The stability of the stablecoin market in Japan is mainly due to the establishment of a clear regulatory framework. Government support and the policies of the ruling Liberal Democratic Party have further accelerated the development of the Web3 industry. In contrast to the uncertain or restrictive positions of many countries towards stablecoins, Japan's positive and open attitude stands out. Therefore, people are optimistic about the future of the Web3 market in Japan. This article will explore the current regulatory status of stablecoins in Japan and analyze the potential impact of stablecoins supported by the yen.

I. Regulatory Promotion of Japan's Stablecoin Market

In June 2022, Japan laid the foundation for amending the Payment Services Act (PSA) and established a regulatory framework for stablecoin issuance and brokerage. These amendments were officially implemented in June 2023, marking the formal start of stablecoin issuance. The new law provides a detailed definition of stablecoins, specifies the issuing entities, and sets out the licenses required for related businesses.

1. Definition of Stablecoins

According to the revised Payment Services Act, stablecoins are classified as "electronic payment instruments" (EPI) and can be used to pay for goods or services to an unspecified number of recipients.

However, not all stablecoins fall into this category. According to Article 5, Paragraph 1, Item 5 of the revised PSA, only stablecoins backed by legal tender are considered electronic payment instruments. This means that stablecoins based on cryptocurrencies such as Bitcoin or Ethereum (e.g., MakerDAO's DAI) are not considered electronic payment instruments. This distinction is an important feature of Japan's regulatory framework.

(Source: Tiger Research)

