TL;DR

With the continued prosperity of the cryptocurrency trading market, on-chain transaction processing capacity and scalability have become key areas of technical exploration in the industry. In Ethereum's scalability solutions, the community has gradually chosen a roadmap centered on Layer 2. At that time, Layer 2 projects, pressured by the high costs of Calldata, had to focus on DA scalability to further reduce costs and increase efficiency. Against this backdrop, proposals such as Danksharding and EIP-4844 have emerged, aiming to utilize new storage mechanisms to make Rollup data publishing on the Ethereum mainnet cheaper and more efficient. Meanwhile, a series of AltDA projects such as Celestia, EigenDA, and Avail have begun to emerge, providing alternative block space solutions for the entire industry through independent consensus and data encoding technologies.

Although AltDA projects have shown potential in terms of block space pricing and scalability, the current market demand for massive data on-chain remains insufficient. For many Rollups, paying a portion of DA fees on the Ethereum mainnet (for example, the DA cost for Base is even less than 5%) is not as important as the legitimacy, liquidity, and ecosystem integration that Ethereum provides. Taking Celestia as an example, it currently relies heavily on a single major client, Eclipse, which accounts for about 85% of Blob upload volume, making Celestia's user structure quite singular. Additionally, since Celestia's launch, the total protocol revenue has only been over $100,000, and such profitability is difficult to sustain for the long-term operation of the project, let alone continue to invest significant resources to attract more potential users or accelerate ecosystem building. Other DA projects, under the pressure from EigenDA, have almost become "ghost chains."

By analyzing the true sources of DA demand and the current challenges faced, we find that traditional finance or lightweight applications consume relatively limited block space. Ethereum DA only accounts for a very small portion of their costs, and as Ethereum DA scalability continues and ZK compression efficiency improves, this will further strengthen Ethereum's dominance in the DA field and weaken the demand for AltDA. We also rethought the user profile, believing that data-intensive applications such as AI, gaming, and social media are more likely to trigger explosive demand for DA, truly testing the high throughput and low-cost potential of the blockchain's DA layer. Therefore, DA projects should explore the development of full-chain applications more and the network effects similar to DeFi financial Legos that they bring.

The Development History of DA Usability

History of Ethereum Scalability, Source: GenesiSee

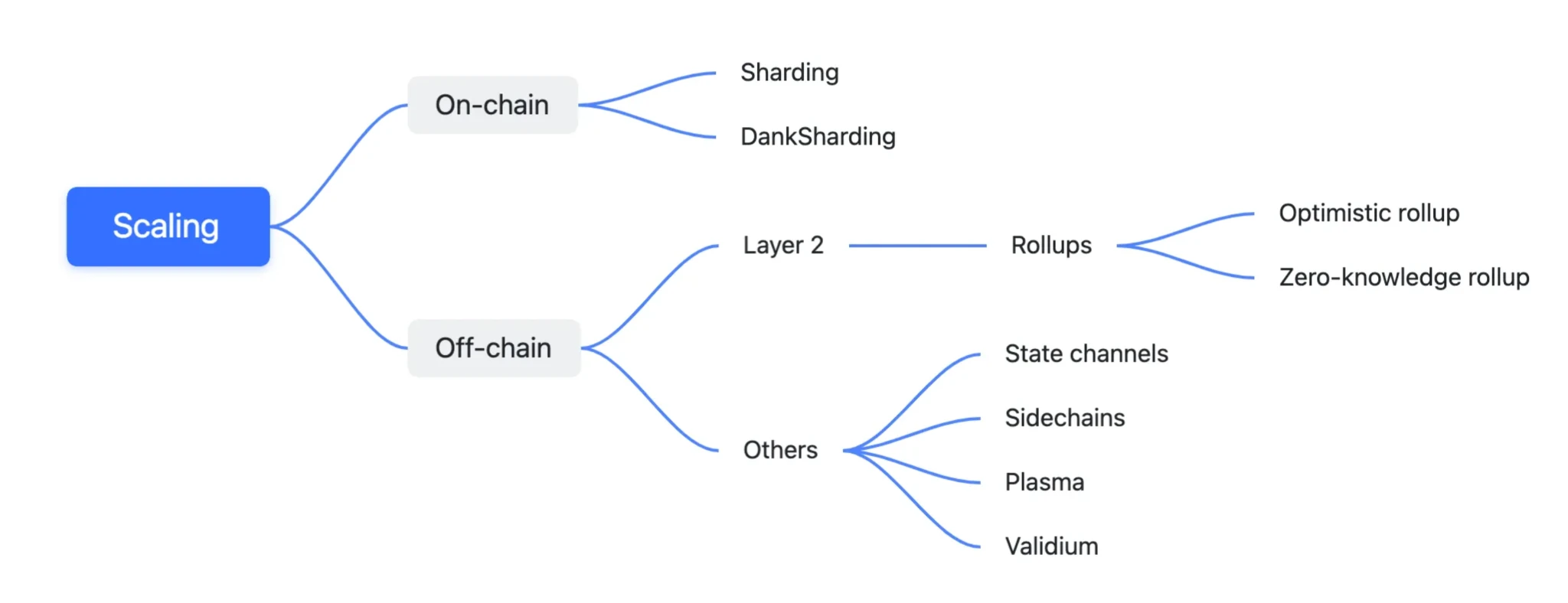

Scalability has always been a timeless topic. Ethereum has gone through the development of various scalability technologies, including state channels, Plasma, ETH2.0 Sharding, Shadow Chain (now Rollup), ZK, OP, etc., ultimately confirming a Layer 2-centric scalability route. ZK Rollup is the main scalability technology for Ethereum, which packages user transactions on Layer 2 and sends them to Calldata, the early data availability storage area. Data availability is not equivalent to data storage; availability lies in its ability to verify whether transactions are valid. However, with the emergence of numerous Layer 2 solutions, the high costs of Ethereum Calldata have gradually become apparent. Calldata is the storage space for parameters that call smart contract functions and is essentially not suitable for large-scale data availability storage.

Therefore, Ethereum researcher Dankrad Feist proposed DankSharding. DankSharding splits Ethereum's architecture into multiple layers, with the data availability layer (DA) being one of them, and stores it on Ethereum in the form of Blobs, while stipulating that it will be deleted from L1 after a certain period to avoid the mainnet state bloat issue, aiming to achieve DAS sampling and a mounting capacity of up to 16MB per slot.

In the early stages, Dankrad Feist introduced Proto-Danksharding to quickly realize an early version of this vision, commonly known as EIP-4844 and the Dencun upgrade. In the EIP-4844 specification, a Blob is 128KB, and a block/slot can mount up to 6 Blobs, with a target of 3; exceeding 3 will adopt a Gas Fee mechanism similar to EIP-1559.

For Layer 2, there are multiple daily operational costs, including execution costs (state updates and cross-chain costs between L1 and L2), DA costs (compressed data, state roots, and ZK proofs), and verification costs (ZK verification). Before the introduction of EIP-4844, L1 costs accounted for 98% of the total costs of Layer 2, primarily due to the excessively high storage costs of Calldata.

