Original Author: Will Awang (X: @Will_7th)

Original Source: Web3小律

When we talk about RWA, we tend to focus more on underlying assets such as US Treasuries, fixed income, and securities. In fact, apart from stablecoins, the largest RWA projects in terms of asset size are money market funds. The top three projects by asset size are: Franklin Templeton: $312 million (government bonds); followed by Centrifuge: $247 million (asset collateral); Ondo Finance: $183 million (government bonds).

Franklin Templeton is a completely tokenized fund, Ondo Finance also has two tokenized funds, and Centrifuge has also established tokenized funds in its RWA project in collaboration with Aave. This shows the importance of tokenized funds in connecting TradFi and DeFi. We believe that funds, as an asset form, are the best carrier for RWA assets due to (1) their regulation and (2) their relatively standardized digital representation.

Currently, when we talk about RWA, we are more focused on the one-sided demand for value capture from the real world by Crypto (or DeFi). However, from the perspective of traditional finance TradFi, after funds are tokenized through blockchain and distributed ledger technology, they can unlock even greater value.

Therefore, this article will gradually analyze the value of funds after tokenization and the active exploration and practice of market participants through the cases observed in the current market.

I. Tokenization of Funds

Tokenization refers to the digital representation of assets on the blockchain and the use of the advantages of distributed ledger technology for accounting and settlement. The assets that can be tokenized not only include financial instruments such as stocks, bonds, and funds, but also tangible assets such as real estate, as well as intangible assets such as music streaming media copyrights. The tokens generated after the tokenization of assets are the carriers of asset value and the certificates of asset rights.

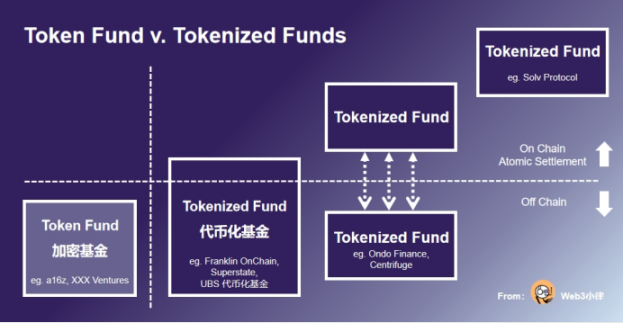

This innovation and disruption also apply to funds. After funds are tokenized, tokenized funds refer to fund shares recorded in digital token form on the blockchain distributed ledger, and the tokens are available for secondary market trading. This type of tokenized fund differs from encrypted funds that only invest in primary and secondary markets (Token Fund).

The global asset management industry is facing many challenges. Although the overall asset management scale of the industry is growing with the rise of the market, fund management fees are being compressed due to peer competition and the industry's shift to passive investment strategies. In addition to investment pressure, the market also has higher requirements for the digital capabilities of funds to meet the increasingly growing online distribution, asset reporting, regulatory compliance, and personalized needs of investors. The growth rate of fund management costs is faster than income, and fund profit margins are being squeezed.

For private equity funds, due to their poor liquidity and high investment thresholds, their investors have long been limited to a small number of institutional investors. The private equity fund market urgently needs to lower the investment threshold and launch alternative products that can meet the investment needs of non-institutional clients such as small and medium-sized institutions, family offices, and even high-net-worth individuals through appropriate product design.

The tokenization of funds can solve many problems in the global asset management industry. Advocates of tokenized funds firmly believe that in the future, funds based on blockchain and distributed ledger technology can not only increase the assets under management (AuM) of funds and invest in a wider range of asset categories (diversity of RWA tokenized assets); they can also attract new categories of investors (investors from unbanked regions in Asia and Africa investing in encrypted assets), improve user investment experience (KYC embedded in smart contracts), help funds win in the competition of industrial digitalization upgrade (digital upgrade), and greatly reduce their operating and marketing costs (advantages of blockchain and distributed ledger).

II. Tokenization Will Bring Profound Impact to the Fund Market

2.1 Tokenization Helps Promote the Digitization of the Fund Market

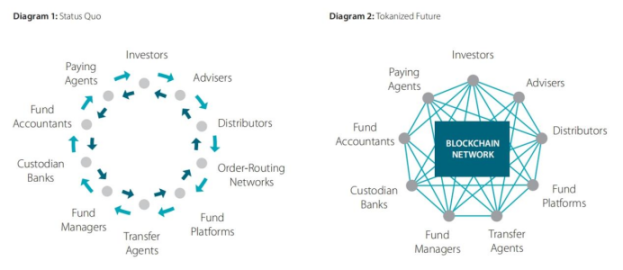

Currently, funds and investors are separated by a large number of intermediaries. Fund distribution includes: financial advisors, fund platforms, and order-routing networks; fund services include: paying agents, custodian banks, and fund accountants.

Transfer agents assist funds by coordinating both ends, responsible for customer (KYC), anti-money laundering (AML), combating the financing of terrorism (CFT), and economic sanctions screening and verification, settlement of fund subscriptions and redemptions, reporting to managers, and maintaining investor registration records.

