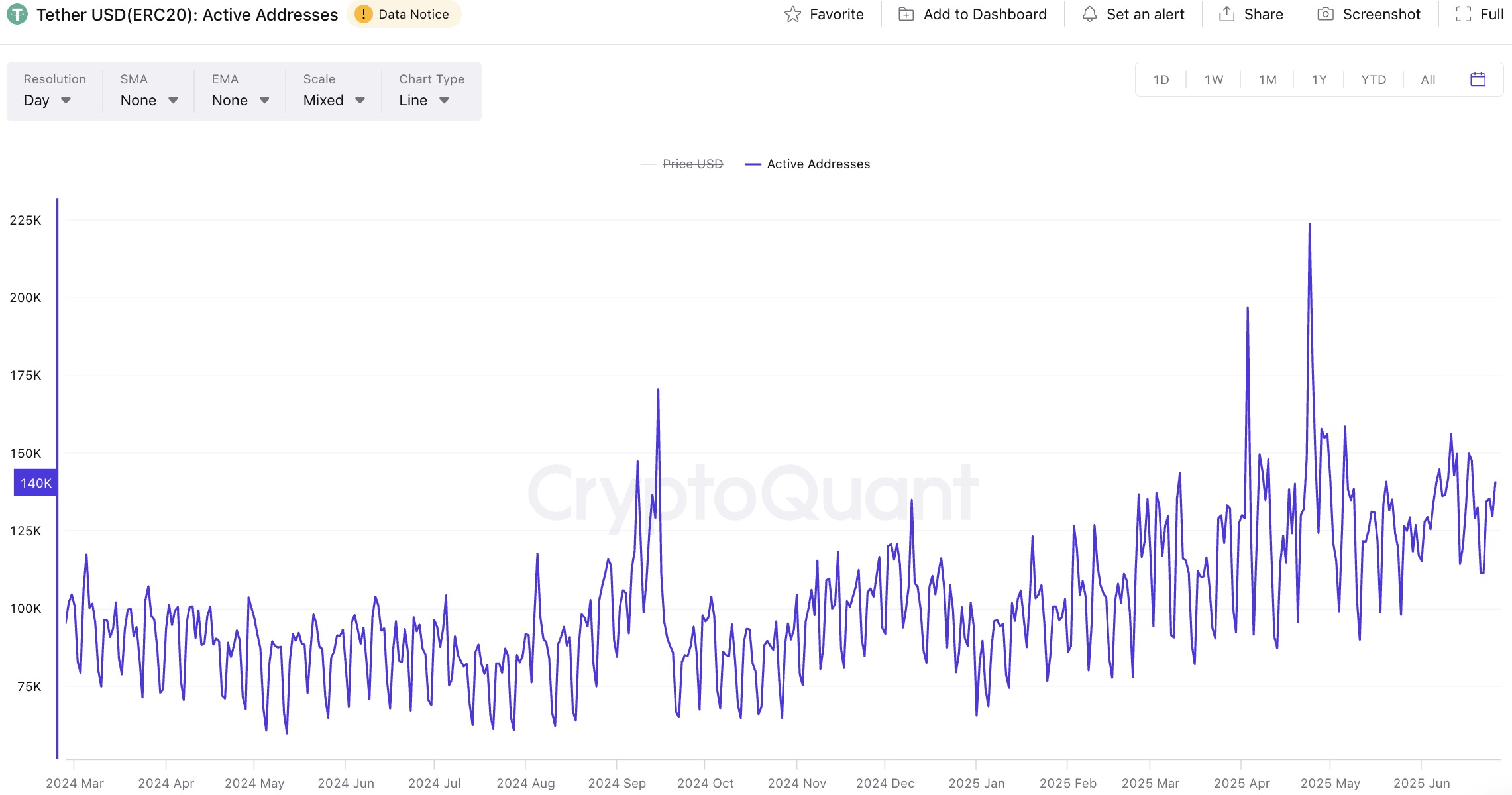

CryptoQuant data shows that the active addresses of USDC (ERC-20) have steadily increased since 2024, with the highest daily active addresses reaching 136,000, reflecting the increasing frequency of daily USDC usage by users. Although Ethereum transaction fees are relatively high, its deep DeFi ecosystem remains the core application scenario for USDC. This also indicates that, despite Layer2 and new public chains like Solana and Base having advantages in user activity, Ethereum's role as the main DeFi ecosystem remains solid.

Figure 15. USDC(ERC-20) active addresses. Source: https://cryptoquant.com/asset/usdc/chart/addresses/active-addresses?window=DAY&sma=0&ema=0&priceScale=log&metricScale=linear&chartStyle=line

USDT Active Address Analysis