On December 5, 2024, the value of a single Bitcoin reached $100,000, a historic high, with a market capitalization of $2.1 trillion. It officially entered the six-figure range. The once unattainable and seemingly fantastical $100,000 is now history.

Any asset that grows from zero to several trillion dollars in market value inevitably has a grand story behind it, and Bitcoin is no exception. For those of us in the midst of it, the journey of Bitcoin over the past decade and more seems almost magical. The Bitcoin network was officially launched on January 3, 2009, with an initial trading price of $0.0008.

At a price of $100,000, Bitcoin's increase exceeds 125 million times. Let us return to the starting point of cryptocurrency, commemorating the release of the Bitcoin white paper.

The 2008 Financial Crisis, The Starting Point

Compared to Bitcoin's current glory, its birth was almost insignificant.

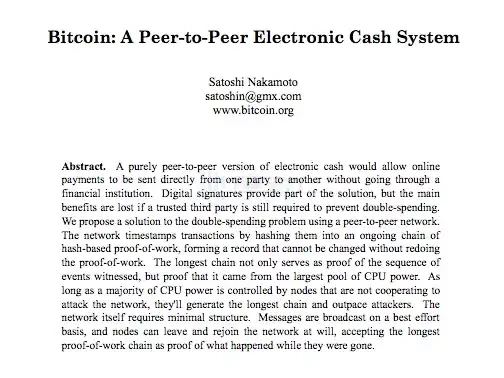

In November 2008, a paper authored by Satoshi Nakamoto was published online, titled "Bitcoin: A Peer-to-Peer Electronic Cash System." The paper detailed how to create a "trustless electronic transaction system" using a peer-to-peer network.

The birth of Bitcoin directly reflected Satoshi Nakamoto's profound disappointment with the financial system of the time. In September 2008, the financial crisis, triggered by the collapse of Lehman Brothers, erupted in the United States and quickly spread globally. To save the economy on the brink of collapse, the U.S. government took unprecedented intervention measures: massive public funds to bail out the market and monetary overexpansion caused by quantitative easing. Although these measures alleviated the crisis in the short term, they also brought a series of side effects such as inflation, market turmoil, and exchange rate fluctuations.

As a result, Satoshi Nakamoto conceived a bold idea: to create a currency system independent of governments and financial institutions. In the traditional system, currency is issued by central banks, and transactions are recorded and confirmed by banks. Bitcoin broke this model, making peer-to-peer transactions possible through decentralized blockchain technology, without the need for third-party intervention.

The core design of Bitcoin also reflects its philosophy: its total supply is limited to 21 million coins, avoiding the devaluation risk caused by unlimited issuance of traditional currencies. This design ensures the scarcity of Bitcoin, allowing it to serve as "digital gold" in an inflationary environment. This characteristic attracted widespread attention from cryptography enthusiasts and economists.

However, there is controversy in the economics community regarding Bitcoin's quantitative design. Keynesian scholars argue that a fixed total supply deprives monetary policy of flexibility, and the deflationary effect may hinder economic development. In contrast, supporters of the Austrian school believe that a fixed money supply helps reduce human intervention, and deflation may actually encourage market efficiency.

Two months after the release of Nakamoto's paper, on January 3, 2009, Satoshi Nakamoto personally mined the Genesis Block on a small server in Helsinki, Finland. As a reward, he received the first 50 Bitcoins, marking the birth of the first Bitcoin.

Silk Road, The Dark Demand

For a long time after Bitcoin's birth, it went unnoticed. People wondered: what is the practical use of this invention? Even Satoshi Nakamoto, the genius founder, never provided a clear answer. In December 2010, he left his last message online and mysteriously disappeared.

In the early years of Bitcoin's existence, its value hovered around $0.1 per coin. The most famous transaction during that time was someone purchasing a pizza for 10,000 Bitcoins. Despite Bitcoin's design being nearly perfect, it was like a script without a performance, deemed to lack practical significance—until it encountered another "genius."

Ross Ulbricht, born in 1984, got involved in drug trafficking during his college years. Limited by the government's strict control over drugs, his business could never scale. The turning point came in 2010 when he heard about Bitcoin from a customer.

Ross Ulbricht

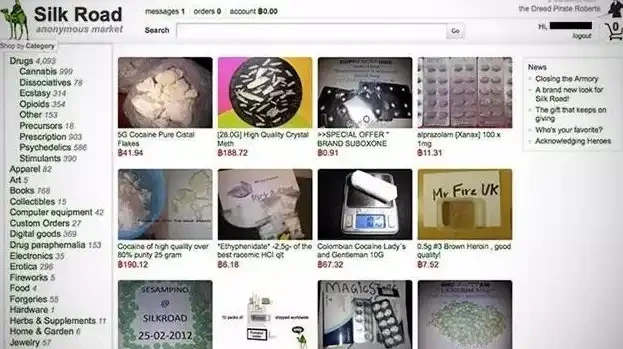

The government's crackdown on illegal activities hinges on monitoring the flow of funds, which relies on the traditional banking system. However, Bitcoin, as a decentralized and hard-to-trace payment tool, is naturally suited to evade regulation. Ross keenly realized that this was the tool he needed. In January 2011, 26-year-old Ross created a deep web platform—commonly referred to as the dark web. He named this platform "Silk Road," symbolizing a market for free trade.

However, the transactions on "Silk Road" were not for tea, silk, or porcelain, but for illegal goods such as drugs, human trafficking, child pornography, hired killers, weapons, and fake documents. This platform quickly became the most notorious dark web market globally, attracting a large number of illegal traders.

With the rise of "Silk Road," Bitcoin finally found its first large-scale application scenario: a payment tool for illicit transactions. Statistics show that Silk Road circulated over 9.5 million Bitcoins, accounting for 80% of the circulating supply at that time. This undoubtedly thrust Bitcoin into the spotlight of public opinion.

Ross's criminal activities ultimately led to his downfall. Not only did he engage in drug trafficking through "Silk Road," but he also attempted to resolve business disputes by hiring hitmen. In August 2013, he was arrested in a public library in San Francisco. In 2015, Ross was sentenced to life in prison without the possibility of parole.

Screenshot of the Silk Road website

Just like the consensus of fools, it is also a consensus. Dark demand is still demand.

Driven by criminal transactions, Bitcoin experienced its first surge, reaching $31 in June 2011. Two months after Ross's arrest, Bitcoin soared to $1,100 per coin. It can be definitively stated that Ross is an important figure in the history of Bitcoin's development. Just as Bitcoin was about to be overlooked by the world, he ended Bitcoin's history as a toy and gave it real-world significance—serving crime.

"Criminals are the most adept at embracing new technologies," summarized Xu Zhihong, a partner at Biyou. Law enforcement agencies gradually mastered the technology to trace Bitcoin transactions, diminishing its appeal in illegal markets. More and more criminal transactions began to shift to harder-to-trace cryptocurrencies, such as Monero, leading Bitcoin into a prolonged bear market lasting several years.

The Block Size War and Forking Crossroads

Fast forward to 2015, the Bitcoin community faced the most intense controversy in its history—the block size war. This "block size war" not only caused a split in the community but also led to the largest hard fork in Bitcoin's history.

