Original Author: 10K Ventures

This article shares our thoughts on 2025 and does not constitute investment advice.

The 10K Beta Fund has been fundraising for exactly six months since it ended in May. We thank all LPs for their support, which allows us to quickly raise funds in the first half of 2024 and get the 10K Family & Friends fund moving forward steadily.

For us, 2024 is a year full of turning points and hope. We have taken this opportunity with our Portfolio to make significant progress in the past six months and gradually expand our ecological layout. We believe 2025 will be an even more hopeful bull market year. In the previous article, we reviewed the industry trends of 2024, and this article will share our predictions for the industry in 2025, mainly including:

(1) Compliance

(2) Exchange Landscape

(3) The Future of AI Agents

(4) The Impact of Stablecoins on Cross-Border Payments

(5) The Competition for BTCFi Leadership

(6) Why Application, Not Infrastructure

01. The Importance of Compliance Rises

After FTX, the industry's tolerance for "opacity" has decreased significantly. For example, in the field of custodial wallets for exchanges, trading venues and fund custody have increasingly resembled traditional models of separation of powers and responsibilities. For instance, many institutional clients' funds are now held in CeFFu, while trading occurs on Binance, and exchanges publicly disclose their proof of reserves.

At the beginning of 2024, in the U.S., as BTC/ETH ETFs gradually passed, we saw the Trump administration becoming increasingly friendly towards crypto, and Gary Gensler is set to step down in January. In Asia, Hong Kong started a stablecoin sandbox in April this year, providing companies like RD/JD with initial opportunities to explore stablecoins. Additionally, OKX became the world's first exchange to obtain a comprehensive operating license in the UAE in 2024.

We won't discuss some vague macro policies for now, but if during Trump's term, some modifications can be made to token utility, we would consider this a significant boon for the industry's copycat projects.

Currently, the SEC accepts the following utilities: 1. Gas fees; 2. Staking (but LST is a security); 3. Governance.

If the SEC can clearly accept the following tokenomics in the future: 1. Revenue sharing; 2. Buybacks; 3. Future ETH/SOL ETFs being able to stake/restake, etc. Once the SEC makes these modifications, crypto centers in HK/SG and other Asian regions will continuously follow suit with policies, which would be extremely beneficial for copycat projects.

2. Changes in CEX Spot Market Landscape

I have always said that CEX, as a public domain traffic market, along with the Maker + Taker flywheel effect, makes it very difficult to change the competitive landscape once formed. For CEX to defeat Binance's flywheel effect, only extremely unlikely events could do so, such as all mid-to-senior level executives at BN being wanted by the FBI or Binance being exposed for misappropriating user assets to manipulate the market.

However, after the recent 2-3 years of evolution, we believe:

2.1 The Penetration Rate in the Korean Market Can Still Double to 60%

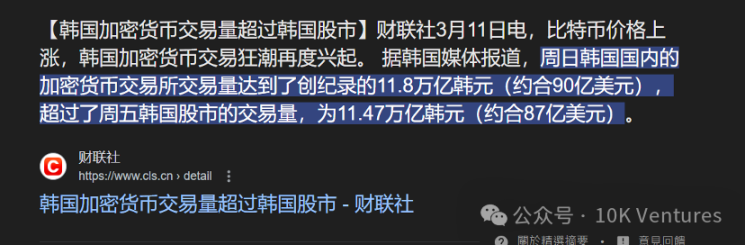

The Bank of Korea concluded based on the number of investors with accounts at the five major Korean exchanges: Upbit, Bithumb, Coin One, Cobit, and Gopax. As of November this year, the number of people holding cryptocurrencies on Korean exchanges exceeded 15.59 million, an increase of 610,000 from 14.98 million in October. Currently, South Korea's total population is estimated to be around 51.23 million. This means that the number of people holding cryptocurrencies accounts for over 30% of the total population.

There is an even more interesting statistic: last August, the number of active stock accounts in South Korea first surpassed 50 million, and by February this year, it had exceeded 60 million, which is 8 million more than the total population, equivalent to 1.16 times the total population.

