Original Author: Charles Yu

Original Translation: Luffy, Foresight News

Key Points

The Bitcoin spot ETF (launched on January 11, 2024) has accumulated a net inflow of $15.1 billion as of June 15, 2024.

Nine issuers are preparing to launch 10 Ethereum spot ETFs in the United States.

The U.S. Securities and Exchange Commission (SEC) approved all 19b-4 filings on May 23, and these ETFs are expected to start trading in July 2024.

Similar to the Bitcoin ETF, we believe that the main source of net inflows is independent investment advisors or investment advisors associated with banks, brokers/traders.

We expect the net inflow of the first 5 months of the Ethereum ETF to account for 20-50% of the net inflow of the same period of the Bitcoin ETF. Our estimated target is 30%, which means a monthly net inflow of $1 billion.

Overall, we believe that the price sensitivity of ETHUSD to ETF inflows is higher than BTC, as a large part of the total supply of ETH is locked in staking, cross-chain bridges, and smart contracts, with fewer held by centralized exchanges.

For months, observers and analysts have underestimated the possibility of the U.S. Securities and Exchange Commission (SEC) approving spot Ethereum exchange-traded products (ETP). Pessimism stemmed from the SEC's reluctance to explicitly acknowledge ETH as a commodity, the lack of news of contact between the SEC and potential issuers, and the SEC's investigation and enforcement actions related to the Ethereum ecosystem. Bloomberg analysts Eric Balchunas and James Seyffart had estimated a 25% chance of approval in May. However, on Monday, May 20, Bloomberg analysts suddenly raised the likelihood of approval to 75% due to reports that the SEC had contacted stock exchanges.

In fact, later that week, all applications for spot Ethereum ETPs were approved by the SEC. We expect these instruments to be truly launched after the effectiveness of the S-1 application (we expect this to happen at some point in the summer of 2024). This report will reference the performance of the Bitcoin spot ETP to predict the demand after the launch of the Ethereum ETP. We estimate that the spot Ethereum ETP will achieve approximately $5 billion in net inflows in the first five months of trading (about 30% of the net inflow of the Bitcoin ETP).

Background

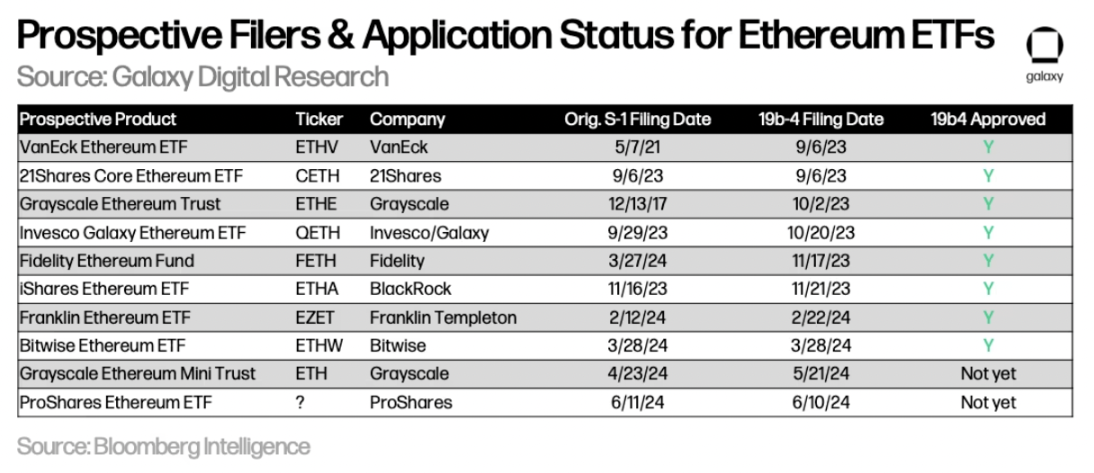

Currently, 9 issuers are competing to launch 10 spot ETH exchange-traded products (ETP). In the past few weeks, some issuers have already withdrawn. ARK chose not to collaborate with 21Shares to launch an Ethereum ETP, while Valkyrie, Hashdex, and WisdomTree have withdrawn their applications. The following chart shows the current status of applicants sorted by the 19b-4 application date:

Grayscale is seeking to convert the Grayscale Ethereum Trust (ETHE) into an ETP, just as the company did with its Grayscale Bitcoin Investment Trust (GBTC), but Grayscale has also applied for a "mini" version of the Ethereum ETP.

