Original Title: "A Comprehensive Summary of the 2025 Berkshire Shareholders Meeting: Buffett Discusses 'Retirement', Trade, Cash Deployment, American Exceptionalism, and US Stock Market Volatility"

Original Source: Wall Street Insights

The annual event in the investment world—the Berkshire Hathaway Shareholders Meeting—kicked off on May 2. The Q&A session for shareholders began at 9 PM Beijing time on Saturday, May 2. The "Oracle of Omaha," Warren Buffett, participated throughout the event, accompanied by his CEO successor—Greg Abel, head of Berkshire's non-insurance businesses, and Ajit Jain, head of the insurance business, to answer shareholder questions.

Here are the key points from Buffett's shareholders meeting summarized by Wall Street Insights:

1) On Trade

"Trade should not be a weapon," the US should seek to trade with other countries, doing what each does best. Protectionist policies are a "serious mistake."

2) On America

"Fiscal policy is my biggest concern in the US," when the government takes irresponsible actions, the value of currency can be 'frightening.' Buffett hinted at a full bet on America, supporting American exceptionalism, stating that his luckiest day was the day he was born in America, which is a model of capitalism.

3) On Japan

We will not easily invest overseas unless I believe it is a truly significant opportunity. I plan to continue holding shares in Japanese trading companies for fifty to sixty years. Even if the Bank of Japan raises interest rates, he does not consider selling. Berkshire's current investment in Japan has reached $20 billion, and I even wish we had invested $100 billion instead of $20 billion.

4) On US Stocks

The recent fluctuations in US stocks are 'not significant,' compared to past crashes, 'it is not a severe bear market,' nor is it a similar situation.

5) On Record Cash Reserves

Regarding how to utilize Berkshire's record cash reserves, there may be investment opportunities in the next five years. Recently, Berkshire almost made a $10 billion investment.

6) On Successors

Greg Abel, head of Berkshire's non-insurance businesses, is expected to take over as CEO by the end of the year. He will not sell any of his Berkshire shares and will gradually donate them.

7) On Berkshire

If one day Berkshire's stock price drops by half, it would be an opportunity for me. It’s not that I have no emotions, but stock price fluctuations will not sway my rational judgment. It will not affect my assessment of value. Overall, Berkshire's profitability will continue to grow over time.

8) On Investment Companies

Buffett believes the balance sheet is a good starting point for assessing whether a company is worth investing in. He said, "I spend more time studying balance sheets than looking at income statements. Wall Street doesn't pay much attention to balance sheets, but I like to look at a company's balance sheet from eight to ten years before looking at the income statement because some things are harder to hide or manipulate on the balance sheet."

9) On Young Investors

If you have a direction in life, you should strive to make those you respect and aspire to be your friends. The fastest path to success is to find truly excellent people and walk alongside them. At the end of the Q&A session, Buffett announced that he plans to propose to the board to step down as CEO by the end of this year. This will mark the beginning of the end of the "Buffett era" at Berkshire. Investors should prepare for a Berkshire without Buffett at the helm.

Before the Q&A session began, Berkshire Hathaway also released its Q1 financial report for this year, with some key points as follows:

The company's operating profit for the first quarter was $9.64 billion, down from $11.2 billion in the same period last year, a 14% year-on-year decline, falling short of analyst expectations. The company warned that tariffs could further impact profits. Berkshire's overall profits were also hit by the depreciation of the dollar in the first quarter. The company reported a loss of about $713 million in foreign exchange, while it had gained $597 million from currency fluctuations in the same period last year.

Berkshire has been a net seller of stocks for the tenth consecutive quarter, with a net sale of $1.5 billion in stock assets in the first quarter. The financial report showed that Berkshire's cash reserves reached $347.7 billion this quarter, setting a new historical high. In an environment of high uncertainty due to tariffs, Buffett is cautious about current investments, expecting good investment opportunities in the next five years, stating that Berkshire's pause in repurchasing some stocks is due to a 1% excise tax on stock buybacks imposed by the Biden administration's legislation last year.

Below are the key points from the Q&A session at the Buffett shareholders meeting, arranged in the order of questions:

21:00 Opening Remarks of the 2025 Shareholders Meeting Q&A

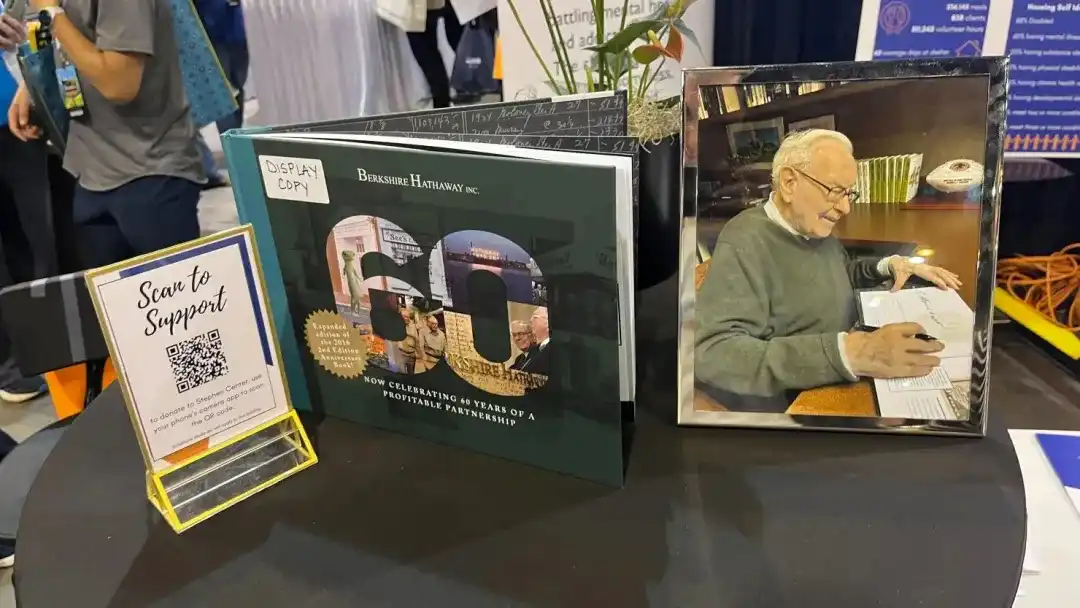

The shareholders meeting has begun. Buffett stated at the opening that this is his sixtieth shareholders meeting. The audience erupted in applause.

Buffett introduced that this year, 19,700 people attended the meeting in person, setting a record for the highest number of attendees. At the meeting, sales of See's Candies reached $317,000. Sales of Brooks running shoes amounted to $310,000, and Jazwares toys and other products sold for $250,000.

