Can unsecured credit lending agreements thrive in the DeFi world?

Author: Rainy Sleep

The market's concerns about such agreements are mainly focused on the repayment ability of the borrowers. In simple terms, it is about whether the project can recover the money lent out—only then will users be more willing to put their money into financial management, and the project can generate fees.

Only by addressing the above issues can such projects truly achieve sustainable development.

The solutions are nothing more than the following two directions:

- Maximizing the assurance that borrowers can repay their loans

- Providing corresponding guarantees/insurance for depositors

So when we look at these projects, we need to focus on these two points. I mentioned $MPL $CPOOL in my August and September outlooks, and next week I will write another article about these two projects.

Today, let's first talk about @humafinance, a project in the same field that just announced a $38 million financing, and take a look at its solutions and new expansions on the product side.

1/ Recently released financing information⬇️

Huma Finance recently completed a $38 million financing, including $10 million in equity investment and $28 million in income-type RWA. The financing was led by Distributed Global, with participation from Hashkey Capital, Folius Ventures, Stellar Development Foundation, and TIBAS Ventures, the risk investment department of Turkey's largest private bank, İşbank.

Huma Finance plans to use this financing to deploy its PayFi product on the Solana and Stellar chains.

Next, I will share my understanding of the project as concisely as possible.

2/ Huma Finance v1

Huma Finance v1 is an unsecured lending platform for enterprises and individuals, focusing on the potential future income of the borrowers—when borrowers borrow money, it mainly examines the borrowers' future income cash flow.

In the words of the official Mirror, "Income and earnings are the most important factors in underwriting, as they have a high predictability for repayment capacity."

To better advance its vertical business, Huma completed a merger with Arf this year. Arf is a liquidity and settlement platform focused on cross-border payments, supported by Circle (also in cooperation with Solana and Stellar).

After the merger, Huma is responsible for the user deposit part, and Arf is responsible for lending to the Web2 world + collecting interest, forming a sustainable cycle. (We can see on its official website that the default rate so far is 0%)

3/ PayFi

Huma v2 is an extension of v1. In addition to lending, Huma hopes to expand its business to the PayFi field.

What is PayFi?

"PayFi" was proposed by Lily Liu, chairman of the Solana Foundation (also an investor in Huma Finance). PayFi refers to a new financial market created around the Time Value of Money. The time value of money refers to the higher value of a certain amount of money currently held compared to an equivalent amount of money to be received in the future. This is because this money has the potential to generate income, such as earning interest on loans, or earning returns on US Treasury bonds, and completing transactions and transfers at lower costs in a shorter time.

Therefore, PayFi is also one of the sub-routes of RWA. (This should also be the reason why Huma Finance considers deploying it on Solana)

However, although it is RWA, the income from PayFi often comes from areas such as transaction fees, cross-border payments, and loan interest, unlike RWA assets constructed through US Treasury bond returns. For example, Arf will use Web3 liquidity to provide cross-border transfer services for licensed financial institutions at the T1 and T2 levels in developed countries (which can be understood as bridge funding).

After the interest rate cut in the United States, with more adoption, PayFi may become a mainstream sub-route leading the development of RWA. Huma is one of the first projects to enter the PayFi field, and it has also received favor from VC/core circles supporting PayFi (just look at the lineup of investors).