On May 23, the U.S. Securities and Exchange Commission approved all 19b-4 filings (allowing rule changes for stock exchanges to finally list ETH spot ETPs), but now each issuer needs to have repeated discussions with regulatory agencies about their registration statements. The products themselves can only truly start trading after the U.S. Securities and Exchange Commission allows these S-1 filings (or ETHE's S-3 filings) to take effect. Based on our research and Bloomberg's reports, we believe that the spot Ethereum ETP may start trading as early as the week of July 11, 2024.

Experience of Bitcoin ETF

The launch of the Bitcoin ETF has been nearly 6 months, serving as a benchmark for predicting the potential popularity of the Ethereum spot ETF.

Source: Bloomberg

Here are some observations from the first few months of trading for the Bitcoin spot ETP:

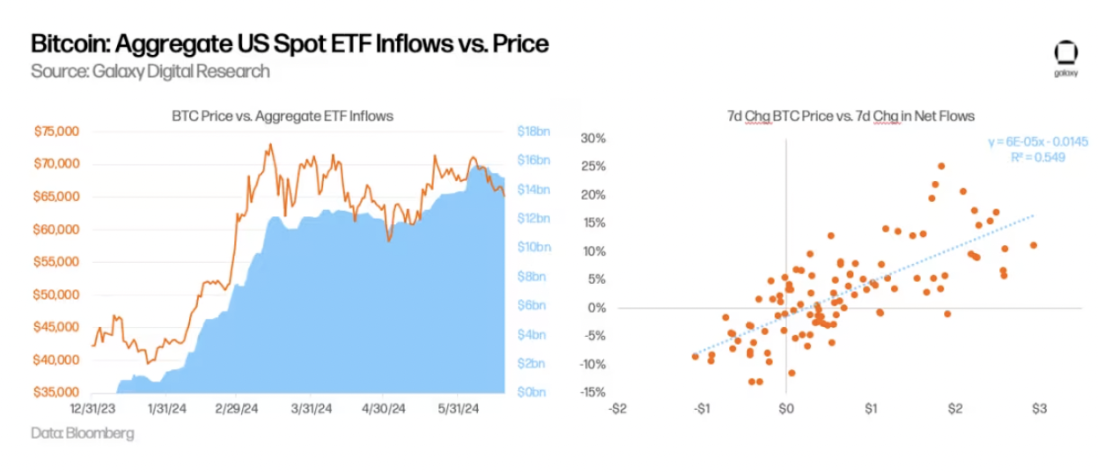

So far, the inflow of funds has been on the rise. As of June 15, the cumulative net inflow of the U.S. spot Bitcoin ETF since its launch has exceeded $15 billion, with an average daily net inflow of $136 million. These ETFs hold approximately 870,000 BTC, accounting for 4.4% of the current supply of BTC. The BTC trading price is approximately $66,000, and the total AUM of all U.S. spot ETFs is approximately $58 billion (Note: Before the ETF was launched, GBTC held approximately 619,000 BTC).

ETF inflows are partly responsible for the rise in BTC prices. By regressing the 1-week change in BTC price and net inflows of the ETF, we calculated an r-squared of 0.55, indicating a high correlation between these two variables. Interestingly, we also found that price changes are leading indicators of inflows, rather than the other way around.