Since Satoshi Nakamoto designed Bitcoin in 2009, the block size has been limited to 1 megabyte. This design aimed to prevent meaningless transactions and network data inflation. However, as the number of users increased, this limitation became increasingly inadequate: transaction congestion, soaring fees, and delayed confirmation times. In 2013, core developer Jeff Garzik proposed increasing the block size to 2 megabytes, sparking intense discussions in the community about scaling.

By 2015, the rapid growth in transaction volume made the scaling issue urgent. The Bitcoin developer camp split into two factions: one faction supporting larger blocks advocated for direct scaling to solve congestion issues; the opponents argued that decentralization was more important and advocated for improving transaction efficiency through technical optimization.

Developers supporting scaling, Gavin Andresen and Mike Hearn, believed that Bitcoin's goal was to serve as an efficient "electronic cash system," rather than merely a store of value. To this end, they proposed the BIP-101 proposal, suggesting increasing the block size to 8 megabytes. They argued that Bitcoin transactions were becoming increasingly slow, and the fees for transactions were rising correspondingly; if this continued, Bitcoin would become as mundane as bank card transactions.

Opponents, including core developers Greg Maxell, Luke-Jr, and Pieter Wuille, warned that larger blocks could increase the hardware costs for running nodes, reducing the number of full nodes and weakening the decentralization of the Bitcoin network. They preferred to adopt second-layer solutions like "Segregated Witness" and "Lightning Network" to optimize transactions without changing the block size. Related reading: "Today in History | Eight Years of Block Size Wars, The Balancing Philosophy of Blockchain"

This dispute directly led to the birth of Ethereum. Ethereum founder Vitalik Buterin was a staunch supporter of larger blocks. When he realized that Bitcoin might struggle to adopt larger blocks, he took a different path, shifting the scalability issue to a new chain, allowing for larger blocks and flexible smart contract designs to reduce transaction fees, enabling Ethereum to do more.

On February 20, 2016, both sides reached an agreement in Hong Kong known as the "Hong Kong Consensus." The agreement included the implementation of Segregated Witness technology and subsequent scaling plans, which were seen as a significant breakthrough to quell the controversy. However, the agreement was soon denied due to the absence of core developers from Bitcoin Core in the signing and their insufficient expression of support. The collapse of the Hong Kong Consensus intensified community conflicts, and trust between miners and developers was nearly obliterated.

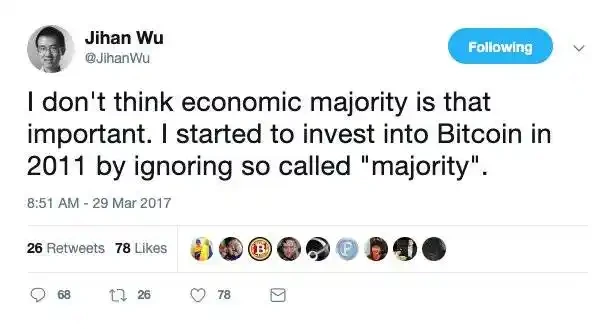

With the failure of the Hong Kong Consensus, the dispute escalated into a philosophical confrontation over Bitcoin's future direction. One side emphasized transaction efficiency, while the other insisted on decentralization. This divergence ultimately led to the hard fork in 2017. Bitmain founder Wu Jihan became the representative of the larger block faction, advocating for creating a new chain through forking to support the 8-megabyte block proposal.

On a day in March 2017, Wu Jihan tweeted, "I believe the economic majority is not important; I ignored the so-called majority when I started investing in Bitcoin in 2011." He decided to start anew and no longer play with Bitcoin Core.

At that time, Wu Jihan, as one of the founders of Bitmain, the world's largest cryptocurrency mining machine manufacturer, was ranked 32nd on Hurun's list of wealthiest individuals born in the 1980s, with assets of 16.5 billion RMB. Bitmain controlled over 60% of the Bitcoin network's computing power, and Wu Jihan was considered "the only person with a chance to destroy and control Bitcoin." Therefore, Wu Jihan's fork plan received support from miners and some developers.

On August 1, 2017, the fork officially occurred, and Bitcoin Cash (BCH) was born. BCH was designed to support larger blocks and was incompatible with the Segregated Witness technology, allowing it to handle more transactions. Meanwhile, the Bitcoin Core camp insisted on the small block solution of 1 megabyte and optimized transaction efficiency through Segregated Witness and the Lightning Network.

After the fork, Bitcoin and Bitcoin Cash developed along different paths. Wu Jihan sought market recognition for BCH by driving up its price and weakening BTC's computing power. In the short term, BCH's price soared from $200 to nearly $900, triggering a wave of miners switching over. However, Bitcoin's brand effect and vast ecosystem kept it in a dominant position. Over time, BCH's price and market capitalization gradually shrank, and its computing power share continued to decline.

But with the arrival of the bear market in 2018, BCH's price plummeted, causing significant losses for Bitmain, which had heavily invested in the BCH sector. Subsequently, BCH maintained a rough 1:20 ratio with Bitcoin in terms of both price and computing power. Due to the heavy holdings in BCH, Bitmain faced scrutiny during its Hong Kong IPO in 2018, with questions raised about relying on BCH sales for revenue.

Looking back two years after the Bitcoin fork, the BTC fork event had long settled, and BCH had taken a parallel route. However, this fork had a profound impact on the entire Bitcoin ecosystem. Related reading: "The History of Bitcoin Forks."

The Story of Miners

If I told you today that Bitcoin had a chance to be controlled by Chinese people ten years ago, would you believe it?

On a night in May 2010, a hungry programmer exchanged 10,000 Bitcoins for two pizzas worth $30, giving Bitcoin its first valuation—$0.003. This intangible protocol suddenly had real value, leading to a bull market filled with wealth myths and the rise of cryptocurrency mining.

In the early days, Bitcoin had no value, and there were very few participants in the network; mining only required a computer CPU. Hal Finney was among the earliest miners, and within a week or two, he mined thousands of Bitcoins with his computer, eventually stopping the mining software due to overheating and the annoying noise of the computer fan.

However, this $0.003 transaction changed everything. Seeing that Bitcoin mining was profitable, more and more people joined the network, and soon, various geeks began writing their own GPU mining programs and building targeted mining machines, which we now know as mining rigs.

Quickly, this technological craze spread to domestic geek forums, sparking enthusiastic discussions among a small group. In 2011, Wu Jihan funded Changsha and established the earliest Bitcoin forum in China, Babit, where discussions on mining began. Zhang Nangen, studying integrated circuit design at Beihang University, gained fame for creating FPGA mining machines and was nicknamed "Pumpkin Zhang" by netizens. Another notable figure was a software engineer from Guilin, "Watermelon Li," who developed the popular "Watermelon Miner."

Just as GPUs were becoming mainstream, a small American company called Butterfly Labs announced that it was developing a machine specifically for Bitcoin mining—ASIC. This machine discarded all other computer functions and was designed solely for the Bitcoin SHA-256 algorithm, achieving speeds far exceeding those of GPU miners.

