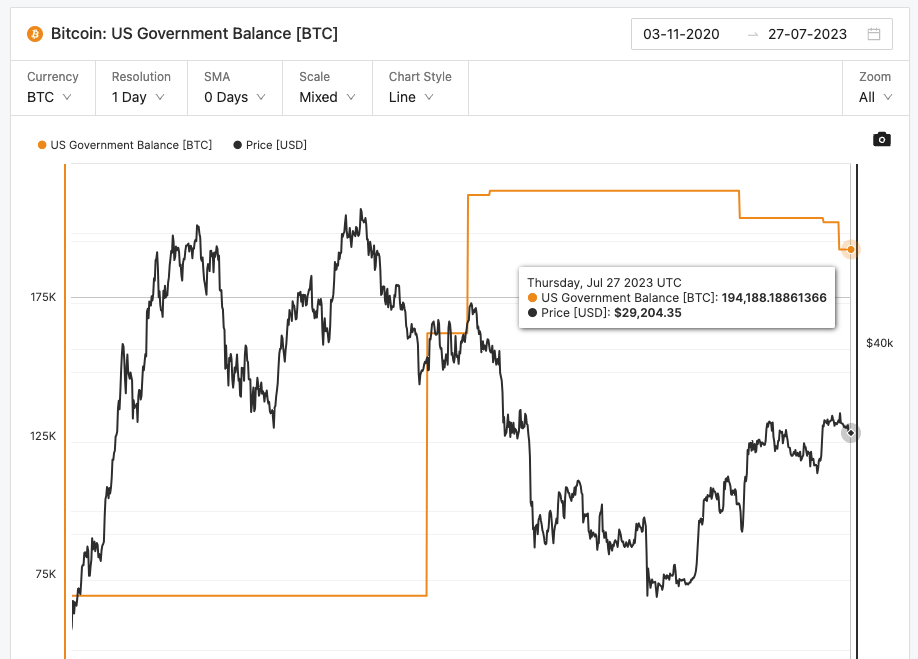

The US government's attitude towards cryptocurrency is very elusive. On the one hand, regulatory agencies continue to increase law enforcement efforts and crack down on cryptocurrencies. In the first half of the year alone, the SEC has successively sued large institutions such as Genesis, Kraken, Binance, and Coinbase. On the other hand, the US government holds the most Bitcoin. According to Glassnode's data, as of July 27, the US government holds approximately 194,188 bitcoins, accounting for about 1% of the Bitcoin supply, with a market value of approximately $5.68 million. Although these bitcoins were all confiscated (for free), compared to other governments, the US government is not in a hurry to liquidate the seized bitcoins, but chooses to hold onto them.

Source of the US government's Bitcoin holdings: Glassnode

Since the emergence of Bitcoin in 2008, the cryptocurrency market has experienced explosive growth, reaching a market value of $1.1 trillion. During the COVID-19 pandemic, the US government considered the cryptocurrency industry as a means to stimulate economic development and increase employment. However, due to regulatory loopholes, illegal activities related to cryptocurrencies such as fraud, money laundering, and cyber attacks have frequently occurred. In particular, the collapse of major institutions such as Terra and FTX has intensified calls for stronger regulatory policies in the market. Recently, both the EU and the UK have introduced their own cryptocurrency regulatory frameworks. In order to ensure the US's position in the global cryptocurrency field, attract more industry companies to stay in the US, and prevent capital outflow, the US also has to accelerate the promotion of related policies.

In September 2022, the Biden administration released the first regulatory framework for cryptocurrencies, urging regulatory agencies such as the CFTC and SEC to formulate specific rules for digital assets. In 2022 alone, the US Congress has proposed more than 50 bills related to digital assets. Recently, the US House Committee passed the "21st Century Financial Innovation and Technology Act" which is considered to have a milestone significance for US cryptocurrency regulation, while the "Responsible Financial Innovation Act" proposed by the Senate is seen as its strong competitor. Both bills are expected to help the US establish a viable cryptocurrency regulatory system.

This article will analyze in depth the factors influencing the US's stance on cryptocurrency regulation, how these two bills will shape the US's cryptocurrency regulatory framework, and evaluate the potential impact of this change on the market.

The US Cryptocurrency Regulatory Dilemma: Who is in Charge of Cryptocurrencies?

Are cryptocurrencies regulated in the US? The answer is yes.