Buffett introduced that this meeting features a limited edition book commemorating the 60th anniversary of Berkshire's acquisition. This is the only book sold by the official bookstore, Bookworm, this year. Berkshire printed about 8,000 copies, increasing by about 3,000 from the initial plan, and about 4,000 copies have been sold at the meeting.

21:21 First Question of the Shareholders Meeting: Trade

The first question posed to Buffett was about import certificates, a proposal he made in a 2003 column aimed at reducing the US trade deficit. Buffett stated, "The design of the import certificate is to balance trade. I came up with this idea for the import certificate. It has some gimmicky elements, but I believe it is certainly much better than anything we are discussing now."

Buffett criticized tariffs and trade protectionism, stating that "trade should not be a weapon." He pointed out that the US has transformed from having nothing to becoming an extremely important country. Buffett said, "We should seek to trade with the rest of the world; we should do what we do best, and they should do what they do best. The more trade, the better."

In response to a question about trade barriers, Buffett said, "You can make some very good arguments that balanced trade is beneficial for the world. Undoubtedly, trade and tariffs can be acts of war. I believe it has brought about negative consequences, simply due to the attitudes it has provoked."

Buffett believes that protectionist policies could have negative long-term effects on the US, especially after the US has become a leading industrial nation globally. He said, "In my view, this is a serious mistake. When you make 7.5 billion people feel indifferent towards you, while 300 million are somewhat boasting about their achievements, I don't think that's right, nor do I think it's wise. I truly believe that the more support and prosperity the rest of the world gains, the better it is for us."

We have grown from having nothing 250 years ago to becoming an extremely important country, which is unprecedented in history. Buffett's speech earned applause from the audience. Buffett did not directly mention US President Trump in his remarks.

21:26 Second Question of the Shareholders Meeting: Japan

When asked whether he would stop investing in Japanese stocks if the Bank of Japan raises interest rates in the future, Buffett stated that he would not sell the stocks. Buffett said, "For the next fifty years, we will not sell these stocks. The operating history of these Japanese companies is very excellent," and pointed out that companies like Apple, American Express, and Coca-Cola have performed well in Japan.

Buffett stated that investing in Japan aligns perfectly with Berkshire's investment philosophy. The five Japanese trading companies that Berkshire has invested in have performed very well in the past, and he plans to continue holding shares in these trading companies for fifty to sixty years, hoping to establish a long-term and deep partnership with them. Buffett said that the culture and practices of these trading companies differ from ours, and their management styles vary, but because of this, we value this partnership even more. "We will not sell any stocks. That won't happen even decades later. The investment in Japan is exactly what we want."

Buffett stated that Berkshire currently has no plans to sell the aforementioned Japanese trading company stocks in the short term. Their current operations are very successful, and he believes this even at the age of 94. Berkshire also plans to further expand cooperation. Buffett said that Berkshire's current investment in Japan has reached $20 billion, and I even wish we had invested $100 billion instead of $20 billion.

21:35 Third Question of the Shareholders Meeting: Deployment of Berkshire's Huge Cash Reserves

When asked about Berkshire's current huge cash reserves, Buffett joked that he stopped investing not to make Greg Abel "look good" in the future. Buffett is cautious about current investment opportunities. He stated that he has been looking for investment opportunities, and Berkshire is a "highly opportunistic" company, and he hopes to reduce the cash on hand, possibly down to $50 billion.

Buffett said that Berkshire will find opportunities to deploy the company's record cash reserves, likely within the next five years. "Occasionally, there will be very enticing opportunities. But good opportunities do not come every day. It is unlikely that an excellent deal will appear tomorrow, but it could happen within five years. We have made a lot of money at times because we did not fully invest."

Buffett revealed that Berkshire recently almost invested $10 billion. "For example, not long ago, we almost spent $10 billion, but now we would spend $100 billion. What I mean is that when a project makes sense to us, we understand it, and it has good value, making such a decision is not difficult."

Buffett pointed out that one problem in the investment industry is that things do not progress in an orderly manner.

21:43 Fourth Question of the Shareholders Meeting: Challenges of Investing in Real Estate in a Globally Uncertain Environment

When asked how to cope with the challenges of the real estate industry in the current globally uncertain environment, Buffett said that investing in real estate is more complex and difficult than investing in stocks. Whether it is communication, negotiation, or pricing, there are many people and factors involved, such as who the owner is, the legal structure, funding arrangements, etc. It is really not easy to close a deal in real estate and get a good price; there are too many variables.

If you choose to invest in stocks, there is a huge advantage: you can see countless opportunities every second, especially in the US market. In contrast, real estate transactions are slow-paced and highly dependent on personal communication and negotiation. Real estate investment can be done individually or as a team effort.

On the New York Stock Exchange, billions of dollars are traded daily, with thousands of unknown investors participating in market activities. You only need a suitable price to execute a trade of 20,000 shares of Berkshire in just five seconds. But real estate is not like that. Completing a real estate transaction involves a complicated process and a long timeline. Even if today's transaction scale is large, once it enters the negotiation phase, there are many factors to weigh and coordinate.

Buffett mentioned that Berkshire has also invested in real estate, such as during the financial crisis in 2008 and 2009. He suggested that if one wants to invest in real estate, it must be done in a smarter and more strategic way to compare and choose.

21:49 Fifth Question of the Shareholders Meeting: The Impact of AI on the Insurance Industry

The question about whether artificial intelligence (AI) can change the insurance industry was first answered by Ajit Jain, head of Berkshire's insurance business. Jain stated that a lot of time and money has been invested in AI. AI will be a tool used to change the rules of the industry. AI technology could "truly change" the way the insurance industry currently assesses, prices, and sells risks, as well as the current claims process.

However, Jain pointed out that Berkshire will not be the first to adopt AI in the industry, and Berkshire takes a more cautious approach to any high-profile new technology claims. Jain said, "I certainly think that people will ultimately invest huge amounts of money chasing the next new thing," he said. "We are not good at being the fastest or the first movers. Our approach is more to wait and see until the opportunity materializes, and we have a clearer understanding of the risks of failure and the pros and cons."

However, Jain added that once the right opportunity arises, Berkshire will invest without hesitation. He said, "Currently, some insurance companies are indeed trying AI and trying to find the best way to utilize it, but we have not consciously invested a large amount of money to seize this opportunity. I guess we will be ready, and once the opportunity arises, we will act quickly."

Buffett said he would let Jain decide on Berkshire's insurance business for the next ten years. Whether to use AI will be up to Jain to choose.