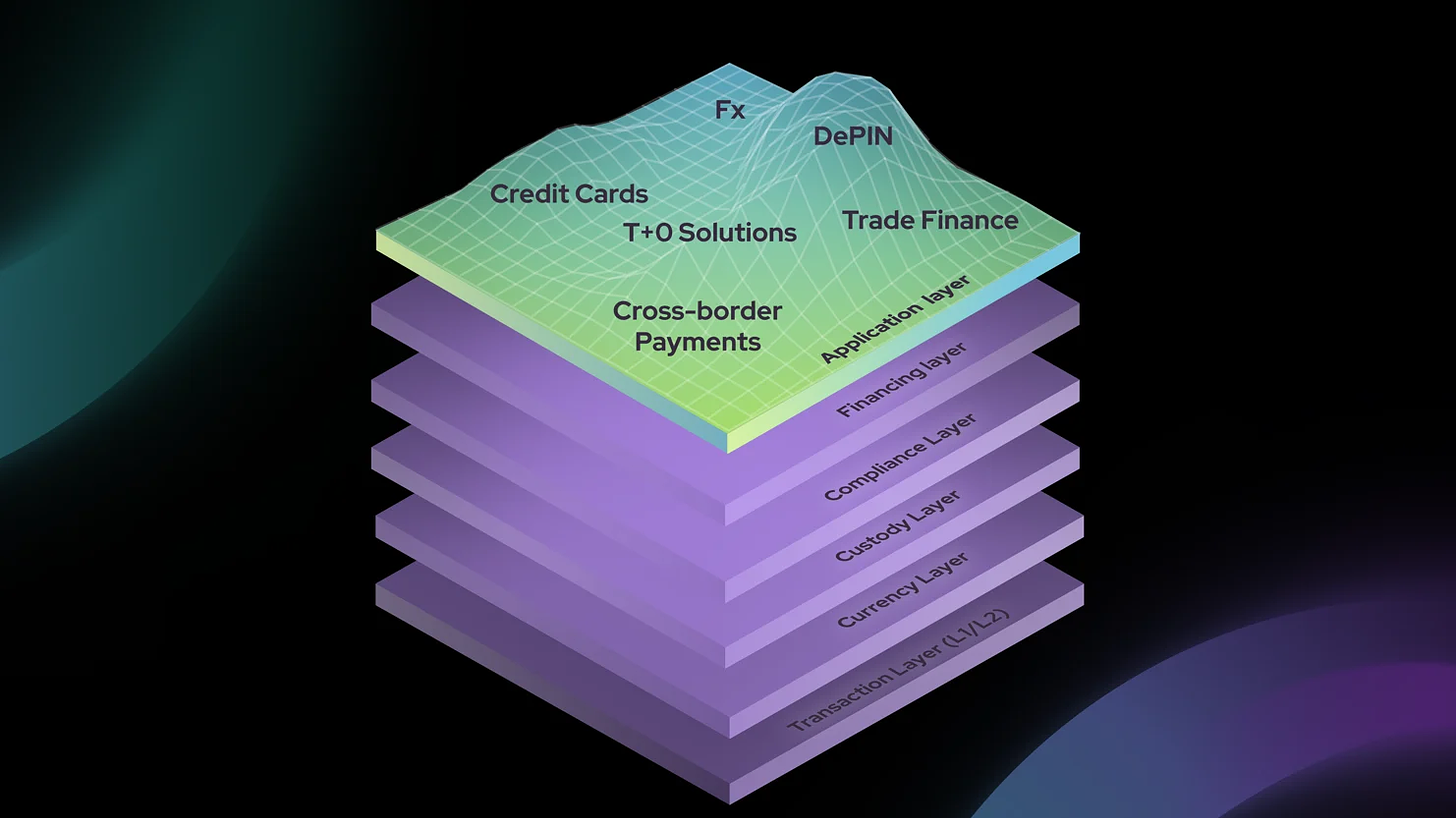

At the same time, in order to become a core infrastructure provider in the PayFi field, Huma has launched PayFi Stack to meet the needs of the PayFi route in terms of transactions, currency, custody, financing, compliance, and application construction.