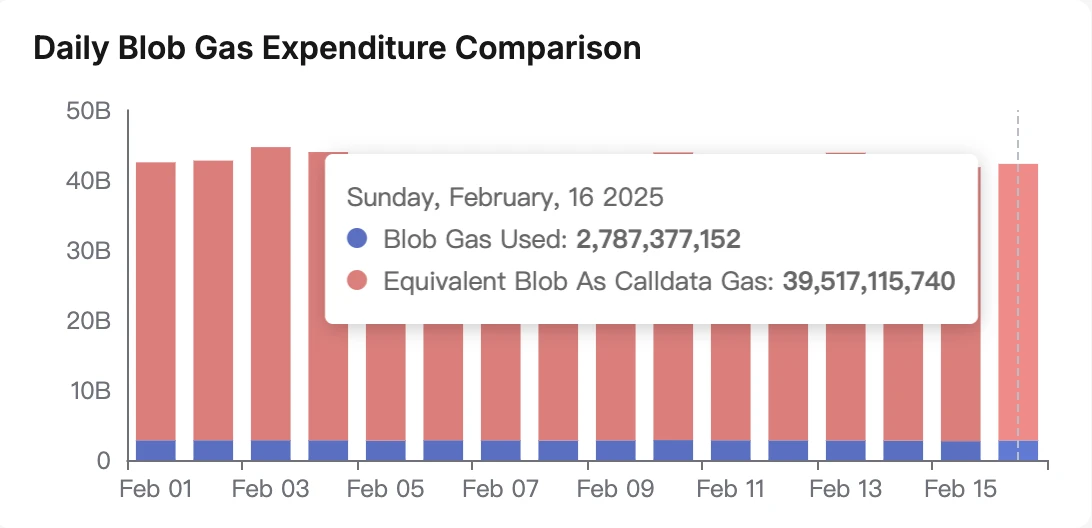

Daily Blob Saving, source: Blobscan

Since the Dencun upgrade, the costs of the DA layer have decreased by 92%. While Ethereum explores the scalability of the DA layer through the Danksharding proposal, Celestia has also launched its own third-party solution, bringing the term "modular" into the public eye. During this period, criticism of Ethereum's roadmap began to emerge, forming the following mainstream viewpoints:

Ethereum has delegated the execution layer to Layer 2, and its vision of a world computer seems to have been strategically abandoned. Instead, it has embarked on the so-called vision of a world settlement layer, which is not accepted by most people. Even when spot ETFs are promoted commercially, ETF institutions do not know how to position Ethereum.

The Layer 2 architecture has inherent issues that need to be addressed, and its overall liquidity is still not as good as that of Monolithic Chains.

Celestia's throughput and performance are thousands of times greater than Ethereum's data availability layer, and the most valuable assets are in data availability, allowing Celestia to capture more data assets.

The modularization of blockchains is a historical trend, with a large number of modular projects emerging, including modular execution, virtual machines, sequencers, data availability, and more.

Ethereum's advantages mainly lie in its legitimacy. For some projects, the cost of legitimacy is difficult to measure and cannot be recognized by the Ethereum community, leading to a reduction in users and a reputation that is often hard to quantify. This is also one of the reasons why many internet communities jokingly refer to it as the "Ethereum cult."

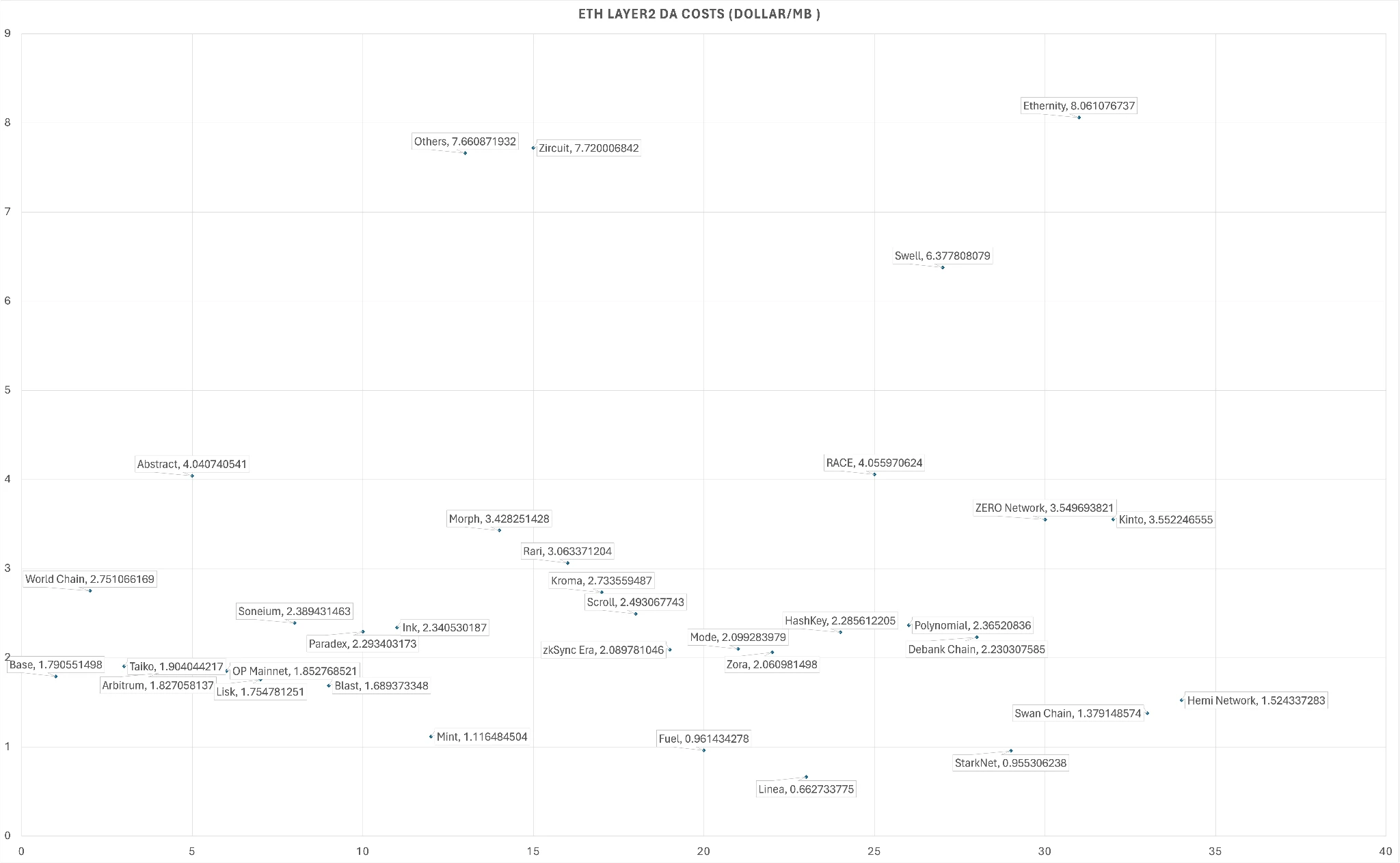

Layer 2 DA Costs (USD/MB)

Since its launch, Celestia has indeed significantly reduced DA costs. As shown in the figure above, after the Dencun upgrade, Ethereum's DA costs per MB generally range from 0.6 to 4.0 USD/MB, with Linea reaching a low of 0.66 USD/MB. We have not yet accounted for the latest Unichain DA costs, while the current usage cost of the OP chain is about 20 USD/MB.