Traditional large institutions and whales in Korea have not fully entered the market yet. As a market where trading pairs are all XXX/KRW, we believe that under the extreme frenzy of a bull market and wealth effect, the penetration rate in the Korean market can significantly increase next year. A typical case is the volatility and trading volume of UXLINK in Korea around Christmas, which was astonishing. I strongly recommend that project CEOs not only speak Chinese and English but also learn Korean to engage with the market in Korea.

2.2 Bitget, the "Pinduoduo" of the Crypto World, is Expected to Become a Top 3 CEX

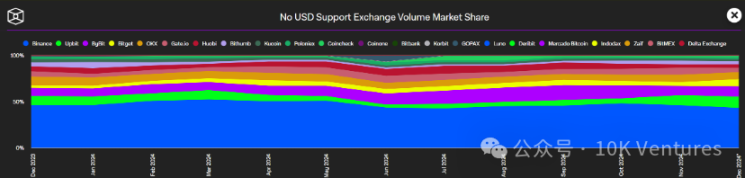

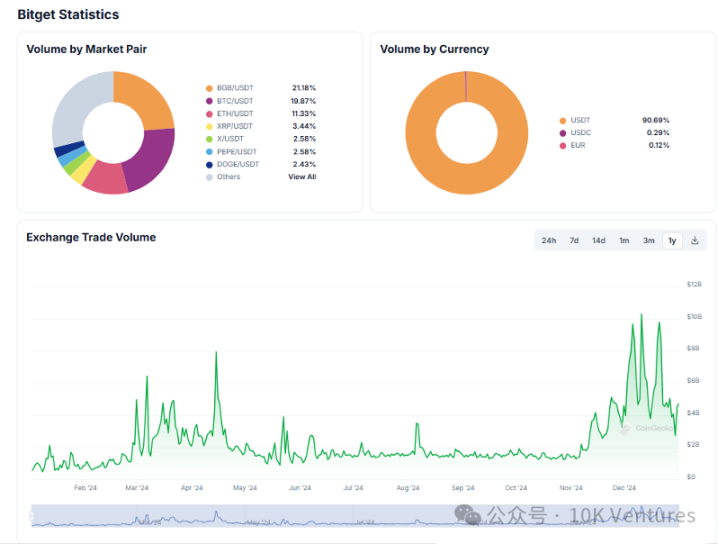

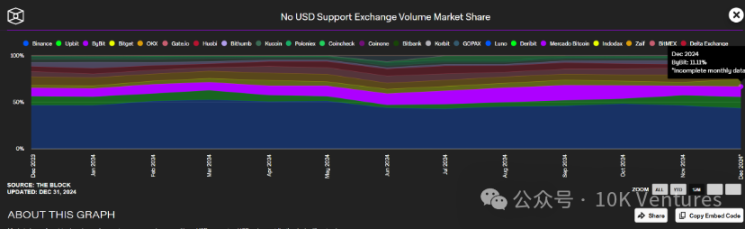

Bitget's trading volume has grown this year, from a daily trading volume of $500-1 billion at the beginning of the year to tens of billions of dollars daily in December (with only about 20% of the trading volume contributed by the great single token BGB, the rest being completely competitive). Its market share increased from 2.8% at the beginning of the year to 7.8% in December, surpassing OKX to become the world's fourth-largest exchange for non-USD trading pairs.

Bitget's success, or its future growth, comes from:

1. The core management team, represented by the handsome boss and Grace, has a clear vision. Based on empowering the platform token (e.g., launching launchpool + poolx 1-2 times a month), they continuously empower Bitget around investment (FV) + media (FN) + Bitget Wallet + Morph (L2). This reminds me of Binance in 2020-2021. Projects invested by FV are continuously listed on BG; now the token for Bitget Wallet, BWB, has been replaced with BGB; will Morph, which aims to create a consumer-grade L2, break through the market?