(Source: SS&C, Tokenization of Funds - Mapping a Way Forward)

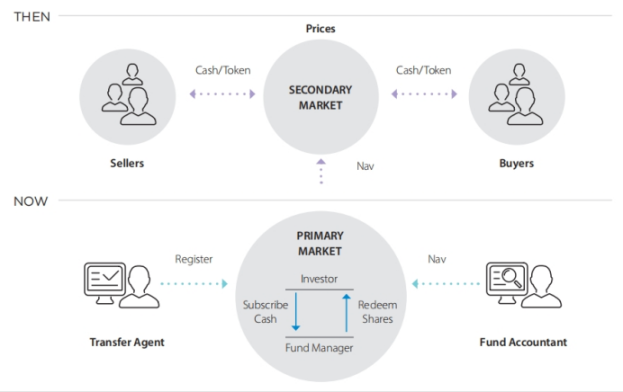

The operational process of traditional funds is fundamentally inefficient: (1) Fund shares are established to meet subscriptions and canceled to meet redemptions; (2) Fund pricing is not based on buying and selling, but on the net asset value set by the fund accountant; (3) Transfer agents settle orders based on the net asset value, integrate orders, and settle orders in a centralized register through posting, then reconcile orders with investors and fund cash positions; (4) Three days before the release of fund shares and cash settlement, funds and investors face market fluctuations and counterparty risks; (5) Fund liquidity also forces fund managers to retain cash positions to bear the cost of rebalancing the fund's net asset value.

In contrast, tokenization can greatly simplify the above complex processes: (1) When tokenized funds are issued and traded on the blockchain, the subscription and redemption process will be settled directly into investors' accounts (e-wallets) through fund tokens and payment-type tokens, with finality of settlement, thereby eliminating market and counterparty risks; (2) Because all transactions are recorded on the blockchain distributed ledger, any change in ownership will be automatically recorded, thereby eliminating the need for centralized registration; (3) Since all intermediaries can access and view data on the blockchain, there is no need for multiple reports and reconciliations.

At the same time, tokenization will help digitize the interaction between fund managers and investors: (1) With integrated KYC, AML, CFT, and economic sanctions screening and verification, the speed of investor account opening will increase; (2) Based on the more efficient atomic settlement of the blockchain, achieve real-time pricing and settlement 24/7; (3) Access to a unified ledger by multiple parties can achieve real-time data sharing, and investors can directly access fund data and trade; (4) Fund managers will gain richer investor information and transaction information.

2.2 Solv Protocol's On-Chain Fund Issuance and Fundraising Platform

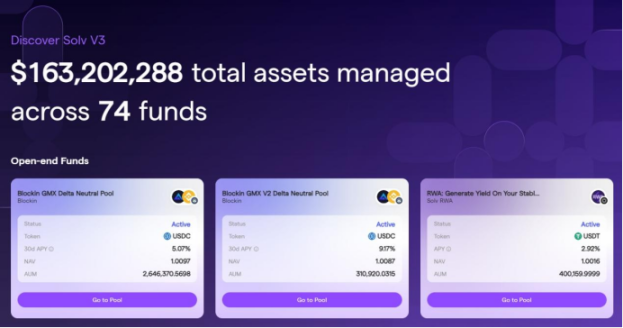

Established in 2020, Solv Protocol is dedicated to providing blockchain-based financial instruments and diversified asset management infrastructure for the crypto industry, and recently completed a $6 million financing. Solv Protocol's latest product, Solv V3, sets a new standard for on-chain fund issuance. Tokenized funds created through Solv Protocol can achieve efficient fund circulation through on-chain fundraising, issuance, subscription, redemption, trading, and settlement.

We have seen on the official website that Solv Protocol has already implemented the issuance and fundraising of 74 tokenized funds (including open-end funds and closed-end funds), serving over 25,000 investors and managing over $160 million in assets.

(Source: app.solv.finance/earn)

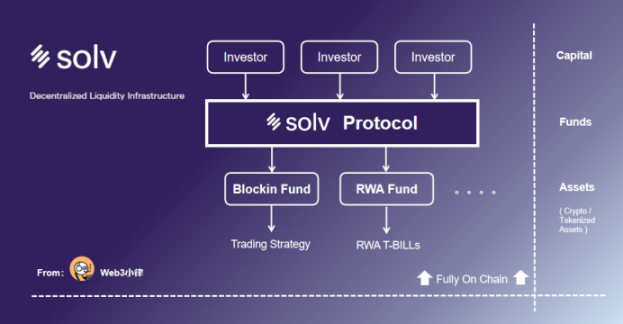

The core mechanism of Solv Protocol allows fund managers to create on-chain funds, deposit raised funds (stablecoins, BTC, ETH, etc.) into Solv Protocol's smart contracts, and generate NFT/SFT certificates representing fund shares for investors, enabling fund managers to invest according to their own investment strategies with the raised funds.