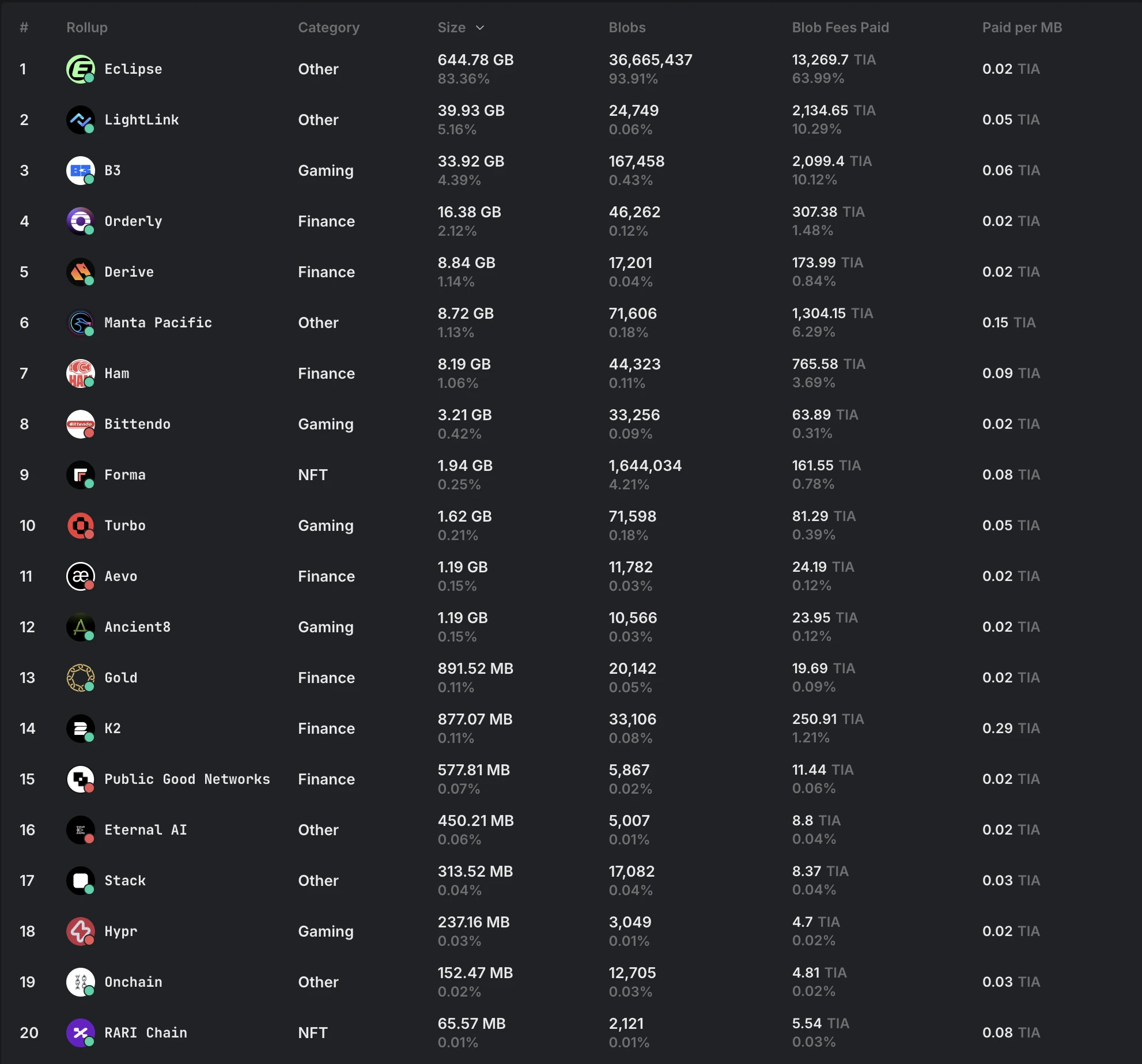

DA Costs using Celestia, source: Celenium.io

In contrast, Celestia's DA costs are about 0.06-0.09 TIA/MB, which is a 60%-90% reduction compared to Ethereum. At the same time, Ethereum's variance is much higher than Celestia's, with the price volatility of its block space being significantly greater than that of Celestia. However, even with such substantial cost savings for clients, Celestia, Avail, and other data availability layers, or the "block selling" business, seem to have made no substantial progress. In Celestia's ecosystem development, Eclipse accounts for about 93.61% of the Blob submission data volume, while other projects like Orderly, Lightlink, and AEVO combined do not even reach a fraction of that. Additionally, the prices of Avail and Celestia have long been in a sluggish state, with rumors that the Celestia project team has been selling tokens at low prices through OTC.

What has happened to the once-promising Celestia? What problems is it facing? What is the current progress? Why is the ecosystem difficult to advance? Why have the former leaders of the modularization wave and Ethereum "killers" gradually faded away? This article aims to explore the true value of the block space business model after shedding the halo of "legitimacy" following two years of market sedimentation and user education.

Analyzing the Technical Development of Mainstream DA Projects

Currently, mainstream DA projects include Celestia, EigenDA, Nuffle (NEAR DA), Avail, as well as newer projects like Bitcoin DA Nubit and AI-oriented 0G (Zero Gravity).

Comparison Chart

The current DA technologies mostly tend to adopt the same core technology—2D Reed-Solomon erasure coding + DAS (Data Availability Sampling), which is also the direction of Ethereum's future upgrades. The 2D Reed-Solomon technology ensures data recoverability during transmission through data redundancy, while DAS achieves high-confidence data availability verification with fewer operations. Next, we will focus on Ethereum EIP-4844, Celestia, EigenDA, Nuffle, and Avail.

Ethereum EIP-4844

EIP-4844 is a "transitional version" before fully implementing sharding, focusing on introducing a new "blob-carrying transaction" that stores large data in the form of Blobs on the consensus layer (Beacon Chain) rather than the execution layer, and deletes it from execution nodes after about two to three weeks, significantly reducing the cost for L2 to write data to L1. Currently, EIP-4844 does not support DAS, but the future goal is to implement DAS. Additionally, it does not set up a dedicated proof mechanism, as Blobs are directly mounted on the mainnet, and the consensus mechanism relies on Ethereum's existing Ghost + Casper mechanism, so the block time still follows Ethereum's mainnet rule of 12 seconds.

Currently, Blobs use the EIP-1559 Gas Fee scheme to control supply and demand, targeting 3 Blobs, with a maximum of 6 Blobs per block, and each Blob being 128KB in size. After the full implementation of Danksharding, the goal is to process 32MB of data per slot and support cross-shard communication while technically implementing 2D Reed-Solomon, DAS, and KZG commitments.

Celestia

Celestia is the first independent L1 that focuses on the idea of "modular blockchain," concentrating on providing data availability and consensus services. It utilizes DAS combined with 2D Reed-Solomon erasure coding and Named Merkle Trees (NMT) to split and encode block data, then verifies it through random sampling by nodes, achieving high-probability verification of data integrity with minimal download volume.

Its consensus mechanism is primarily based on the Tendermint mechanism under the Cosmos architecture, which involves a "proposer" proposing a new block, followed by two rounds of voting (Prevote and Precommit) by all nodes. When 2/3 of the nodes acknowledge the block, it is considered finalized. The block time is about 15 seconds, and the Finality time in Celestia is theoretically also 15 seconds, but in practice, both can reach 6 seconds. Celestia adopts an Optimistic Proof architecture rather than the mainstream KZG, triggering interactive verification only in cases of fraud.

In terms of block size, Celestia's early single block size was 2MB, and after combining 2D Reed-Solomon and DAS technologies, it effectively reduced the operational pressure on nodes, thus supporting the efficient operation of more light nodes.