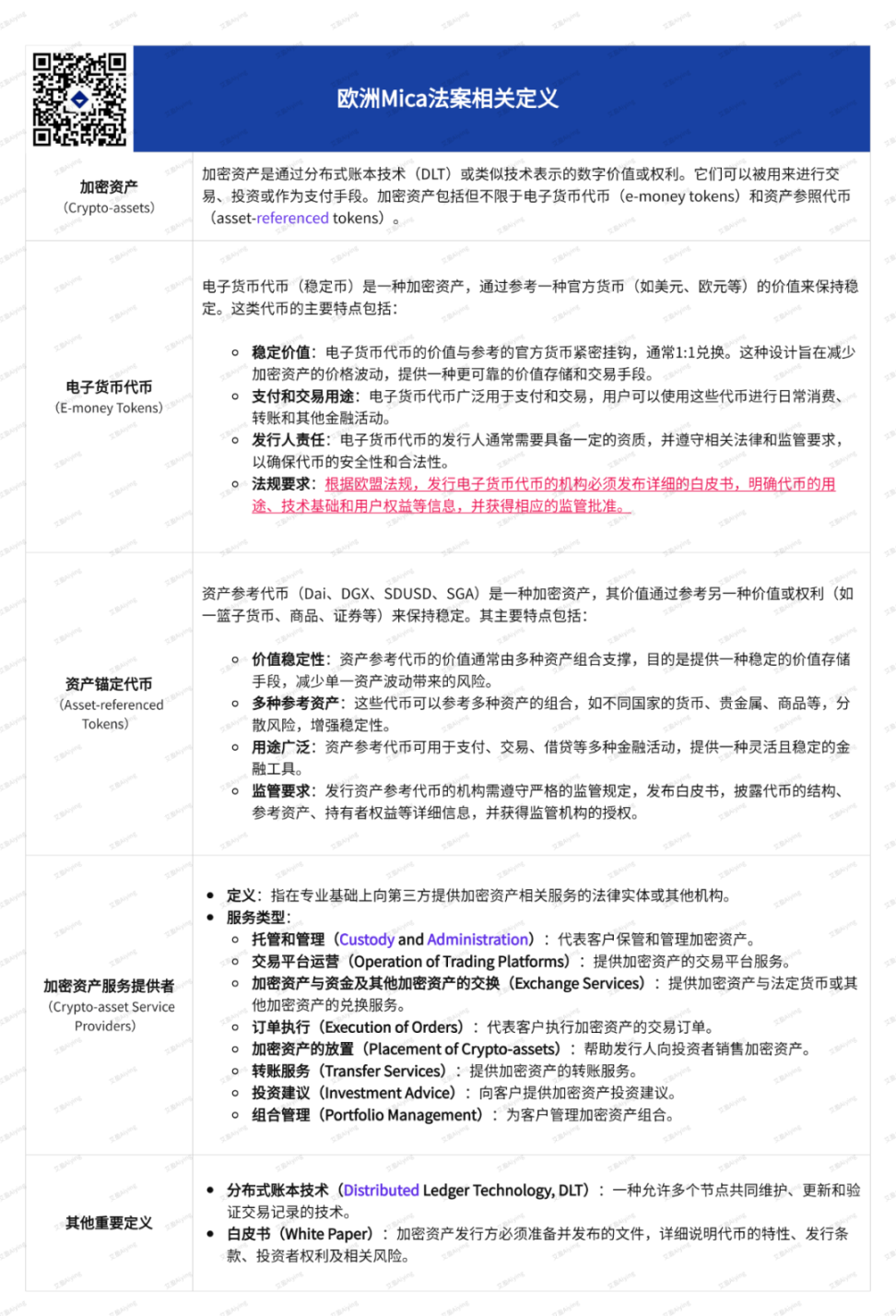

Aiying's Addition: Japan's classification of stablecoins is somewhat similar to the European MICA regulation. Stablecoins backed by legal tender are classified as "E-money Tokens" under MICA, while stablecoins anchored to assets like DAI are "Asset-referenced Tokens." For more details, refer to the report "European MiCA Regulation: Comprehensive Analysis of Its Far-reaching Impact on the Web3 Industry, DeFi, Stablecoins, and ICO Projects"

2. Issuing Entities of Stablecoins

According to the revised PSA, stablecoins can only be issued by three types of entities:

- Banks

- Funds transfer service providers

- Trust companies

Each type of entity has functional differences in stablecoin issuance, such as transfer limits and recipient restrictions.

Among them, stablecoins issued by trust companies are the most noteworthy because they are expected to best fit Japan's current regulatory environment and are very similar in characteristics to common stablecoins like USDT and USDC.

Stablecoins issued by banks will be subject to some restrictions. Due to the need to maintain the stability of the financial system, regulatory authorities have indicated that stablecoins issued by banks need careful consideration and may require further legislation.

Funds transfer service providers are also subject to some limitations, with a maximum transfer amount of 1 million yen per transaction, and it is currently unclear whether transfers can be made without Know Your Customer (KYC) verification. Therefore, these stablecoins may require further regulatory updates. Given these conditions, stablecoins issued by trust companies are the most likely form to emerge.

3. Stablecoin-Related Licenses

To engage in stablecoin-related businesses in Japan, entities must register as Electronic Payment Instrument Service Providers (EPISP) and obtain the relevant licenses. This requirement was introduced after the revision of the Payment Services Act in June 2023. Stablecoin-related businesses include buying, selling, exchanging, brokering, or acting as agents for stablecoins. For example, virtual asset exchanges that support stablecoin trading or custody wallet services for managing stablecoins for others all need to be registered. In addition, these businesses must also comply with user protection and anti-money laundering (AML) requirements.

II. Yen-Supported Stablecoins

With the improvement of Japan's stablecoin regulatory framework, multiple projects are actively researching and testing yen-supported stablecoins. The following introduces several major stablecoin projects in Japan to help understand the current status and characteristics of the yen stablecoin ecosystem.

1. JPYC: Prepaid Payment Instrument

JPYC is Japan's first digital asset issuer pegged to the yen, established in January 2021. However, JPYC is currently classified as a prepaid payment instrument rather than the electronic payment instrument defined after the revision of the Payment Services Act, and therefore is not considered a stablecoin. JPYC has usage restrictions, such as only supporting the conversion of legal tender to JPYC (top-up), but not the conversion of JPYC back to legal tender, similar to a rechargeable card, which to some extent limits its use cases.

However, JPYC is actively working to issue stablecoins that comply with the new law, planning to issue fund transfer stablecoins by obtaining a fund transfer license and expanding their use, such as exchanging with Tochika issued by Hokkoku Bank.

In addition, JPYC also plans to register as an EPISP to operate stablecoin businesses. In the long term, the company also plans to issue and operate trust-type stablecoins based on Progmat Coin to support cash or bank deposit-related business activities.