For example, we see that Blockin GMX Delta Neutral Pool is an open-end fund managing approximately $2.6 million in assets, based on the investment strategy of fund manager Blockin. Additionally, another open-end fund, RWA: Generate Yield On Your Stable Coins, initiated by fund manager Solv RWA, raises USDT stablecoins and invests in US Treasury RWA assets to provide interest income on stablecoins for holders.

Open-end funds refer to funds where the total size of fund units or shares is not fixed when the fund is established, and the fund can issue shares at any time and allow investors to redeem them regularly. Fund managers with high liquidity investment portfolios typically use an open-end company structure to establish funds.

Funds issued entirely on the blockchain through Solv Protocol raise funds in the form of BTC/ETH/stablecoins and invest in native encrypted assets or tokenized assets (such as US Treasury RWA). This fully on-chain tokenized fund structure can maximize the value brought by tokenization. For example, Solv Protocol's tokenized funds can (1) allow fund managers to directly interact with investors and obtain more investor data and trading information; (2) eliminate many frictions of fund service intermediaries, reducing costs; (3) achieve fundraising, issuance, trading, and settlement of tokenized funds through the blockchain, recorded in a distributed ledger, efficient and transparent; (4) real-time updates of the fund's net asset value (NAV), and subscription/redemption of fund shares anytime, anywhere 24/7, and many other advantages.

Solv Protocol states: Currently, most crypto asset management services come from CeFi institutions, and the opaque asset creation and fund management processes of these institutions have caused trust issues. Providing a transparent and secure investment experience with better decentralized solutions, while helping asset management companies gain trust and liquidity. Solv is building infrastructure and an ecosystem, providing comprehensive services including creation, issuance, marketing, and risk management. This reduces barriers to participating in Web3 while promoting the maturity of the crypto market.

Olivier Deng, an investor at Solv Protocol from Nomura Securities, said: "Solv has built a trustless institutional-grade DeFi platform, integrating brokers, underwriters, market makers, and custodians, creating the first liquidity financial infrastructure bridging DeFi, CeFi, and TradFi on the blockchain."

III. Settlement of Tokenized Funds

Tokenized funds can to some extent replace some intermediaries (such as fund distributors) and enhance the digitization level of the fund market, but the market is not built in a day. For fund managers and investors, the most realistic change brought about by tokenization is the settlement of fund subscriptions and redemptions.

3.1 Settlement of Tokenized Funds

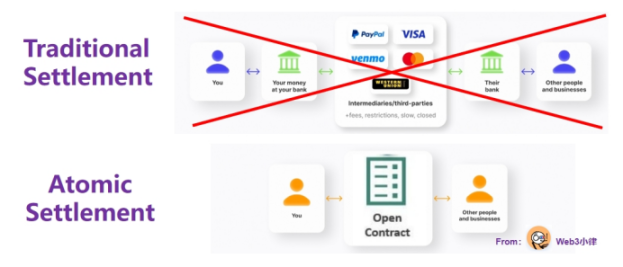

Currently, funds are generally priced based on net asset value, and fund managers settle subscriptions and redemptions through the banking system by paying or receiving cash three days later (T+3). However, tokenized funds calculate prices multiple times a day, and since subscriptions and redemptions will be "automatically" settled on the blockchain, the settlement method based on the banking system (T+3) will be replaced. We can see in the case of Solv Protocol that fully on-chain tokenized funds can achieve real-time pricing and settlement in a 24/7 market.

This settlement method using blockchain and distributed ledger technology is called Atomic Settlement, which means that the transaction of cash equivalents and fund shares is directly linked, i.e., when one asset transfer occurs, the transfer of the other asset occurs simultaneously. In other words, the prerequisite for settlement is that there is cash and fund shares available for exchange in the buyer's and seller's e-wallets, and settlement ultimately depends on simultaneous exchange. If cash or shares are not delivered, the transaction will not occur. This settlement method not only eliminates counterparty risk but also enables real-time settlement, greatly improving transaction efficiency.

Bitcoin was designed from the beginning to achieve a decentralized peer-to-peer electronic cash payment system. Bitcoin payments allow direct transfers between users without the need for third-party institutions such as banks, clearinghouses, and electronic payment platforms, avoiding high fees and cumbersome transfer processes. This atomic settlement method applied to cross-border payments can solve problems such as high fees, low efficiency of cross-border transfers, and high costs in traditional cross-border payments.

Another interesting use case is the more effective settlement of exchange-traded funds (ETFs) through tokenization. Because ETFs are redeemed and subscribed through physical means, tokenizing the underlying securities (a basket of securities in the ETF) can greatly simplify the settlement process of the underlying securities of the ETF and achieve real-time settlement.

3.2 Use Cases of Settlement for Tokenized Funds

This atomic settlement trading method has been approved by the US SEC and is being applied to the Franklin OnChain U.S. Government Money Fund, which has reached an asset size of $310 million. Additionally, we see a similar pilot project for tokenized funds by UBS in Singapore. Although these funds are not purely on-chain tokenized funds, they leverage the advantages of blockchain and distributed ledger technology for accounting and settlement, creating a tokenized fund model.