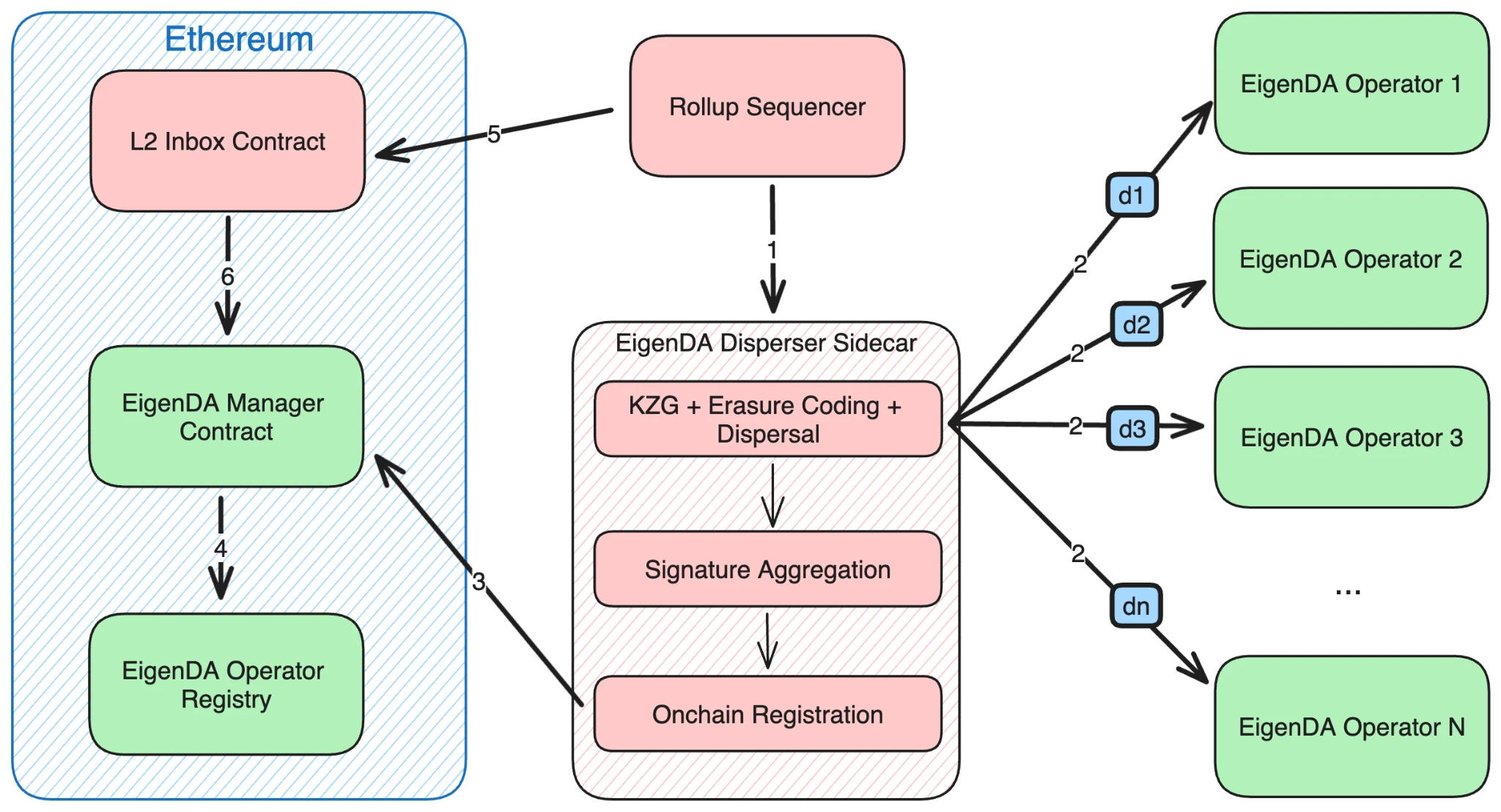

EigenDA

EigenLayer is middleware that provides "restaking" infrastructure on Ethereum, allowing existing ETH validators to choose to join and provide additional services, one of which is EigenDA. EigenDA does not restart a new consensus network but constrains nodes providing data availability services through a Slashing mechanism. If a node fails to provide published data as required, it will have its staked ETH confiscated. Therefore, strictly speaking, EigenDA is more like a collection of multiple DA projects, establishing operational norms for these DA projects, allowing multiple DA projects to run in parallel while using xETH as collateral for restaking.

EigenDA Structure, source: EigenDA

Specifically, unlike the architectures of Celestia and Avail, EigenDA has a role called Operator, which needs to stake xETH on EigenLayer, effectively locking up collateral. Each Operator stores a portion of the Blob, but when combined, they can form complete data, similar to data sharding. If an Operator commits fraud, they will face economic slashing penalties.

The role that interacts directly with the Rollup on the C side is the Disperser, acting as an intermediary for the Operator. The Disperser splits the Rollup's Blob into multiple chunks, performs Reed-Solomon encoding (constructing redundant information for data recovery in case of transmission loss). Subsequently, the Disperser verifies these chunks through KZG commitments to ensure they come from a specific Blob and sends the chunks and corresponding proofs to the Operators while collecting their signatures. After collecting enough (threshold-satisfying) signatures, the Disperser submits this "signature aggregation" to the Ethereum mainnet contract to punish dishonest Operators when necessary.

The Retriever is responsible for retrieving chunk data and assembling it into a complete Blob. EigenLabs provides an official Retriever, but each Rollup project can also deploy its own.

EigenDA is not a blockchain because it does not have an independent consensus mechanism; Operators rely on EigenLayer for staking, thus implementing a mechanism for reducing malicious behavior.

Throughout the process, Ethereum's role is to collect necessary information such as KZG commitments and signatures through on-chain contracts. Security claims originate from the Ethereum mainnet, but in reality, they depend on the middleware Disperser, commonly referred to as DAC. The consensus mechanism relies on the Ethereum mainnet, and the final transaction determinism aligns with the Ethereum mainnet's timing, approximately 2-3 epochs. It is important to note that the block time is not the Ethereum 12 seconds per slot, as EigenDA can aggregate N Blobs and submit them to a single slot at once. In terms of block size, the official claim states that throughput can reach 15MB/s.

