Differences Between On-Chain U.S. Stocks (RWA) and Brokerages — — Liquidity Section

Today, during the introduction, I found that many friends mentioned the issue of broker liquidity, all asking me whether the liquidity of brokerages is sufficient. In fact, this is a misguided question and a reflexive thought many have after trading U.S. stocks on-chain or on exchanges.

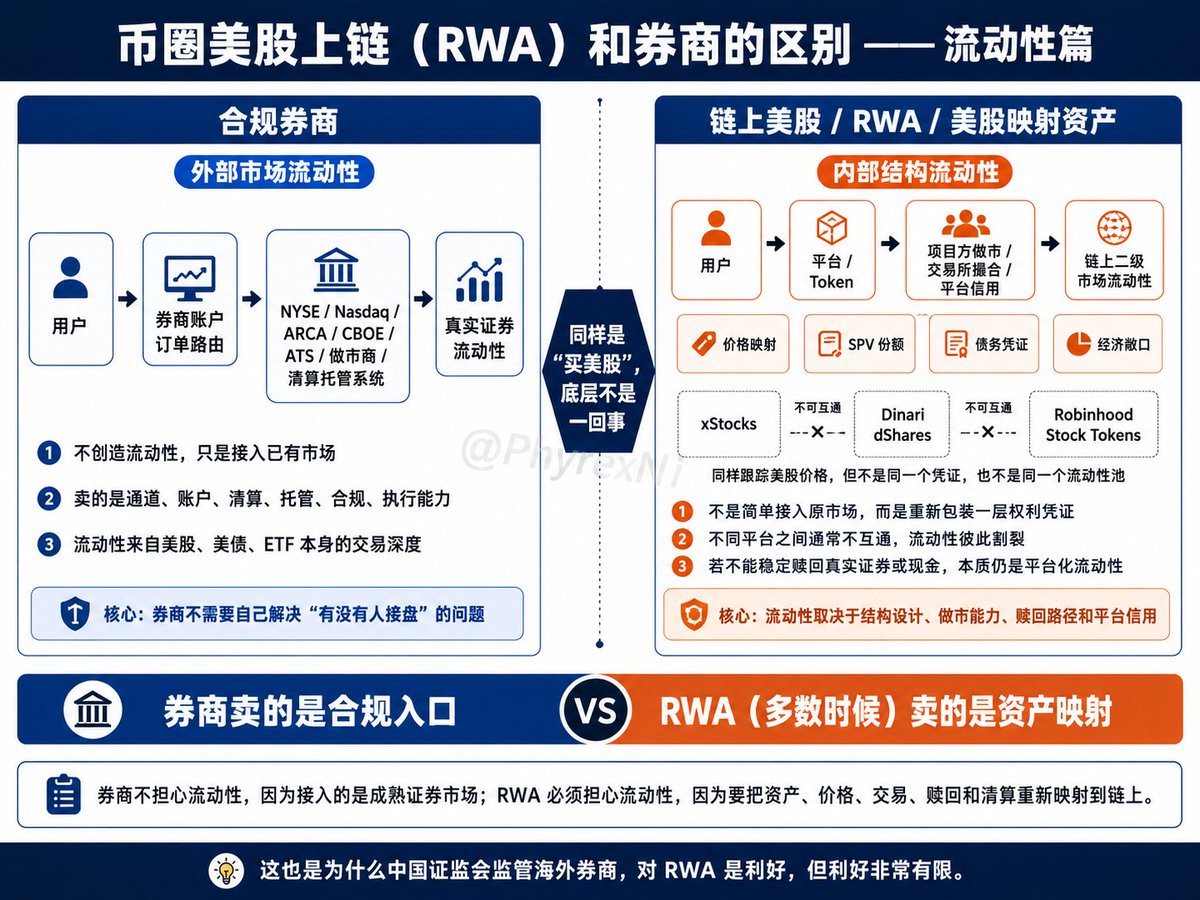

First, let's talk about brokerages. Compliant brokerages do not have liquidity issues because compliant brokerages are not selling “liquidity created by themselves,” but rather “a compliant gateway to existing liquidity markets.”