3.2.1 Franklin OnChain U.S. Government Money Fund

We see that Franklin Templeton launched the Franklin OnChain U.S. Government Money Fund (FOBXX) in 2021, the first fund in the US approved by the SEC to use Stellar blockchain technology to process transactions and record ownership of tokenized funds. In April of this year, it expanded to Polygon and may later be issued on the Avalanche and Aptos blockchains, as well as the Ethereum Layer 2 solution Arbitrum.

As of now, its assets under management have exceeded $310 million, and investors can enjoy an annualized return of 5.19%. One share of the fund is represented by one BENJI token, and we have not yet seen BENJI tokens interact with DeFi protocols on the blockchain. Investors need to undergo compliance verification through Franklin Templeton's app or website to enter its whitelist, meeting the compliance requirements of KYC/AML/CTF.

Franklin Templeton's digital asset manager stated, "We believe that blockchain technology has the potential to reshape the asset management industry, providing greater transparency and lower operational costs for traditional financial products. Blockchains like Stellar are crucial for the future of asset management, and tokenized assets built on blockchains will ultimately interoperate with other parts of the crypto asset ecosystem." It is reported that the overall cost of Franklin's tokenized fund is only 1/10 of traditional fund costs.

3.2.2 Compound Founder's Superstate Fund

Fund managers with extensive DeFi experience will leverage the advantages of blockchain and distributed ledger technology. For example, Compound founder Robert Leshner announced on June 28, 2023, the establishment of a new company, Superstate, dedicated to bringing regulated financial products from traditional financial markets to the blockchain.

According to documents submitted by Superstate to the U.S. Securities and Exchange Commission (SEC), Superstate will use Ethereum as a supplementary accounting and settlement tool and create a fund investing in short-term government bonds, including U.S. Treasury bonds and government agency securities. In short, Superstate will establish an SEC-compliant fund off-chain to invest in short-term U.S. government bonds and use the Ethereum blockchain for fund accounting, settlement, and tracking ownership shares. Superstate will implement an investor whitelist system, so fund tokens cannot be used in DeFi protocols like Uniswap or Compound.

In a statement to Blockworks, Superstate stated, "We are creating an SEC-compliant investment product that will allow investors to obtain ownership certificates of traditional financial products, just like holding stablecoins and other crypto assets."

Although Superstate did not mention composability with DeFi, it is conceivable that Superstate fund tokens could be pledged in Compound's lending pools to borrow stablecoins for DeFi building blocks.

3.2.3 UBS Tokenized Fund Pilot

(Source: UBS Asset Management launches first blockchain-native tokenized VCC fund pilot in Singapore)

On October 2, 2023, UBS Asset Management announced the launch of a tokenized fund pilot project. Through UBS's internal tokenization service (UBS Tokenize), fund tokens appear on the Ethereum blockchain in the form of smart contracts, representing ownership of underlying money market funds. Tokenization can help improve the issuance, distribution, subscription, and redemption processes of funds.

The project is part of a broader Variable Capital Company (VCC) umbrella initiative led by the Monetary Authority of Singapore -- "Project Guardian," aimed at tokenizing various real-world assets. For UBS, the project is part of its global distributed ledger technology strategy, focusing on using public and private blockchain networks to enhance fund issuance and distribution. In November 2022, UBS launched the world's first publicly traded tokenized bond. In December 2022, UBS issued $50 million in tokenized fixed-rate notes, and in June 2023, issued $200 million in tokenized structured notes for a third-party issuer.

The project lead stated, "This is a key milestone in understanding fund tokenization, based on UBS's expertise in tokenizing bonds and structured products. Through this exploratory initiative, we will collaborate with traditional financial institutions and fintech providers to help improve market liquidity and customer market access."

3.3 Technical Challenges of Tokenized Fund Settlement

Tokenization represents a significant change in the settlement method of funds, replacing the current reliance on transfer agents to record subscriptions and redemptions in the fund holder register for settlement. This atomic settlement method, similar to cash transactions, eliminates any intermediaries, and if cash and tokens are not delivered, the transaction will not occur. In other words, tokenized transactions exist only in a settleable form and cannot be pre-agreed and recorded and then canceled. The biggest advantage here is the elimination of counterparty risk if the buyer fails to deliver cash equivalents or the seller fails to deliver shares.

However, the atomic settlement method also presents a technical challenge: in most cases, the e-wallets on the blockchain must have sufficient funds before settlement, or the transaction will not occur. Unlike failed deliveries in traditional transactions, the party that fails to deliver does not have a grace period to purchase or borrow the missing assets, and the transaction does not enter a pending state awaiting repair but stops directly. This can result in additional costs for issuers and investors, as they must maintain excess balances in their wallets. Pre-financing has a cost. The accompanying risk is that the cost of maintaining fund wallets exceeds the cost saved by the transaction.

However, other means of reducing costs can be employed, including: sharing data ledgers through blockchain instead of bilateral reporting and reconciliation; transfer registration without transfer agents; replacing centralized ledgers with self-maintained distributed ledgers; and using smart contracts to ensure timely access to corresponding rights for fund token holders.

