Original | Odaily Planet Daily (@OdailyChina)

Author | Vincent Fu (@vincent31515173)

In the third quarter of 2024, the primary market investment and financing showed a downward trend.

At the macro level, the Federal Reserve initiated a new round of interest rate cuts after four years, with the first rate cut of 50 basis points in September. As the U.S. presidential election approaches, the cryptocurrency market faces the final crucial point of the year.

Internally in the cryptocurrency market, meme coins have become a new growth point, but still face issues such as weak radiation, short duration, and unpredictability, making it difficult to become a new driving force. A new economic model has yet to emerge.

Affected by various factors, the performance of the primary market declined compared to the previous quarter, with both the number and amount of investment and financing in Q3 lower than the previous quarter.

Looking back at the investment and financing activities in the primary market in Q3, Odaily Planet Daily found:

- The financing situation in Q3 has declined, and Q4 will usher in a crucial turning point;

- The number of financings in Q3 was 272, with a disclosed total amount of financing of $1.813 billion;

- The underlying infrastructure is gradually moving towards a B2B business model;

- The largest single investment amount was $100 million for Celestia;

- Robot Ventures made 22 moves in Q3, ranking first.

Note: Odaily Planet Daily categorizes all projects that disclosed financing in Q1 into 5 major tracks based on business type, target audience, business model, etc.: infrastructure, applications, technology service providers, financial service providers, and other service providers. Each track is further divided into different subcategories, including GameFi, DeFi, NFT, payments, wallets, DAO, Layer1, cross-chain, and others.

The financing situation in Q3 has declined, and Q4 will usher in a crucial turning point

In the previous quarter's report, the view was that the first small peak of the bull market had passed. The primary market financing data in Q3 validates this view's accuracy, and based on the macro trend, it is expected that the cryptocurrency market will reach a crucial turning point in Q4.

From the above chart, it can be seen that the financing in Q3, both in terms of quantity and amount, is not as good as the previous quarter, showing a downward trend, and is close to the starting point of the first small peak of this round of bull market at the end of 2023.

At the same time, the cryptocurrency market also shows a certain degree of retracement in the market, but the subsequent interest rate cuts by the Federal Reserve and the results of the U.S. presidential election have put the cryptocurrency market in a new round of expected upward space.

It can be judged that Q3 is in a stage of overall retracement, and the investment and financing data in Q4 will reflect the later trend of the cryptocurrency market.