21:52 Sixth Question of the Shareholders Meeting: Why Did Berkshire Invest in Hot Dog Company Portillo's?

Someone asked why Berkshire acquired the Chicago hot dog chain Portillo's. Buffett replied that he does not know much about Portillo's. He joked that perhaps someone else invested secretly. Buffett then recounted an anecdote about Jay Pritzker. Jay is a relative of Illinois Governor JB Pritzker, who acquired a chocolate company in Brooklyn decades ago. Buffett stated that Jain is an excellent manager. Abel clarified that Berkshire does not own Portillo's. The company is actually owned by an investment firm with a name similar to Berkshire.

22:00 Seventh Question of the Shareholders Meeting: Is the US Experiencing a Major Change, Should We Be Pessimistic or Optimistic?

The questioner stated that Buffett has always believed in America's long-term advantages, but today America seems to be undergoing unprecedented, almost "revolutionary" changes. As an investor, how should one assess the current situation—should one remain optimistic or pessimistic?

In response to this question, Buffett said the questioner is part of a new generation of investors. In Berkshire's annual manager reports, such macro-level comments are usually not seen. But he can say that America will not experience such drastic "revolutionary" changes. Buffett stated that America was once an agricultural country, and then society changed, and the economy performed very well. It was a male-dominated era, but then fair reforms were made, and the constitution was amended, giving women the same opportunities.

"I have mentioned that we were initially an agricultural society. We were initially a hopeful society, but we did not fulfill our promises well. We have been changing. We will always find various criticisms in this country, but the luckiest day of my life was the day I was born (because) I was born in America."

Buffett said that from the changes from 1920 to now, and from 1776 to now, we have done a lot and taken a long time. I was born in America when almost everything happened there, but now it is different. As a man born in America, I am very lucky—it's not easy, but America has changed.

"We have experienced the Great Depression, world wars, and the development of atomic bombs that I could not have dreamed of when I was born. So even if it seems we have not solved all the problems that have arisen, I will not be discouraged. If I were born today, I would negotiate in the womb until they allowed me to go to America." From 1930 to now, we have experienced many things, such as the Great Depression, two world wars, and the tensions brought by atomic bombs. These are all experiences we have gone through. We are a very lucky country, and I am a very lucky person. I feel that being born in America is much luckier than being born elsewhere.

22:04 Eighth Question of the Shareholders Meeting: Can the Principle of Patience Be Broken in Investing?

Someone asked if there are times in investing when one can show impatience and break the principle of patience. Buffett stated that sometimes you must act quickly. Berkshire has made a lot of money because it is willing to act swiftly. You wouldn't want to be patient on those meaningful deals.

Buffett said, "When a good opportunity arises, you should not show patience at that time. You should have patience to wait for those occasional opportunities. But for those reasonable deals, you should not hesitate. You also should not be patient listening to empty talk that will never materialize."

22:13 Ninth Question of the Shareholders Meeting: Car Insurance Company Geico

Jain said that Geico did face a crisis, but we turned the crisis into an opportunity. When we first took over, there were two main issues: first, our rate structure was unreasonable, and second, we had systemic issues in our actuarial and pricing mechanisms. Five or six years ago, these were areas of concern for us.

Through rapid technological adjustments and process optimizations, these issues have now been resolved. We have not only improved the pricing model but also done a lot of work on risk matching and optimized the overall pricing system. Today's Geico can price everyone based on comprehensive risk levels, and we are doing very well in this regard, which has translated into considerable profits.

Although we have achieved a lot, I do not think the task is complete. We still have many technologies to leverage, such as AI and other new tools. Our goal is not to "catch up with others," but to "do better." Buffett said this is a very interesting case study, especially regarding how a company responds to changes in industry rules. Every business has its own challenges and opportunities.

Berkshire bought Geico for $50 million in the 1970s, at that time only holding a partial stake. Later, Geico brought us huge returns, and now we fully own the company, with profits in a single quarter reaching $2 billion. But this is the result of decades of continuous investment and improvement. A hundred years ago, car insurance hardly existed; but now, besides property and casualty insurance, car insurance has become one of the largest types of insurance. Geico's profits are very substantial, with as much as $29 billion in liquid cash on hand. The $50 million I spent to acquire this company was a very worthwhile investment.

Geico was founded in 1936, originally by a government employee who was a former employee of USAA. It was profitable in its first year, earned more in the second year, and then the company grew and successfully went public. This marked the beginning of the rise of the car insurance industry. No one likes to buy insurance, but everyone loves to drive, which makes car insurance a necessity. Geico's development story is very interesting; it once tripled in a few years, although it later went off track, it ultimately returned to the right path. We almost discuss Geico-related issues at every annual meeting.

Buffett specifically mentioned Geico's CEO Todd Combs. He said Combs has done an excellent job in this transformation. He successfully turned around the situation of this subsidiary. The "telematics" system, which was once seen as a disadvantage, is no longer a competitive disadvantage. Combs also significantly streamlined the company's personnel structure, cutting thousands of positions, which played an important role in improving efficiency.

22:22 Tenth Question of the Shareholders Meeting: Why Do You Think Abel is the Right Successor?

Buffett did not directly answer this question. He stated that it is important to work with excellent talents that one enjoys collaborating with. Buffett provided advice on choosing jobs and starting a career. He said one needs to "do what you love." Buffett reminded that employees' habits can influence colleagues, so it is crucial to choose a workplace carefully.

Buffett suggested that while one should "be cautious" in choosing an employer, there is no need to be overly concerned about starting salary and similar factors. "If you can find excellent colleagues there, then go there." Abel stated that he is honored to be part of Berkshire.

22:31 Eleventh Question of the Shareholders Meeting: Dollar Depreciation and Currency Risk

Someone asked about the weakening dollar and currency risk. In response to how to reduce exposure to the risk of dollar depreciation, Buffett stated that his company will not invest in "worthless" currencies. "We do not want to hold any currency that we believe will depreciate." Buffett also mentioned an increase in holdings of yen. He did not rule out the possibility of exploring and focusing on other currencies in the future.

Buffett also emphasized the complexity of currency games and pointed out that one of the government's responsibilities is to devalue its own currency. Buffett stated, "I will not take any action to manage currency risk based solely on quarterly or annual earnings." In the currency value system, it is very difficult to build an effective system of checks and balances.

Additionally, Buffett stated, "The fiscal policy of the US scares me because the way it is formulated and all the motivations are to do many things that could cause trouble with money. But this is not limited to the US; it is a global issue." "I briefly mentioned in the annual report that fiscal policy is my biggest concern in the US because of the way it is formulated."