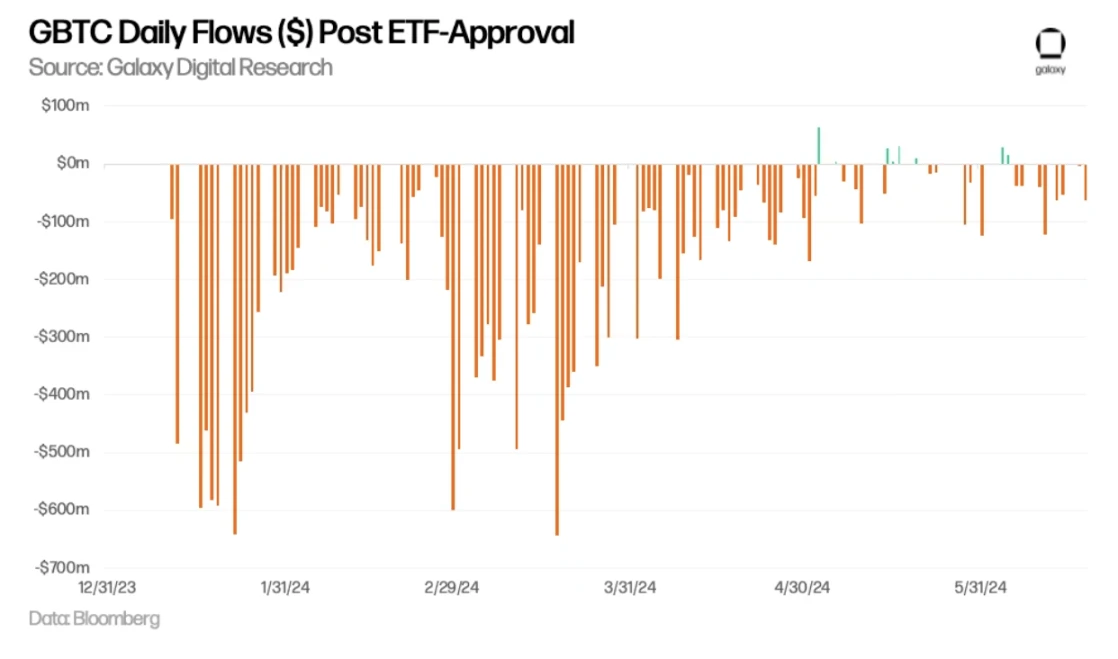

GBTC has been a major drag on the overall flow of the ETF. Since the trust was converted into an ETF, GBTC experienced a large outflow of funds in the first few months. The daily outflow of funds from GBTC peaked in mid-March, reaching $642 million on March 18, 2024. Subsequently, the outflow of funds eased, and GBTC even saw several days of positive net inflows starting in May. As of June 15, since the launch of the ETF, the balance of BTC held by GBTC has decreased from 619,000 to 278,000.

ETF demand is mainly driven by retail investors, and institutional demand is rebounding. 13F filings show that as of March 31, 2024, over 900 U.S. investment companies held Bitcoin ETFs with a value of approximately $11 billion, accounting for about 20% of the total holdings of Bitcoin ETFs, indicating that most of the demand is driven by retail investors. The list of institutional buyers includes major banks (such as JPMorgan, Morgan Stanley, and Wells Fargo), hedge funds (such as Millennium, Point72, Citadel), and even pension funds (such as the Wisconsin Investment Board).

Wealth management platforms have not yet started purchasing Bitcoin ETFs for clients. The largest wealth management platforms have not allowed their brokers to recommend Bitcoin ETFs, but reportedly, Morgan Stanley is exploring allowing its brokers to solicit clients to purchase them. In our report "Market Size of Bitcoin ETF," we wrote that it may take several years for wealth management platforms (including broker-dealers, banks, and RIAs) to help clients purchase Bitcoin ETFs. So far, inflows from wealth management platforms have been minimal, but we believe it will be an important catalyst for Bitcoin adoption in the near to medium term.

GBTC Daily Liquidity After ETF Approval (USD)

Estimating Potential Inflows of Ethereum ETF

Referring to the situation of Bitcoin ETP, we can roughly estimate the potential demand for Ethereum ETP in the market.