IV. Issuance of Tokenized Funds

Although tokenization can bring many benefits such as real-time settlement, the issuance of tokenized funds is only applicable to new funds. This is because tokenizing existing funds would mean that fund shares might be recorded on the distributed ledger of the blockchain or by transfer agents in traditional registers, resulting in the cost of duplicate classification registration. Additionally, existing fund shareholders would conflict with tokenized fund shareholders.

As of mid-2021, out of the existing 127,913 funds globally (managing $68.6 trillion in assets), it is more feasible to add tokenized asset categories to existing funds (such as Fund 9, which allows funds to invest 100% of their quota in crypto assets after completing virtual asset business upgrades with the Hong Kong Securities and Futures Commission), or to provide tokenized versions of existing asset categories (i.e., tokenizing real assets, such as tokenized stocks, tokenized debt, including tokenized funds).

4.1 Tokenization of Money Market Funds - Franklin OnChain, Ondo Finance, Centrifuge

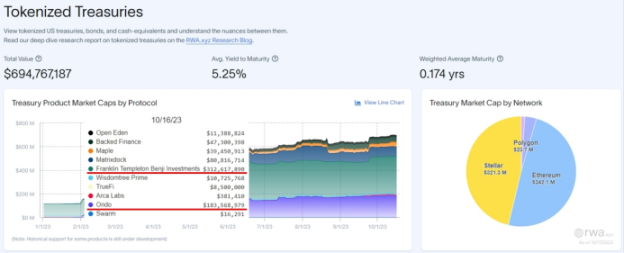

Apart from stablecoins, the largest tokenized RWA projects in terms of asset size are money market funds. The top three are Franklin Templeton: $312 million (government bonds); Centrifuge: $247 million (asset-backed); Ondo Finance: $183 million (government bonds).

Franklin Templeton is a fully tokenized fund, Ondo Finance also has two tokenized funds, and Centrifuge, in collaboration with Aave, has established tokenized funds in the RWA project. This demonstrates the importance of tokenized funds in connecting TradFi and DeFi.

(Source: RWA.xyz)

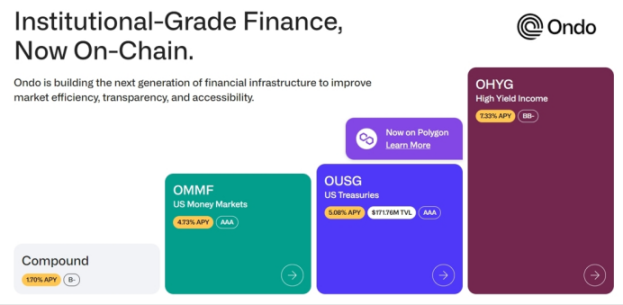

4.1.1 Ondo Finance OUSG / OMMF

(Source: Ondo.Finance)

Ondo Finance launched tokenized funds in January 2023, aiming to provide institutional investment opportunities and services to professional investors on-chain. It brings risk-free/low-risk interest rate fund products to the chain, allowing stablecoin holders to invest in government bonds and U.S. Treasury bonds on-chain. Ondo Finance's two tokenized funds, OUSG and OMMF, are backed by BlackRock's short-term U.S. Treasury ETF and money market funds, respectively.

Investors need to undergo Ondo Finance's official KYC and AML verification process before signing subscription documents. Qualified investors can then invest stablecoins in Ondo Finance's tokenized funds. Ondo Finance uses Coinbase Custody for fiat deposits and withdrawals and executes U.S. Treasury ETF trades through compliant broker Clear Street.

For regulatory compliance, Ondo Finance strictly implements a whitelist system for investors, allowing investment only for Qualified Purchasers. Investors need to complete Ondo Finance's official KYC and AML verification process before signing subscription documents.

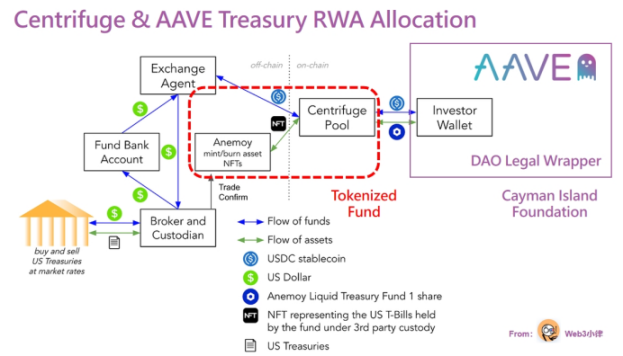

4.1.2 Centrifuge & Aave Treasury RWA Allocation

As a top player in the RWA collateralized lending model, Centrifuge has designed an RWA tokenization solution for Aave to capture the yield value of U.S. bonds in Aave's treasury assets. This solution also involves tokenized funds.