Butterfly miner, image sourced from the internet

Once the concept of ASIC miners reached China, action was quickly taken. Besides the previously mentioned "Pumpkin Zhang," there was another legendary figure in the mining circle, "Cat Miner" Jiang Xinyu. Cat Miner entered the University of Science and Technology of China at 15 and later pursued a PhD in computer science at Yale. He was captivated by Bitcoin's ideology upon first hearing about it and returned to China to become a miner before finishing his studies, becoming the second person in China to develop an ASIC miner after Zhang Nangen.

In August 2012, Cat Miner established a company in Shenzhen and conducted an IPO online, issuing 160,000 shares at a price of 0.1 Bitcoins per share, with the code ASICMINER. He then used the funds raised to open a mining farm in Shenzhen, mining Bitcoin with his machines, reportedly earning 200 million RMB in three months.

A rare public photo of Cat Miner (on the left), image sourced from the internet

Seventeen days after Cat Miner's ASIC prototype was announced, Zhang Nangen also formed his Avalon team and completed the delivery of the first mining machine, Avalon 1. While Cat Miner and Zhang Nangen were rapidly developing, another competitor entered the scene. In the first half of 2013, Wu Jihan founded Bitmain, which launched three types of computing power chips in just 13 months, forming a three-way competition with Cat Miner and Zhang Nangen. After the winter season, Bitmain's Antminer S1 swept away many competitors, allowing its mining machine agents to earn a significant profit.

Cat Miner and Zhang Nangen also faced high demand and thriving businesses, ushering in the era of Bitcoin ASIC miners.

The enormous wealth effect attracted countless entrepreneurs to enter the market, producing various Bitcoin mining machines, with names like "Chrysanthemum Miner," "Cockroach Miner," and "Silverfish Miner" in abundance. Manufacturers competed fiercely, and the iteration of mining machines accelerated to the point where early pre-ordered futures mining machines became outdated by the time they were delivered. Eventually, manufacturers realized that while their mining machines were still on the production line, their competitors' customers had already received machines with better performance. Companies like Bitmain, which entered the market early, began deploying computing power on a larger scale, and from this point on, over 70% of Bitcoin's computing power was firmly rooted in China.

On the other hand, under the leadership of geek miners, a large number of gold diggers flooded into China's Bitcoin market. Driven by "Chinese aunties," Bitcoin's price skyrocketed, breaking through the 4,000 RMB mark and approaching 7,000 RMB within days, while at the beginning of the year, Bitcoin was still below 80 RMB. In just a few months, approximately 10 billion RMB of capital was injected into the market, making China the most enthusiastic market for mining and trading Bitcoin in the world.

In 2013, Bitcoin created one wealth myth after another, with Li Xiaolai being the most typical example. This former New Oriental English teacher purchased 100,000 Bitcoins in 2011 and has since become China's "Bitcoin billionaire," founding the Bitcoin Fund and Yunbi. Another example is "Old Cat," who, ten years ago, saw a report about Bitcoin in a newspaper kiosk while on a business trip with his boss, which changed the trajectory of his life.

Related reading: "The End of the 8-Year Mining Era for Ethereum: Vitalik, Chinese Mining, and Nvidia"

The Great Migration

Time quickly moved to 2021, and the dark moment for miners arrived.

At midnight on June 20, all Bitcoin mining farms in Sichuan were forced to shut down due to a directive. Previously, domestic Bitcoin miners had been relocating their machines from Inner Mongolia, Qinghai, to Xinjiang and Yunnan, with Sichuan becoming the last gathering place. However, the issuance of the shutdown notice in Sichuan completely dashed miners' hopes and marked the theoretical end of mining farms within China, as the computing power that once accounted for 75% of the Bitcoin network would entirely disappear from the map.

After that unforgettable night, the capital of China's cryptocurrency mining—Chengdu—was filled with distressed and confused miners.

On June 22, in a jazz bar on the top floor of a five-star hotel in Chengdu, young men with serious expressions sat in small groups, smoking and chatting. Their T-shirts bore sporadic prints of "Bitcoin," "To Da Moon," and other cryptocurrency slogans, and their conversations were filled with keywords like "mining machines," "going overseas," and "overseas resource connections." In the bar's corridor, a few individuals were scattered about, pacing back and forth while making phone calls to sell mining machines, lighting one cigarette after another.

On the same day, a "Global Mining Resource Connection Conference" was quietly held at another five-star hotel in Chengdu, where miners from various parts of Sichuan who had already lost power gathered to systematically learn about the overseas process from presentations by various companies, hoping to salvage a "Noah's Ark" to venture across the ocean through collective warmth and shared wisdom.

From the miners' state, it was evident that the halted Chinese Bitcoin mining industry was engulfed in confusion and panic.

Fifty kilometers from Chengdu, in Dujiangyan, the mighty Min River surged down, where the father and son Li Bing from the Warring States period witnessed the world-famous water conservancy project. Contemporary Bitcoin miners saw the electric resources on which their mining machines depended.

Old Wu's mining farm is located in the mountains of Dujiangyan, covering about 1,000 square meters, relying on the impact of water flow to maintain the day-and-night roar of thousands of mining machines.

Bitcoin mining farm in the deep mountains, image from the miner

"When the policy to shut down mining farms in Inner Mongolia and Xinjiang was announced in May, I wasn't panicking," Old Wu told BlockBeats. "Having been in this industry for a long time, since 2013, there has been a crackdown on mining policies roughly every one or two years, especially in Inner Mongolia, which relies on thermal power. We are used to it."

Therefore, when the mining farms in Inner Mongolia began shutting down, Old Wu was still online, purchasing second-hand mining machines and attracting more machines to his farm for hosting. At that time, he calmly told his friends, "Don't panic."

As June approached, even Old Wu began to feel restless. The mining farm, located on the front lines, had already received wind from various channels, but Old Wu still held onto hope. "Sichuan is different from Inner Mongolia and Xinjiang; there is a lot of wasted water and electricity here, all of which are clean resources. If we don't use these resources, they will just go to waste."

Disturbing news initially began in Ya'an. On June 17, market rumors indicated that Ya'an, Sichuan, was implementing a "one-size-fits-all" policy, requiring all mining farms to shut down by the 25th, including those utilizing consumed and wasted electricity. On June 18, a notice titled "Notice on Cleaning Up and Shutting Down Virtual Currency 'Mining' Projects" was circulated within the community, issued by the Sichuan Provincial Development and Reform Commission and the Sichuan Provincial Energy Bureau, demanding the shutdown of 26 suspected virtual currency "mining" projects by June 20.

On the evening of the 19th, Old Wu finally set aside his luck and lamented, "I have to change careers again," as he turned off the continuously roaring mining machines and began to transfer the mining farm.

Compared to miner Old Long, Old Wu was somewhat fortunate, as his mining farm had been operational for several years, and the profits from the previous years were still considerable.