Relative Market Size of BTC and ETH ETPs

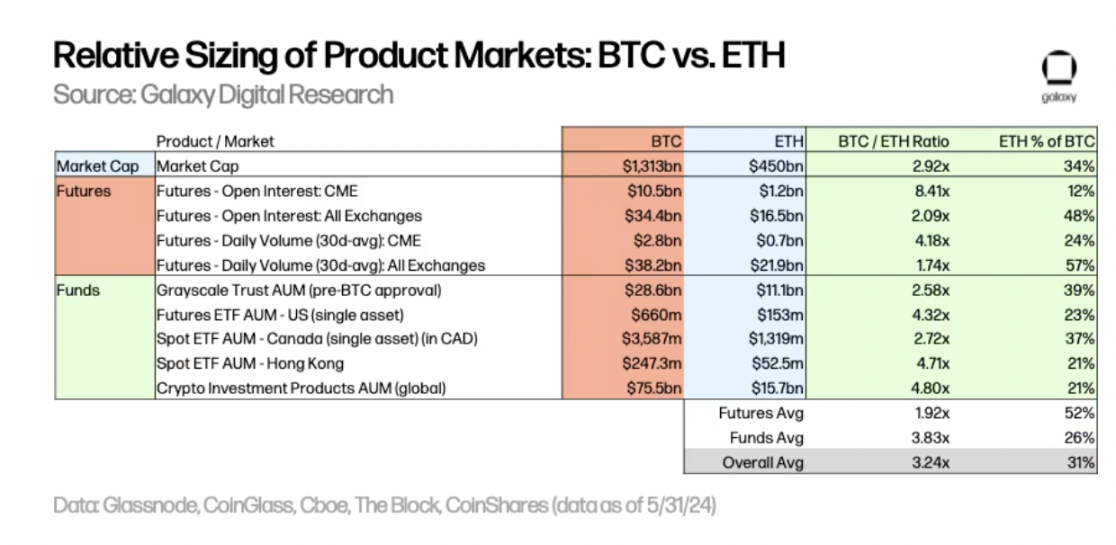

To estimate the potential inflows of the Ethereum ETF, we applied the BTC/ETH multiple to the inflows of the U.S. Bitcoin spot ETF, based on the relative asset sizes of BTC and ETH traded across multiple markets. As of May 31:

The market value of BTC is 2.9 times that of ETH.

Across all exchanges, based on open interest levels and trading volumes, the futures market for BTC is approximately 2 times that of ETH. Specifically at CME, the open interest for BTC is 8.4 times that of ETH, and the daily trading volume for BTC is 4.2 times that of ETH.

The AUM of various funds (categorized by Grayscale Trust, futures, spot, and selected global markets) shows that the scale of BTC funds is 2.6 to 5.3 times that of ETH funds.

Based on the above, we believe that the inflow of the Ethereum spot ETF will be approximately one-third of the inflow of the Bitcoin spot ETF (estimated range 20%-50%).

Applying this data to the $15 billion inflow of the Bitcoin spot ETF before June 15, implies that in the first five months after the launch of the Ethereum ETF, the monthly inflow of funds will be approximately $1 billion (estimated range: $600 million to $1.5 billion per month).

Estimated Inflows of the U.S. Spot Ethereum ETF

We see some valuations lower than our forecast due to several factors. Nevertheless, our previous report estimated the first-year inflow of the Bitcoin ETF to be $14 billion, assuming entry of wealth management platforms, but there was already a significant inflow into the Bitcoin ETF before these platforms entered. Therefore, we recommend caution in predicting subdued demand for the Ethereum ETF.

Some structural/market differences between BTC and ETH will affect ETF flows:

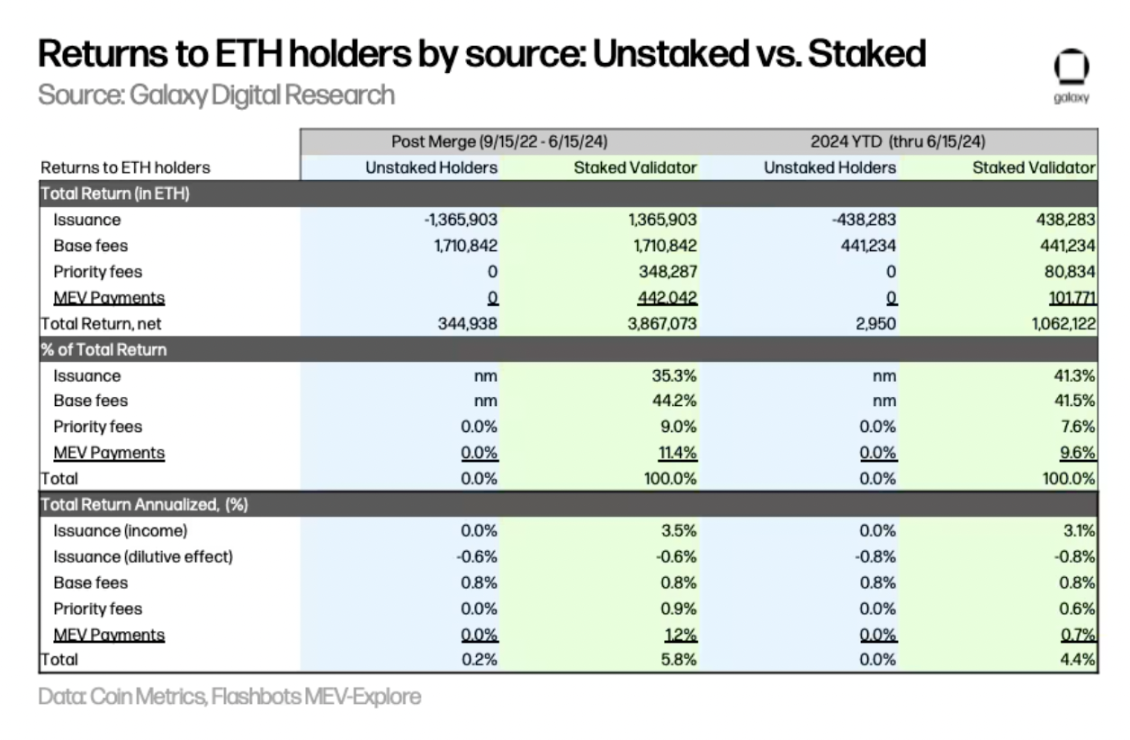

Lack of staking rewards may impact the demand for the spot Ethereum ETF. Non-staked ETH has an opportunity cost of forgoing (i) inflation rewards paid to validators, (ii) priority fees paid to validators, and MEV income paid to validators through relayers. Based on data from September 15, 2022, to June 15, 2024, we estimate the annualized opportunity cost of forgoing staking rewards for spot ETH holders to be 5.6% (if using year-to-date data, the result is 4.4%), which is a significant difference. This will reduce the attractiveness of the spot Ethereum ETF to potential buyers. Note that ETPs offered outside the U.S. (e.g., in Canada) provide additional income to holders through staking.

Sources of Income for Non-Staked and Staked ETH Holders

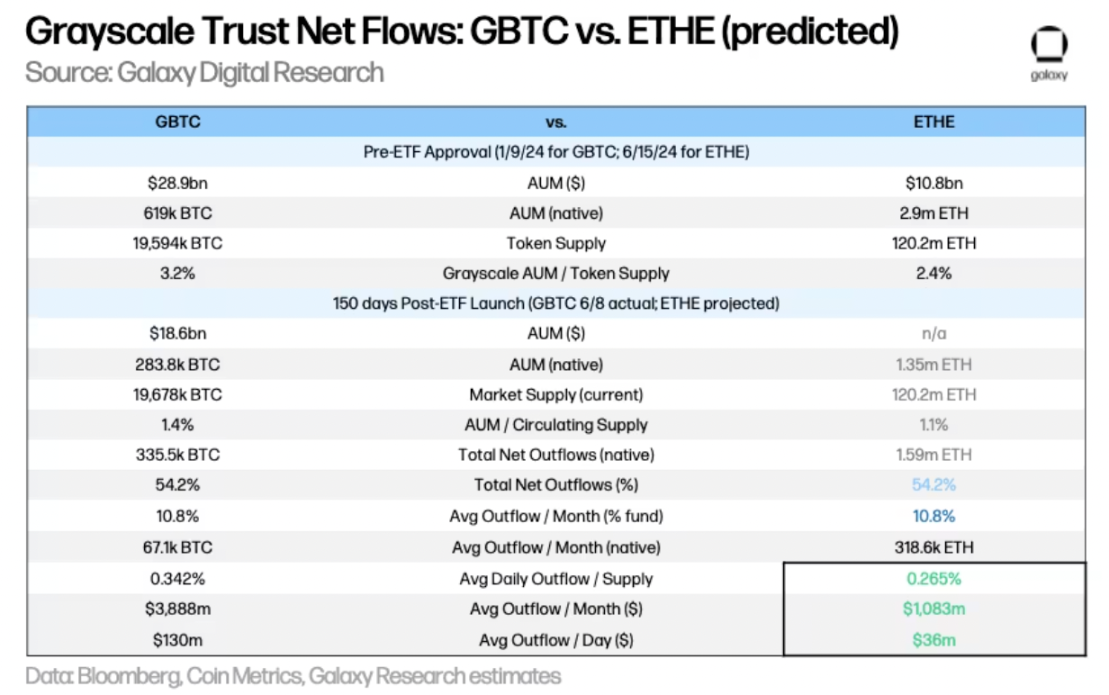

Grayscale's ETHE may drag down the inflows of the Ethereum ETF. Just as the GBTC Grayscale Trust experienced a significant outflow of funds during the ETF conversion, the conversion of the ETHE Grayscale Trust into an ETF will also result in outflows. Assuming the outflow rate of ETHE matches that of GBTC in the first 150 days (i.e., 54.2% of the trust supply is withdrawn), we estimate that the outflow of ETHE will be approximately 319,000 ETH per month, which at the current price of $3,400, will amount to approximately $1.1 billion per month or an average daily outflow of $36 million. Note that the percentage of tokens held by these trusts as a proportion of the total supply is: BTC 3.2%, ETH 2.4%. This indicates that the pressure on the price of ETH from the ETHE ETF conversion is less than that of GBTC. Additionally, unlike GBTC, ETHE will not face forced selling due to bankruptcy cases (e.g., 3AC or Genesis), further supporting the view that the selling pressure related to Grayscale Trusts on ETH will be relatively less than that on BTC.