He said, "All the motivations are driving some actions that could, and indeed will, cause trouble with currency issues. But this is not limited to the US; many places around the world are like this. In some places, this situation often gets out of control." Buffett said, "We will not really invest in a currency that is about to 'collapse'," adding that when the government takes irresponsible actions, the value of currency can be "frightening."

When talking about the late Vice Chairman Charlie Munger, Buffett said, "Charlie always believed that if he had to choose an investment area outside of stocks, he felt he could make a lot of money in the foreign exchange market." Buffett stated, "We once tried it. I can't say we won't do it again, but the likelihood is low. Unless something happens in the US that makes us willing to hold a large amount of other countries' currencies."

22:41 Twelfth Question of the Shareholders Meeting: Mongolia

The questioner stated that Mongolia is an emerging market located between China and Russia. We have livestock and mining, and the economy is still growing. We held a Mongolia Investors Conference in New York last year, attracting many interested investors. What does Buffett think of emerging markets like Mongolia? Are there any long-term investment plans?

Buffett said, "I remember about twenty years ago, I attended an annual meeting where I started to pay attention to Mongolia and heard some introductions about it, so I have some understanding of the situation in Mongolia—though that was a long time ago. Now we hear some reports from the government and assess which are the truly developable business opportunities. But we won't easily invest overseas unless I believe it is a truly significant opportunity with great potential.

Many people think that to make money, you have to go to places with high inflation, as that can yield a lot of profit, but I don't see it that way. Currently, our company has no short-term investment plans in Mongolia unless it is a project that is very attractive in scale. Perhaps twenty years ago, we would have considered going to take a look. But regarding your economy, such as livestock and mining, I don't know much. That's my current view."

22:45 Thirteenth Question of the Shareholders Meeting: Private Equity Firms Competing in the Insurance Industry

Someone asked about the expansion of private equity firms like Blackstone, Apollo, and KKR in the insurance sector, which are more aggressive. Jain acknowledged that competition from private equity has made Berkshire's investments in the insurance business more difficult. "There is no doubt that private equity firms have entered this field, and we have lost competitiveness in this area. We participated a lot in this field in the past, but in the last three or four years, I believe we haven't completed a single deal."

However, Jain stated that private equity adopts a model with higher leverage and more aggressive investment strategies. When the economy performs well, private equity firms take on certain risks in leverage and credit risk, especially in the life insurance sector. "As long as the economy is good and credit spreads are low, they will make a lot of money," Jain said. However, there is always the risk that at some point, regulators may become dissatisfied and say that you are taking on too much risk on behalf of policyholders, which could ultimately end in tragedy. "We do not like the risk-return ratio in these scenarios, so we choose to raise the white flag and decide not to compete with private equity firms in the life insurance sector."

Buffett stated that many companies want to imitate Berkshire's model, but their CEOs do not invest all their assets in the company like we do. Buffett added that the difference between Berkshire and its competitors is that he personally takes on greater responsibility for investments. He said, "Their sense of fiduciary responsibility for what they do may be somewhat different; sometimes it works, and sometimes it doesn't. When it doesn't work, they turn to other things. But if what we do at Berkshire doesn't work, I will regret everything I created for the rest of my life, so this is a completely different personal relationship. In the property and casualty insurance sector, no company can truly replicate Berkshire's model."

22:50 Fourteenth Question of the Shareholders Meeting: Young People Investing

The questioner was a young girl. She said she just started learning about investing and wanted to hear Buffett's thoughts on the lessons he learned in the early stages of investing. Buffett said, "That's a very good question. I really wish someone had given me such advice when I was young."

This matter is closely related to the people around you. Don't expect every decision you make to be correct. If you have a direction in life, then you should work hard to make those you respect and aspire to be your friends. I just mentioned a few people I worked with in the past; perhaps what they did was not on the same scale as mine, but they are people I really like, and being with them means a lot to me. Walking the path of life with like-minded people is very valuable. Unfortunately, these truths are often only truly understood later in life. When you get older, you will realize that these are the truly important things.

Buffett mentioned two former Berkshire directors, Tom Murphy and Walter Scott. He said, "If you have people like Tom Murphy and Walter Scott around you, your life will definitely be better." But that doesn't mean you should follow wealthy people and replicate their lifestyle. I would suggest you get close to those who are truly smart and wise, learn from them, seek their advice, and try things together with them.

If you are looking for a meaningful job and are not in a hurry to make money, then I suggest you, like Charlie Munger, spend time with excellent people. Find opportunities to share in their success; if you can't find them, that's okay, just keep doing what you are doing and keep working hard. Stick with it, and you will eventually find those who live and think as seriously as you do. Buffett recalled that when he first went to Geico, the door was locked, and he didn't know who was behind it. Ten minutes later, he met that person, who later had a significant impact on his life. When you meet such people, remember their help to you and think about how you can repay them in the future. Never forget these benefactors.

Of course, sometimes you may encounter less than ideal situations. But if you are truly lucky to live in a good environment surrounded by great people, then cherish it. You don't need to feel guilty for being lucky. There are 8 billion people in the world, and only over 300 million in the US. If you live here, you are already ahead in this game, and you should make good use of that. If at work, someone asks you to do something you really don't want to do, then don't be with them. Different industries have different standards for choosing people, but if you find a direction that excites you, then work hard to pursue it, especially if it is a career you want to do for a lifetime.

The investment industry is very interesting; many people, after making their first pot of gold, are unwilling to continue. But I personally feel lucky because I saw its long-term appeal from the very beginning. Like Tom Murphy, who lived to 98, he had a knack for seeing potential in others. We have not encountered another person like him who can so keenly identify talent. If you want to become a better person, you should strive to find people like him and work with them.

There are many successful people in the world, but not everyone can make the right choices. The fastest path to success is to find those truly excellent people and walk alongside them. Berkshire's experience has also been very valuable to me. Sandy Gottesman managed our assets for us starting in 1963 until he passed away a few years ago, along with Walter Scott and Abel, who all embody what long-term success looks like. You can learn a lot of truly valuable things from them.

That's the advice I can give you. Some people live long, perhaps because they are surrounded by good people, or maybe because they drink Coke every day (laughs). But I believe that happy and joyful people tend to live longer because they are always doing what they truly love.

22:59 Fifteenth Question of the Shareholders Meeting: Have Recent Market Turmoil Provided Investment Opportunities?

When asked whether the recent market fluctuations have provided opportunities for large investments, Buffett downplayed the recent market volatility, stating that "there's really nothing" (really nothing), it's part of investing. He was indifferent to the stock market fluctuations that have made investors uneasy in recent weeks.