"In March of this year, I started building a hosting mining farm in Ganzi Prefecture, which was completed in May. It has a load capacity of 50,000 kilowatts and can accommodate over 30,000 mining machines, but it was blocked by policy just before it started operating," Old Long told BlockBeats. The total investment in this mining farm was close to 20 million RMB, which can be considered a total loss. "After all, the profit from a hosting mining farm comes from the difference in electricity costs and management fees."

The speed and strength of this government policy, along with the firm national stance, left Old Long feeling somewhat hopeless. "I've been in this industry for five years, and there are usually policy crackdowns every one or two years, but this time it's just too severe. Mining farms, miners, mining pools—every mining group has been affected."

In the mining circle, Old Long's experience was not the worst. "I have a friend who also runs a hosting mining farm that was already in operation. His mining farm had an investment of 160 million, with the total value of the mining machines reaching 400 million. However, after the policy was announced, not only did the mining farm lose power and the machines stop, but the roads in and out of the farm were also blocked, making it impossible to move the machines out. It was a complete mess."

In the face of the mining disaster, selling mining machines became a forced choice for many miners.

Unlike the famous mining machine sales point "Seg Plaza" in Shenzhen, although Chengdu is an important city for miners, the computer city, known as Chengdu's "Zhongguancun," did not exhibit a bustling scene of mining machine sales.

BlockBeats conducted an on-site visit and found no stalls related to mining machines in Chengdu's computer city. Upon further inquiry with merchants, it was discovered that they were not unfamiliar with mining machines. "Currently, there are very few Bitcoin mining machines flowing through offline channels, and we also need to inquire with suppliers; instead, there are more graphics card mining machines," a salesperson in the computer city told BlockBeats.

In stark contrast to the quiet offline market, online Bitcoin mining machines are experiencing a 50% clearance sale.

In the miner community, where reputation and privacy are valued, information from strangers can easily raise their suspicions. They prefer to trade with familiar miners and farms within the same circle, so the main trading market during this round of mining disaster remains large online intermediaries and communities.

Mr. Tu from Coin Core Technology told BlockBeats, "The price of mining machines has already dropped by more than half, and it has entered a buyer's market where the price is determined by the buyers." For example, the commonly seen Antminer S19 Pro 95t, which could reach prices of 60,000 to 70,000 RMB at the peak of the bull market, is now only priced at over 30,000 RMB domestically.

Online quotes for Antminer S19 at the time of publication, image from miners

BlockBeats also discovered that while foreign mining companies and farms are taking advantage of the domestic "mining disaster" to acquire mining machines at low prices, they are pushing the prices even lower. A foreign buyer expressed, "We hope to receive S19j Pro at $40/T," which translates to only 252 RMB/T, making the total price for a 100T machine only 25,200 RMB, which can be considered the "floor price" in recent months.

Such low prices indicate that the second-hand mining machine market has become saturated. Previously, Bitmain also announced a pause in the sale of spot mining machines. However, some miners believe the prices are too low and choose to wait and see.

"Perhaps because I have experienced multiple rounds of policy crackdowns, I always believe that the mining industry has prospects," Old Long told BlockBeats. "Now that the prices of mining machines are too low, I would rather shut down and wait than sell at a loss."

Senior mining industry insider Ah Hao also told BlockBeats that most mining farms are currently shut down and waiting, not selling, and are waiting for clearer policies. "Most are struggling like this now."

With the domestic survival space continuously shrinking, miners unwilling to sell their machines and leave the industry are looking to go overseas for a glimmer of hope.

Currently, there are approximately 10 million kilowatts of mining machines in Sichuan that need to go overseas. Ah Hao told BlockBeats that if these machines remain stagnant in China, the owners and investors will face significant financial costs. Just like using leverage to speculate in real estate, many miners also use borrowed funds to buy machines and build farms, carrying the pressure of millions of RMB. "They need to replenish funds every day and are very anxious," Ah Hao said.

In the face of overseas demand, mining machine companies with long-term overseas layouts see opportunities and have designed customized "overseas module containers" for miners' dilemmas, which include equipment for thermal and cold isolation, fans, networks, monitoring, and distribution cabinets, essentially creating mobile mining farms built from containers.

Such designs naturally come at a high price. For example, for Bit Deer, the minimum price for each container is 142,000 RMB, accommodating 180 units of the 19 series mining machines. Given that domestic mining farms often have thousands of machines, the cost of just the container for a medium-sized mining farm can reach nearly a million, while large farms may require tens of millions.

Currently, the main directions for mining overseas are North America and the Middle East. In North America, represented by the United States and Canada, local policies are relatively stable, and the legal system is relatively sound, with many large mining companies already stationed there. However, the comprehensive costs of mining farms in North America are high, and the U.S. imposes a 25% tariff on Chinese electronic products.

Another relatively cheaper option is Kazakhstan. This region has abundant energy resources, is closer to China, and has lower labor and construction costs, with tariffs far below those of the U.S. However, the level of legal development is not high, the business environment needs improvement, and like China, policy remains the biggest risk.

The road to going overseas is long, and on the path to "seeking true scriptures," there is not only no "Sun Wukong" to protect them but also countless pitfalls to encounter.

Recently, industry insiders reported that at a mining farm in Kazakhstan, as soon as the mining machines arrived locally, they were robbed clean, leaving miners in tears.

"There are too many pitfalls in going overseas; it's not that easy," Ah Hao also believes. "Initially, Kyrgyzstan attracted mining farms with investment promotion, but in the end, the military directly seized the Chinese mining farms, resulting in total loss."

In legal countries like the U.S. and Canada, building factories overseas faces extremely high costs. Ah Hao told BlockBeats that building a mining farm with a load of 10,000 in China costs about 3.5 to 5 million RMB. For the same scale abroad, it requires 18 to 40 million RMB. Currently, Bitmain quotes 18 million, while Bit Deer quotes 40 million.

It is worth noting that although there are various resource connections and one-stop services during the overseas process, the ultimate losses are often "fully borne by the miners."

Related reading: "The Last Bitcoin Miners in China"

Western Development

Since the comprehensive ban on Bitcoin mining activities in the inland areas in June 2021, the center of Bitcoin computing power has shifted from China to North America.

By the end of 2021, this change was visibly apparent. According to the Bitcoin Electricity Consumption Index from Cambridge, if we take the average monthly hash rate share as the standard, the global Bitcoin mining center was still in China in January 2021, but by December 2021, this center had shifted to North America.

Left image: January 2021; Right image: December 2021. Source: Cambridge Bitcoin Electricity Consumption Index

Behind this change is the continuous rise of mining companies in North America. Since 2020, North American mining companies led by Core Scientific (NASDAQ: CORZ), Riot Platform (NASDAQ: RIOT), Bitfarms (NASDAQ: BITF), and Iris Energy (NASDAQ: IREN) have begun to purchase mining machines in large quantities and have successively gone public in North America, embarking on a path of compliant operations.

In February 2020, Bit Digital (NASDAQ: BTBT) went public; in June 2021, Bitfarms, Hut 8 (TSE: HUT), and HIVE Digital (CVE: HIVE) went public; in November 2021, Iris Energy went public; in January 2022, Core Scientific went public; Riot Platform, originally a biopharmaceutical company, also took off after entering the mining wave.