2. The employees are genuinely hardworking, working in a demanding environment with a high workload, and they are compensated significantly more. They are hiring from BN, OKX, and Bybit with salaries exceeding 30%-50%.

From the perspective of on-chain DEX market share, the emergence of Pumpfun has greatly increased Raydium's market share, which once accounted for 28% of the total DEX market share. Due to this year's Ethereum developments…

2.3 Bybit, the Invisible Winner of VC Tokens

Bybit started the year with an 8.79% market share, reached 16% mid-year, and ended the year with an 11% market share, making it the third-largest exchange after BN and Upbit. Many VC projects that couldn't get onto Binance found that they could achieve significant trading volume on Bybit. Moreover, after listing on Bybit, going on to Korean exchanges + Binance is also a good option. Additionally, we have recently seen Mantle starting to take action, recruiting KOLs for promotion.

Will Bybit continue to rise in 2025 and become a smaller version of Binance?

3. AI Solving Core Industry Conflicts

At the end of this year, during a conversation in Shanghai with a senior figure, a question was raised that made me ponder: What core conflict has the industry really solved?

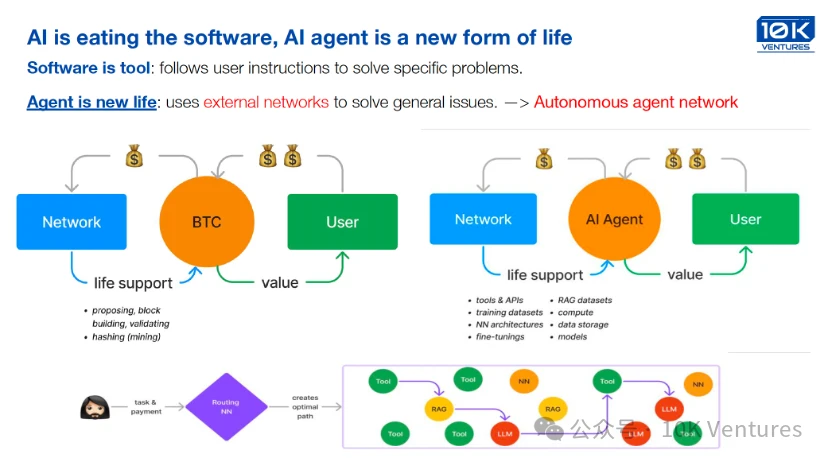

I realized that understanding this question would simultaneously provide our fund with answers regarding the industry and how we should face the upcoming primary market. I firmly believe that "In trustless we trust." If the essence of the AI era is that people have gained access to low-cost advanced intelligence, then Crypto may help facilitate open-source AI, solving core issues such as: (1) How to establish trust in Agents; (2) How Agents interact with each other; (3) How the Agentic economy unfolds.

We believe that great opportunities will arise in AI + Crypto, precisely because the essence of a crypto network is to build and transmit trust. The crypto network not only provides a reliable trust foundation for Agents through cryptography and code, but its decentralized and open characteristics, along with its inclusivity in defining subject identities, create a digital space where Agents can act autonomously, fundamentally addressing the issues of identity recognition and trust dilemmas for Agents, opening a door to true autonomy.

3.1 Agent Economy

We believe that the Agent Economy will be the most attractive direction in the AI + Crypto track, as AI Agents are reshaping the boundaries between technology and business. This is not just a technical concept but a new form of productivity and organization. Multi-Agent collaboration is a key feature of future technological architecture. Imagine an ecosystem composed of hundreds of specialized Agents, such as:

Agents specialized in Solidity programming

Agents proficient in Python development

Project management Agents responsible for overall coordination

These Agents may not directly know each other, but through a central coordinator, they can achieve efficient collaboration on complex tasks. This organizational form is similar to intelligent container orchestration systems, which will fundamentally change traditional work patterns.