Buffett said, "What has happened in the past 30 days, 45 days, 100 days… really doesn't count for much." Buffett pointed out that in the past 60 years, Berkshire's stock price has dropped 50% less than three times. During this period, there were no fundamental issues with the company.

In the past 60 years, Berkshire Hathaway's stock price has dropped 50% less than three times. He noted that during this period, there were no fundamental issues with the company. Given this, compared to periods like the stock market crash of 1929, Buffett believes that the recent movements in the US stock market are "not a huge move," and "this is not a dramatic bear market, nor a similar situation."

Buffett recalled that on his birthday in 1930, August 30, the Dow was at 240 points, and then it dropped to 41 points. Despite having experienced some "chilling" events, the Dow closed above 41,300 points this Friday.

For those worried about the cyclical ups and downs of their investment portfolios, Buffett advised: they should change their investment philosophy to adapt to the world—rather than expecting the world to adapt to them. Buffett said, "For you, if it matters whether your stock drops 15%, then you need to change your investment philosophy. The world will not adapt to you; you must adapt to the world." He added, "Everyone has emotions. But you must control your emotions when investing."

23:03 Sixteenth Question of the Shareholders Meeting: How to Deal with Life's Setbacks

A shareholder from Shanghai, China, sought advice on how to cope with life's setbacks. Buffett said, "I focus on the good things, not the bad things. Life can often be wonderful—but it can also encounter terrible setbacks."

23:09 Seventeenth Question of the Shareholders Meeting: Autonomous Driving

Someone asked about the lack of widespread adoption of autonomous driving in the US. If it really takes off in the future, how will Geico's insurance business be affected? What are your thoughts on the liability distribution, software issues, and broader changes brought about by autonomous driving?

Jain, who is responsible for the insurance business, answered that from an insurance perspective, autonomous driving will not immediately bring about fundamental changes. Currently, most auto insurance premiums are priced based on the frequency of driver errors, and our policies and claims systems operate according to this risk calculation method.

Jain said that autonomous driving technology may indeed reduce the likelihood of accidents, and Geico shares a similar view with other insurance companies. But once this technology is truly widespread, we will also make corresponding adjustments.

Buffett said this reminds him of something Charlie Munger once told him. When we decided to enter the textile industry, we could not foresee the future transformation of the entire industry.

The world is always changing. Just like in baseball or golf, not every swing will hit a home run, and not every stroke will be a hole-in-one. You have to accept the fact that you will make mistakes.

Today we discuss whether auto insurance will be changed; this is a very important question. But for now, autonomous driving has not yet fully commercialized, and the US has not yet pushed for large-scale adoption. No one can accurately predict what the insurance industry will look like in the next hundred years.

However, one thing is clear: the world is dynamically changing. People love to drive, and we do not want to destroy this world. We have learned how to better protect the Earth, even though it has been a difficult journey. We know that there are eight countries that have a significant impact on the development of all humanity, and we hope these countries can have the best leaders.

Einstein published the theory of relativity in 1905, which also promoted research into the conversion of energy into powerful forces, ultimately leading us to face the threats posed by nuclear weapons. I witnessed these consequences after being born in 1930. Even Einstein could not have predicted how these inventions would ultimately change the world.

We have also seen the development of North Korea. No one can truly predict what they will do next. These uncertainties will not disappear quickly.

Even so, change has brought many benefits, making our lives today much better than 100 years ago. But we still have to face real issues like weapons of mass destruction.

Just like today's auto insurance, we see that technology is developing rapidly, but for me, this change is not as impactful as the upheaval in the textile industry back in the day. We are currently in one of the "luckiest" phases in human history; you should enjoy life while also paying attention to the changes happening in the insurance industry.

We are doing well in the insurance sector. Although there are many structural issues, we cannot control everything completely. If you don't know how to swing, don't play golf.

There are indeed many clauses that need to be clarified regarding product liability and accidents caused by autonomous driving. Once an accident occurs, due to technological upgrades, repair costs will significantly increase. Today's cars are increasingly resembling high-tech products, and these new technology-related issues have not been fully resolved.

For example, when I first went to Geico in 1950, the average annual premium was about $40, depending on which state you lived in. But now, an annual premium of $2,000 is common. However, at the same time, the number of traffic accident fatalities has significantly decreased. If you look at it from a different perspective, driving is actually much safer now than it was before. The future trends of the entire industry are difficult to predict. You must consider research, reality, and various data.

Changes in the energy sector, healthcare, and political environment can also lead to structural adjustments in industries. In the business world, many issues do not have "answers," only "action points." The rules of the game today are completely different from the past, so you need to rethink how to operate your industry every day when you wake up.

Some additional notes on Berkshire's first-quarter financial report:

Our insurance segment's performance declined significantly in the first quarter of this year. Last year was very strong, but this year it is under pressure due to falling prices and rising risks. Some of our achievements are not replicable, and we do not recommend that everyone try to replicate others' models. We do have some advantages. Our investment income has not changed much because we have made few overall mistakes. We expect total investments this year to be around $40 billion; although overall returns will be lower, the negatives are also fewer than in the past.

The railroad business has seen slight growth this year compared to last year, with some issues improving, and it remains a quality asset for Berkshire. The issues in the energy sector have mostly been resolved, and this year's earnings have rebounded. Other businesses need us to continue to put in more effort. We have done a lot of calculations; some are growing, some are declining, but overall it is quite good. Regarding cash flow, please be patient. Munger once told me, "As long as you have patience and are willing to read financial reports every day and listen to politicians' speeches, you will find very excellent opportunities."

We currently still have ample cash, and as long as the businesses we underwrite can generate profits, this cash will come in handy. In the next 50 years or 100 years, we may make significant investments. Of course, difficult years will come, and at that time, these cash reserves will be particularly important. Currently, the retention rate for the life insurance segment is -2.2%. If you are not prepared to deal with the future, you may very well run into trouble. Running a business requires a different mindset to think about problems.

This year, we have not made any acquisitions. If you buy Berkshire stock, you will also receive your rightful share. Buffett stated that one reason Berkshire has paused its stock buyback program this year is that about a year ago, the Inflation Reduction Act was enacted, which imposes a 1% excise tax on stock buybacks. This has a greater negative impact on us than on other companies.

Buffett said, "This indeed makes its (buyback) attractiveness slightly lower than before." He cited Apple as an example, which performed well this year and spent $100 billion on buybacks. The taxes they paid for these buybacks are also substantial. They bought back at prices even higher than your purchase price—this is good news.

Nowadays, people are looking for ways to increase their chances of success, but I want to emphasize: you must read carefully. Without in-depth reading, you cannot make informed decisions. If significant changes occur in the future, our company will still adhere to a conservative and prudent participation strategy. Although we have made some buybacks, the tax burden cannot be underestimated.