In this solution, the Anemoy Liquid Treasury Fund is a fund registered in the BVI, tokenized through the Centrifuge protocol. Aave then invests its treasury funds in the Anemoy tokenized fund's corresponding Centrifuge Pool, generating fund token certificates. The Centrifuge Pool then allocates the assets invested by Aave to the Anemoy fund. Finally, the Anemoy fund executes U.S. bond purchases through deposits, custody, and brokerages, bringing U.S. bond yields on-chain.

(Source: [ARFC] Aave Treasury RWA Allocation)

4.2 Tokenization of Private Equity Funds - Hamilton Lane, KKR

Historically, investing in private equity funds has had certain barriers for retail investors, with the market limited to large institutional investors and ultra-high-net-worth individuals. Additionally, a clear goal in the asset management market is to increase allocations to retail investors. The reasons for the continued under-allocation include high investment thresholds, long holding periods, limited liquidity (including a lack of developed secondary markets), a lack of price discovery mechanisms, complex manual investment processes, and a lack of investor education.

Although the tokenization market is still in its early stages, some private equity fund management companies are testing the waters by launching tokenized versions of their flagship funds. Notable private equity giants such as Hamilton Lane, KKR, and Apollo are exploring tokenized funds.

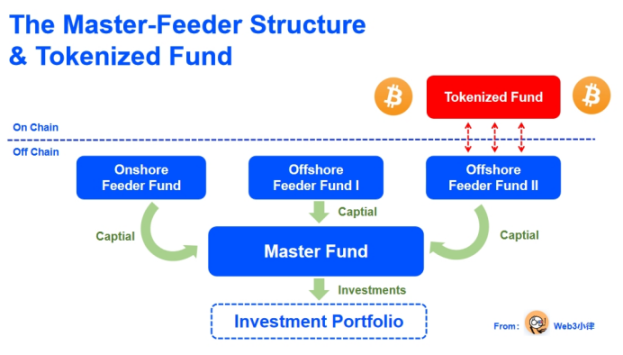

Due to limitations of existing funds, tokenizing only a portion of existing fund shares would result in the same shares being recorded on the blockchain's distributed ledger or by transfer agents in traditional centralized registers, leading to the cost of duplicate classification registration. One solution is for transfer agents to handle aggregation and consolidation. Another solution is to achieve tokenization through feeder funds.

Private equity funds can directly tokenize a portion of their fund shares by tokenizing the feeder fund in a master-feeder structure. In the master-feeder structure, the fund manager can raise funds from different types of investors to establish the feeder fund, which then invests the funds in a master fund. Investors invest and pay management fees at the feeder fund level, while transactions and investments occur at the master fund level.

The master-feeder structure is the preferred structure for large financial institutions issuing funds, typically facing investors in different jurisdictions to meet regulatory requirements and establish different business terms such as management fees, subscription terms, and investment strategies.

4.2.1 Hamilton Lane

Hamilton Lane, a global leading private equity investment firm managing assets of up to $823.9 billion, tokenized a portion of its fund on the Polygon network and made it available to investors on the Securitize trading platform. Through its collaboration with Securitize, the fund tokenized a portion of its fund shares in the form of a feeder fund and is managed by Securitize Capital (registered under SEC Reg D 506(c)).

The CEO of Securitize stated, "Hamilton Lane offers some of the best-performing private market products, but historically, they have been limited to institutional investors. Tokenization will enable individual investors to participate in private equity investments in a digital way for the first time and create value together."

From the perspective of individual investors, although tokenized funds provide an "affordable" way to participate in top-tier private equity funds, with the minimum investment threshold significantly reduced from an average of $5 million to just $20,000, individual investors still need to undergo qualified investor verification on the Securitize platform, presenting a certain barrier.

(Source: Securitize.io)

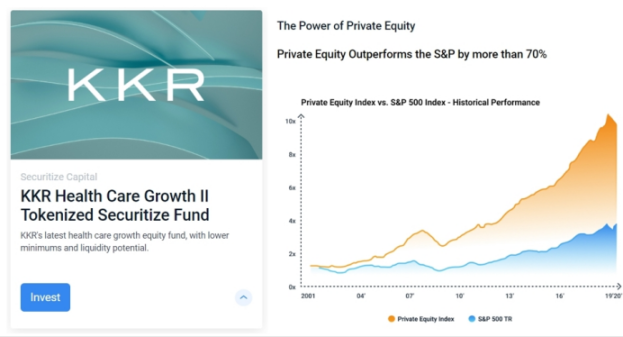

4.2.2 KKR

Similarly, KKR, managing assets of nearly $500 million, collaborated with the trading platform Securitize in October 2022 to tokenize a portion of its closed-end fund, Health Care Strategic Growth Fund II, on the Avalanche network.

From the perspective of private equity funds, the advantages of tokenized funds are evident. They not only provide real-time liquidity for a portion of private equity fund shares (in contrast to the traditional 7-10 year lock-up period) but also enable LP diversification and funding flexibility. This advantage may address the current market dilemma of being unable to exit projects obtained in a period of loose liquidity and high valuations during a period of reduced risk appetite and tight liquidity.