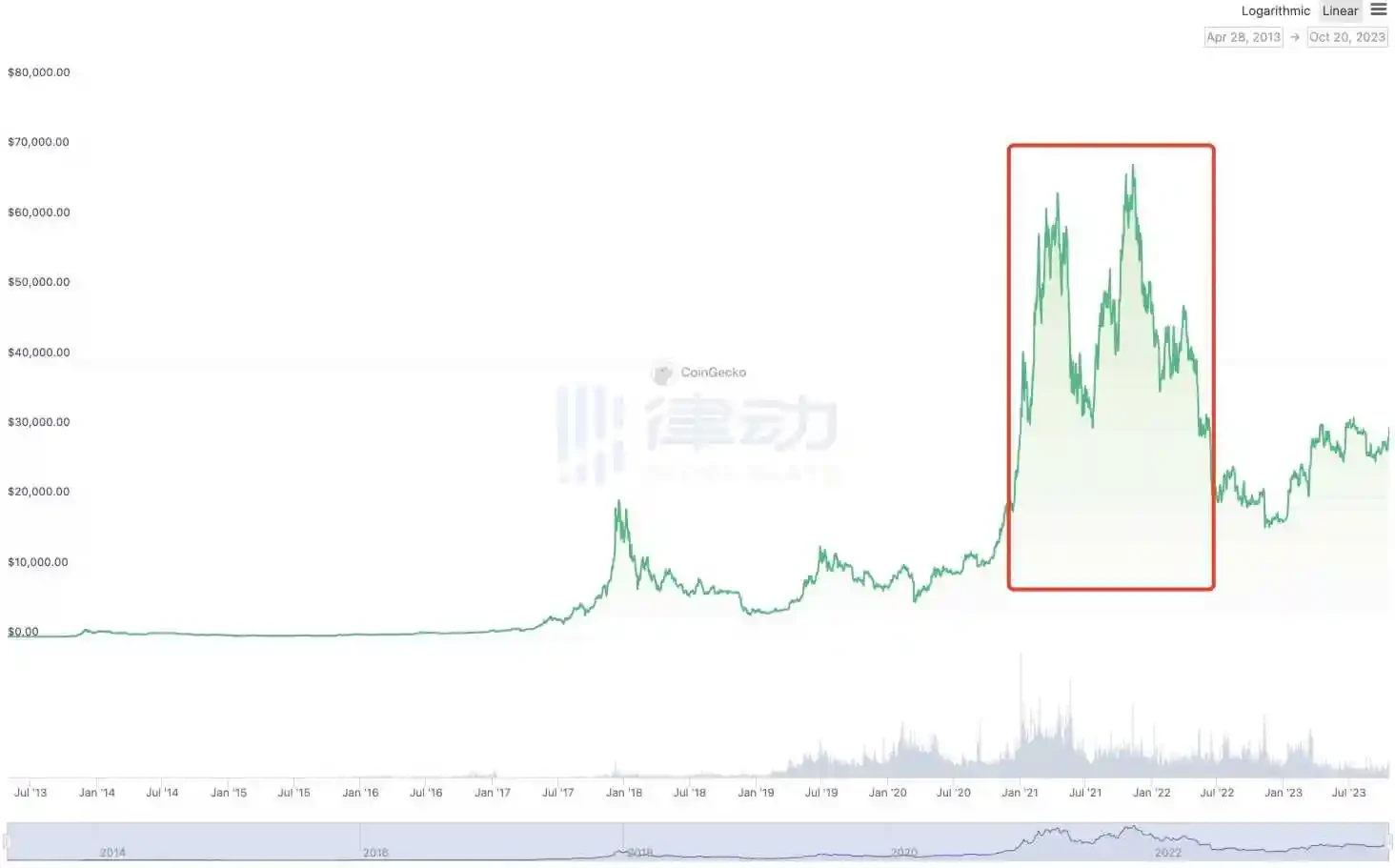

These mining companies primarily engage in Bitcoin mining, so their development is highly correlated with Bitcoin prices. During the bull market from January 2021 to May 2022, the stock prices of these companies soared. According to Nasdaq data, compared to their initial public offering prices, the stock prices of Core Scientific, Bitfarms, Hut 8, and HIVE Digital rose by as much as 57%, 707%, 371%, and 228%, respectively, during the bull market in the cryptocurrency market.

Bull market conditions from January 2021 to May 2022. Source: Coingecko

During this period, most mining companies achieved profitability through a combination of hash rate mining and debt/equity financing. Taking Marathon Digital (MARA) as an example, its main business is self-operated Bitcoin mining, with a strategy of financing to purchase mining machines and deploy mining farms, holding Bitcoin as a long-term investment after covering cash operating costs. Data shows that in 2021, Marathon Digital spent $120 million to purchase 30,000 Antminer machines from Bitmain in one go, and also obtained a $100 million revolving credit line from Silvergate Bank, planning to raise $500 million in debt through the issuance of senior convertible notes to continue purchasing mining machines, at one point becoming the largest Bitcoin holder among mining companies in North America.

Coincidentally, Core Scientific was even more extravagant, operating over 200,000 Bitcoin mining machines across five states in the U.S. At one point in June 2022, it produced over 7,000 Bitcoins. Additionally, Core Scientific received a $54 million investment from Celsius and signed a $100 million equity investment agreement with investment bank B. Riley.

However, due to its high-leverage business model, the sudden bear market caught these mining companies off guard.

First, Marathon Digital recorded a net loss of $686.7 million for the entire year of 2022; Riot Platform had a net loss of $509.6 million in 2022; Bitfarms reported a net loss of $239 million in 2022; Core Scientific lost over $1.7 billion in just the first nine months of 2022, leading to Core Scientific being on the brink of bankruptcy by the end of 2022.

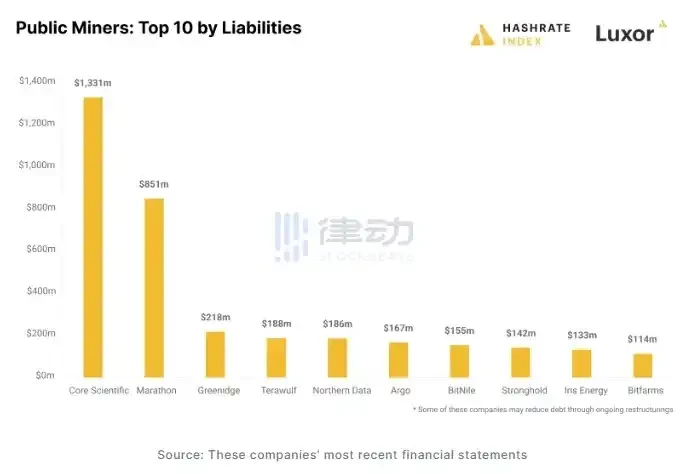

According to a report from Hashrate Index, the total collective debt of mainstream centralized mining companies exceeded $4 billion by the end of 2022, with Core Scientific having the highest debt, owing creditors $1.3 billion as of September 30, 2022; Marathon Digital owed about $851 million, most of which was in convertible notes; the third debtor was Greenidge Generation, with debts of $218 million.