4/ Huma Finance v2

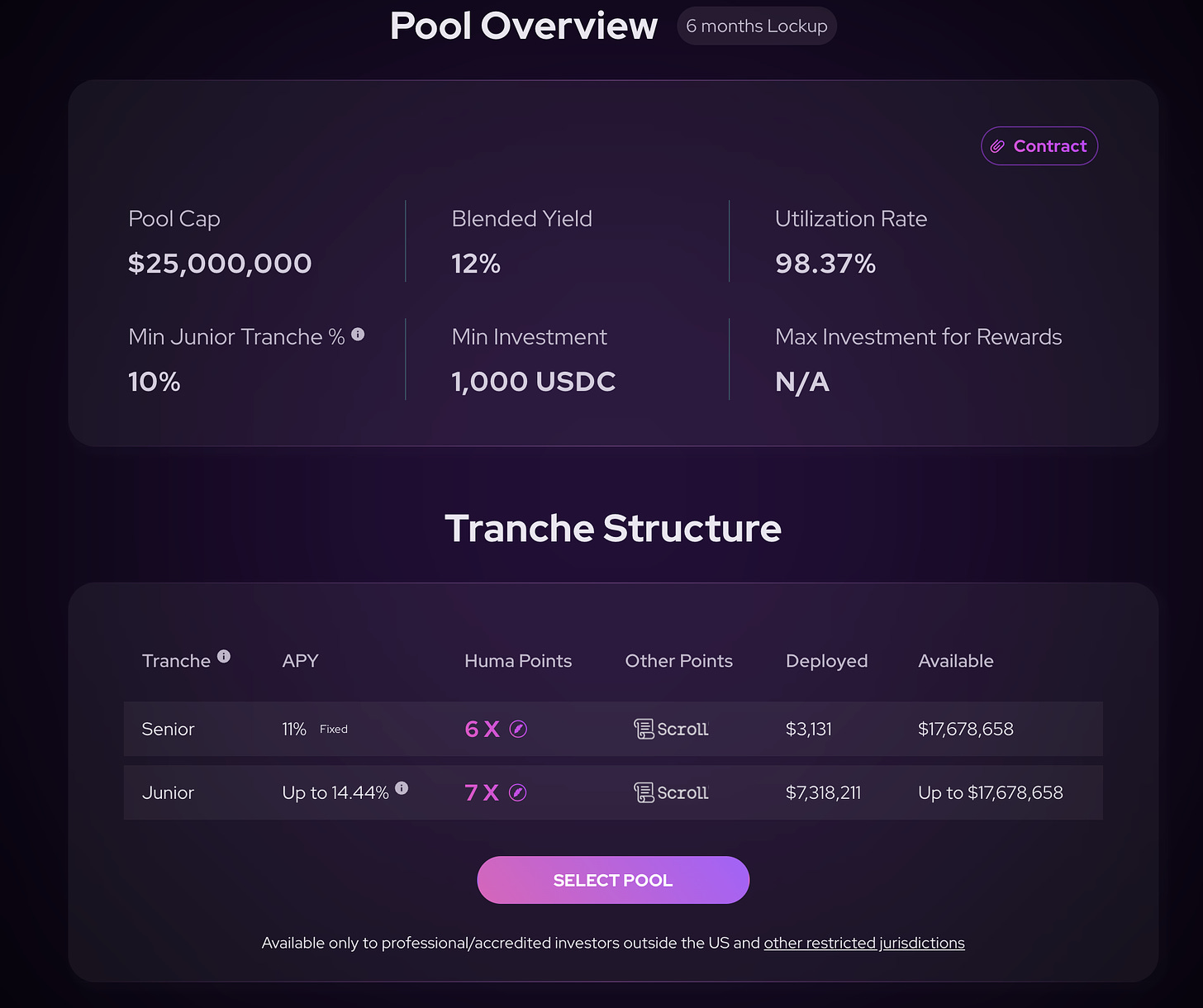

On the product side, v2 has implemented a more complex product structure, such as adding features like Senior Tranche, Junior Tranche, and First Loss Cover that we will mention below. In simple terms, this upgrade subdivides the functions to meet the needs of different users.

Huma v2's Pool is divided into Senior and Junior Pools. The Senior Pool has a fixed interest rate, and the Junior Pool has a floating interest rate, which depends on the real-time income of the project.

The cost of the higher floating interest rate of the Junior Pool is that it needs to bear corresponding losses when bad debts occur. From a product perspective, I personally think that in the future, the project may need to subsidize depositors of the Junior Pool through tokens or other forms of incentives—after all, the Junior Pool is the security module of the product.

5/ How does Arf handle the liquidity provided by investors?

After we deposit money into the Huma Finance Arf Pool, these assets will be held by Arf in a bankruptcy-isolated SPV (special purpose vehicle, a legal entity created for a specific or temporary purpose, mainly for risk isolation).

Arf Financial GmbH, as the service provider, provides services to the SPV. Lending, cross-border payments, trade settlement, and risk management are carried out here. After a transaction is completed, the SPV will return the money and profits from the pool to the chain. Arf Financial GmbH does not have control over the corresponding pool funds.

6/ Fill in the gaps

Here I will add two points:

- Circle's official website has a very detailed introduction to Arf: https://www.circle.com/en/case-studies/arf

Arf has done well in risk control, but this has also led to some issues, such as the need for KYC before depositing, which is not friendly to many DeFi players. Also, I personally feel that Huma Finance's UI/UX still has room for improvement.

- Collaboration with Scroll

Currently, we can deposit USDC into Huma through Scroll, achieving a triple benefit—10%+ financial income + Huma points + Scroll points.

7/ Conclusion

Why have I been looking at such financial products recently? It's because after clearing out my assets some time ago, most of the assets in my hands are U, so I want to find a good place for these U to be managed.

From my personal perspective, before the market shows a potential upward trend, I will not be fully invested or leveraged, at most I will do some short-term trading.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。