TL;DR

- Morgan Stanley raised the target price for SIMO from $155 to $400, primarily due to accelerated demand for enterprise SSDs and boot drives driven by AI.

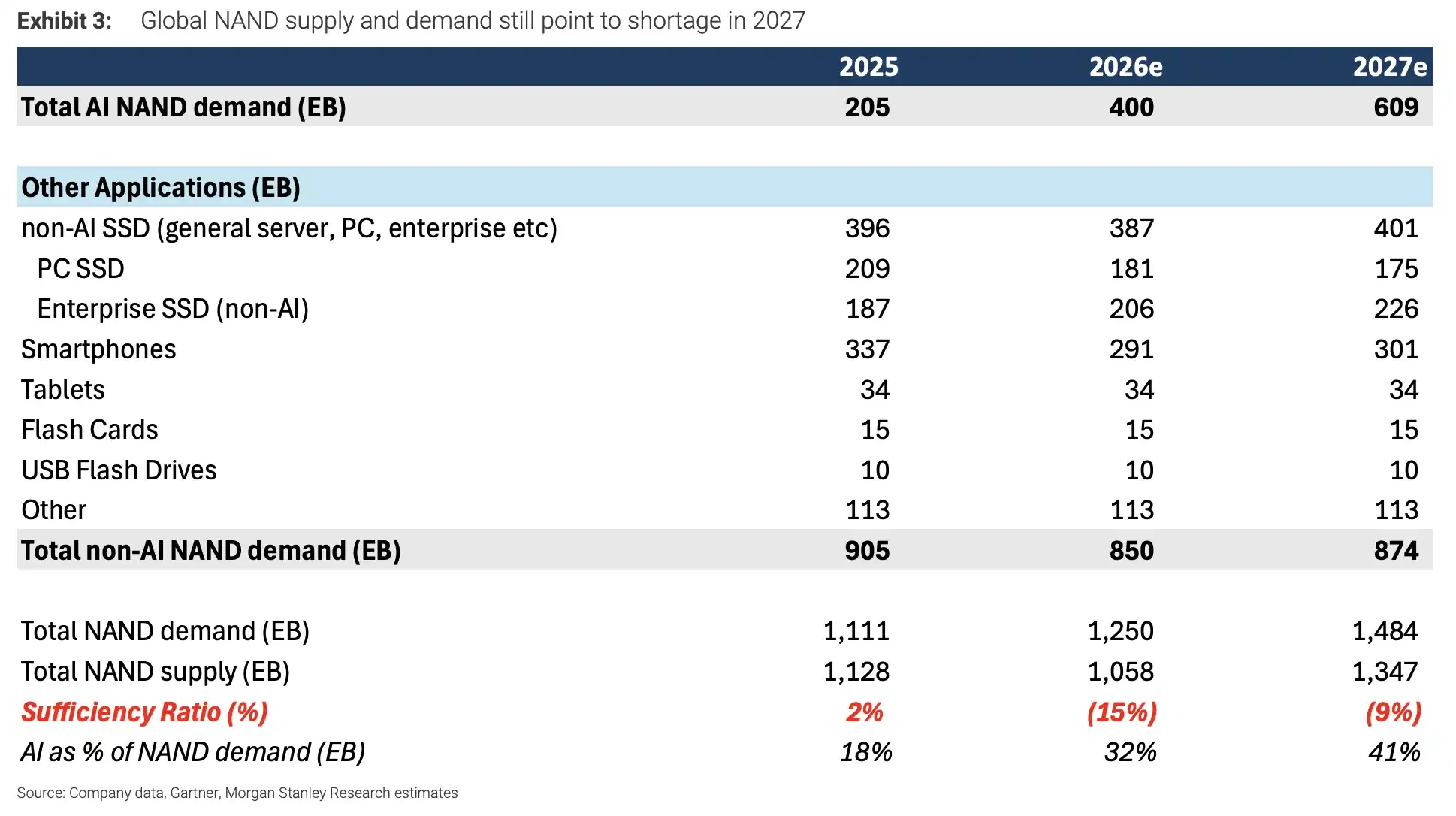

- It anticipates a 15% shortage of global NAND in 2026 and a 9% shortage in 2027, with AI-related demand reaching 609EB by 2027.