- In 2013, the US Department of the Treasury defined Bitcoin as virtual currency and classified cryptocurrency exchanges and management institutions as Money Services Businesses (MSBs), requiring them to comply with FinCEN's anti-money laundering policies.

- In 2014, the Internal Revenue Service (IRS) classified cryptocurrencies as property and required them to be taxed.

- In 2015, the Commodity Futures Trading Commission (CFTC) classified Bitcoin and Ethereum as commodities and brought their trading under regulation.

- In 2017, the Securities and Exchange Commission (SEC) stated that ICOs are securities offerings and should be registered with the SEC and comply with anti-fraud regulations.

- In 2021, the "Infrastructure Bill" defined digital assets as cash.

It is not difficult to see that in the US, different regulatory agencies have different definitions of cryptocurrencies/digital assets. This is also an important reason why the US government has been unable to establish a complete regulatory system, as regulatory agencies cannot define what cryptocurrencies are and who is in charge.

Cryptocurrencies go beyond the classification framework of traditional assets. If a traditional financial asset is a commodity (similar to gold, coffee), it should be regulated by the CFTC; if it is a security (such as stocks, bonds), it should be regulated by the SEC; if it is a currency, the situation becomes more complicated, subject to regulation by multiple agencies such as the Department of the Treasury. However, cryptocurrencies may have one or more attributes of assets. For example, ETH can be bought and sold on exchanges, thus having commodity attributes; at the same time, it can be used as a medium of exchange for various goods and services within the Ethereum network, having currency attributes; in addition, during the early ICO sales, Ethereum was similar to traditional securities issuance, thus having security attributes.

Conflict between SEC and CFTC

Due to the difficulty in defining the nature of cryptocurrencies, the responsibilities of regulatory agencies are not clear, resulting in many overlaps and gaps in the regulatory system. Among them, the conflict between SEC and CFTC is particularly significant.

Source: LinkedIn

Firstly, in US law, the boundary between securities and commodities is blurred. The federal securities laws define an "investment contract" as a type of security, i.e., an investment in a common enterprise with the expectation of profits primarily from the efforts of others. Based on this definition, SEC Chairman Gary Gensler has stated that most cryptocurrencies should be classified as securities and should be regulated by the SEC.

For more information about Gary Gensler, please refer to: Is Gary Gensler Still Worth the Crypto Market's Expectations?

However, in commodity trading law, "commodity" almost covers all goods and services, including Bitcoin and other cryptocurrencies. (In fact, securities can also be considered a type of commodity.) The overlap between the concepts of "commodity" and "security" has led to ongoing disputes between the SEC and CFTC in recent years.

However, the CFTC primarily regulates derivatives trading of commodities, with relatively limited regulatory authority over spot trading, only being able to prosecute when fraudulent and manipulative activities are found in digital assets. This has led to a problem: when a digital asset is neither a security nor engaged in derivatives trading, both the SEC and CFTC have no regulatory authority. This situation is not uncommon, for example, with DAO, where token investors are also managers of the protocol, it is not within the SEC's regulatory scope (because it does not meet the standard of investors benefiting from the efforts of others). The regulatory gap between the SEC and CFTC has allowed many cryptocurrency projects to successfully evade institutional regulation.

Two Bills That Could Change the US Cryptocurrency Regulatory Landscape

Recently, two bills proposed by the US Congress, named the "Financial Innovation and Technology for the 21st Century Act" and the "Responsible Financial Innovation Act," may provide solutions to the long-standing issues of the CFTC and SEC.

TL;DR

- Both bills aim to establish a viable regulatory framework for digital assets, clarify the definition of digital assets, and differentiate the regulatory responsibilities of the CFTC and SEC.

- Both bills grant greater regulatory powers to the CFTC.

- Both bills aim to protect the rights of consumers/investors, requiring more information disclosure from digital asset-related institutions for regulation.

- Both bills aim to legislate to determine the US's leadership position in the cryptocurrency field.

- Both bills do not involve the regulation of NFTs.

- Compared to the "Financial Innovation and Technology for the 21st Century Act," the "Responsible Financial Innovation Act" has a broader scope. In addition to the above, it also addresses issues such as stablecoin issuance, combating financial crimes, digital asset taxation, and institutional funding.

Financial Innovation and Technology for the 21st Century Act

The "Financial Innovation and Technology for the 21st Century Act" (FIT21) was introduced by Republican members of the House Financial Services Committee and the Agriculture Committee on July 20, 2023, and was voted on by the two committees of the House on July 26 and 27, respectively. The bill will be transferred to the House and is expected to be voted on after the adjournment on September 12.