Net Flows of GBTC and ETHE (Projected)

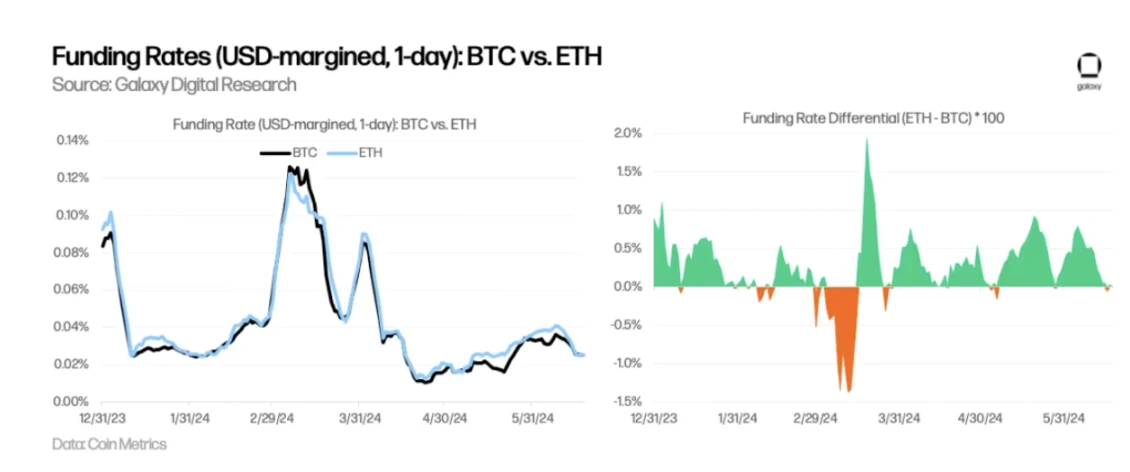

Basis trading may drive demand for the Bitcoin ETF from hedge funds. Basis trading may drive demand for the Bitcoin ETF from hedge funds looking to arbitrage the differences between the spot and futures prices of Bitcoin. As mentioned earlier, 13F filings show that as of March 31, 2024, over 900 U.S. investment companies held Bitcoin ETFs, including some well-known hedge funds such as Millennium and Schonfeld. Throughout 2024, the financing rate for ETH on various exchanges has been on average higher than that of BTC, indicating (i) relatively greater demand for longing ETH, and (ii) the potential for the spot Ethereum ETF to bring more demand from hedge funds utilizing basis trading.

Financing Rates for BTC and ETH

Factors Affecting Price Sensitivity of ETH and BTC

Since we estimate that the ratio of the inflows of the Ethereum ETF to market value is roughly equal to the ratio of Bitcoin flows to market value, we expect the price impact to be roughly similar under all other conditions being equal. However, there are several key differences in the supply and demand of these two assets, which may lead to Ethereum's price being more sensitive to ETF flows:

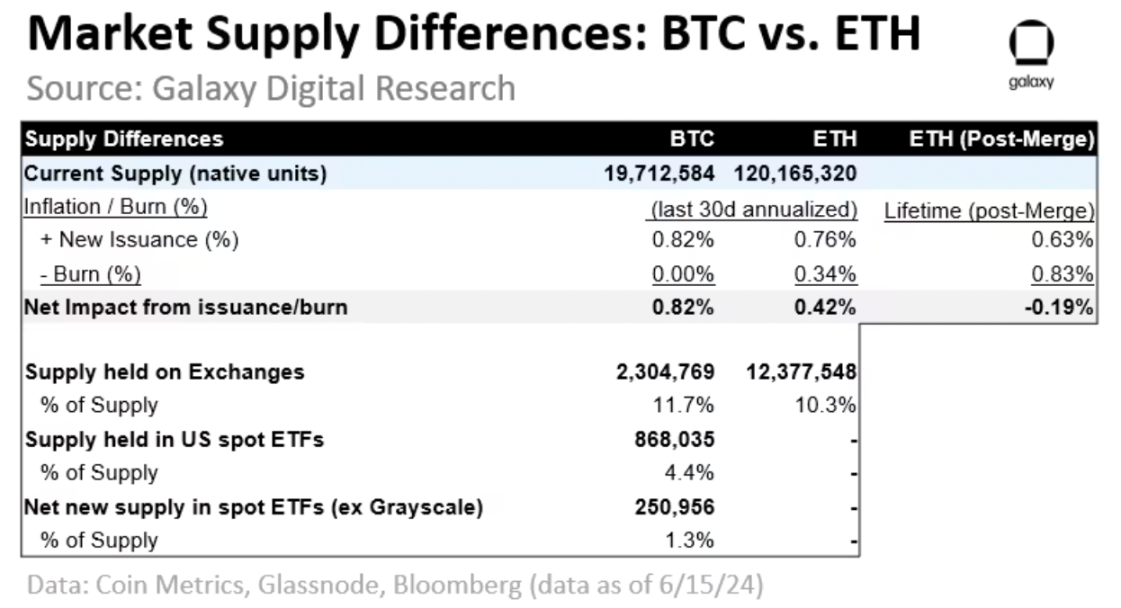

Market Supply Differences Between BTC and ETH

Exchange-held supply: Currently, the proportion of BTC held by exchanges is greater than ETH (11.7% vs. 10.3%), indicating that ETH supply may be tighter, and assuming inflows are proportional to market value, the price sensitivity of ETH will be higher (Note: This metric heavily depends on exchange address attribution and varies greatly between different data providers).

Inflation and burn: Following the latest halving on April 20, 2024, BTC's annual inflation rate is approximately 0.8%. After the Ethereum merge, ETH has experienced net negative issuance (annualized -0.19%) as the new issuance paid to stakers (+0.63%) has been offset by the burned base fees (-0.83%). In the past month, the base fees for ETH have been relatively low (annualized -0.34%), failing to offset the new issuance (annualized +0.76%), resulting in a net positive annualized inflation rate of +0.42%.

ETF-held supply: Since its launch, the net amount of BTC entering the U.S. spot ETF (excluding the initial balance of GBTC) totals 251,000 BTC, accounting for 1.3% of the current supply. If calculated on an annual basis, the ETF will absorb 583,000 BTC, accounting for 3.0% of the current BTC supply, far exceeding the dilution brought by mining rewards (0.81% inflation rate).