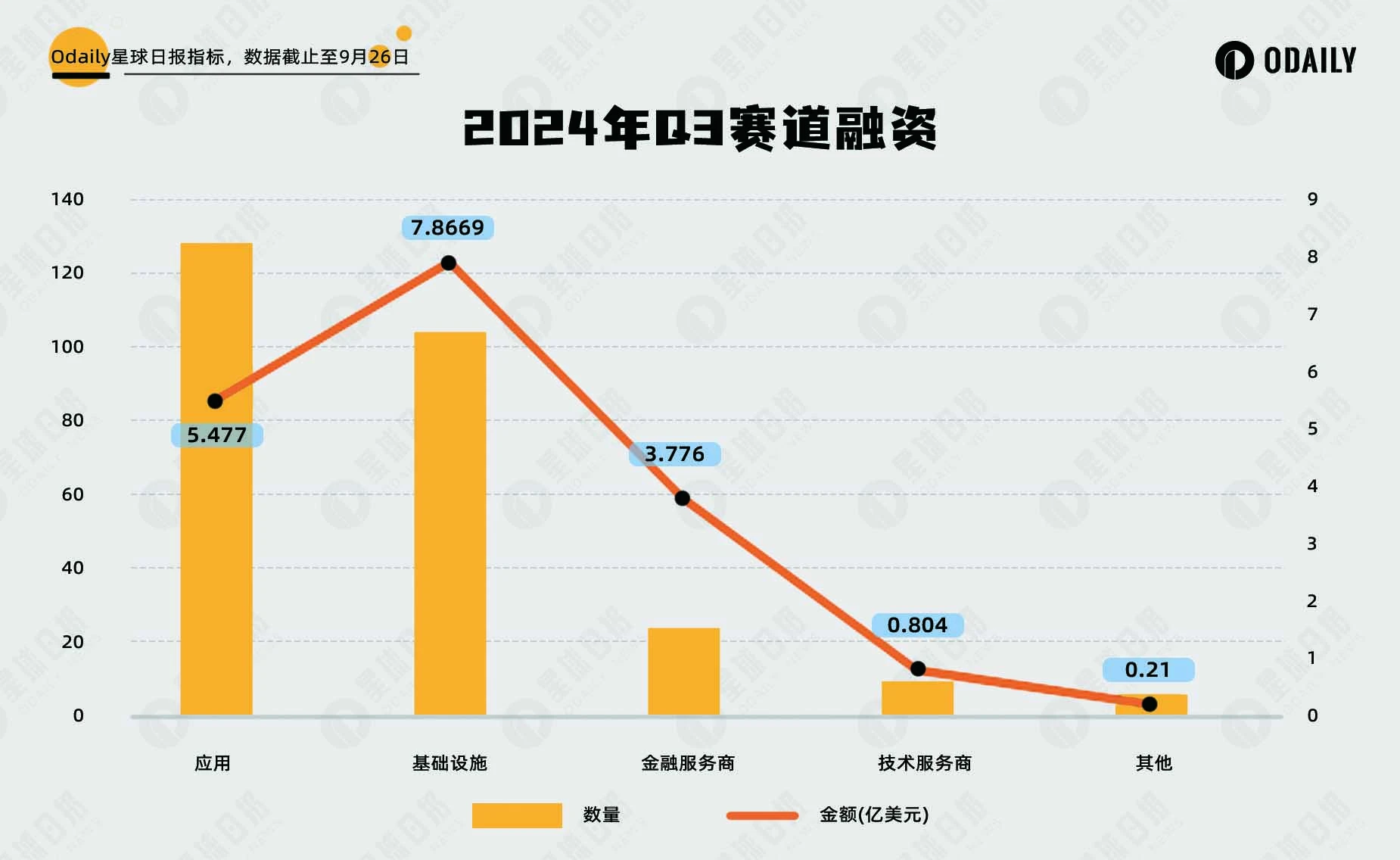

The number of financings in Q3 was 272, with a disclosed total amount of financing of $1.813 billion

According to incomplete statistics from Odaily Planet Daily, from July to September 2024, a total of 272 investment and financing events (excluding fund-raising and mergers and acquisitions) occurred in the global cryptocurrency market, with a disclosed total amount of $1.813 billion, distributed in the tracks of infrastructure, technology service providers, financial service providers, applications, and other service providers. Among them, the application track received the most financing, totaling 128; the infrastructure track received the most financing amount, with a financing amount of $787 million. Both of them still lead in terms of financing amount and quantity.

From the above chart, the financing quantity and amount in each track are basically the same as the previous quarter. The financial service providers have increased in both quantity and amount compared to the previous quarter, possibly due to the accelerated integration of traditional finance and the cryptocurrency industry, attracting attention from capital for digital currency banks in multiple regions and countries.

The underlying infrastructure is gradually moving towards a B2B business model

According to incomplete statistics from Odaily Planet Daily, financing events in Q3 were concentrated in DeFi, underlying infrastructure, and GameFi, accounting for nearly half of the total financing events, with 62 in the DeFi track, 54 in the underlying infrastructure track, and 31 in the GameFi track.

Looking at the distribution of financing in sub-tracks:

DeFi, games, and some AI application sectors rank in the top five in terms of financing quantity. DeFi ranks first, and related financing mostly occurs in new public chain ecosystems or new models, with token launch platforms becoming popular investment projects in the DeFi sector, reflecting the important position of meme coins in the current market; the game sector still attracts the attention of many capital, and games using the Tap to Earn model are about to see a wave of coin launches.

The AI+ sector remains an important target for capital pursuit, with various types of AI projects such as AI tools, AI large language models, and AI+ blockchain receiving high financing amounts and attention. However, most projects are still in the early development stage, and it is unknown when they will go live and whether they can seize the Web2 market.

The underlying infrastructure sector remains hot, with new projects for middleware and modular public chains continuously emerging, mostly optimizing the underlying parts on existing public chains. Furthermore, more underlying projects adopt a B2B business model and do not have a tendency to issue coins.

NFT-related sectors are still in a trough, with no new growth in the past two quarters, and previous blue-chip projects and NFTfi-related platforms have no noteworthy highlights.

The largest single investment amount was $100 million for Celestia

From the above table of the top 10 financing amounts in Q4, it is not difficult to see that large financing projects in the CeFi sector account for one-third, including cross-border payment and settlement blockchain company Partior, global stablecoin payment network Bridge, and the Singapore digital asset exchange SDAX. This to some extent indicates the continuous strengthening of the application of digital currencies in traditional finance within the cryptocurrency market, although the growth of intrinsic value in the current cryptocurrency market is limited, it has greatly improved the external expansion channels of the cryptocurrency market.

As of September 26th this quarter, the largest single financing amount occurred in Celestia, but there are some doubts in the community about this financing, believing that it was deliberately released before a large-scale unlocking of TIA, with the intention of boosting the coin price to facilitate institutions and projects to unload.

In addition, the open-source artificial intelligence development platform Sentient is also worth paying attention to. Sentient is built on Polygon and radiates the EVM ecosystem led by Ethereum, incentivizing contributors to collectively build, replicate, and expand AI models, and rewarding contributors.

Robot Ventures made 22 moves in Q3, ranking first

Institutions were more cautious in Q3 compared to the previous quarter: Robot Ventures made 22 moves, ranking first; OKX Ventures and Binance Labs made 16 moves, tying for second place; Animoca Brands made 14 moves, ranking third, followed by Spartan Group, a16z, and Polychain, all making 10 moves or more.

Among the projects invested by the above institutions, except for Animoca Brands focusing on the gaming sector, the investment proportion of the other institutions is dominated by infrastructure, followed closely by DeFi, which generally conforms to the overall distribution of various tracks in the previous subcategories.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。