Image source: Hashrate Index

Many institutions believe that the development of centralized mining companies is highly correlated with Bitcoin prices, thus "the business model of financing to purchase Bitcoin mining machines is a significant test of a company's cash flow management ability during a bear market," and it is also easy to face the risk of insolvency.

Related reading: "A Market Exceeding $9 Billion, The Paradigm Shift of Bitcoin RWA is Underway"

Regular Army

In 2017, Bitcoin experienced an epic bull market, and the cryptocurrency craze quickly swept the globe. In China, a Bitcoin trading platform named OKCoin was quietly established, which later became known as "the Huangpu Military Academy of the cryptocurrency circle." Its founder, Xu Mingxing, was originally a technical expert in the internet field and served as the CTO of Douyin. Xu Mingxing had a clear goal: to make it easier for ordinary people to access and purchase Bitcoin.

Many shared his vision. From miners to mining machine manufacturers, and blockchain developers to tech enthusiasts, more and more people joined this emerging industry. They realized that Bitcoin is not just a decentralized currency; its growth also requires a deep connection with the traditional fiat currency world. Electricity costs, equipment R&D expenses, technology development expenditures… all of these need support from the fiat economy, making trading platforms an essential bridge.

With the arrival of the first wave of the bull market, the wave of Bitcoin trading platforms also quickly rose. Platforms like OKCoin, Huobi, Binance, Coinbase, BitMEX, and Bitfinex emerged. These platforms not only provided investors with a pathway into the cryptocurrency world but also injected a continuous flow of funds into the Bitcoin ecosystem. Investors could trade Bitcoin as easily as opening a stock account through these platforms. At that stage, trading platforms almost became the only entry point for ordinary people to access Bitcoin.

Although Bitcoin prices fluctuated, the continuous inflow of traditional capital helped its price steadily rise. Meanwhile, the prosperity of trading platforms also spurred innovation in more areas. From infrastructure development to payment method exploration, Bitcoin was gradually moving from a niche experiment to the mainstream market through these platforms.

However, merely relying on investor interest was far from enough to bring Bitcoin into mainstream society. Bitcoin needed to be understood and used by more people, even entering everyday payment scenarios. In February 2021, Bitcoin's price broke through $50,000, setting a new historical record.

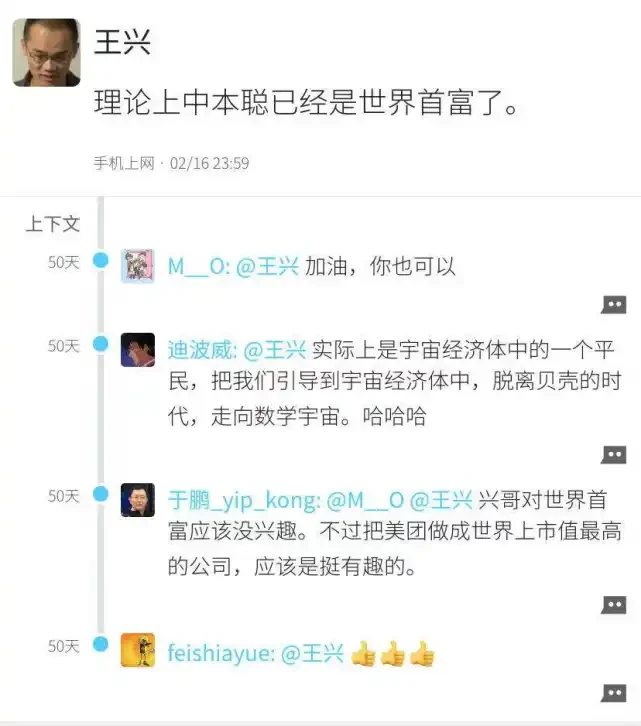

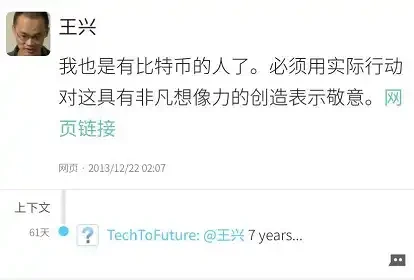

At this juncture, Meituan founder Wang Xing expressed his high recognition of Bitcoin in a post on the social platform Fanfou. As an early investor in 2013, Wang Xing had bought Bitcoin at a very low price and regarded it as a "highly imaginative creation."

Few Bitcoin supporters in China came from the financial industry. Most supporters, like Wang Xing, were from the internet sector.

XU Zhihong, a partner at Biyou, once gave a Bitcoin as a wedding gift to a friend. At that time, the value of that Bitcoin was only $300, but he repeatedly advised the recipient, "Keep it; when your child gets married, it might be able to buy a house in Beijing." Today, ten years later, such a gift has become a rare luxury.

"Bitcoin will quickly approach 80% of gold's market value (within 1.5-2 years), which is $400,000 per coin," predicted Chen Weixing, founder of Kuaidi. After merging with Didi, Chen Weixing ventured into blockchain and founded Dache Chain. As Bitcoin rose, similar predictions became increasingly common.

Related reading: "Bitcoin's Past: Meituan's Wang Xing Holds for Eight Years, Profiting a Hundredfold; Theoretically, Satoshi Nakamoto is the World's Richest"

At that time, there were two larger peaks in front of Bitcoin—how to enter the investment portfolios of mainstream financial institutions and how to enter the balance sheets of publicly listed companies.

"Currently, most financial institutions and banks cannot buy Bitcoin, and it will take a long time to form further consensus," said Zhu Xiaohu of Jinsha River Ventures in an interview with Tencent Technology. He had previously invested in a series of cutting-edge technology companies like Didi, OFO, and Yingke. Wherever there is a windfall, he is there.

"The biggest limitation for institutional participation in Bitcoin investment is still the financial regulations of various countries," said Yuan Yuming, CEO of Huolian Technology. In 2018, Yuan Yuming, then the chief analyst of TMT at Industrial Securities, announced his move to join Huobi China, which caused a stir in the circle.

And today, with Bitcoin at $100,000, both of these peaks have been achieved.

MicroStrategy, Silicon Valley, and Wall Street

When asked why there is this new market trend, almost all cryptocurrency practitioners gave the same answer—America.

"The center of blockchain innovation has always been in the U.S., and in the past two years, blockchain innovation, particularly Ethereum's innovation, has basically had nothing to do with China," said Chen Yong, founder of Biyou, who was previously a senior vice president at Cheetah Mobile before entering the cryptocurrency space. "This situation of U.S. financial innovation as the cornerstone still cannot be changed."

Also purchasing Bitcoin is the American company MicroStrategy. As the first publicly traded company to adopt Bitcoin as a primary reserve asset, MicroStrategy was founded in November 1989 and went public through an IPO on June 11, 1998.

As of the time of writing on November 21, MicroStrategy's Bitcoin holdings reached a new all-time high: 331,200 Bitcoins, with an average purchase price of $49,874.