From the investors' perspective, the tokenization of private equity funds provides them with a low threshold opportunity to invest in top-tier private equity funds (with a performance rate far exceeding the S&P index by 70%). The threshold requirements for large institutional investors and ultra-high-net-worth individuals to participate in KKR funds are typically in the millions of dollars, while individual investors can now invest with a minimum threshold of $100,000 through this "tokenized" Feeder Fund.

(Source: Securitize.io)

### 5. Trading and Investment of Tokenized Funds

5.1 Secondary Market Trading of Tokenized Funds

(Source: SS&C, Tokenization of Funds - Mapping a Way Forward)

The most exciting potential brought about by tokenization may not be the blockchain-based settlement and issuance, but rather the secondary market trading of fund tokens.

As the tokenization market matures, the fully traded prices of fund tokens in the secondary market can more accurately reflect the value of the funds. This facilitates price discovery and provides a basis for fund pricing, rather than trading solely based on published net asset values, as with ETFs. This not only allows investors to view trades, portfolio valuations, and investment performance in real-time but also enables them to adjust their risk exposure. Fund tokens can also be traded based on investor demand, currency trends, and arbitrage, with arbitrageurs eliminating any price differences between tokenized funds and non-tokenized versions.

Furthermore, fund tokens circulating in the secondary market can serve as a liquidity supplement for fund redemptions. Funds can reduce the low-yield cash reserves held to meet redemptions. Once investors can sell tokens instead of redeeming shares, the fund's asset size stabilizes, and the cost of rebalancing decreases. If the underlying assets of the fund are also tokenized, fund managers will no longer need to sell underlying assets or borrow from banks to address liquidity mismatches between subscriptions and redemptions. Instead, the relevant underlying assets can be sold directly in tokenized form on the secondary market.

While tokenization may not actually increase the liquidity of some inherently illiquid asset classes, such as private equity and credit, infrastructure, real estate, art, and timberland, it can fully leverage the advantages of interacting directly with investor communities and increasing the application of DeFi scenarios, reducing the asset's high discount due to lack of liquidity. Additionally, tokenization can capitalize on the fragmentation of assets, allowing unit assets to be divided into smaller denominations, thereby lowering the investment threshold and allowing previously excluded investors to participate, bringing additional liquidity. The importance of these features has already been demonstrated in the cryptocurrency and DeFi markets.

The shrinking of publicly traded stocks and the subsequent growth of the private equity industry have cut off a series of investment channels for retail investors. Tokenization can allow them to re-enter asset classes that are currently only open to institutional investors.

Unfortunately, for compliance reasons such as KYC/AML/CTF, most tokenized funds are not yet open for permissionless trading on public blockchains. For example, the largest asset management scale tokenized fund, Franklin OnChain U.S. Government Money Fund, although it processes transactions and records ownership on the Stellar blockchain, has not yet seen any operations on public blockchains. Tokenized private equity funds such as Hamilton Lane and KKR can only subscribe to and redeem funds through the platform's entrance (after strict KYC), with more trading operations possibly taking place in the form of OTC. In the future, secondary market trading may be conducted through permissioned blockchains.

5.2 Tokenization Will Accelerate the Development of Personalized Investments

The higher investment threshold in traditional investments reflects higher capital costs. Tokenization significantly reduces the investment threshold by reducing the costs of fund issuance, subscription, redemption, registration, and services. Tokenization solutions may also be applied to small investor funds, which can invest in assets such as commercial and residential real estate, infrastructure projects, private equity and debt, art, and collectibles, which are currently excluded from traditional investments.

In the long run, the impact of tokenization may be far more profound than just reducing transaction costs, improving price discovery, increasing liquidity, and expanding the investor base of funds. Tokenization has the potential to create investment portfolios that fully meet the individual investors' needs, desires, and values.

Currently, funds are generic products that are expected to achieve returns or capital growth, or comply with a set of environmental, social, and governance (ESG) standards. Millennials have grown up with the digital economy and have never known a world without smartphones. What they need are direct, simple, and transparent fund products. For them, mutual funds are complex products that are difficult to understand, slow to purchase, and difficult to customize.

Tokenization can eliminate these barriers. Buying and selling fund tokens is cheaper, easier, and faster than traditional fund shares. Smart contracts can be embedded in fund tokens to conduct due diligence quickly and conveniently, allowing young investors to open accounts (e-wallets) in minutes rather than days, similar to owning a wallet for trading and holding cryptocurrencies.

Most importantly, tokens enable personalized investment portfolios. They can tokenize and fragmentize any asset, expanding the range of investable assets and even allowing small amounts of capital to be invested and customized based on the investor's personal preferences. Over time, tokenized funds may provide personalized investment portfolio packages for each investor, allowing them to manage their own bank accounts. Most importantly, personalized investment through tokenized funds has an intuitive appeal to a large number of young investors.

According to Newzoo's data, there are 2.9 billion electronic game players worldwide. The intersection between electronic game players and cryptocurrency enthusiasts means that use cases for cryptocurrencies already exist, allowing electronic game players to buy and sell in-game items on the blockchain. NFTs are actually an invention of electronic game players. Technically, tokenized funds have become part of the lives of millennials and Generation Z.