The boundaries of commercial imagination are constantly being expanded. Taking IP operation as an example, AI Agents can achieve unprecedented innovative models:

Low-cost acquisition of historically valuable IP

AI Agents acting as IP brokers

Precision marketing on social networks

Exploring diversified monetization paths

3.2 On-chain Autonomous Agents: Intelligent Systems that Think and Execute Independently

In the Web3 field, the potential of AI Agents is equally exciting. For instance, the task scope of Crypto Enabled AI Autonomous Agents is vast. It could involve simple USDC payments or require the autonomous deployment of batch transfer contracts to save on gas fees, or involve multi-step on-chain interactions and complex contract creation. While many operations can be achieved using technical indicators, we cannot foresee and exhaust all scenarios. Therefore, a truly autonomous agent needs to understand tasks, decide which tools to use, gather information, and ultimately translate this into a multi-step action plan to execute operations and complete tasks.

The ideal of technology for autonomous agents driven by AI models is to build intelligent systems capable of independent thought and execution. An ideal AI Agent should possess:

Deep understanding of complex tasks

Ability to autonomously decompose tasks

Capability to independently write implementation code

Ability to integrate interdisciplinary knowledge

Autonomy in deploying smart contracts

Management of complex on-chain assets

Execution of cross-chain intelligent operations

3.3 AI Agents + Payment: The Future Economic Model of Human-Machine Collaboration

As a large and complex network of Agents forms, interactions between Agents, as well as between Agents and humans, will become more frequent, in-depth, and diverse. Payments are one of the foundations of the Agent economy; however, the existing technology stack and payment systems cannot support Agents in making autonomous payments. Agents need cryptocurrency payments.

In decentralized crypto networks, these obstacles faced by Agents are almost effortlessly resolved. Permissionless networks and open ecosystems greatly expand the capabilities of Agents. Therefore, I believe that among all directions of AI and crypto technology integration, enabling AI Agents to utilize crypto networks is very close to real-world needs and has practical prospects.

In the short term, empowering Agents with more convenient crypto payment capabilities is sufficient to expand their operational scope. From a medium to long-term perspective, digital identities based on crypto networks, permissionless protocols, decentralized applications, and the capabilities granted by smart contracts will enable Agents to operate autonomously in the digital world, collaborating, competing, and strategizing with humans and other Agents. The crypto network not only provides the foundation for Agents to act autonomously but also opens up new possibilities for future economic models of human-machine collaboration—when Agents can autonomously participate in economic activities, this development will bring about significant changes in society. (The above is written by our LP Wang Chao, which is excellent, so I must include the original text.)

3.4 AI Data: Do Leftist and Rightist Approaches Lead to the Same Outcome?

With our first round of heavy investment in Sahara in 2023 and the mid-2024 investment in Portfolio Vana listing in BN/Upbit, we have become more aware of the importance of AI data for AI companies. Nowadays, algorithms and computing power are no longer the core factors limiting model capabilities. In early 2023 to early 2024, computing power was very tight, and AI companies had a high demand for A100/H100, leading to a phenomenon where these machines were hard to come by domestically. A large number of A100/H100 units were smuggled into the country, and cloud vendors required a rental period of 1-2 years. Thus, many decentralized computing power projects, such as IO/Aethir, emerged in 2023.

As the market gradually evolved, discussions began around decentralized algorithms and token incentives for developers to contribute model algorithms for revenue sharing. We won't evaluate the reliability or narrative of these projects; everyone can think for themselves about their credibility. On December 27, 2024, Deepsake, a subsidiary of Huanshuo, emerged, training with only 1/10 of the pre-training cost of other major models in North America, achieving capabilities comparable to leading closed-source models in North America, with stronger inference capabilities and lower costs. This gradually indicates that algorithms are no longer the core limiting factor for model capabilities.

We have always believed that the only true limiting factor for model capabilities is data. We believe that in 2024, whether in web2 or web3, AI data companies will increasingly highlight their value.

In the world of web2 AI, there are more and more leading players in the data track. For example, Scale.AI has become the leader in the data labeling track. Companies like Guanglun Intelligent, representing synthetic data, are making strides in embodied intelligence and autonomous driving, securing many orders from large overseas companies.