- Suppliers and controller manufacturers will benefit more directly, but price increases at the consumer end are limited, while YMTC's capacity expansion and AI capital spending slowdown may alter supply and demand in 2028.

Morgan Stanley significantly raised the target prices for Silicon Motion (SIMO.O) and Longsys in its latest report, pointing to the NAND demand gap created by AI servers. For investors, this is not just an ordinary expectation of SSD price increases; it is a shift towards enterprise-level SSDs, AI boot drives, and long-term procurement by cloud providers, moving NAND demand away from consumer electronics cycles such as smartphones and PCs.

The most aggressive adjustment is for SIMO. Morgan Stanley increased its target price from $155 to $400, corresponding to 23 times the expected EPS for 2027, and expects the company’s revenue to reach an all-time high in 2026. The target price for Longsys was also raised from 300 yuan to 673 yuan, and for Phison from 2248 New Taiwan dollars to 2588 New Taiwan dollars. However, Morgan Stanley maintains an Equal Weight rating on Longsys and Phison, indicating that not all module vendors will benefit uniformly from this cycle.

The core judgment of this report is: The demand pull from AI for NAND will continue until 2027. In 2025, the previous round of inventory surplus will still allow the global NAND supply and demand to present about a 2% surplus; by 2026, the market is expected to shift to a 15% shortage; and even with continued supply release in 2027, there could still be a 9% gap. The key drivers are not smartphones and PCs but rather AI servers, SSDs for cloud providers, enterprise storage, and boot drive demand.

The global NAND supply and demand still point to a shortage in 2027. Total demand estimates for 2025-2027 are 1111/1250/1484 EB, supply 1128/1058/1347 EB, shifting the supply-demand ratio from a 2% surplus to -15% and -9%.

AI shifts NAND demand focus from consumer electronics to data centers

NAND has historically been more easily influenced by the inventory cycles of smartphones, PCs, and consumer-grade SSDs. The current change is that AI servers need not only GPU and HBM but also substantial local storage, enterprise SSDs, and boot drives. Once cloud providers enter into long-term agreements for procurement, the fluctuations in NAND prices and supply-demand dynamics will also change.

Morgan Stanley predicts that AI-related NAND demand will grow by 60% year-on-year in 2027, reaching 609EB, accounting for 41% of overall NAND demand. The total global NAND demand for that year is expected to be 1484EB, while supply will be 1347EB, corresponding to about a 9% shortage. In contrast, the assumptions for smartphones and PCs are not aggressive: individual NAND capacities will roughly remain flat, and terminal shipments are expected to decline according to hardware team models.

This indicates that the shortage judgment in the report is not based on a full recovery in consumer electronics but rather on the continued expansion of AI servers and cloud capital expenditures. The greater the contribution from AI demand, the higher the sensitivity of the NAND cycle to CSP procurement, server configurations, and enterprise SSD supply.

The channel prices have already begun to diverge. Channel checks in 3Q26 show that TLC enterprise SSD pricing increased by about 30% quarter-on-quarter, server-grade DRAM rose by 20%, and legacy DRAM like DDR3/DDR4 increased by 30%-40%. However, the price increases for consumer-grade NAND are significantly smaller, as smartphone and PC customers face greater profit pressure and are unable to bear similar price hikes.

In other words, price increases are indeed occurring, but the strongest increases are seen in data center-related products, not all NAND categories.

Why was SIMO raised the most?

The core reason for the upward revision of the target price for SIMO is that its business just happens to hit two segments of the incremental AI storage: enterprise SSD controllers and AI boot drive modules.

The MonTitan enterprise SSD business is viewed as the most important new growth point for the company over the next few years. Morgan Stanley expects this business to contribute 5%, 13%, and 19% of SIMO's revenue in 2026, 2027, and 2028, respectively. Meanwhile, boot drive modules are also expected to ramp up, contributing approximately 15% and 21% to the company's revenue in 2026 and 2027, respectively.