0:05 Opening Remarks for the Second Half and the 18th Question of the Shareholders Meeting: What Have You Learned from Munger and Others

Before starting the second half of the Q&A, Buffett recommended a documentary about the late Washington Post publisher Katharine Graham: "Becoming Katharine Graham." Buffett appears in this film due to his friendship with Graham and his role on the board of the Washington Post. Jain did not take the stage in the second half; Buffett and Abel continued to answer questions.

A shareholder asked Abel how he hopes people will remember him. He stated that his role as a father and coach is very important to him. Buffett joked that he hopes people remember him for his "old age," eliciting laughter from the audience. Buffett explained why he believes the balance sheet is a good starting point for assessing whether a company is worth investing in.

He said, "I spend more time studying balance sheets than looking at income statements. Wall Street doesn't really pay much attention to balance sheets, but I like to look at a company's balance sheet for eight to ten years before looking at the income statement because some things are harder to hide or manipulate on the balance sheet."

He added, "Of course, neither can give you the whole answer."

0:13 The 19th Question of the Shareholders Meeting: Abel's Capital Allocation After Succeeding Buffett

Someone asked that for the past decade or so, everyone has been focused on Buffett and Charlie Munger's investment strategies. Now that Abel will succeed Buffett as CEO, more capital allocation decisions may be led by him in the future. How does he view this aspect of succession, and what are his thoughts on the future?

Abel first mentioned that Berkshire has a very strong investment culture, which is the result of Mr. Buffett's long-term establishment. All of our colleagues uphold a shared set of values. Capital allocation is the core part of our business philosophy. When making decisions, it is not just a discussion among management; more importantly, we have a clear awareness of risk. These values are the key to our company's success.

We always value Berkshire's reputation, which is our greatest asset. Buffett has reminded everyone that when making any investment decision, the first thing is to look at the income statement and understand the real numbers. Now we have a lot of cash, which is a huge advantage, but it also brings challenges—how to allocate this capital? This is not a simple question but a profound philosophy. We always have the capacity to allocate, but we pursue "better allocation."

We have always emphasized that Berkshire will not rely on others in any environment; we will not rely on bank loans for capital operations. Whether in insurance or non-insurance businesses, we must have sufficient cash flow to ensure that Berkshire can continue to operate.

We will continue to focus on high-quality opportunities across various industries, not limited to the insurance sector. Our goal is that when investing, whether buying 100% of a company or just holding a portion, we must fully understand the company's vision. As Buffett mentioned before: we completed a $10 billion acquisition in the last quarter. Sometimes a full acquisition is appropriate, and sometimes buying only a portion of the equity can also be effective. The key is that whether we hold 1% or 100%, we must understand what this company wants to become in the next 5, 10, or 20 years.

We will continue to uphold this philosophy. This is the core of Berkshire's success over the past 60 years, and we will not change it. Buffett then emphasized that the United States is indeed facing some significant transformation needs. Our electrical grid and highway system have fallen behind the current population and economic growth rates. To drive these changes, the US government must take stronger measures. There are 50 states in the US, each with different ways of thinking. Just like after World War II, we mobilized the entire manufacturing sector to support the war in a very short time, achieving incredible efficiency. But in peacetime, achieving the same efficiency is not easy.

Investment depends on the context; we have knowledge and capital, but we also need to make strategic shifts. How to leverage Berkshire's role requires solutions that are meaningful both to the country and to the people and the company. Abel may next present his views on these issues. But one thing is clear: we need to be prepared with ample cash reserves to intervene at critical moments.

In the past, we have done many collaborative projects. For example, the US highway system was completed with the federal government's push. It would not have been possible relying solely on one company. Future large projects will also require close cooperation between the government and the private sector. Abel said that from the energy sector's perspective, we indeed have many areas to advance. Currently, electricity demand is growing rapidly, and to meet long-term energy needs, necessary capital investments must be made. We have strong capabilities in this area and are actively addressing related risks.

Only by addressing these risks can we deploy the capacity to meet future demands. And we must start preparing now. Buffett agreed and added that we must leverage the power of the US federal government. Just like building the highway system during World War II, it would not have been possible to complete it quickly without national coordination.

We do have capital and sufficient knowledge, which enables us to participate. But merely having the desire to cooperate is not enough; we also need the ability to "concentrate efforts to accomplish great things." We were able to do this during World War II, but in peacetime, promoting similar national construction is very difficult. This task may ultimately fall to the next generation.

0:26 The 20th Question of the Shareholders Meeting: A 14-Year-Old Girl Aspires to Join Berkshire, How to Strive

A 14-year-old girl from Hong Kong expressed her desire to join Berkshire in the future and asked what she could do. Abel said that hard work and a willingness to contribute will take you further. "We sincerely look forward to the day you become a part of Berkshire." Buffett added, "Stay curious and read more."

0:29 The 21st Question of the Shareholders Meeting: Wildfire Impact on Utilities, What Strategies for Protection

When discussing wildfire risks, Abel said, "It won't go away. The company has decided that when a fire occurs, sometimes it is necessary to cut off power to the equipment. This is not just a matter of turning off the lights." Wildfires are occurring in California and Texas. Where to invest is the first viewpoint. When discussing the responsibilities of Berkshire's utility company during wildfire spread, Abel said, "We cannot just be the last insurer. We cannot be responsible for everything that happens."

Buffett assured shareholders that Berkshire will not use their money on things the company considers "foolish." He added that if they really did so, shareholders "should kick us out." "Doing foolish things with other people's money is easier than doing it with your own. This is one of the common problems in government. We do not want to bring this phenomenon to private enterprises," Buffett joked.

0:43 The 22nd Question of the Shareholders Meeting: A Female Fan Hopes Buffett Will Arrange a Meeting in the Office

A question came from a Polish woman who said that 74 years ago, in January 1951, Buffett took an eight-hour train ride to Washington just to learn about insurance, and he has consistently pursued this path ever since. This is a very touching experience. In 2011, she was only 15 years old, but she set a goal for herself: one day, she would meet you. Today, she has finally fulfilled that promise and would like to request a small wish from Buffett: could she have some time to spend an hour in your office?

Buffett thanked her for her question and smiled, saying, "You don't need to announce my life anecdotes, but I really appreciate your persistence and effort. There are 40,000 people here today, and your question is indeed very special." Buffett said that when he was young, he often drove across the country to visit various companies. At that time, these companies usually did not have investor relations departments, so many times the CEO personally received him. He was also worried that they might not pay attention to him, but he would prepare two very specific questions in advance.