In other words, when users buy and sell U.S. stocks, U.S. bonds, or ETFs through compliant brokerages, they are essentially not trading within the brokerage’s own pool, nor is the brokerage using its inventory to act as the counterparty for users. Instead, the brokerage connects user orders to the NYSE, Nasdaq, ARCA, CBOE, ATS, market makers, clearing systems, and custodial systems.

Brokerages sell gateways, accounts, clearing, custody, compliance, and execution capabilities, rather than creating a secondary market for Apple, Nvidia, VOO, QQQ, IBIT, etc.

Therefore, compliant brokerages do not need to worry about “if there is someone to take over,” because liquidity is inherently present in the U.S. stock market. When users buy and sell Nvidia, the liquidity comes from the trading depth of Nvidia stock itself. When users buy and sell SPY, VOO, QQQ, liquidity comes from the secondary market of ETFs, market makers, and the primary market’s subscription and redemption mechanism. When users buy and sell U.S. bond ETFs, liquidity comes from the underlying bond market, ETF market making, and institutional arbitrage.

As long as brokerages compliantly integrate into this system, liquidity is not an issue for brokerages, and there is no liquidity problem.

On the contrary, it is on-chain U.S. stocks, RWA, or U.S. stock-mapped assets in exchanges that truly need to worry about liquidity. This is because such products do not simply connect to existing markets but recreate a trading scenario and even repackaged a layer of rights certificates. This is what I have always said before: the liquidity provided by different providers of on-chain U.S. stocks varies.

Even each so-called “U.S. stock” is not interchangeable; for example, the simplest case is that even though they are all on-chain U.S. stocks, the gateways behind xStocks, Dinari dShares, and Robinhood Stock Tokens are different. So even if they are all called “Tesla Token” or “Apple Token,” it does not mean they can interconnect.

Users cannot directly use TSLAx from Kraken as Dinari's TSLA dShare. They also cannot directly take Dinari's dShare to convert it into Robinhood Stock Token on the Robinhood platform. Nor can they treat Robinhood's Stock Token as genuine stocks to withdraw and transfer into a U.S. brokerage account.

This is analogous to three companies issuing three “certificates tracking Nvidia's price.” The price is based on Nvidia, but the certificates themselves are not the same. Naturally, they represent different liquidity pools and have absolutely no relation to traditional NYSE or Nasdaq.

The difference here is significant.

For example, when a user buys a share of Nvidia through a brokerage, at least in legal terms, the user is purchasing a true securities interest held through the brokerage, clearing, and custodial systems. However, when a user buys a Nvidia Token on-chain, what they may receive is a price mapping, a debt certificate, an SPV share, an economic exposure promised by a certain platform, or perhaps just a contract linked to the real stock price.

The liquidity of brokerages is “external market liquidity,” while RWA’s liquidity is “internal structural liquidity.” Brokerages connect to the most mature, deepest, and most market maker and institutional participant-engaged securities markets globally, whereas RWA involves project parties market-making, exchanges facilitating trades, and users backfilling each other.

As long as on-chain assets cannot stably connect to real securities, cash, or compliant redemption paths, RWA’s liquidity will never be native U.S. stock liquidity, but rather secondary market liquidity that has been repackaged.

This is also why I say that the China Securities Regulatory Commission’s regulation of overseas brokerages is favorable for RWA, but the benefits are very limited.

This regulatory crackdown is not on U.S. stocks themselves, nor on U.S. stock liquidity, but rather on the actions of providing cross-border securities services to Chinese residents without licenses within China. The real demand of most users is for overseas asset allocation, to buy U.S. stocks, U.S. bonds, ETFs, and to hold U.S. dollar assets, not necessarily to buy an on-chain certificate. Only when the compliant brokerage entry point is restricted might some users seek alternative paths, but an alternative path does not equal a natural migration to RWA.

More accurately, compliant brokerages solve the issue of “how users can legally buy real U.S. stocks,” while RWA addresses the question of “whether users can accept an on-chain rights certificate to gain economic exposure to U.S. stocks.” Although they seem similar, the differences are substantial.

Therefore, compliant brokerages do not worry about liquidity, as they do not need to create liquidity themselves but simply connect users to existing markets. RWA must be concerned with liquidity because it needs to remap real market assets, prices, trading, redemption, and clearing onto the blockchain.

In conclusion, brokerages sell compliant access, while RWA (most of the time) sells asset mapping.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。