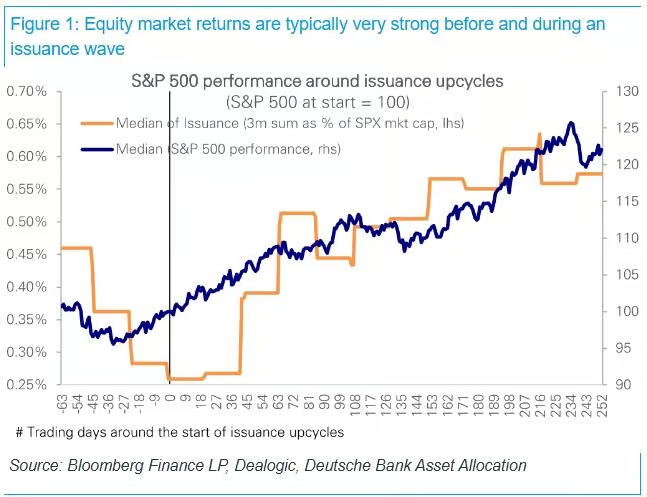

Deutsche Bank strategists found after sorting through thirty years of data that during peak IPO periods, the median return rate of U.S. stocks is about 8% over three months and over 20% over twelve months. A strong market stimulates strong IPOs, rather than IPOs overwhelming the market.

Written by: Long Yue

Source: Wall Street Journal

The current U.S. IPO market is experiencing a wave of large-scale stock issuance, and the most pressing question is: will this "massive supply" lead to a "draining" of the market that collapses U.S. stocks?

Deutsche Bank strategists, including Binky Chadha, recently gave a clear answer to this question. The strategists systematically analyzed the historical data of multiple stock issuance cycles over the past several decades, combined with academic literature and empirical studies, and concluded that waves of stock issuance usually coincide with strong stock market performance, rather than triggering market declines.

Strategist Jim Reid stated that this is one of the most common questions he hears from clients. His assessment is that such concerns are often misaligned historically. At the same time, the institution acknowledges that large IPOs could indeed cause about a 1% drag on the market in isolated scenarios, but every one to two months, the U.S. stock market tends to experience a drop of 3% or more for various reasons, and IPO supply is just one of many factors.

How significant is the IPO wave? First, understand the scale

The scale of stock issuance in the U.S. has been climbing steadily since the beginning of 2023, with quarterly issuance rising from a low of about $30 billion to around $120 billion now. SpaceX is about to go public. In the coming months, several highly anticipated mega-companies, such as OpenAI, are expected to go public, with individual financing amounts potentially reaching several tens of billions of dollars.

Sounds alarming? But in the context of the entire market, even the largest anticipated IPOs only account for just over 0.1% of the total market capitalization of the S&P 500.

The logic behind investors' concerns is that new stocks entering the market require capital, buyers need to free up money, which means selling existing stocks and thus lowering the overall market. This reasoning sounds reasonable, but the data does not support it.

Historical pattern: During peak IPO periods, the stock market often performs better

Over the past thirty years, during multiple stock issuance peaks, the median return rate of U.S. stocks has been approximately 8% over three months and over 20% over twelve months.

Why is this the case? The logic is quite direct: companies choose to go public precisely because of strong market demand, good profit momentum, and high investor risk appetite.

In other words, it is a strong market that stimulates IPOs, rather than IPOs overwhelming the market.

Academic research has indeed found that issuance waves eventually accompany weakening returns— but the key is that this "eventually" often takes a long time, and prior to that, the market has usually already risen significantly.

The only exception was during the 2008 to 2009 financial crisis. At that time, stock issuance was forced, occurring against the backdrop of a systemic crisis, which was fundamentally different.

How significant is the supply pressure? Strong demand is key

From a supply-demand framework, large IPOs could indeed cause about a 1% drag on the market in isolated circumstances, and concentrated issuances could trigger short-term volatility.

However, disturbances of this magnitude are not uncommon. Every one to two months, the U.S. stock market experiences a 3% or greater pullback for various reasons, and IPO supply is just one of many factors.

More importantly, the current market demand side is extremely strong: funds are continuously flowing in, corporate earnings are growing steadily, overall stock positions remain at relatively moderate levels, buyback activities are active, and household balance sheets have ample space to absorb the new supply.

"Strong demand, rather than excess supply, is likely the decisive characteristic of this IPO wave." This is the core judgment given by strategist Chadha.

Is it now 1999 or 2000?

Deutsche Bank used a vivid analogy to describe the current market situation: "It feels like it is still 1999, not 2000."

The implication is that the party is not over yet, but one must also recognize that the party will ultimately end. Returns will weaken after the issuance wave, but it is difficult to determine the timing, and before that, the market often sees a period of strong performance.

Therefore, Deutsche Bank states that regardless of whether we ultimately reach 2000 (the internet bubble era), it still feels like 1999 now.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。