In the world of web3 AI, our Portfolio Sahara is also doing the same, securing orders from leading domestic model companies like Zhipu, Moon's Dark Side, and Aishi Technology, as well as from leading overseas AI companies like Snapchat and Microsoft, and even securing orders from a certain department of a sovereign nation, progressing rapidly. Sahara is the most right-wing segment in the AI Data track, operating in an extremely top-down manner, distributing orders to users for labeling after securing them. In the current alpha test, more long-text labeling is being conducted; details can be seen in the screenshots of Sahara in section 1.3.3. Vana is the most left-wing segment in the AI Data track, with VANA's data sourced from user contributions within the ecosystem. VANA ecosystem participants contribute data from X, LinkedIn, and other social media or IoT data, all of which will be securely stored off-chain. The data is verified, cleaned, and labeled before being applied to model development.

Whether companies in the AI data track can cross cycles and become evergreen companies similar to Chainlink still depends on their ability to achieve long-term commercialization (2B securing orders) and to listen to the community (2C, creating products that users can perceive), rather than just their storytelling ability.

4. Stablecoins are Changing Cross-Border Payments

Fiat-backed stablecoins are changing the payment industry from the top down, with stablecoins addressing core issues such as settlement cycles and transaction friction in traditional payment channels.

At the end of this year, we are working with a fiat-backed stablecoin company that I believe has the potential to make a significant impact in the web2 cross-border payment field among stablecoin companies I have seen in the past two years. In the crypto-native stablecoin track, I have discussed Ethena and Usual over the past two years. I believe Ethena may have systemic risks and its token utility is too weak; Usual, as a decentralized Tether, is somewhat awkward, with returns not matching those of purely delta-neutral Ethena, and its AUM not surpassing FDUSD. In the fiat-backed stablecoin track, we have had in-depth discussions about FDUSD and RD, and we believe each has its own issues. The problem with FD is that the team is neither crypto-native nor knowledgeable about traditional payments. The problem with RD is that it is completely not crypto-native.

However, after recently talking with executives from this team, I saw a truly crypto-native + web2 cross-border payment use case that aligns with my expectations. After interviews with the team’s executives and upstream and downstream (payment companies, bulk traders), we summarized and shared some interesting points:

1. Problems Needing Resolution in Traditional Trade

In traditional trade, the settlement cycle is a headache, requiring the arrangement of cash flow, determining arrival times, shipping settlement times, and waiting for the delivery of documents before proceeding to the next round of collections and payments. Remittance times typically range from 1 to 5 days, with friction due to the strength of fiat currencies ranging from 1% to 3%. When importing or exporting to countries with smaller currencies, real-time exchange rates need to be monitored. If it involves countries with severe conflicts, it can be quite risky for both parties. Transactions have historically been conducted in USD, but USD transactions face issues in cross-border dealings, and time zone differences are also a concern. Additionally, contacting intermediary banks involves both one's own bank and the counterpart's bank, which can sometimes lead to liquidity shortages, causing delays in payments and collections, making it difficult to calculate cash flow costs. There are also issues with exchange rate discrepancies and a series of problems where goods have arrived but payments have not yet been received.

For example, one international trader we researched has suppliers in Africa, where the local financial system is so poor that they do not trust banks, only USDC, because USDC can be exchanged for USD through CB.

Another trader we researched, with clients in Latin America, told us that after their clients pay USD into their Argentine accounts, it becomes very difficult to transfer that money out because Argentina is so short on USD; while the process of transferring in is easy, the process of remitting out is very complicated.

2. The Demand for Stablecoins is Entirely Bottom-Up, with Payment Institutions Accepting Stablecoins

Initially, there was not much demand from customers, but as the past two years have progressed, demand has gradually increased. During a visit to Yiwu, I found that many small vendors in Yiwu provide foreigners with two QR codes, one for payment and the other for a stablecoin address. You will find that its use cases are becoming increasingly diverse.