This approach is not a bad idea. If you want to visit someone and chat for ten minutes, you need to think carefully about what you want to say and what you want to ask. You set the conditions for those ten minutes, rather than letting the other party set them. You will find that most companies now have investor relations departments, and their job is to tell you why you should buy their stock. This is an increasingly large business. But you can completely learn and understand this world in your own way. Berkshire also has our own way; we do not simply copy others.

Now we have enough information and talent, so we do not need to conduct interviews one by one as we did in the past. With over 40,000 people here today, we really cannot accommodate everyone's request for an hour. But I truly appreciate your enthusiasm and persistence; I can only say this to you.

0:50 The 23rd Question of the Shareholders Meeting: Acquisition of Berkshire's Remaining Energy Assets

Regarding Berkshire's decision to acquire its remaining energy assets, Buffett expressed a lack of optimism about the utility industry, stating, "The utility business is not as good as it was a few years ago." He attributed this to social factors, saying that value can change and is not always upward.

Buffett discussed investment opportunities in the American energy sector and the role Berkshire can play. "The solution to this problem is to achieve some form of cooperation between the government and private enterprises, just like during wartime. I don't think the government sent people to lay a lot of concrete or do similar things when building the highway system." He added, "We do have capital, and we also possess knowledge that is rare in some places."

0:54 The 24th Question of the Shareholders Meeting: Berkshire's Future Earnings

Someone asked Buffett about the company's earnings forecast for the recent fiscal year. Will future earnings increase or possibly decline? Buffett said, "I think our utility income will be somewhat affected; earnings are not necessarily determined solely by mergers and acquisitions, but it is undeniable that we will indeed engage in mergers and acquisitions from time to time. This year, we invested $10 billion."

Such questions often depend on market conditions and people's sentiments. Some people are more pessimistic. As someone born in the 1930s, I have experienced very difficult times. Sometimes you feel that certain opportunities are particularly attractive, but you do not take action and miss out. This has happened many times in my life.

Many times, I choose not to try things that I feel uncertain about—like if you asked me to walk a tightrope, I wouldn't do it. But in the financial markets, there are some things that others might fear, but I do not. If one day Berkshire's stock price drops by half, it would actually be an opportunity for me. I know many people's reactions are different from mine, but I won't worry. It's not that I don't have emotions, but the fluctuations in stock prices do not sway my rational judgment. They do not affect my assessment of value.

Overall, Berkshire's profitability will continue to grow over time. What we need to do is retain the money we earn and then make rational decisions. Everyone's abilities and risk tolerance are different, and it is these differences that create opportunities in the investment market.

0:59 The 25th Question of the Shareholders Meeting: Stocks of Tech Giants

Tech giants are currently making significant capital expenditures, investing in AI. Buffett stated that tech giants have made a lot of money and have also made many investments. For example, Coca-Cola has its own bottling company, and these investments are not very large. The initial investments for companies, such as machinery, are significant, but later on, they decrease. Buffett said it will be very interesting to observe the future capital intensity of the Magnificent Seven tech giants. "Many people in America have become very wealthy by paying attention to how others invest."

1:09 The 26th Question of the Shareholders Meeting: High School Courses or Activities That Help with Future Investing

Buffett said that future school teachers can learn a lot on the job.

1:17 The 27th Question of the Shareholders Meeting: Is DOGE Good or Bad for the Long Term in the U.S.?

When asked about the Department of Government Efficiency (DOGE), Buffett laughed and said, "Why ask me such a difficult question?" For me, the government bureaucracy has always been a confusing matter. In a capitalist market, many bureaucratic structures can "infect" other areas, meaning their inefficiencies can spread. In fact, many systems have better management methods, and even within Berkshire, there is room for streamlining and improving efficiency.

But the government is the government. It does not have a real "superior" overseeing it, which makes one uneasy about future governance and fiscal conditions. Especially when elected officials say one thing and do another, it really raises concerns. I have always believed that if a politician has money but no credibility, that is a very negative signal for me. In terms of fiscal policy, the U.S. has not truly addressed the issue of fiscal deficits for a long time; this has never been a thoroughly resolved topic.

As for the United States, "our current fiscal deficit situation is difficult to sustain for a long time. We do not know whether this will last for two years or twenty years, because no country has ever been like the United States; this situation cannot continue indefinitely."

Sometimes you know that something cannot last, but you do not know how to stop it—eventually, you can only throw up your hands in surrender. It was (former Federal Reserve Chairman) Paul Volcker who helped the U.S. avoid the worst inflation collapse. And now, the inflation problem in the U.S. is quite serious, and we have also experienced the consequences of such policies.

Buffett did not directly address DOGE, but he admitted that reducing the budget deficit is a daunting but important task. To be honest, I would not want to be responsible for fixing the fiscal system and balancing the budget—"that is not the job I want to do, but it is a job that should be done." It just seems that Congress is not addressing this issue right now.

We are a great country with the most innovative talent in the world, but we also have many structural problems. If something goes wrong, these problems will not explode immediately, but they will definitely ferment slowly. Governance certainly has incentives and checks and balances. Just like in a company, even the most successful companies cannot be without problems.

Buffett again mentioned the risk of dollar depreciation, stating, "However, the root of all this lies in having a currency that does not depreciate. If all those who trust the government are deceived, and all those who find ways to profit become wealthy or wealthier, what impact will depreciation have on social stability? I think you would not want a society that operates in this way."

1:23 The 28th Question of the Shareholders Meeting: If You Could Travel Back to 1776, How Would You Establish the Foundations of Capitalism in America and Support Its Long-Term Prosperity?

Buffett stated, "When people are most pessimistic, we will make the best deals." He indicated that Berkshire will continue to enhance its profitability, but this growth will not be linear. Buffett defended Berkshire's long-standing decision not to use other people's capital for transactions.

Buffett described America as a shining example of capitalism and compared this system to a cathedral with a casino attached. He said, "American capitalism has achieved unprecedented success. It is a magnificent cathedral that has created an economic system never seen before in the world, while also having a huge casino next to it. The temptation is very great, especially now, the temptation is to walk into that casino."

"In that cathedral, people are essentially designing a system to produce goods and services for over 300 million people, a scale unprecedented in history." While it is indeed very tempting to invest all time and energy into this metaphorical casino, Buffett reminded that maintaining balance is crucial. "In the casino, everyone is having a great time, money is flowing frequently, but you must also ensure that the cathedral is supported. In the next 100 years, America must ensure that this cathedral is not consumed by the casino."

He added, "We have established an interesting system, but it has indeed worked. Capitalism seems very arbitrary and capricious in terms of distributing returns."