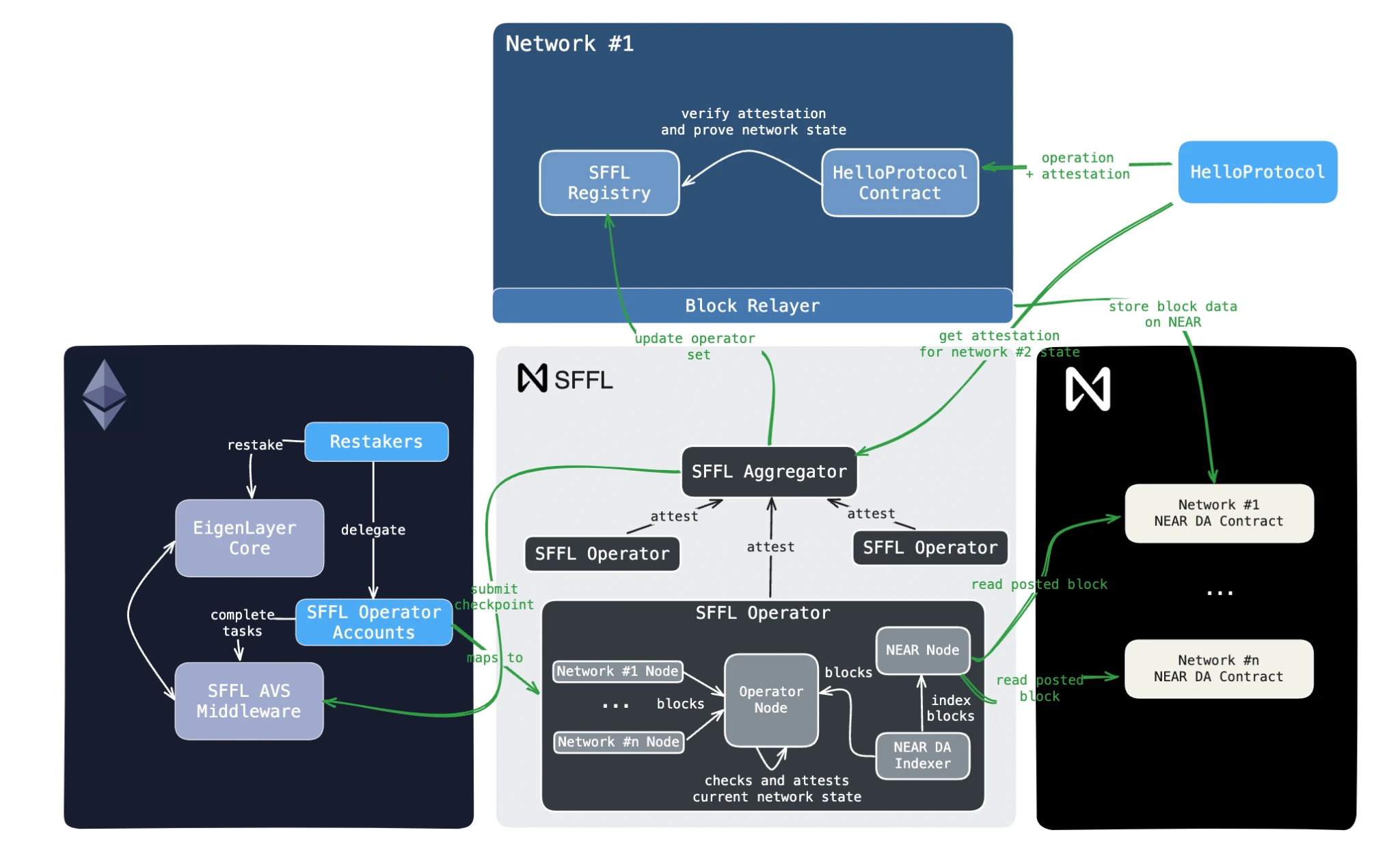

Nuffle

Nuffle is a project spun off from NEAR DA, one of the chain abstraction components incubated by the Near Foundation. Currently, the project has completed independent financing, raising $13 million in a seed round led by Electric Capital. Although NEAR DA has not fully disclosed its specific design plan, limited information from the official website indicates:

Nuffle's DA layer may adopt an architecture similar to NEAR's execution sharding technology, Nightshade. Nuffle applies Nightshade technology to data storage while implementing state pruning, with complete data storage lasting at least three days. The specific implementation plan is still under construction, but official documentation reveals that it may use a 2D Reed-Solomon + KZG scheme, but will not use DAS. The reason is that while DAS can achieve 99% reliability probabilistically with a small number of verifications, there is still a possibility of malicious behavior (0G also abandoned the DAS scheme last year).

Nuffle DA + NFFL Structure, source: Nuffle

Notably, Nuffle also introduces a new protocol called NFFL (Nuffle Fast Finality Layer, formerly known as SFFL). This protocol relies on EigenLayer to provide cryptographic security and includes two off-chain roles, Operator and Aggregator, with the following workflow:

Rollup publishes its block data to Nuffle DA.

Operator retrieves data from Nuffle DA and verifies its consistency with the original data from Rollup.

Upon successful verification, the Operator signs the state root and submits it to the Aggregator.

The Aggregator generates a unified proof and submits it to the NFFL contract on Ethereum.

Upon successful verification, the state proof is synchronized back to each Rollup network for rapid settlement.

At the same time, NFFL is middleware registered on EigenLayer, with Operators responsible for signing the validity of Blob data, and these Operators also run AVS nodes, thus facing the threat of slashing under the POS mechanism. The complexity of Nuffle's architecture is designed to leverage NEAR's Nightshade technology, which can provide extremely high Blob throughput, while introducing NFFL as a means of rapid settlement, allowing Rollup to primarily rely on the security of EigenLayer's xETH restaking, thereby enhancing throughput at the DA layer. Since final settlement occurs on Ethereum, its Finality time remains around 15 minutes.

Avail

Avail was initially incubated internally by Polygon as one of its scalability solutions and later spun off from Polygon. Avail adopts the BABE and GRANDPA consensus mechanisms inherited from the Polkadot SDK (Substrate). Similar to Celestia, Avail also uses 2D Reed-Solomon encoding + KZG commitments + DAS to ensure that data is not intentionally hidden or tampered with.

BABE is the validator election rule of Polkadot, similar to a lottery draw. For example, a random number is generated for each slot, and each node holds a fixed number. If a node's number is less than the random number, it can participate in the block production for that slot. Each slot is fixed, set to 6 seconds for Polkadot, while Avail has chosen 20 seconds. The problem is that often multiple nodes meet the criteria simultaneously, leading to multiple forked chains. GRANDPA is used to determine which forked chain becomes the final chain; it is essentially a voting mechanism where multiple validators participate in Byzantine voting. As long as 2/3 of the validators acknowledge a certain forked chain, that chain is considered the final chain. The main issue is that it usually requires multiple rounds of voting, so each 20-second slot may need several slots to ultimately confirm the validity of a transaction.

Currently, Avail's block size is 2MB, block production time is 20 seconds, and final confirmation time is 40 seconds, meaning an additional slot is consumed for validator voting beyond the original slot.

Comparison Chart

The above is a summary chart based on five DA projects and the future DA expansion goals of Ethereum. EigenDA, relying entirely on the staking security of EigenLayer and shifting away from public chain architecture to AVS, has achieved higher throughput. Nuffle adopts a dual security architecture relying on both Ethereum and its own DA, and is also one of the Eigenlayer AVS ecosystems on the Ethereum side, combined with NEAR's Nightshade sharding expansion plan, resulting in relatively outstanding performance.

In the future, the goal of Danksharding is to expand Blobs to 16-32MB, achieving a 20-40 times increase in capacity. In terms of the tech stack, most projects plan to use KZG and DAS, but some projects are gradually abandoning the DAS scheme, believing it may lead to longer settlement times. Meanwhile, projects like Ethereum prefer to verify block validity through DAS technology to introduce more light nodes, thus achieving a certain degree of node decentralization. This reflects different value propositions.