(Source: www.tbd.website/)

### 5. Regulation of Tokenized Funds

Traditional funds are generally subject to strict regulation in their local jurisdictions, with clear operational guidelines and implementation paths. However, after fund tokenization, who will regulate them? This is still a new topic. Participants in tokenized funds need to adapt to the fact that after tokenization, funds can be globally circulated based on public blockchains (although currently only limited permissioned circulation scenarios are seen), and may face regulatory authorities in all major fund markets globally, as well as regulatory frameworks for global crypto assets.

Although regulatory authorities around the world have responded to the rise of blockchain token financing since 2017, international regulatory bodies are also attempting to reach global consensus on how to regulate crypto assets. However, the legal regulations for regulating tokenized funds are still only applicable to specific jurisdictions and are not clear or explicit. The scope of regulating crypto assets includes legislating roles, rights, and obligations of issuers, investors, and intermediaries from a legislative perspective (as in Liechtenstein), to guiding which crypto assets and crypto asset activities require regulatory authorization (as in the UK). Without clear legal definitions of crypto assets and smart contracts, as well as subsequent precedents, tokenization still faces legal and regulatory uncertainty.

The uncertainty of regulation makes fund management companies uneasy. As regulated entities, they are reluctant to take action before seeking approval from regulatory authorities. However, at least in the UK, the guidance from the Financial Conduct Authority (FCA) has proven sufficient to allow the tokenization industry to develop on a certain basis, namely that the issuance of crypto assets on private networks, rather than public networks, is subject to existing securities and cash payment rules.

Firstly, issuing crypto assets on private blockchains (rather than public blockchains) enables fund managers to fulfill their regulatory obligations, conduct KYC, AML, CTF, and economic sanctions screening and verification of investors, which are prerequisites for investment. Secondly, fund tokens are regulated as securities by the FCA. This particularly assures investors that risks will be controlled, information disclosure will maintain market integrity, market manipulation and insider trading will be suppressed, and tokens will be securely held.

Although the above fund tokens are classified as "security tokens," fund tokens issued in the UK are subject to regulation under the Financial Conduct Authority's Collective Investment Schemes sourcebook (COLL), in the same manner as shares of mutual funds today. In other words, the issuer of fund tokens must issue a prospectus and key investor information document (KIID), comply with detailed COLL rules regarding investment, borrowing, risk management, and valuation, and appoint a depositary to protect investors.

Conclusion

If we want to realize the ultimate form of tokenized funds using the advantages of blockchain and distributed ledger, the current situation is analogous to the need to change the engine of an airplane flying at 30,000 feet. Additionally, the new engine needs to be completely rewired while remaining compatible with the old system. Of course, change will not happen overnight.

In the fund industry, the shift in strategic direction is already evident, with fund companies exploring tokenization and repositioning their businesses for the tokenized future. Fund management companies are acquiring wealth management businesses and investing in fund platforms. Fund platforms are considering the capabilities of transfer agents. Transfer agents and custodians are investing in order and execution management technology, as well as fund platform and custody services.

These developments indicate that the distribution and service ends of the fund industry have begun to restructure. The advantages touted by tokenization—lower costs, larger markets, greater liquidity, reduced counterparty risk, automated account opening/ongoing verification, expanded investable asset classes, changes in customer service, and personalized fund investments—are gradually being realized.

There is reason to believe that tokenization can simplify the intermediaries that separate fund managers from investors; accelerate the digitization of products and expand the range of investable assets under management; ultimately, the issuance and redemption of fund shares may give way to an active secondary market for fund tokens, freeing funds from the constraints of daily net asset values and enabling trading in a manner equivalent to investment trusts and ETFs.

Before realizing the value brought about by tokenization, many obstacles still need to be overcome. Common standards for KYC, AML, CTF, and economic sanctions screening and verification, cross-chain channels and oracles between public and private permissioned chains, and how to construct the secondary market. In addition, there is regulatory uncertainty, the lack of legal tender on the blockchain is a major constraint, but the biggest obstacle hindering progress is time.

A global industry's transition to the future cannot happen overnight. The danger lies in using the extended time for reform as an excuse for inaction, which would be a mistake. For blockchain, what is valuable today will still be valuable tomorrow, just like Bitcoin.

Reference:

[1] SS&C, Tokenization of Funds - Mapping a Way Forward

[2] CMS, Tokenised funds series

[3] Open for Investing 24/7: An Introduction to Open-End Funds on Solv V3

[4] Franklin Templeton Announces the Franklin OnChain U.S. Government Money Fund Surpasses $270 Million in Assets Under Management

https://investors.franklinresources.com/news-center/press-releases/press-release-details/2023/Franklin-Templeton-Announces-the-Franklin-OnChain-U.S.-Government-Money-Fund-Surpasses-270-Million-in-Assets-Under-Management/default.aspx

[5] UBS Asset Management launches first blockchain-native tokenized VCC fund pilot in Singapore

[7] [ARFC] Aave Treasury RWA Allocation

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。