Especially in some emerging markets, stablecoins are effectively products that replace the US dollar. Many local users are willing to accept stablecoins, which, compared to the US dollar, are not on the same scale in terms of bank accounts or liquidity.

Therefore, once many end users possess U, for Chinese companies going overseas, such as in Africa or along the Belt and Road, when local suppliers offer them money to choose between local fiat currency or stablecoins, I believe many companies will opt to receive stablecoins. This is a bottom-up process. As the adoption at the grassroots level becomes more widespread, these companies gradually start accepting stablecoins. Moreover, during the payment collection process, they find that stablecoins can indeed solve payment issues, prompting them to pressure payment institutions to inquire whether they are willing to accept this form of payment, even assisting them with foreign exchange transactions. Eventually, payment institutions begin to reflect and push back, starting to handle related business.

3. The Competitiveness of Different Fiat-Backed Stablecoins in Web2 Cross-Border Payments Comes from Localization for 2B and Whether They Can Serve Customers in Real-Time

Being able to find a team when issues arise is a core competitive advantage. Most traditional customers and traders are completely unaware of U; they perceive U as just another form of US dollar. Thus, this process involves whether the product can be easily understood and operated by those who have never used it before, whether the operation is secure, and how well the service provider maintains customer relationships, all of which are very important.

Customers are most concerned about sending money and not receiving a response for half a day, especially when they need to pay for goods today. At this moment, if you tell me that the cash flow is insufficient and that we need to delay for another day due to this or that issue, delaying another day could incur an additional penalty of 20,000 to 30,000.

5. Who Will Become the Leader in BTCFi?

Continuing from what we discussed in our November quarterly report, we have always placed great importance on how to provide Bitcoin holders with risk-free yield (and congratulations to our Portfolio Solv on Binance). Based on first principles, we believe this is the most essential need of Bitcoin holders. Based on this, our first bullish direction is Bitcoin (re)staking for yield, and the other is how to trustlessly transfer Bitcoin to other chains to provide liquidity (the result of cross-chain is also to provide liquidity for financial management).

We will not delve too deeply into the fundamentals of Babylon and Solv; instead, we want to present a few viewpoints:

1. Solv's revenue primarily comes from tangible trading activities, such as funding rate arbitrage, JLP's delta-neutral strategies, and BTC-denominated options arbitrage. This type of revenue is very high in a bull market, starting at 15%-20%, but the yield in a bear market will be relatively low, starting at 3%-5%.

Babylon's revenue comes more from the clients' own coins and BBN coins. BBN may experience a flywheel effect in a bull market, while in a bear market, the Babylon ecosystem's revenue may be quite bleak.

2. During a bear market, it is necessary to seek financial management income in traditional web2 scenarios; currently, we see opportunities in supply chain finance and similar areas.

3. The first-mover advantage will be significant; as the leaders in the field, Babylon/Solv will likely capture users' minds first if they can issue tokens and create considerable wealth effects (market rallies equate to marketing).

- From the growth in ETF holdings, it is evident that an increasing amount of BTC is being held by large institutions. Whoever can operate more compliantly and meet the needs of large institutions, Babylon or Solv, is more likely to become the leader in BTCFi in the long run.

6. Application☑️ Infra❌

Speaking of this topic, we can look at how much it costs to build a good ecosystem. Hyperliquid went from $3 to $30, conservatively estimated to have cost over $100M. The funds required to build a top-tier public chain ecosystem in this cycle have far exceeded the costs that ordinary infrastructure projects can bear. We also do not believe that there is a significant possibility of a paradigm shift in underlying blockchain technology, and the probability of early VC bets on infrastructure projects breaking through is indeed low and hard to sustain. We will be cautious about early investment opportunities in the infrastructure field and will focus on betting on application use cases.