For AI servers, the boot drive is not the most obvious component, but it is an essential storage configuration for system startup, management, and operation. As AI server shipments increase, the demand for relevant controllers and modules will also rise accordingly. SIMO was originally more easily perceived by the market as a consumer-grade controller company, but the key to its valuation adjustment now is the potentially rapid increase in the proportion of enterprise and AI-related revenues.

However, this is still a prediction and not a realized profit. The $400 target price from Morgan Stanley corresponds to 23 times the expected EPS for 2027, with the underlying assumption being that enterprise SSDs and boot drives ramp up smoothly, customer integration continues, and AI server demand does not slow down significantly. Any shortfall in any one of these areas could impact whether the valuation can hold.

Module manufacturers raise target prices, but may not receive the largest share of the pie

Longsys and Phison also benefit from storage price increases and AI server demand, but the report did not upgrade their ratings to a more favorable level. The reason is that module manufacturers face a realistic constraint in this cycle: when NAND supply is tight, original manufacturers are more likely to prioritize capacity allocation to large cloud providers and core CSP customers, meaning module manufacturers may not receive enough incremental supply.

This is also why target prices can be raised, but ratings remain at Equal Weight. Price increases benefit inventory and ASP, and improving the enterprise product mix can also support profit margins, but if the volume is locked by upstream suppliers and large customers, the revenue elasticity for module manufacturers will be limited.

Long-term procurement agreements (LTA) are another important clue. Suppliers can achieve some price downside protection through LTAs, with Kioxia's LTA coverage expected to exceed 50% in 2027. However, these agreements do not solely favor the suppliers, as Micron has pointed out that LTAs often include both price ceilings and floors. They can reduce the risk of price crashes but may also limit suppliers' ability to raise prices during extreme shortages.

Module manufacturers hope to transfer more inventory pressure to customers through models like TCM, stabilizing long-term gross margins within a range of 25%-35%. However, this also depends on customer acceptance, the degree of supply tightness, and whether the products are sufficiently high-end.

The risk in 2028 lies in supply and AI spending

The biggest boundary for this optimistic forecast comes in 2028.

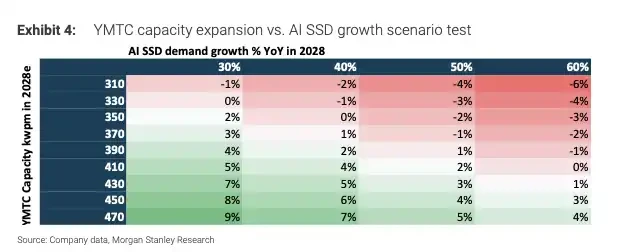

In Morgan Stanley's baseline scenario, even by 2028, if AI NAND demand continues to grow by 60% year-on-year and YMTC's production capacity remains around 310kwpm, there could still be about a 5% shortage in the market. However, if YMTC's production capacity rises to 470kwpm while AI growth slows down, the NAND market could shift from shortage to surplus.

YMTC's capacity expansion in 2028 vs. AI SSD growth scenario testing. The matrix shows the combinations of YMTC's production capacity at 310-470kwpm with AI growth at 30%-60%, indicating supply and demand could shift from shortage toward near balance or even surplus.

This is also the most challenging aspect of judging the memory cycle: short-term price increases and low inventory levels can easily reinforce optimistic expectations, but once semiconductor memory supply discipline loosens, a surplus can return quickly. There have already been some order reductions from the consumer side, and smartphone and PC customers have limited capacity to absorb price increases; the price ceiling for consumer-grade NAND may appear sooner than for enterprise-grade products.

Therefore, the real question posed by this report to the market is not "Will SSD prices rise?" but rather whether AI demand will be strong enough to absorb the additional supply over the next two years. For companies like SIMO and others in the AI storage chain, 2026 may be the starting point for an increase in enterprise and AI business; for the entire NAND cycle, the pace of capacity expansion by manufacturers like YMTC, CSP capital expenditure intensity, and supplier discipline in 2028 will be key to determining whether shortages can continue.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。