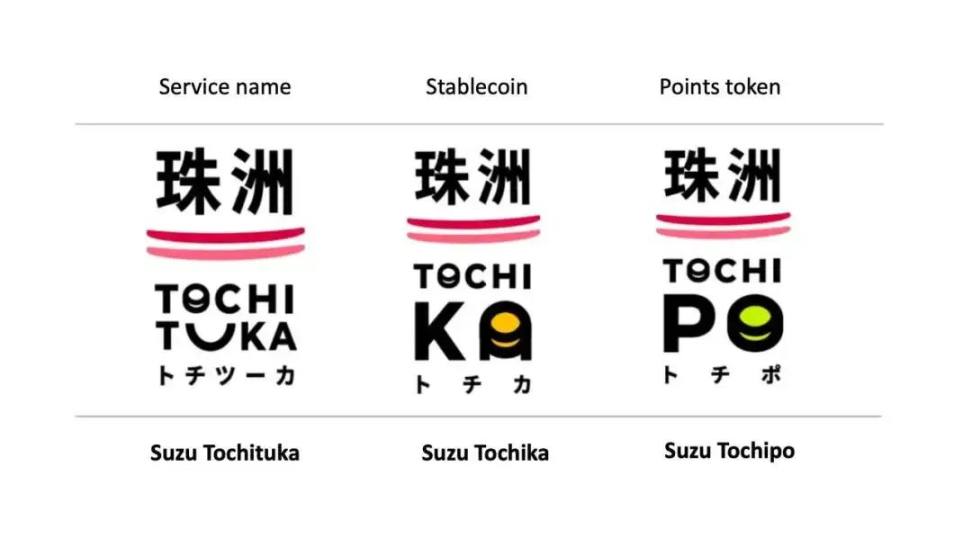

2. Tochika: Deposit-Supported Digital Currency

Tochika is Japan's first digital currency supported by bank deposits, launched by Hokkoku Bank in 2024. Tochika is supported by bank deposits, and users can easily access it through the "Tochika" app and use it at cooperating merchants in Ishikawa Prefecture.

Tochika is characterized by its simplicity and low merchant fees of only 0.5%. However, it is currently limited to use within Ishikawa Prefecture, with only one free cash withdrawal opportunity per month. After exceeding this limit, a fee of 110 Tochika (equivalent to 110 yen) will be charged. Additionally, Tochika operates on a private blockchain, limiting its scope of use.

In the future, Tochika plans to expand its services, including linking accounts with other financial institutions, expanding its geographical coverage, and introducing peer-to-peer remittance functionality.

3. GYEN: Offshore Stablecoin

GYEN is a yen stablecoin issued by GMO Trust, a subsidiary of the Japanese GMO Internet Group based in New York. It is regulated by the New York State Department of Financial Services and is on the state's green list. GYEN is pegged to the yen at a 1:1 ratio, but because it is not issued by a Japanese trust company, it cannot circulate domestically in Japan.

However, GYEN may be included in Japan's regulatory framework in the future as part of compliant stablecoins.

Is the Stablecoin Business Really Feasible?

Despite stablecoins being legally recognized for over a year, stablecoin projects in Japan have made limited progress. Stablecoin projects similar to USDT or USDC are still scarce in the Japanese market, and no company has completed EPISP registration.

Furthermore, the requirement for stablecoin issuers to manage all reserve funds as demand deposits poses a significant limitation on commercial operations. Demand deposits can be withdrawn at any time and offer thin profits, making it difficult to generate revenue for stablecoin businesses. Although Japanese banks recently raised interest rates from 0%, the 0.25% short-term rate is still low, weakening the profitability of stablecoin businesses. Therefore, there is a growing demand in the market for competitive stablecoins supported by assets such as Japanese government bonds.

Despite these challenges, large financial institutions and corporate groups in Japan are actively involved in the stablecoin business, including major banks such as Mitsubishi UFJ Bank (MUFG), Mizuho Bank, Sumitomo Mitsui Banking Corporation (SMBC), as well as companies like Sony and DMM Group.

Conclusion

Data Source: Financial Times, Refinitiv

In recent years, Japan has been working to address the issue of a weak yen and has implemented various strategies to enhance its competitiveness. Stablecoins are part of this effort, as an attempt to enhance the scale and competitiveness of the yen. By adopting advanced stablecoins, it is expected that Japan can not only apply them domestically but also explore new use cases in the global payment field, providing new opportunities for Japan to expand its influence in the international financial market.

Source: rwa.xyz

Despite the establishment of a regulatory framework for stablecoins for some time, the influence of the yen in the stablecoin market remains limited. There are few actual use cases for stablecoins, and no company has completed EPISP registration. The declining approval ratings of the Kishida Cabinet and the Liberal Democratic Party also make it difficult to push forward strong Web3-related policies. Nevertheless, establishing a regulatory framework is a meaningful step. While progress may be slow, the anticipated changes are worth looking forward to.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。