Returning to the Source of Value: The Costs, Ecosystem, and Business Model of AltDA

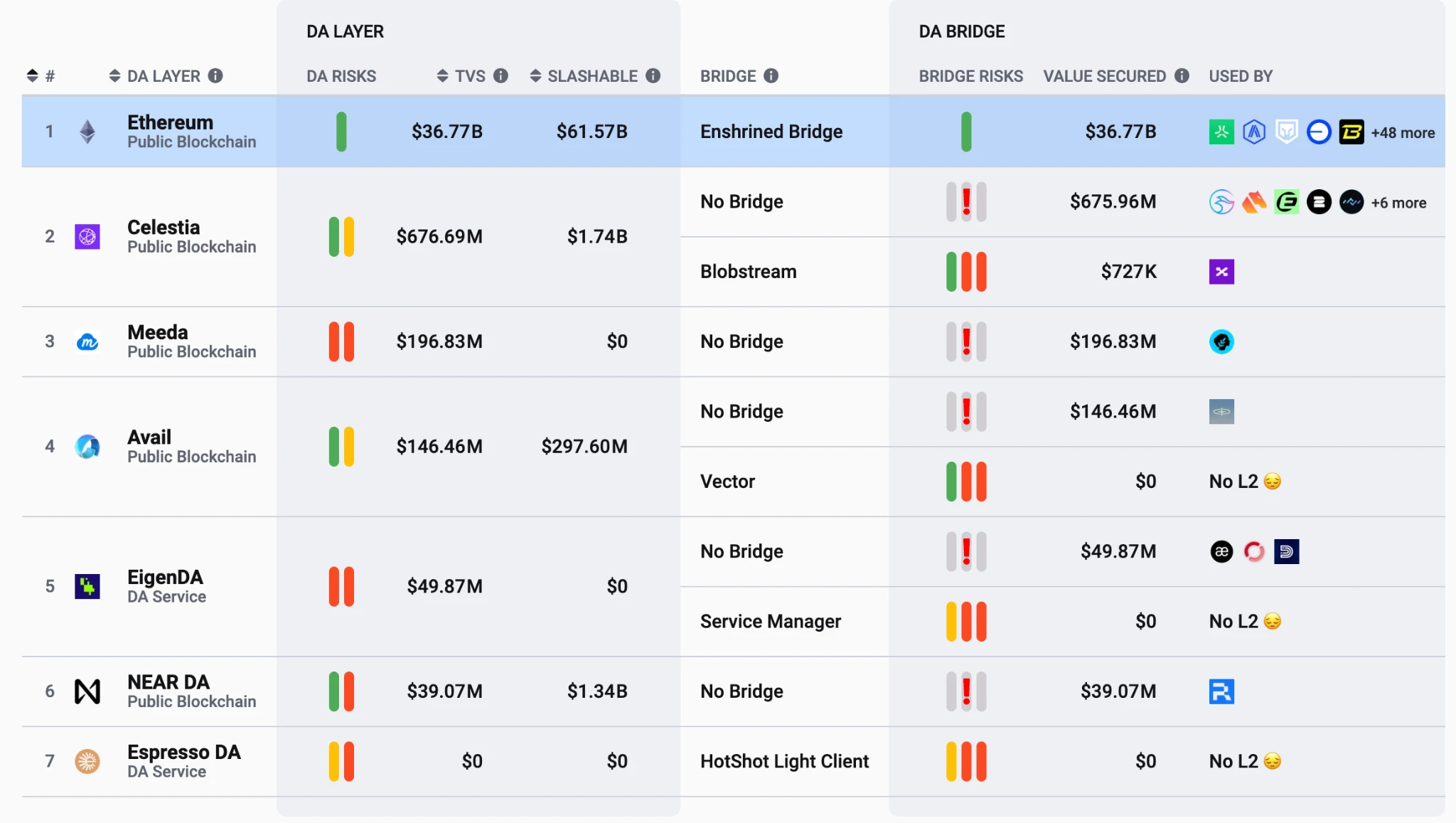

Data Availability Ecosystems, source: L2beat

The main business model of AltDA is to sell block space, primarily focusing on a B2B model, making it crucial to persuade large clients to adopt the AltDA solution. Currently, the AltDA ecosystem is illustrated above; aside from Eclipse, which occupies 96% of the Blob share in the early Celestia ecosystem, the other projects have not achieved significant development.