The "Financial Innovation and Technology for the 21st Century Act" aims to establish a regulatory framework for the digital asset market in the US, provide clear rules for market participants, and protect investors and consumers.

Passage of the FIT21 bill, Source: Twitter

Clarification of CFTC and SEC Jurisdiction

The bill advocates for the joint management of digital assets by the CFTC and SEC, with the CFTC as the primary regulator and the SEC as the secondary regulator. The bill classifies digital assets into digital commodities, restricted digital assets, and payment stablecoins. Digital commodities are managed by the CFTC, while restricted digital assets are managed by the SEC. Payment stablecoins can be traded in venues regulated by the SEC and CFTC, but both agencies have no authority to regulate stablecoins or stablecoin issuers.

What are digital commodities? The bill stipulates that when a digital asset's related blockchain network meets both of the following conditions, the asset is considered a digital commodity: 1) functional network 2) decentralization. A functional network refers to a digital asset that can be used on the network for value transfer and storage, participation in services or applications, and governance. Decentralization means that no individual or entity can unilaterally control the blockchain. If a digital asset does not meet the conditions for a digital commodity, it is considered a restricted digital asset.

Similarly, the bill categorizes intermediaries into digital commodity intermediaries and digital asset intermediaries. Digital commodity intermediaries are regulated by the CFTC, while digital asset intermediaries are regulated by the SEC.

Information Disclosure and Consumer Protection

The bill requires disclosure of source code, transaction records, economic models, development plans, related entities and personnel, and risk factors for digital assets and blockchain systems.

For intermediaries, before providing services, they need to prove to the CFTC that they are not involved in market manipulation and register with the National Futures Association. After registration, intermediaries must meet various requirements during operation, including meeting business conduct standards, minimum capital requirements, ensuring fair trading, segregating customer assets, disclosing operational conditions, ledger records, conflicts of interest, etc.; if there is any misconduct, they will be subject to penalties from regulatory agencies.

Auxiliary activities related to blockchain operations do not need to be registered with regulatory agencies

The bill specifically states that individuals involved in auxiliary activities related to blockchain operations, such as network validation, node management, providing API/RPC services, development, maintenance, or management of blockchain systems, do not need to register with regulatory agencies.

Analysis of the Stance

The sponsors of the "Financial Innovation and Technology for the 21st Century Act" have attracted attention, including the Chairman of the House Agriculture Committee (Glenn “GT” Thompson) and the Chairman of the House Financial Services Committee (Patrick McHenry). The bill has received support from Republicans and the crypto community. Patrick McHenry publicly stated that this is the committee's first revision of legislation on cryptocurrencies and emphasized the need to prevent the US from falling behind other countries in cryptocurrency regulation. CoinBase CEO, Brian Armstrong, has also publicly supported the bill before the vote. Brian believes that this is a vote to protect cryptocurrencies, US innovation, and security.

CoinBase CEO advocating for FIT21, Source: Twitter

However, most Democrats lean more towards Gary Gensler's view, believing that most cryptocurrencies are securities. They believe that primary regulatory powers should not be handed over to the CFTC, as other important figures in the crypto industry, such as SBF, have requested this regulatory agency to oversee the crypto industry, which could lead to more fraud in the future. Democratic House member Stephen Lynch stated, "I've been on this committee for 20 years, and I can say definitively that this is the worst legislation to enter the markup in 20 years."

Responsible Financial Innovation Act

The Responsible Financial Innovation Act (RFIA) was first introduced by Republican and Democratic senators on June 7, 2022, and its updated version was released on July 12, 2023. Its main goal is to create a regulatory framework for digital assets, clarify the jurisdiction of the CFTC and SEC, address stablecoin issuance, digital asset taxation, and protect consumers, providing certainty and clarity for the industry.

RFIA sponsors, Source: The Washington Post

Clarification of CFTC and SEC Jurisdiction

The bill considers most digital currencies to be commodities rather than securities, including BTC and ETH, and regulated by the CFTC. However, when digital assets have characteristics similar to debt or equity, they are considered securities and regulated by the SEC. When digital assets meet any of the following conditions, they are considered securities: 1) debt or equity, 2) liquidation rights, 3) rights to interest or dividends, 4) profits or income derived solely from the efforts of others, 5) any other economic interest in the enterprise.

Under this bill, digital assets are considered commodities and do not need to be fully decentralized, and can also be certified as commodities.