MicroStrategy founder Michael Saylor stated that MSTR and BTC have a cooperative relationship and has published MicroStrategy's nine BTC principles, including: 1. Purchase and hold BTC indefinitely, exclusively, and securely; 2. Prioritize the long-term value creation of MSTR common stock; 3. Treat all investors with respect, consistency, and transparency; 4. Build MSTR with smart leverage to surpass BTC; 5. Continuously purchase BTC while achieving positive BTC returns; 6. Grow quickly and responsibly based on market dynamics; 7. Issue innovative fixed-income securities backed by BTC; 8. Maintain a healthy, robust, and clean balance sheet; 9. Promote the global adoption of BTC as a fiscal reserve asset.

Under such strategies and principles, MicroStrategy has also benefited significantly from the price increase of Bitcoin.

"This year, MicroStrategy's capital operations achieved a 26.4% BTC yield, bringing approximately 49,936 BTC in net gains to shareholders," stated MicroStrategy founder Michael Saylor in a social media post on November 12, 2024. Following the confirmation of "Bitcoin President" Trump returning to the White House, MicroStrategy's after-hours price briefly surpassed $360, currently reported at $355.43, setting a new historical high.

On the other hand, Silicon Valley, a hub of innovation, is experiencing FOMO. Jack Dorsey, the founder of Twitter, is a well-known tech leader in the U.S. and a more steadfast advocate of cryptocurrency than Elon Musk, believing that cryptocurrency will become the "single currency" of the world.

While Twitter is widely recognized, it is not the most successful business company founded by Dorsey. Square, under Dorsey, is a pioneer in the Bitcoin innovation space, currently valued at $120 billion, double that of Twitter. If Grayscale is likened to a pump, drawing water from the fiat world into the Bitcoin world, Silicon Valley tech companies are inventing new tools that gradually consume Bitcoin inventory like ants moving their homes.

In January 2018, Square's Cash App launched a new feature allowing users to purchase Bitcoin. "In 2020, 3 million people purchased Bitcoin through Cash App, with an additional 1 million in January 2021," data disclosed by Square's CFO indicates that Bitcoin is entering the wallets of the general public in various ways.

Under pressure from competitors, in October 2020, the world's leading online payment tool, PayPal, announced support for purchasing Bitcoin, Litecoin, and other digital currencies.

Research shows that the number of Bitcoins stored on trading platforms decreased from 3 million to 2.2 million over the past year, a reduction of 800,000. The amount of Bitcoin stored on trading platforms continues to decline.

In February 2021, Tesla announced it had purchased $1.5 billion worth of Bitcoin and would allow customers to buy Tesla cars with Bitcoin. The price of Bitcoin surged 10% instantly. Musk also announced that customers would be able to purchase Tesla cars with Bitcoin, and Tesla would not sell these Bitcoins.

Tesla was not the first tech company to take the plunge; in 2020, Square invested approximately $50 million to purchase 4,709 BTC. Square's attempt marked the first time Bitcoin appeared on the balance sheet of a publicly listed company and was recognized by accounting standards.

The limited supply of Bitcoin and the increasing demand are creating a more severe supply-demand contradiction. The approval of Bitcoin ETFs at the beginning of 2024 directly expanded this supply-demand contradiction.

Spot ETF

On January 11, 2024, the U.S. Securities and Exchange Commission (SEC) finally approved the application for Bitcoin ETFs, with 11 Bitcoin ETFs listed.

"Guys are no longer just crypto speculators; they are now serious U.S. stock traders," was a joke circulating at the time, but it genuinely reflects Bitcoin's changed status in the financial circle.

Among the approved ETFs, Grayscale (GBTC) stands out with approximately $46 billion in assets under management, while BlackRock's iShares leads the industry with a massive $9.42 trillion in assets under management. Following closely is ARK 21Shares (ARKB), managing about $6.7 billion in assets. In comparison, Bitwise (BITB), although smaller, still has around $1 billion in assets under management.

Other significant participants include VanEck, managing about $76.4 billion in assets; WisdomTree (BTCW) with $97.5 billion in assets under management; Invesco Galaxy (BTCO) and Fidelity (Wise Origin), managing $1.5 trillion and $4.5 trillion in assets, respectively.

Among them, BlackRock's spot ETF application was the most talked-about in the market. Looking back at 2023, BlackRock's application for a Bitcoin spot ETF was seen as a crucial turning point in the crypto market's bull-bear cycle. As an asset management company with over $10 trillion in assets under management, BlackRock's assets even exceed Japan's GDP of $4.97 trillion in 2018. BlackRock, Vanguard, and State Street were once referred to as the "Big Three," controlling the entire index fund industry in the U.S.

More importantly, BlackRock has an impressive success record with the SEC in getting its ETF applications approved. Historical data shows that BlackRock's success rate for SEC-approved ETFs is 575 to 1, meaning that out of 576 ETFs it applied for, only one was rejected. Therefore, when BlackRock submitted its spot Bitcoin ETF filing to the SEC in June 2023, it sparked considerable discussion in the community, which generally believed that BlackRock's entry signified the inevitable approval of Bitcoin spot ETFs.

After the approval of the spot Bitcoin ETF, its significance is primarily reflected in two aspects.

First, it enhances accessibility and popularity. As a regulated financial product, Bitcoin ETFs provide a pathway for a broader group of investors to access Bitcoin. With the Bitcoin spot ETF, financial advisors can start guiding their clients to invest in Bitcoin, which is significant for the wealth management sector, especially for capital that has not been able to invest in Bitcoin directly through traditional channels.

More directly, this opens up easy purchasing channels for many "old money" investors without worrying about the potential risks of crypto trading platforms. In contrast, the spot Bitcoin ETF is listed on strictly regulated securities trading platforms, allowing investors to hold Bitcoin price exposure through traditional stock accounts without the complexities and risks of directly holding Bitcoin.

Moreover, the ETF structure increases the likelihood of institutional investors accessing Bitcoin, some of whom are prohibited from directly investing in alternative assets. This type of product will attract large-scale capital into the market, further driving the growth of the Bitcoin marketplace.

The approval of the spot Bitcoin ETF enhances regulatory recognition and market acceptance. SEC-approved ETFs alleviate investors' concerns about safety and compliance, as they provide more comprehensive risk disclosures. A more mature regulatory framework will attract more investment, and this regulatory clarity is crucial for market participants, helping them conduct business in the cryptocurrency industry.

The legitimacy of the cryptocurrency industry has been elevated, and Bitcoin is further moving into the mainstream. This is also a step that changes the rules of the game in the cryptocurrency industry, with continuous capital inflow leading to a new surge in the entire crypto circle. Consequently, after the approval, Bitcoin's price briefly fell from $49,000 to $38,500 but gradually rebounded and successfully broke through the $53,000 mark.

Ten months have passed, and Bitcoin's price has risen significantly due to multiple factors. As of now, according to Trader T's monitoring, the total holdings of Bitcoin ETFs worldwide have surpassed the holdings of Satoshi Nakamoto's wallet address. Nate Geraci, president of The ETF Store, also disclosed that BlackRock's Bitcoin ETF asset size has exceeded that of its gold ETF, achieved in just 10 months.

At this point, it is necessary to mention the "first Bitcoin President" of the United States, Trump.