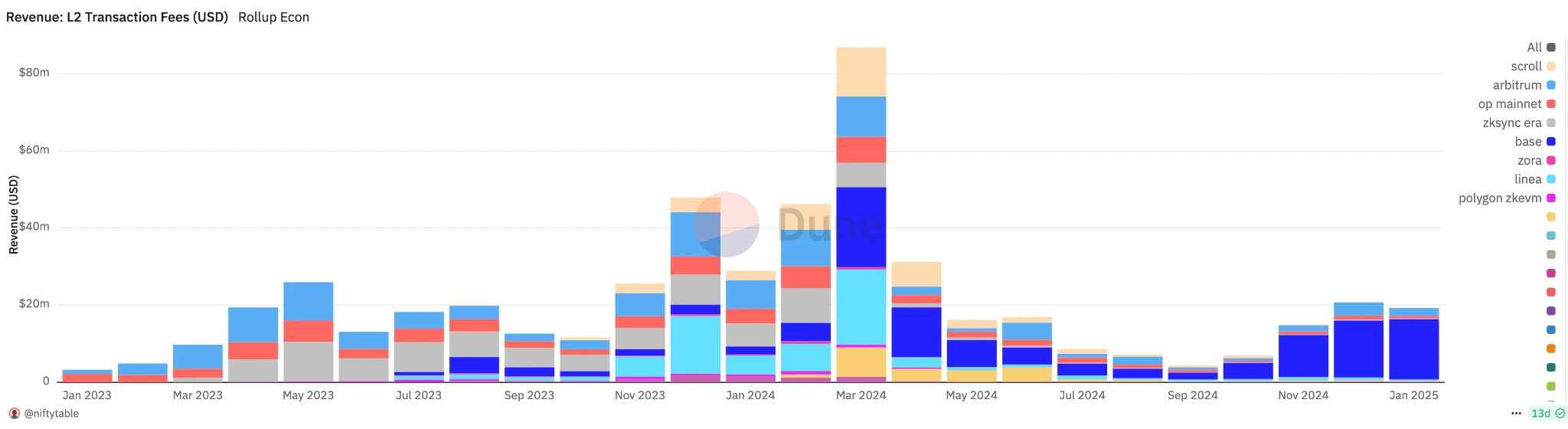

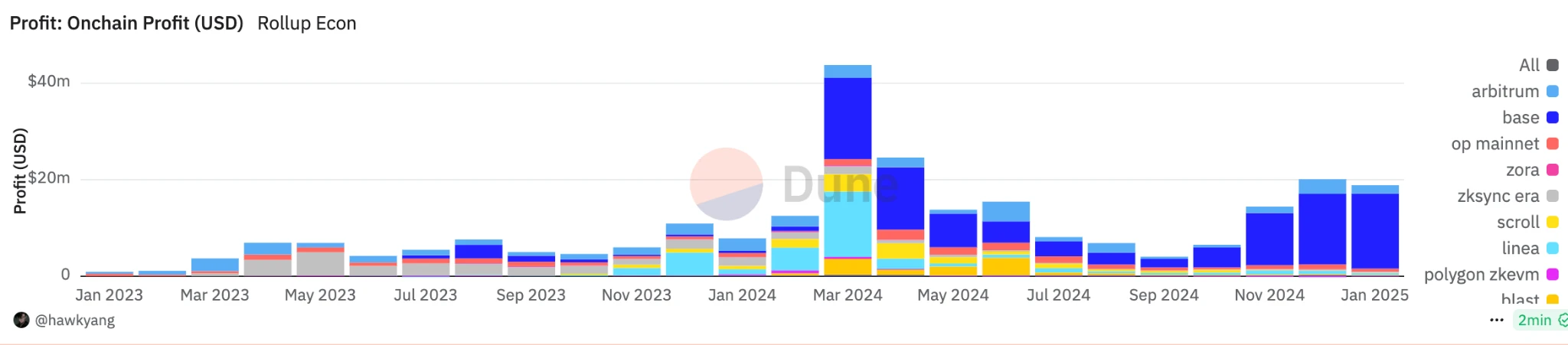

Layer2 Revenue in USD

Layer2 Profit in USD

Currently, the entire industry, whether Rollup or public chain, is far from the point of discussing profits and revenues. The current profits of Layer2 (not accounting for costs such as teams, sequencers, network development, etc.) mainly come from the fees obtained by the Sequencer, minus the Blob and execution costs on Layer1. Currently, the Base chain occupies most of the market share, with total revenue of $16.6 million in January and a profit of $15.54 million, while the actual Layer1 cost is only about $1.06 million; Arbitrum had a cost of $238,700 in January and a profit of $1.77 million. Since the Dencun upgrade, the cost of Blobs on the Ethereum mainnet has become negligible compared to the real-world costs of teams, marketing, and development.

This is also why, even if AltDA reduces DA costs by 60%-90%, most project parties are still unwilling to migrate to AltDA, as the absolute value of cost reduction is far less than the benefits brought by legitimacy and liquidity on Ethereum. At the same time, Eclipse is also considering migrating from Celestia to EigenDA after its launch. We believe the main consideration is that EigenDA has a closer relationship with Ethereum's interests, stronger legitimacy, and currently optimal expansion effects.

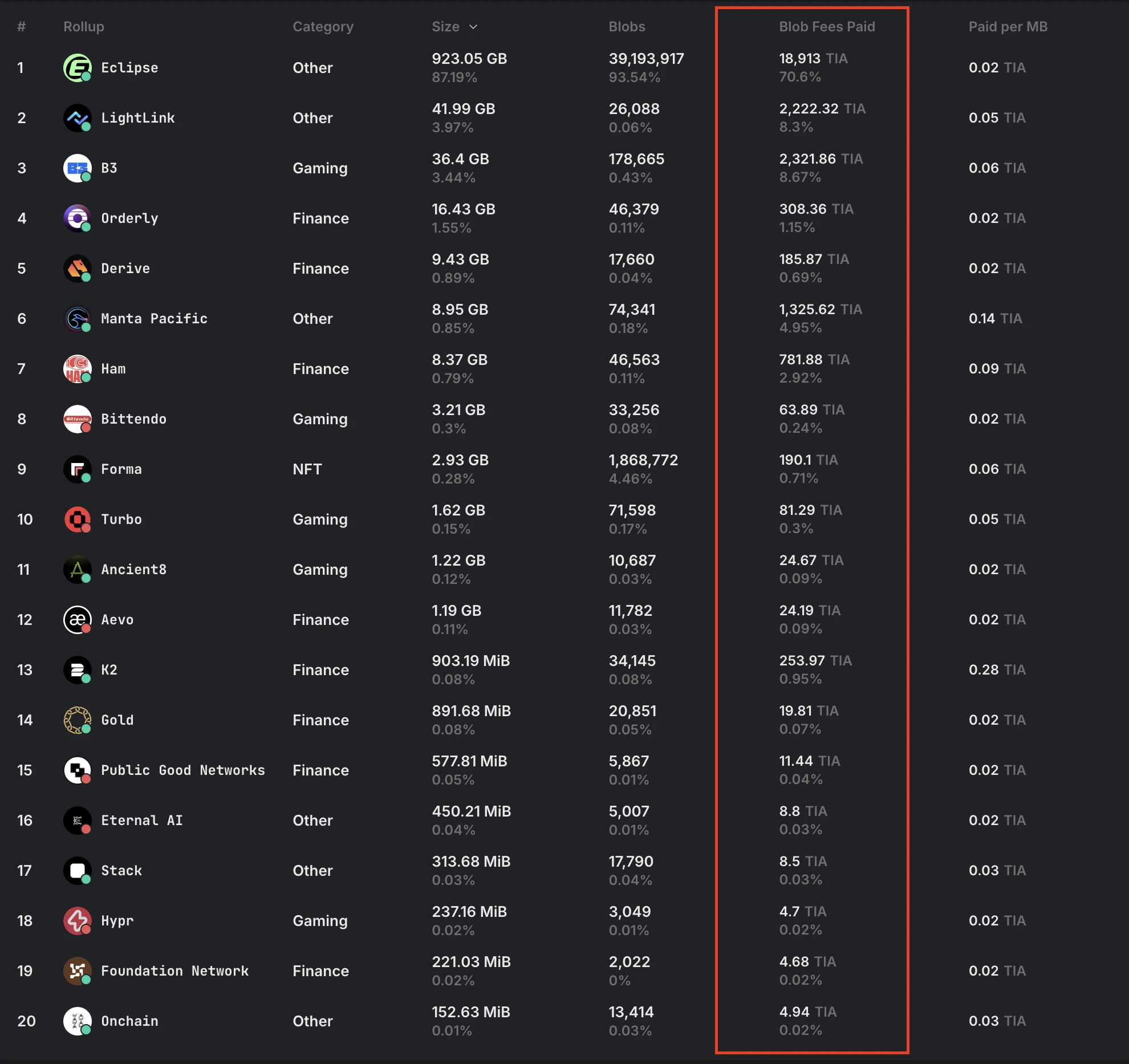

Celestia Revenue, source: Celenium.io

With Eclipse accounting for 87% of Blob uploads, it has contributed a total of 18,913 TIA in revenue to Celestia, approximately $100,000. This is an extremely unhealthy business model, as the excessively low Blob costs are far from covering Celestia's own off-chain operating costs, while being overly reliant on a single client. Moreover, this is already with Celestia having a certain ecosystem, not to mention Avail, which is almost like a "ghost chain."

Overall, Ethereum's DA currently meets the needs of the relatively sluggish ecosystem, and the subsequent Blob expansion is still underway. Currently, Blob costs are low enough, and what truly needs to lower Gas fees is the Sequencer. This is the main reason AltDA cannot effectively acquire customers. Because when Layer2 makes choices, unlike in the past, DA costs are no longer a core consideration. This also reflects a fact—the speed of infrastructure construction far exceeds the speed of application development, and applications cannot effectively drive the growth of demand for block space, making it difficult to promote the development of AltDA.

The Dilemma of AltDA: Cost Reduction and Efficiency Improvement Cannot Solve Demand Slump

"Celestia and others" seem to be caught in a dilemma: Ethereum DA is sufficient to meet current demand, and DA has become a negligible cost in projects like Layer2. The costs and loss of legitimacy associated with migrating out of the Ethereum ecosystem may far exceed the small savings from DA.

We hope to revisit a question: compared to general-purpose Rollups and other Layer2s, what is the true customer profile for DA? Our conclusion is that the customer base for DA should be non-general-purpose, vector data-driven applications.

AI data is a typical type of vector data, and applications in gaming, social media, music, etc., also fall into this category. First, we acknowledge the core idea behind the DA business model—"the DA layer is where the most valuable assets are accumulated." However, the data on the Ethereum mainnet is still primarily financial or lightweight applications, and the actual contribution of general-purpose Rollups to DA is minimal. In contrast, if vector data is on-chain, its data volume will be enormous, leading to exponential growth in demand for DA. This is also one of the reasons Lens Protocol chose to build its own public chain, as the existing DA solutions are far from sufficient to support the demand for the massive on-chain social data.