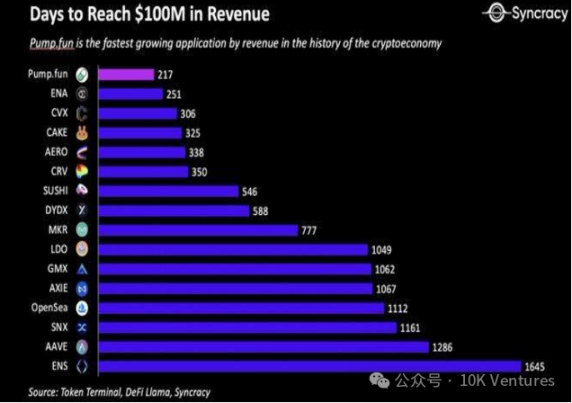

However, looking back at the performance of applications in 2024, it is truly impressive. This year, records for days when revenue breaks $100M have been continuously shattered, first by Ethena (8 months), then by Pump.fun (7 months), showcasing the blockchain industry's tremendous explosive power—if the direction and product are right, the market will provide the fastest feedback. But have you ever wondered why the following lists are all related to trading?

It is because of the right to record transactions; in the blockchain industry, it is all about the right to record. Since the first barter transaction occurred thousands of years ago, trading and recording have been passed down through human civilization, from single-entry bookkeeping to the double-entry bookkeeping method developed during the Renaissance, and now to blockchain recording, which essentially decentralizes the right to record to everyone.

(The following is a direct quote from our LP, which is excellently written.)

The most mainstream assets arise from the most important powers. Bitcoin is used to record scarce fixed outputs, Ethereum and Tron are used to record currency codes, primarily US dollar stablecoins and related transactions, while Solana is used to record high-frequency trading and meme gambling. The question arises: this industry currently only records about 0.3% of global assets and less than 1% of transactions; the remaining 99.7% of assets and 99% of transactions have yet to be recorded. This is the true beta and also alpha. RWA needs to be thought of from this perspective. More interestingly, the so-called tokenization and valuations that cannot be analyzed using traditional fundamentals grant a premium to this recording power, which is the only means to ensure that this power does not flow back into the traditional system, driven by human greed.

Looking back at the applications that have had a breakout effect in recent years, they are essentially upgrades in the recording of assets in different application scenarios—DeFi (recording financial assets), GameFi (recording gaming assets), NFT (recording art/images), Friend.tech (quantifying social value), and Meme (recording gambling). As blockchain underlying technology continues to iterate and has demonstrated substantial commercialization capabilities and products from 2020 to 2024, we may see new asset recording upgrades in 2025 and beyond, such as AI x Crypto (recording computing power and data), DeSci (recording science/charity), RWA (recording houses/offices), PayFi (recording supply chain finance), and SocialFi (recording quantified social value).

7. Traditional Giants Begin to Enter

This year, we have observed an increasing number of traditional companies entering the crypto space from various angles, such as PayPal entering the stablecoin space through PYUSD; JD.com entering the Hong Kong stablecoin sandbox; a large number of US-listed companies beginning to accumulate BTC; and traditional cross-border payment companies starting to accept stablecoin payments.

Does this prompt us to think anew about how to serve this new batch of players entering crypto? Will these new players have new ideas? Our focus next year will be to closely observe the needs of these large new players regarding crypto.

8. What Does Everyone Think?

In preparing this annual report, we gathered insights from industry friends regarding next year's primary and secondary investment opportunities.

Here are their main viewpoints for your reference:

The combination of AI and Crypto is still seen as the most promising direction for the future, especially AI Agents, which are viewed as important applications for the next bull market. The coordination of multiple AI Agents, the shift of Web2 AI startups, and the integration of AI with MEME, payments, TEE, and stablecoins are all highly anticipated.

Payments and RWA

New public chain ecosystems, with a focus on Hyperliquid, Monad, Berachain, Base, and Solana

The return of ICOs

BTC is a deterministic opportunity

Risk-free arbitrage

DEX trading terminals (such as Dexx, GMGN, Infinex) and intent-based chain abstractions (such as Across, Near Intent for Base and SOL)

Options-related opportunities that can yield real returns and arbitrage both within and outside the industry

User acquisition tools combined with MEME, MEMEFi

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。