1:31 The 29th Question of the Shareholders Meeting: Berkshire's Non-Intervention Management Model for Subsidiaries

Berkshire adopts a "non-intervention" management approach for its subsidiaries. Someone asked if he could elaborate on how it operates. Abel stated that since 2018, he has begun to understand Berkshire's various businesses more deeply. Buffett's knowledge is very admirable, and he is very willing to share: he points out potential risks in business models, and when we encounter problems, we communicate with him in a timely manner.

I communicate with him more on framework issues, such as how to view industry trends and whether a certain strategy is reasonable. But in daily operations, we have a lot of autonomy to make independent decisions and advance projects.

If an opportunity suddenly arises in an industry, or if we plan to pursue a new direction, we will discuss with Buffett whether it is worth pursuing. But at the execution level, we have a high degree of freedom. The managers selected by Berkshire are very familiar with the operations of their respective industries, such as the leaders of Geico. Especially in the past few years of transformation in the insurance sector, a visionary leader is crucial. We benefit from past experiences.

Buffett smiled and said that he has worked with Abel for many years. Abel is very serious about his work, and sometimes Buffett wishes he could be a bit more relaxed like an artist and not work so hard. But to be honest, if a business is doing well, then you don't have to worry about being fired.

Abel is doing an excellent job. Not everyone is suited to be a manager. Some people want someone to tell them what to do; others will quit the moment you give them orders, and I won't blame them. But Abel is different; he has autonomy and is willing to accept suggestions or assistance from others. He is a true leader.

At Berkshire, we do not require every manager to operate in the same way. Some people are very admirable, while others may not be. But the quality of management in an organization can be seen—if the atmosphere in the organization begins to decline, it indicates that the leadership may also need to make improvements.

For example, in one of our retail stores, an employee once told a friend, "Come buy something, and I'll give you a discount." Although they meant well, it violated the company's employee discount rules. Such behavior can be "contagious." We do not want to see upper management leading by changing the rules for personal gain. Once this happens, the entire organization may head in the wrong direction.

1:38 The 30th Question of the Shareholders Meeting: Berkshire's View on Environmental Changes

Abel said that Berkshire considers this issue when supporting and acquiring energy companies, and it must take into account the requirements of the federal and state governments. Abel provided an example of the changes in Iowa's electricity structure in the early 21st century. He mentioned that there was a power shortage in Iowa at that time, which relied heavily on fossil fuel generation. He had discussions with the governor to determine how to maintain a long-term energy supply. Various types of energy were discussed at that time.

Abel emphasized that with the support of state legislators, Iowa built a large wind power project while phasing out a number of coal-fired units. Berkshire invested $16 billion in the largest wind farm project in the U.S. in Iowa, while also phasing out several coal-fired units. Abel added, "Coal-fired units are still needed to maintain a stable power supply." This statement received applause from the audience.

Abel stated that renewable energy and non-carbon energy must advance in accordance with national requirements. Berkshire made decisions that fully comply with federal and state government requirements, respecting the processes of all states and cooperating with them. "We will continue to work with states to determine the routes they want to plan."

Abel warned, "We cannot have a situation like that in Spain and Portugal." He referred to the recent power outages that swept through Spain and Portugal on the Iberian Peninsula, indicating that Berkshire's energy business still requires coal-fired power plants to continue generating sufficient electricity.

1:44 The 31st Question of the Shareholders Meeting: U.S. Healthcare Reform

A nurse asked why Berkshire terminated its collaboration with JPMorgan and Amazon in the healthcare sector and what its thoughts were on U.S. healthcare reform. Buffett stated that the termination of the collaboration was due to the significant resistance to change they faced.

1:54 The 32nd Question of the Shareholders Meeting: Abel's Future Role

Someone asked whether Abel would fully take over Berkshire in the future, including responsibilities for asset allocation, and whether his focus would be more as an investor or as a corporate operator. Buffett said, "To be honest, being a corporate operator is very difficult, while managing money from a room is relatively easier and more enviable. I have always felt lucky because I have had the opportunity to choose who to work with. I have never been let down by my teachers or partners in my life, which is rare."

"I am also grateful that I have the freedom to choose what I want to do each day; this freedom and flexibility are not available to many professional managers. Honestly, I never thought about becoming a 'top manager' of a company—that is not a role I excel in or enjoy. Now I can run the company in a way that I like, which is a happy thing for me. Abel is an outstanding operator; he excels at handling complex operational matters. The reason I can hand this work over to him is that I believe he will handle it well."

As for asset allocation, that is certainly also part of future work. But I want to emphasize that the real challenge is not just 'investing,' but how to do the right things with Berkshire's resources. Abel will be someone who can combine these two aspects very well.

1:57 Conclusion of the Shareholders Meeting Q&A

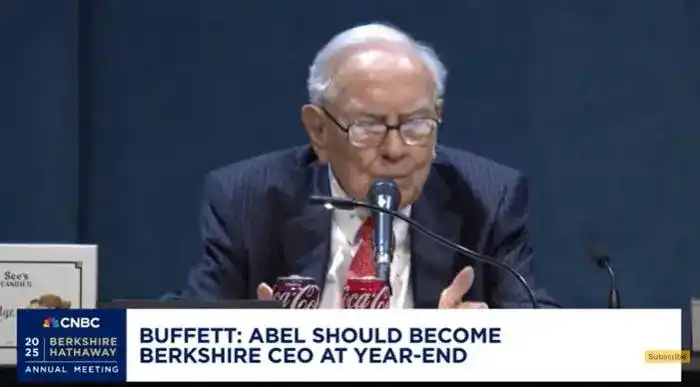

Buffett announced, "Greg (Abel) should become (Berkshire's) CEO by the end of the year." Buffett stated that after stepping down, he would remain at Berkshire and provide assistance, but the "final decision-making power" would be in Abel's hands. Buffett mentioned that Abel was not aware of this. Other members of the board, aside from his children, also did not know.

Buffett stated that he has no intention of selling any shares of Berkshire but will gradually donate his holdings. He said, "I absolutely do not intend to sell any shares of Berkshire Hathaway; I will gradually give them away." This statement elicited rounds of applause and cheers from the audience. Buffett continued, "I want to add that the decision to retain all shares is an economic decision because I believe that under Greg (Abel's) management, Berkshire's prospects will be better than when I was managing it."

He stated that this decision also reflects his confidence in Abel's leadership abilities. Buffett concluded, "But I will join, and perhaps one day we will have the opportunity to invest a large amount of money. By then, I think it will be very helpful for the board—to let them know that I have invested all my money in the company, which I think is wise, and I have already seen Greg's achievements."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。