In the future, if the business model of SocialFi can be successfully implemented, the social and gaming sectors will bring real and significant market demand for DA projects, which is key to resolving the AltDA dilemma.

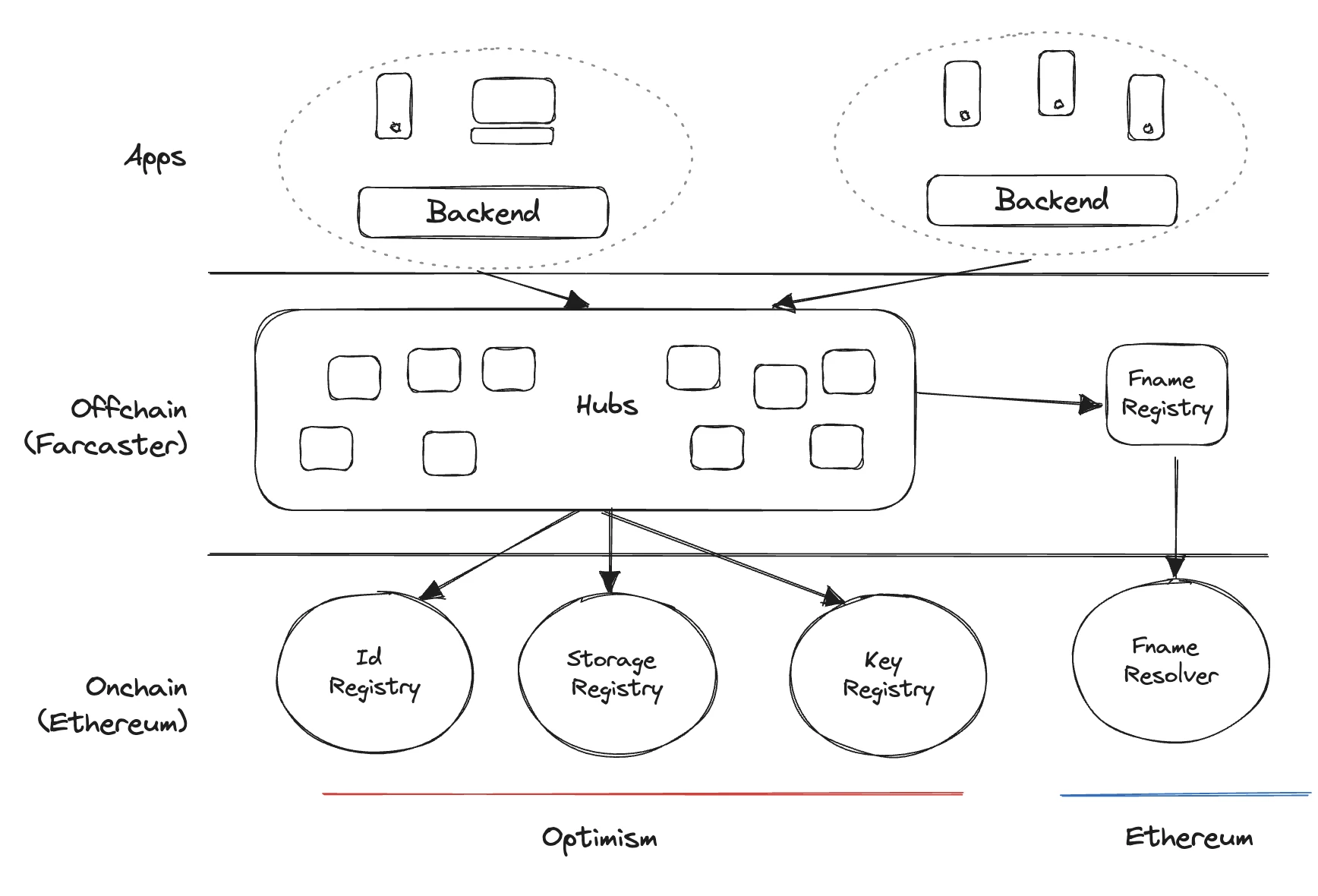

Farcaster Structure, source: Farcaster

Farcaster's architecture also adopts a method of partially indexing data on-chain, but essentially the data is not fully on-chain, which still leads to the problem of data being unable to be completely reconstructed on-chain. In the vision of Web3, in an ecosystem similar to "financial Lego," social data should possess sufficient credibility and portability, yet current social applications still fall short in terms of openness. DA projects need to vigorously promote complete data on-chain, especially in the social and gaming fields. Because even if compressed data is put on-chain, the demand for DA remains limited, far from supporting the long-term development of DA.

We can see that the actual supply of DA layer projects far exceeds market demand. In the current environment of almost zero real market demand, all DA projects are severely overvalued. Although DA is one of the real needs of Layer2, under the competition of Ethereum's native DA, AltDA has almost no market space. This is also one of the reasons why Celestia has been reported to be selling tokens over-the-counter for cashing out—up to now, the on-chain revenue of this project since its establishment has only been a few hundred thousand dollars, making it clear how difficult it is to turn the tide.

0G has also recognized the dilemma of the DA layer, and its improvements mainly target data-intensive applications, especially in AI scenarios, by building an execution layer for parallel processing of AI computations, while using a data storage layer to preserve vector data. The official claim states it supports throughput of up to 50GB/s (while the fastest EigenDA only claims to reach 15MB/s). This direction actually forms a certain competitive relationship with Filecoin/FVM and Arweave/AO. 0G believes its main advantages lie in higher throughput and execution speed, and the ability to support massive structured data.

Future Development

AltDA seems to be caught in a dilemma that is theoretically valid but lacks demand in practical business operations. The development of AltDA began when Ethereum was still in the Calldata era, at a time when DA expansion was a necessity. However, Ethereum's current DA is sufficient to meet existing demand, and the factors limiting Layer2 development are no longer just low DA costs; issues such as liquidity fragmentation and finality have become more prominent. The Gas fees paid by users are not directly caused by Ethereum but are driven by the profit orientation of Rollups, especially the revenue growth of the Base chain, which has significantly boosted the stock price of its parent company, Coinbase. In the cost structure of Rollups, DA fees account for only a small portion, making it difficult for Rollup projects to forgo the additional value brought by liquidity spillover and legitimacy from the Ethereum ecosystem for such a trivial saving.

Looking ahead, as on-chain applications flourish and Layer2 public chains continue to emerge, the demand for DA will undoubtedly rise further. However, with the ongoing expansion of Ethereum's DA and the gradual maturation of ZK compression technology, these technological advancements will further compress the market space for AltDA. Therefore, DA has reached a critical moment where transformation is necessary. DA projects need to actively explore the development of full-chain applications, especially in data-intensive scenarios such as AI, gaming, and social media, to build their own ecological barriers and cultivate real and sustainable market demand.

References

About Gate Ventures

Gate Ventures is the venture capital arm of Gate.io, focusing on investments in decentralized infrastructure, ecosystems, and applications that will reshape the world in the Web 3.0 era. Gate Ventures collaborates with global industry leaders to empower teams and startups with innovative thinking and capabilities, redefining the interaction patterns of society and finance.

Official website: https://ventures.gate.io/

Twitter: https://x.com/gate_ventures

Medium: https://medium.com/gate_ventures

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。