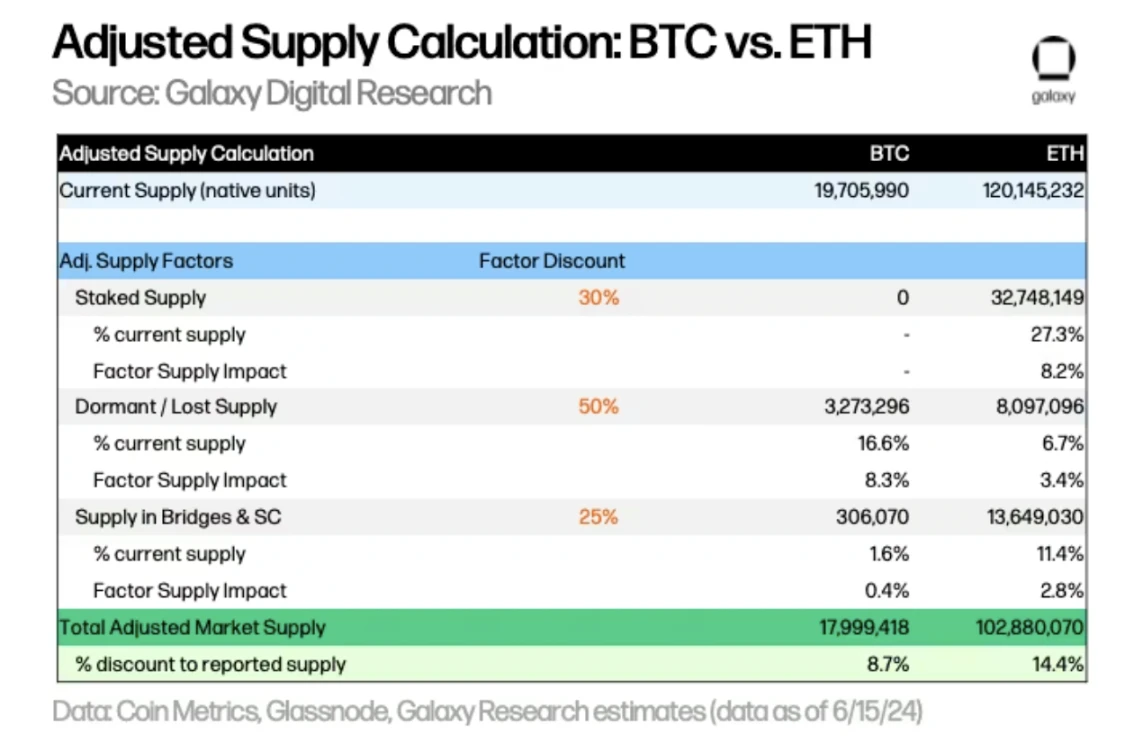

However, the actual market liquidity available for purchase is much lower than the reported current supply. We believe that a better representation of the available market supply for each asset held by the ETF would include adjustments for staked supply, dormant/lost supply, and supply held in cross-chain bridges and smart contracts:

Adjusted Supply Calculation for BTC and ETH

Staked supply (discount: 30%): Staking reduces the amount of tokens available for ETF purchase. Currently, Bitcoin does not have staking functionality. Ethereum requires staking of ETH to secure the network, but stakers can unstake some ETH for other purposes. Currently, the amount of staked ETH accounts for approximately 27% of the current ETH supply, and we apply a 30% discount to estimate the available market supply, resulting in an 8.2% supply discount.

Dormant/lost supply (discount: 50%): Some BTC and ETH are considered unrecoverable (e.g., lost keys, shipwrecks), reducing the available supply. We use BTC addresses dormant for over 10 years and ETH addresses dormant for over 7 years, accounting for 16.6% and 6.7% of the current BTC and ETH supply, respectively. We apply a 50% discount to this balance, as some of the supply held in dormant addresses may come back online at any time.

Supply in cross-chain bridges and smart contracts (discount: 25%): This is the supply locked in cross-chain bridges and contracts for productive purposes. BitGo holds approximately 153,000 BTC in wrapped BTC (wBTC), and we estimate a similar amount locked in other cross-chain bridges, totaling approximately 1.6% of the BTC supply. The ETH locked in smart contracts accounts for 11.4% of the current supply. We apply a discount lower than the staked supply, i.e., 25%, as we assume this supply is more liquid than staked supply (i.e., possibly not subject to the same locking requirements and withdrawal queue restrictions).

Applying discount weights for each factor to calculate the adjusted supply for BTC and ETH, we estimate that the available supply for BTC and ETH is 8.7% and 14.4% less than the reported current supply, respectively.

Overall, we believe that the price sensitivity of ETH weighted against relative market value inflows should be higher than that of BTC, due to: (i) lower available market supply based on adjusted supply factors, (ii) lower percentage of supply held by exchanges, and (iii) lower inflation rates. Each of these factors should have a multiplier effect on price sensitivity (rather than an additive effect), with prices tending to be more sensitive to significant changes in market supply and liquidity.

Outlook for the Future

Looking ahead, we still face several questions regarding adoption and second-order effects:

How should allocators view BTC and ETH? Will existing holders shift from Bitcoin ETF to ETH? For allocators, some rebalancing is expected. Will the spot Ethereum ETF attract new buyers who have not yet purchased BTC? What will the potential buyers' portfolios look like? Will they hold only BTC, only ETH, or both?

When can staking be added? Does the lack of staking rewards affect the adoption of the spot Ethereum ETF? Will the demand for investments in DeFi, tokenization, NFTs, and other crypto-related applications further increase the adoption of the Ethereum ETF?

What potential impact does this have on other altcoins? Are we more likely to see approval for ETFs of other altcoins after Ethereum?

Overall, we believe that the launch of the spot Ethereum ETF will have a significantly positive impact on the adoption of Ethereum and the broader cryptocurrency market, primarily for two reasons: (i) expanding the reach of cryptocurrencies and (ii) gaining greater recognition for cryptocurrencies through formal recognition by regulatory agencies and trusted financial service brands. ETFs can expand the coverage of retail and institutional investors, provide broader distribution through more investment channels, and support Ethereum for a wider range of investment strategies in portfolios. Additionally, further understanding of Ethereum by financial professionals will accelerate investment and adoption.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。