Information Disclosure and Consumer Protection

After the collapses of institutions such as Terra and FTX, the Responsible Financial Innovation Act emphasizes consumer protection, with many requirements for information disclosure, reserve proof, advertising standards, and loan restrictions.

- Digital asset exchanges must register with the CFTC and comply with disclosure requirements.

- Digital asset issuers need to regularly disclose information to the SEC to prove the commodity nature of digital assets.

- Intermediaries need to disclose significant changes and operations to users, including asset custody, bankruptcy handling, fee structure, dispute resolution, etc.

Formulation of Stablecoin Issuance Policies

The bill imposes strict requirements on the issuance of stablecoins, which can only be issued by federal/state depository institutions and regulated by federal/state regulatory agencies. Additionally, issuers are required to maintain a 100% reserve of high-quality assets and publicly disclose the reserve assets supporting the stablecoin and their value. The bill also proposes that algorithmic stablecoins should be regulated by the CFTC.

Adjustment of Digital Currency Taxation

The bill clarifies the taxation policy for digital assets and provides small-scale tax incentives for cryptocurrency holders. Additionally, the bill proposes convenient measures for providing cryptocurrency services to non-US individuals in terms of taxation.

Analysis of the Stance

The Responsible Financial Innovation Act was first proposed after the collapse of Terra, emphasizing regulatory issues related to stablecoins in the bill. However, the bill did not receive much support at the time. After the collapse of FTX, the sponsors Cynthia Lummis and Kirsten Gillibrand made significant modifications to the bill. The modified bill emphasizes consumer protection and clarifies the CFTC's superior regulatory position over the SEC.

To learn more about the story of FTX and SBF, please read: Who is SBF — From Mansions and Yachts to Silver Bracelets and Iron Bars in Five Years

It is worth noting that unlike the "Financial Innovation and Technology for the 21st Century Act," this bill was jointly proposed by bipartisan lawmakers. However, the bill is also likely to face scrutiny from some SEC supporters. Additionally, the bill falls under the jurisdiction of the Banking Committee and the Agriculture Committee in the Senate, but Banking Committee Chairman Sherrod Brown (Democratic) has explicitly stated that he will not support the bill.

However, some opinions suggest that the bill has a broad scope and may not necessarily need to be passed as legislation, as each part of it could have far-reaching implications for more specific proposals.

How the New Bills Will Impact the Market

The introduction of the two bills has sparked a lot of attention, but the actual implementation of these bills will go through a long process, including stages from proposal to passage in the House, Senate, and ultimately approval by the President to become law. Currently, the "Financial Innovation and Technology for the 21st Century Act" has just passed the House committee review, while the "Responsible Financial Innovation Act" has just been proposed. It is worth noting that the "Financial Innovation and Technology for the 21st Century Act" is expected to be voted on in the House after the adjournment in September. If passed, the market is expected to experience a short-term correction.

Overall, the original intention of the new cryptocurrency regulatory framework is to clarify the responsibilities of regulatory agencies and protect consumer rights through enhanced information disclosure. Both bills have fully considered the characteristics of the digital asset industry, such as decentralization, and have not attempted to suppress the industry's development. A clear regulatory framework will help eliminate market uncertainty, providing a clearer operating environment for participants, attracting more institutional and individual investors to enter the market, further promoting market maturity and stability.

However, any kind of change will inevitably bring some fluctuations in its initial stages. The implementation of regulatory policies will undoubtedly affect some gray areas in the current cryptocurrency market, potentially causing market turmoil in the short term. The requirements for information disclosure may also contradict the vision of decentralization and lack of regulation for some market participants. However, both bills support the CFTC as the regulator of the cryptocurrency industry. The CFTC has always had a more friendly attitude towards the industry compared to the SEC and has received support from leading figures in the crypto industry. Therefore, the CFTC becoming the ultimate regulator of the industry is in line with the expectations of the crypto community and is a positive development.

In the long run, the introduction of these new regulatory policies will help protect consumer interests and bring greater transparency and trust to the cryptocurrency market.

TokenInsight's Latest Updates

Historical price data for cryptocurrencies and historical trading volume for exchanges are available for free download. In addition, our API product has added interfaces for historical data of cryptocurrencies and exchanges.

Thank you for reading our report and using our products. For feedback on the report content and products, please feel free to email us at info@tokeninsight.com, and we will be happy to assist you.

A 100% open-source, no additional cost bulk transfer tool that supports multiple chains is also available.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。