"Bitcoin President" to Return to the White House

Once upon a time, Trump was a staunch opponent of cryptocurrency. In early 2019, during his presidency, Trump publicly criticized Bitcoin and other cryptocurrencies, calling them "worthless" and believing that crypto assets could be used as tools for illegal activities. He stated that Bitcoin "is not money" and is highly volatile.

After leaving the White House, Trump continued to hold a reserved attitude in interviews, calling Bitcoin a "scam" and insisting that the dollar should be the world's only reserve currency. During this period, Trump's attitude toward cryptocurrency was generally negative. However, the NFT craze in 2021 soon began to influence Trump's perspective.

The story begins in 2022. At that time, the cryptocurrency market was in a "winter," with many crypto projects on the brink of bankruptcy and market confidence low. It was during this time that Trump's long-time advisor, Bill Zanker, appeared in his life with a suggestion that would change Trump's mind: to issue Trump-themed NFTs.

Trump expressed unexpected interest in this—however, he did not like the term "NFT" and preferred to call it "digital trading cards." Although it seemed quirky, these cards became immensely popular, selling for $99 each and almost selling out immediately after release. Trump's NFTs allowed the former president to "stand in front of the crypto community" for the first time, bringing him tens of millions of dollars in revenue and introducing him to a new, powerful support group.

As a result, Trump's attitude toward crypto has undergone a complete reversal over the past few years.

On November 1, 2024, the 16th anniversary of the Bitcoin white paper's release, Trump tweeted his blessings for Bitcoin and stated that if elected, he would end the Harris administration's crackdown on cryptocurrency, even calling on supporters to help him realize the vision of "Bitcoin made in America." At this point, he was no longer an opponent, nor just a bystander, but a "presidential candidate" advocating for crypto.

One of the most iconic events was his attendance at the Bitcoin 2024 conference in Nashville, where Trump announced that he would become a staunch supporter of cryptocurrency, even clearly understanding the biggest pain points in the crypto community, promising to fire the current SEC chairman Gary Gensler and replace him with a "regulator who understands crypto."

He candidly stated that "opposing crypto is the wrong policy" and that he would make the U.S. a "Bitcoin superpower," hoping to lead the global crypto industry development through a more friendly regulatory environment. He even praised Bitcoin as the core of the modern economy, stating that if Bitcoin were to "moon," he hoped the U.S. could be the leader in that endeavor.

Trump attended the Bitcoin 2024 conference, image source WSJ

In his speech, Trump vigorously positioned himself against the Democratic Party's harsh stance on crypto, especially contrasting himself with Elizabeth Warren, known for her crypto regulation. He also pointed out that if elected, he would create a "Presidential Crypto Advisory Committee," which immediately sparked enthusiastic applause and cheers from the audience. More shockingly, he suggested that Bitcoin's market value could one day surpass gold and publicly criticized the Biden and Harris administration's anti-crypto policies.

During the conference, Trump seemed to undergo a "public awakening," no longer the former president who held a skeptical attitude toward cryptocurrency, but rather a spirited defender of Bitcoin and the free market. The audience was inspired by his change in attitude, viewing him as a "hero" of the crypto community.

Trump attended the Bitcoin 2024 conference, image source The New York Times

Another detail behind this transformation reveals the subtle connection between Trump and cryptocurrency. At the conference, he looked at the crypto supporters in the crowd and mentioned that Bitcoin had risen 3,900% during his previous presidential term, skyrocketing from under $1,000 to over $30,000. His speech not only ignited the crowd but also garnered support from major figures in the Bitcoin industry, such as Elon Musk, the Winklevoss twins, and Marc Andreessen, founder of venture capital giant A16Z, who all expressed their support for his crypto policies.

Beyond Bitcoin itself, Trump has gradually recognized the important role of Bitcoin mining in U.S. energy security and economic sovereignty. In June 2024, he met with executives from several large Bitcoin mining companies in the U.S. and promised to strongly support cryptocurrency mining activities through policy. He even posted on Truth Social that Bitcoin mining is the "last line of defense" against central bank digital currencies (CBDCs) and expressed a desire for "all remaining Bitcoins to be made in America." In Trump's view, Bitcoin mining is not just an economic activity; it symbolizes America's will to resist central banks.

As September approached, Trump purchased a cheeseburger with Bitcoin at PubKey, a Bitcoin-themed bar in New York. This action also pushed the possibility of Bitcoin being pulled back from a financial investment to a daily transaction currency, becoming a symbol of his stance on crypto.

Trump also made bigger promises to the crypto community, publicly stating his intention to retain Bitcoin as a strategic reserve and planning to pardon Ross Ulbricht, who was sentenced to life in prison for operating a darknet platform. Through these radical moves, Trump successfully crafted himself as the "savior" of the crypto community, promising to protect Bitcoin from excessive government regulation and pledging to make the U.S. a global center for cryptocurrency. Related reading: "Reviewing Trump's Commitment to Bitcoin: He Will Fire the SEC Chairman and Never Sell Your Bitcoin."

As the dust settled from the U.S. elections, Trump won the votes in swing states, sweeping both houses and confirming his election as the next U.S. president returning to the White House. Bitcoin could no longer contain its surge. On November 14, according to HTX market data, Bitcoin briefly surpassed $93,000, setting a new historical high.

According to data from the Stand With Crypto website initiated by Coinbase, a total of 247 pro-crypto candidates won seats in the House of Representatives, while only 113 members opposed cryptocurrency. The Stand With Crypto website also showed that the Senate leaned toward supporting cryptocurrency, with 15 supporters and 10 opponents.

Coinbase CEO Brian Armstrong praised the results of this congressional election as a watershed moment for cryptocurrency, writing on Twitter: "Welcome the most pro-crypto new members of Congress in U.S. history."

With a larger number of members in the House of Representatives, representing diversity, they typically initiate legislation, while the smaller, more conservative Senate usually reviews proposals initiated by the House. Since both the House and Senate tend to support cryptocurrency, the path for favorable legislation may be smoother, and crypto insiders are optimistic about the potential for supportive regulation from the U.S. Congress in the future.

Bitcoin has traversed 16 years of remarkable history, with its price climbing from zero to $100,000. This is not only a victory for technological innovation but also a bold attempt by humanity to reconstruct the trust system. From the white paper during the financial crisis to now being a financial giant with a global market value exceeding $2 trillion, Bitcoin has changed our understanding of currency, wealth, and power in an unforeseen way.

Behind all this are the efforts of countless evangelists: early miners, platform founders, and developers who ignited the spark of belief amid uncertainty; as well as ordinary investors who maintained their faith through extreme volatility, navigating bull and bear markets. This revolution, crossing technology, philosophy, and economics, is not just a transfer of wealth but a transformation of ideas.

And the story of Bitcoin is far from over. It continues to evolve, attracting more institutions and individuals to participate, pushing for a new balance between regulation and the market. From Satoshi Nakamoto's original intention to today's brilliance, Bitcoin is not only writing a legendary past but also the prologue to the future. As many supporters firmly believe, Bitcoin is not the end but the starting point for redefining global finance.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。